Trade talk optimism, trade pessimism, drove markets up and down last week. In the end, Presidents of US and China decided to give markets some lip service and boosted stocks towards weekly close. Words, rather than substance, are enough to make investors happy. Yen and Swiss Franc ended as the weakest ones on late rally in stocks. Sterling followed as the third weakest for the week, as Brexit impasse continued. But strong retail sales from UK did give the Pound a mild lift.

On the other hand, commodity currencies made a strong come back. New Zealand Dollar ended as strongest as RBNZ did nothing to endorse market views that next move is a cut. Australian Dollar followed as second with help from the impression that US and China will finally make a trade deal. But the Aussie is set to face a string of tests in RBA minutes, wage price and employment data this week. Canadian Dollar was pulled up to third place by rallying oil prices, with WTI crude oil ended above 56 handle.

US-China trade talks made unknown progress, to be continued in Washington

Specifics were virtually non-existent regarding the week-long US-China trade negotiations in Beijing. But markets nevertheless cheered positive words from both sides. Trump hailed that the talks was “going extremely well” and “we’re a lot closer than we ever were in this country with having a real trade deal”. He even offered that “it would be my honor to remove” the tariffs if they cane make the deal.

On the rumor of 60-day extension to the March 1 trade truce deadline, Trump said “there is a possibility that I will extend the date. But if I do that – if I see that we’re close to a deal or the deal is going in the right direction – I would do that at the same tariffs that we’re charging now, I would not increase the tariffs.”

White House also issued a statement regrading the meetings in Beijing. It’s noted that “These detailed and intensive discussions led to progress between the two parties… Both sides will continue working on all outstanding issues in advance of the March 1, 2019, deadline… United States and Chinese officials have agreed that any commitments will be stated in a Memoranda of Understanding between the two countries.”.

According to a statement published by China Daily, “Both sides reached consensus in principle on major issues and had specific discussions about a memorandum of understanding on bilateral economic and trade issues… The two sides said they will step up their work within the time limit for consultations set by both heads of state, and strive for consensus.”

Now, both team will meet again in Washington this week (starting Feb 18), at both ministerial and vice-ministerial levels. Focus will be on whether they could really deliver a certain MOU.

Fed might stand pat through 2019, or maybe just one hike

The shockingly poor US December retail sales, which released was delayed due to government shutdown, was more than enough to offset the positive impact from higher than expected January inflation reading. Headline sales dropped -1.2% mom while ex-auto sales decreased -1.8%. That was the worse contraction in nine years since 2009. The data prompted Atlanta Fed to slash its Q4 GDP estimate by -1.2% to just 1.5%, less than half of Q3’s 3.4%. Later in the week, New York Fed also halved Q1’s GDP forecast to 1.08%, from 2.17% just a week ago.

Fed officials generally played down the importance of just one month of data. But they’re firmer than ever of their “patient” stance regarding monetary policy. San Francisco Fed President Mary Daly said “the case for a rate increase isn’t there for 2019, if the economy evolves as I just said I expect it to, 2 percent growth, 1.9 percent inflation, no sense that (price pressures are) going up, no sense that we have any acceleration.”

Fed Governor Lael Brainard warned that “downside risks have definitely increased relative to that modal outlook for continued solid growth.” And, on monetary policy, she’s “comfortable waiting and learning” and the current policy is “in a good place”. And, she would weigh “what move, if any, later in the year”. Atlanta Fed President Raphael Bostic though, said his’ outlook for 2019 is “still above trend” at around 2.3 to 2.5% growth. Fed will still likely need to raise interest rates once this year.

Fed fund futures are pricing in 85.3% chance of federal funds rate staying at current 2.25-2.5% after December FOMC meeting, up from 76.0% a week ago, and 72.7% a month ago.

