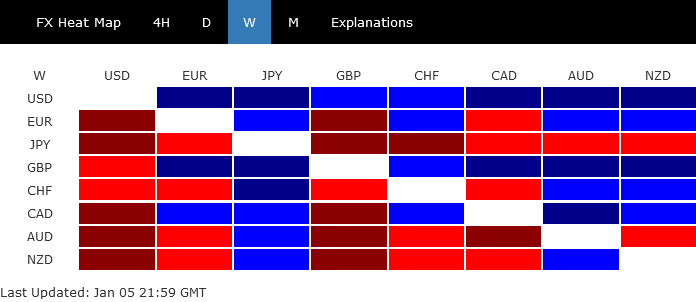

The onset of 2024 marked a notable shift in global market sentiment. Major U.S. stock indexes ended their nine-week winning streak, closing lower, while major benchmark treasury yields experienced a notable recovery. Concurrently, this shift in market dynamics was accompanied by a scaling back of bets on an immediate rate cut by Fed. Amidst these changes, Dollar concluded broadly higher, though it faced conflicting reactions due to mixed economic data. Looking ahead, extended pullback in risk markets and stabilization in yields could potentially bolster the greenback in the near term.

Japanese Yen, on the other hand, ended the week as the worst performer, undoing some of its massive gains from the end of last year. This reversal was primarily driven by the market adjusting its expectations for BoJ policy in the aftermath of the recent devastating earthquake in Japan. Moreover, Yen faced additional pressure due to the rise in treasury yields in other major economies. Australian and New Zealand Dollars also ended the week on a weaker note, affected by broader aversion to risk. Aussie, in particular, was further impacted by extended pullback in Copper prices as well.

Elsewhere in the currency markets, Euro ended the week mixed but softened against British Pound, weighed down by lower-than-expected headline inflation reading. The rebound in inflation seemed not as strong as ECB had anticipated. Meanwhile, Sterling was a standout performer among European majors, while Canadian Dollar ranked as the third strongest. Swiss Franc, despite reaching a new record high against Yen, showed a mixed performance overall.

Yields stabilize and stock pullback could support greenback

Dollar emerged as the strongest major currency last week, although it experienced some jittery on Friday. The robust non-farm payroll data, surprisingly, did not provide lasting momentum for Dollar’s rebound. Instead, traders seemed more influenced by the weaker-than-expected ISM Services PMI. This suggests a shift in market sensitivity, with growth now appearing to be a more critical concern than employment or inflation. The upcoming US CPI release is expected to further clarify this trend.

As for Dollar Index, currently, the favored case is that fall from 107.34 is the second leg of the leg of the consolidation pattern from 99.57. While another fall cannot be ruled out, downside should be contained by 99.57 to bring reversal. On the upside, break of 55 D EMA (now at 103.41) is the first sign that fall from 107.34 has completed. Sustained trading above 104.26 resistance will argue that rise from 100.61 is already the third leg of the pattern and target 107.34.

The pullback in stock markets could be a supporting factor for Dollar in the short term. With last week’s decline, a short term top should be formed at 4793.30 in S&P 500, ahead of 4818.62 (2022 high). The index should have now entered into a consolidation phase to rise from 4103.78. If that is correct, any rally attempt should be capped by 4818.62 key resistance. Risk is mildly on the downside for gyrating towards 55 D EMA (now at 4579.15).

Another element that might bolster the greenback is stabilization in treasury yields. 10-year yield should have formed a short term bottom at 3.785. For the near term, recovery from there should extend towards 55 D EMA (now at 4.206). Strong resistance could be seen from 38.2% retracement of 4.997 to 3.785 at 4.247 to set the range for consolidation to the fall from 4.997.

Earthquake aftermath and BoJ expectations weigh on Yen

Japanese Yen concluded the week as the weakest performer, primarily influenced by the economic repercussions of the recent devastating earthquake. This natural disaster has significantly reduced the probability of BoJ abandoning negative interest rates in the immediate future.