DOW surged on trade optimism, now in key resistance zone

DOW reaccelerated on Friday to close strongly at 25883.25 last week, above 78.6% retracement of 26951.81 to 21712.53. at 25830.60. There is no clear loss of momentum as we expected yet. But our overall view is unchanged that rebound from 21712.53 is a leg in the medium- to long-term corrective pattern from 26951.81. That is, the long term up trend shouldn’t be ready to resume yet.

Thus, we’d still expected overbought condition to limit upside inside 25830.60/26951.81 resistance zone to limit upside. Break of 24883.04 support should indicate completion of the rebound and near term reversal. However, S&P 500 and NASDAQ are kept rather well below equivalent 78.6% fibonacci level at 2813.72 and 7717.47 respectively. Thus as two catch up, there is a chance for DOW to be squeezed through 26951.81 high briefly.

Yield curve flattened further, 10- and 30-year yield at critical support

Meanwhile, market optimism was not quite reflected in treasury yields. 10-year yield lost 2.7 handle again to close at 2.666. 30-year yield also close below 3.0 handle at 2.997. Also, 5-year yield closed at 2.495, below 6-month yield at 2.504. Yield curve continued to flatten between 1-month (2.423) and 5-year, even though it’s not seriously inverted.

Technically, we’re still expect strong support at 38.2% retracement of 1.366 to 3.248 at 2.517 in 10-year yield to bring reversal.

30-year yield should also see strong support from 2.963, which is close to 38.2% retracement of 2.102 to 3.447 at 2.933, to bring sustainable rebound. But let’s see.

Position trading

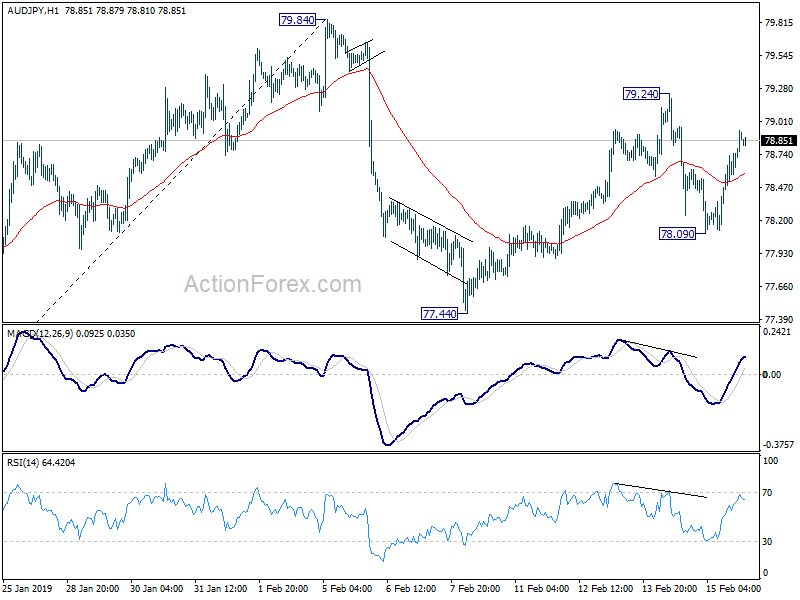

We entered AUD/JPY short at 78.40 last week as last updated here. The rebound to 79.24 was firstly stronger than expected. And sequent fall, which was contained at 78.09 as supported by risk appetite, was also quite disappointing.

Nevertheless, AUD/JPY is, for now, kept by falling 55 day EMA, with daily MACD staying negative. We’re not seeing clear strength in Aussie or weakness in Yen elsewhere. For example, AUD/USD is held below 55 day EMA at 0.7158. EUR/AUD is kept well above 1.5721 short term bottom. GBP/AUD is kept well above 1.7868 support. AUD/CAD is also kept below 55 day EMA at 0.9499. On the other hand, USD/JPY failed to sustain above key fibonacci level at 110.77. EUR/JPY and GBP/JPY are held well below 125.95 and 144.85 highs. CAD/JPY was also rejected by 83.98 resistance last week.

So, we’ll hold short in AUD/JPY, with stop placed at 79.84, with target at 61.8% retracement of 70.27 to 79.84 at 73.92.

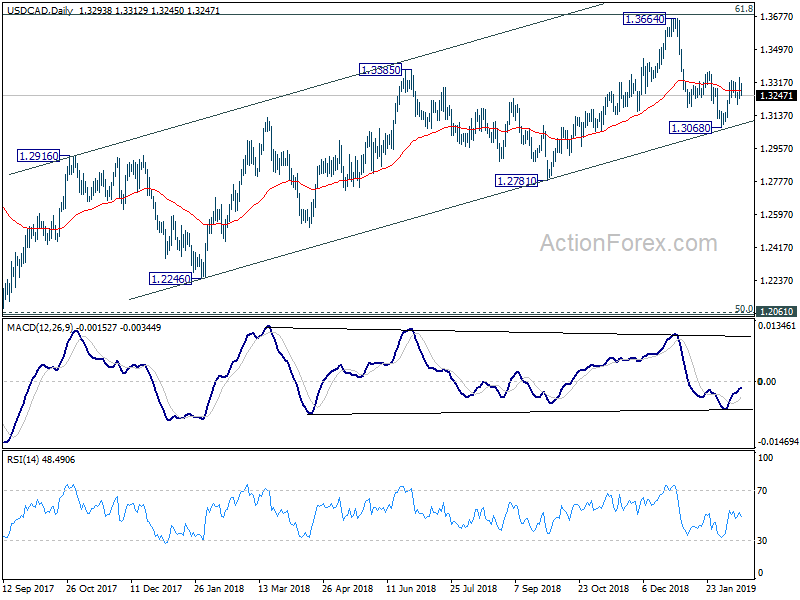

USD/CAD Weekly Outlook

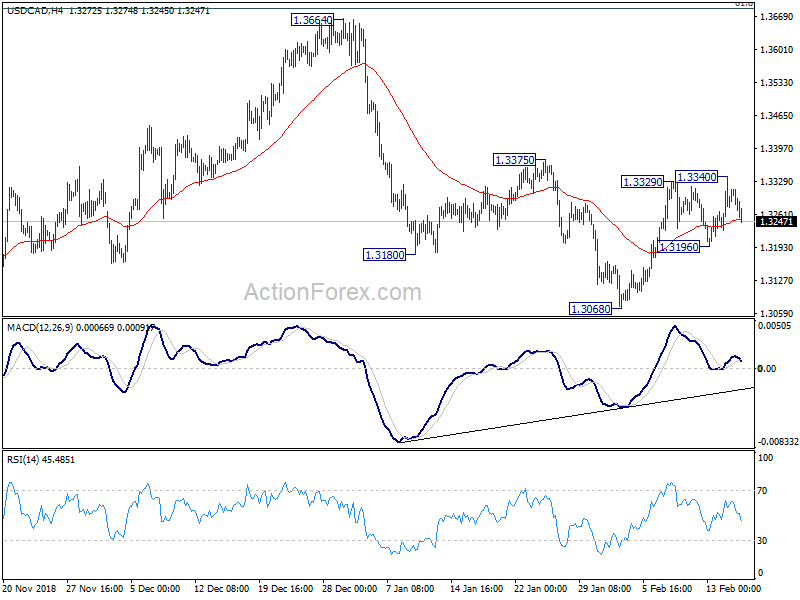

USD/CAD edged higher to 1.3340 last week but failed to break through 1.3375 resistance and retreated. Initial bias remains neutral this week first and some more consolidation could be seen. For now, further rise is in favor as long as 1.3196 minor support holds. We’re favoring the case that decline from 1.3664 has completed with three waves down to 1.3068 already, on bullish convergence condition in 4 hour MACD, just ahead of medium term channel support. Decisive break of 1.3375 resistance will confirm this bullish case and target a test on 1.3664 high. However, break of 1.3196 will now dampen our view and turn bias back to the downside for 1.3068 support instead.