However, this shift represents more of an adjustment in aggressive market bets rather than a complete overhaul of the overall outlook. The consensus remains that BoJ is still on track to normalize its monetary policy within the year, though a rate hike in January can now be ruled out. The general market expectation is still leaning towards April for a rate hike, after with the outcomes of Spring wage negotiations and the availability of a new set of economic forecasts.

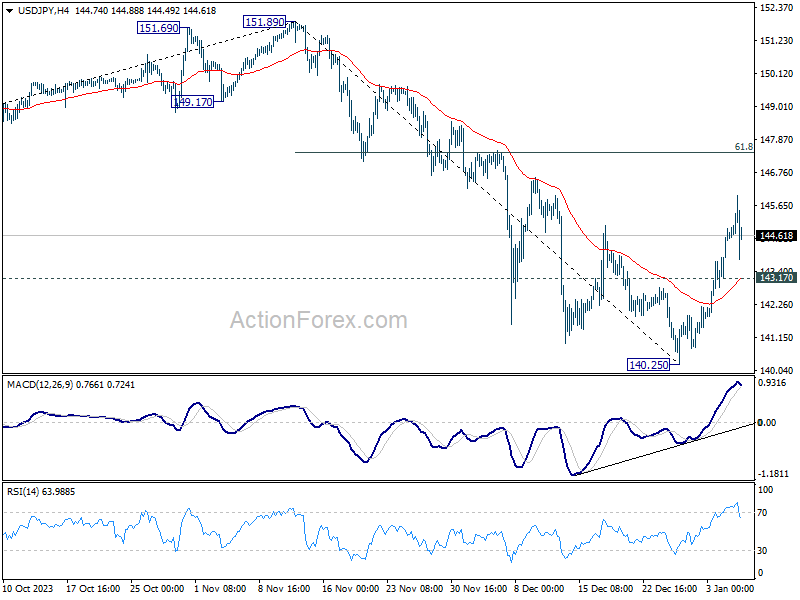

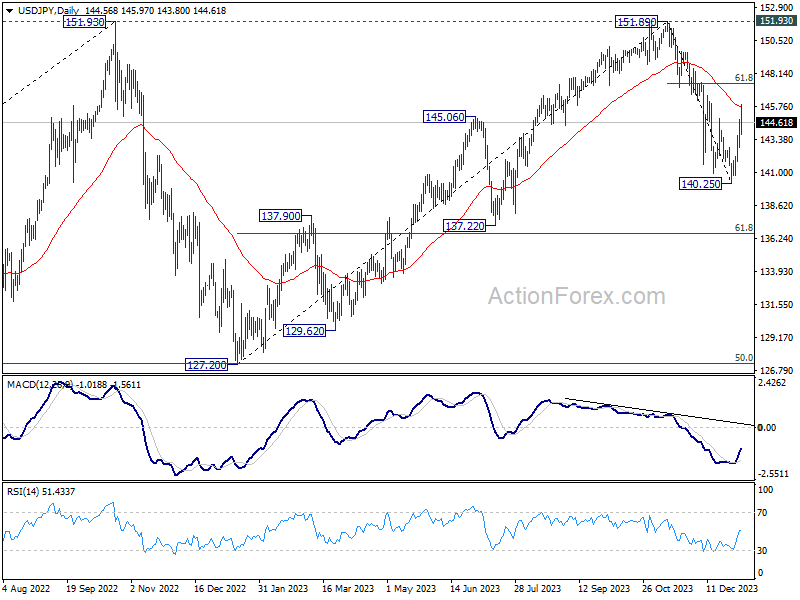

While USD/JPY’s rebound from 140.25 was strong last week, there is no change in the overall outlook. Fall from 151.89 is still seen as the third leg of the pattern from 151.93 (2022 high). Rebound from 140.25 is seen as a correction to fall from 151.89 only. While further rise could be seen in the near term, upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. Break of 143.17 minor support will bring retest of 140.25. However sustained break of 147.44 will dampen this view, and bring retest of 151.89 instead.