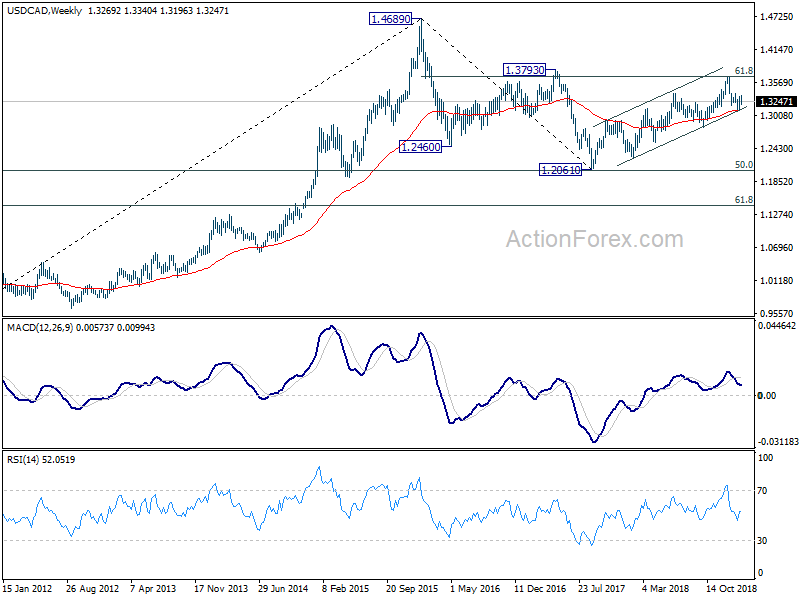

In the bigger picture, structure of the medium term rise from 1.2061 (2017 low) to 1.3664 is not clearly impulsive. Hence, we’d stay cautious on strong resistance from 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 and 1.3793 resistance to limit upside, and bring medium term topping. But in any case, medium term outlook will stay bullish as long as channel support (now at 1.3095) holds. Sustained break of 1.3793 will pave the way to retest 1.4689 (2015 high). Firm break of the channel support should confirm reversal target 1.2061 low again.

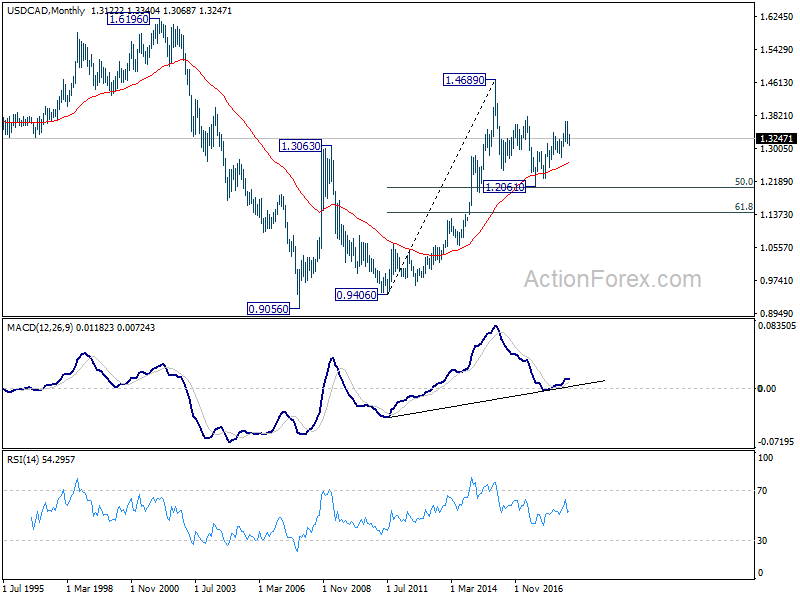

In the longer term picture, corrective fall from 1.4689 (2015 high) should have completed with three waves down to 1.2061, just ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. The development keeps long term up trend from 0.9406 and that from 0.9056 (2007 low) intact. For now, there is still prospect of extending the long term up trend through 1.4689.

{kind=link}