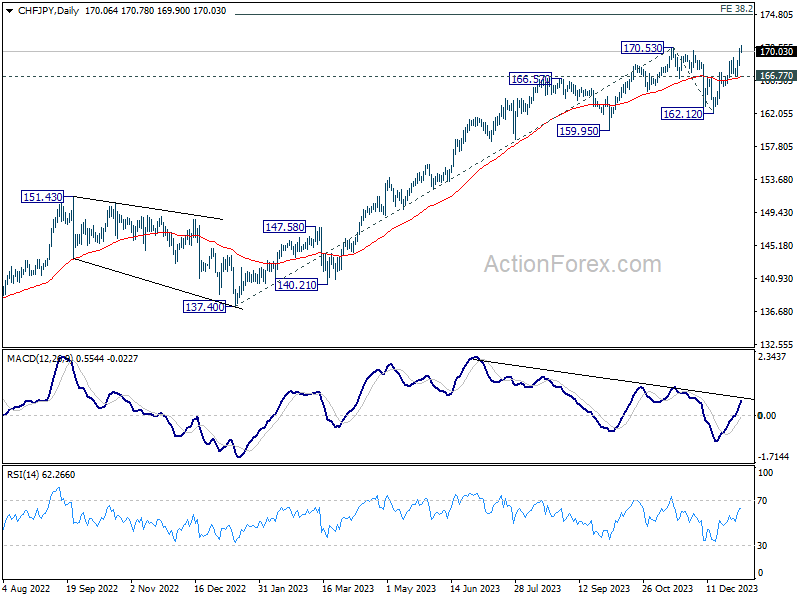

Another interesting development to note is that CHF/JPY made new record high last week, by breaching 170.53, even though it couldn’t close above that level. For now, near term outlook will stay bullish as long as 166.77 support holds. The long term up trend would target 38.2% projection of 137.40 to 170.53 from 162.12 at 174.44 next.

Sterling gains while Aussie struggles, contrasting fortunes

Sterling ended as the second strongest currency, supported by PMI data that suggested resurgence in UK’s services sector., which might help the economy steer clear of recession. Concurrently, there are indications of mounting inflationary pressures, particularly through wages. Pound’s comparative strength against Euro also contributed to the downturn in EUR/GBP, further supporting Sterling’s position.

In contrast, Australian Dollar was the second worst performer, its decline influenced partly by the pullback in risk-sensitive markets. The rebounds in Chinese stocks and Yuan have also been notably underwhelming. Moreover, there is an increasing risk of a near-term bearish reversal in Copper prices, which could have further implications for Aussie’s performance.

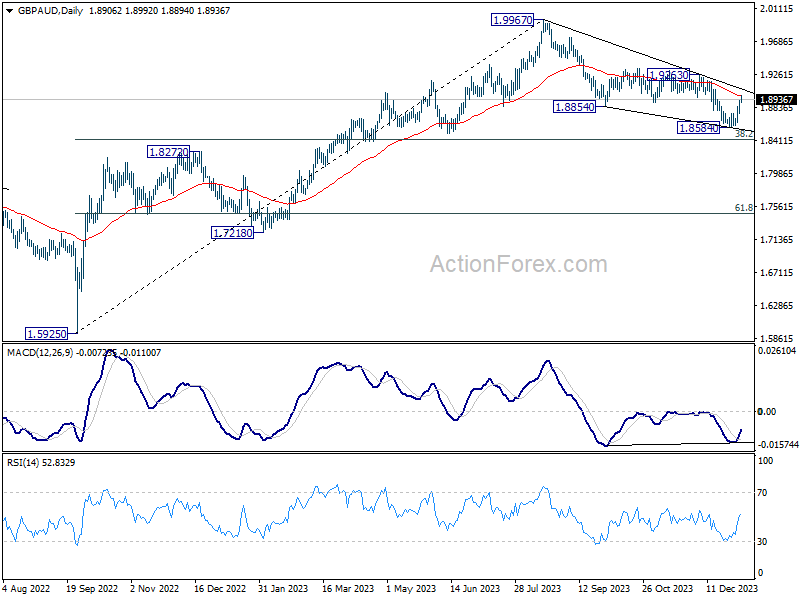

GBP/AUD’s strong rebound suggests short term bottoming at 1.8584. Considering bullish convergence condition in D MACD, correction from 1.9967 might have completed with three waves down to 1.8584, just ahead of 38.2% retracement of 1.5925 (2022 low) to 1.9967 (2023 high) at 1.8423. Firm break of 55 D EMA (now at 1.8992) will strengthen this bullish case and target 1.9263 resistance for confirmation. Nevertheless, rejection by 55 D EMA could bring another fall to 1.8423 before completing the corrective pattern.

Copper’s extended decline from 3.9346 argues that rebound from 3.5021 might have completed, and the corrective pattern from 4.3556 (2023 high) is extending with another falling leg. Immediate focus is on 55 D EMA (now at 3.7688), and sustained trading below there will affirm this bearish case, and pave the way back to 3.5021 support. If realized, this bearish development in Copper would add additional pressure to Aussie.

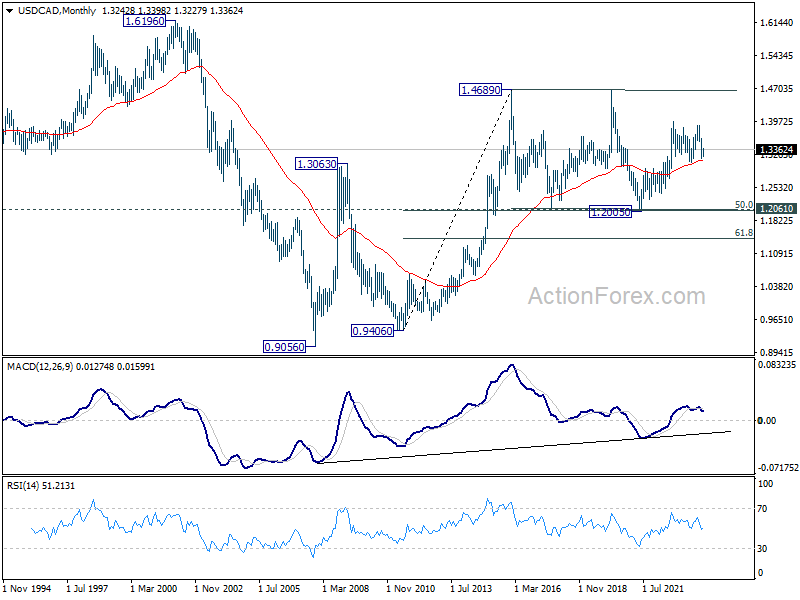

USD/CAD Weekly Outlook

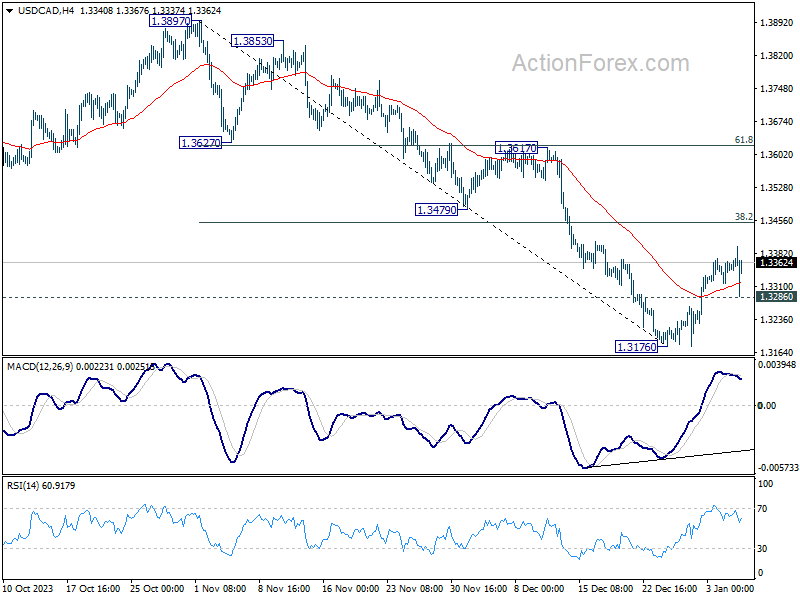

USD/CAD’s strong rebound suggests short term bottoming at 1.3176, on bullish convergence condition in 4H MACD. Despite some loss of upside momentum, further rally is in favor this week as long as 1.3286 minor support holds, to 38.2% retracement of 1.3897 to 1.3176 at 1.3451. Firm break there will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3286 will turn bias back to the downside for 1.3176 low instead.

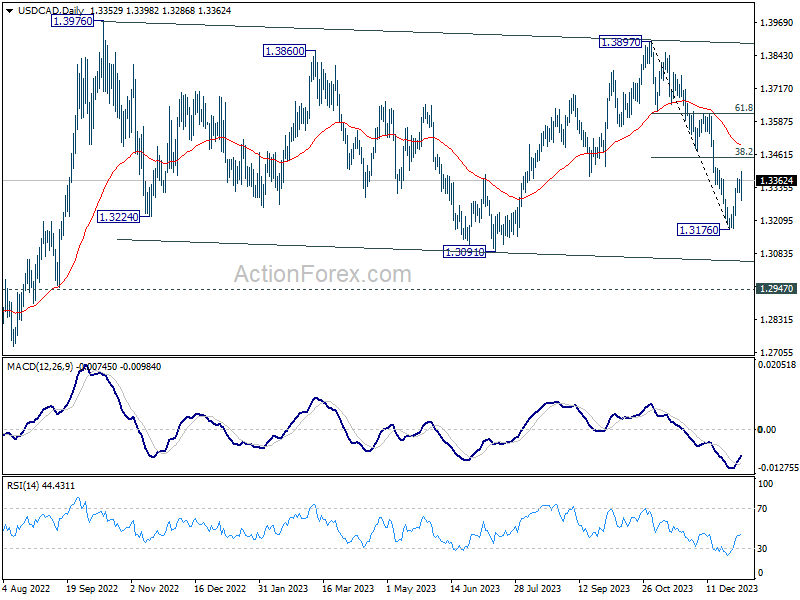

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

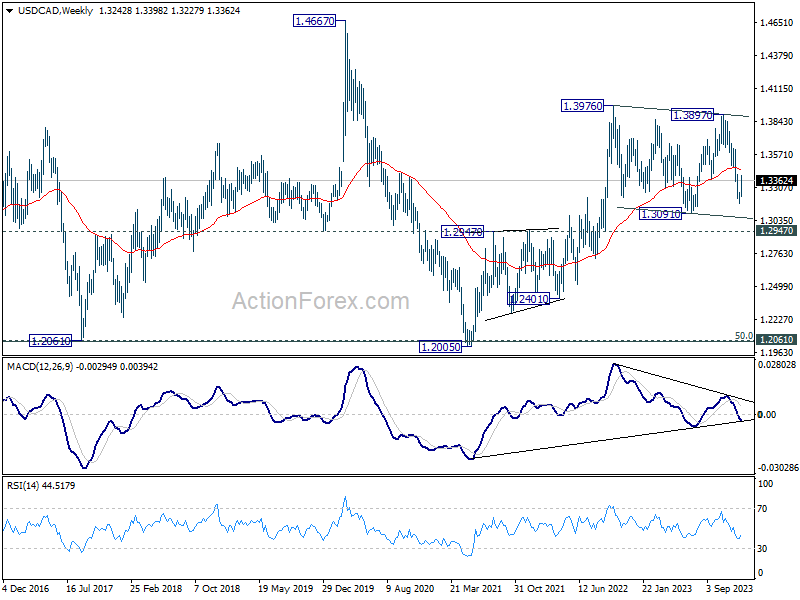

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

{kind=link}