{kind=link}

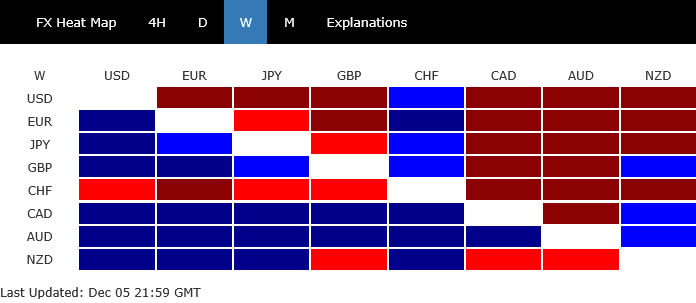

Dollar spent most of the week pinned to the bottom of the performance board, as a steady flow of data reinforced expectations for a Fed rate cut in December. Even though selling pressure eased slightly into Friday—thanks in part to a surprisingly firm rebound in longer-dated Treasury yields—the greenback still struggled to find a foothold.

Risk sentiment improved across major markets, and that shift alone did much of the heavy lifting. The notable underperformance of the Swiss Franc highlighted the change in tone, with safe-haven demand fading while yields elsewhere climbed. Euro was also heavy.

Against that backdrop, the outperformers told their own story. Aussie surged to the top of the weekly rankings as traders began to position for the possibility of an RBA hike in 2026. Governor Michele Bullock’s message to the parliament—signaling that policymakers may need to pivot back toward tightening if inflation re-accelerates—gave markets a narrative they were quick to embrace.

Canada’s Dollar was not far behind, propelled by another impressive labor-market beat that further cemented expectations for the BoC to hold rates unchanged through 2026. Sterling also benefited from persistent optimism following the well-received Autumn Budget, helping it round out the top three.

Yen and Kiwi held the middle ground but for very different reasons. In Japan, rising expectations for a December BoJ rate hike were tempered by stronger global risk appetite. For Kiwi, the tone was firm but restrained, with investors largely respecting the RBNZ’s hawkish hold last month, without chasing the move.

US Stocks Hold Their Nerve, but Santa Needs More Data

Whether US equities are entering a genuine Santa Claus rally remains an open question, but last week’s performance at least showed that dip buyers are still very much alive. The brief pullback in mid-November was swiftly absorbed, with major indexes defending near-term technical supports and re-establishing upward momentum. That resilience alone keeps the year-end rally narrative on the table.

Still, the conviction behind the move is less than overwhelming. Many investors are reluctant to chase the highs given the sheer volume of event risk ahead. Markets have already fully priced in a Fed rate cut this month, and incoming data last week largely validated that view. What remains uncertain is the path beyond December, and that lack of clarity is holding sentiment in check.

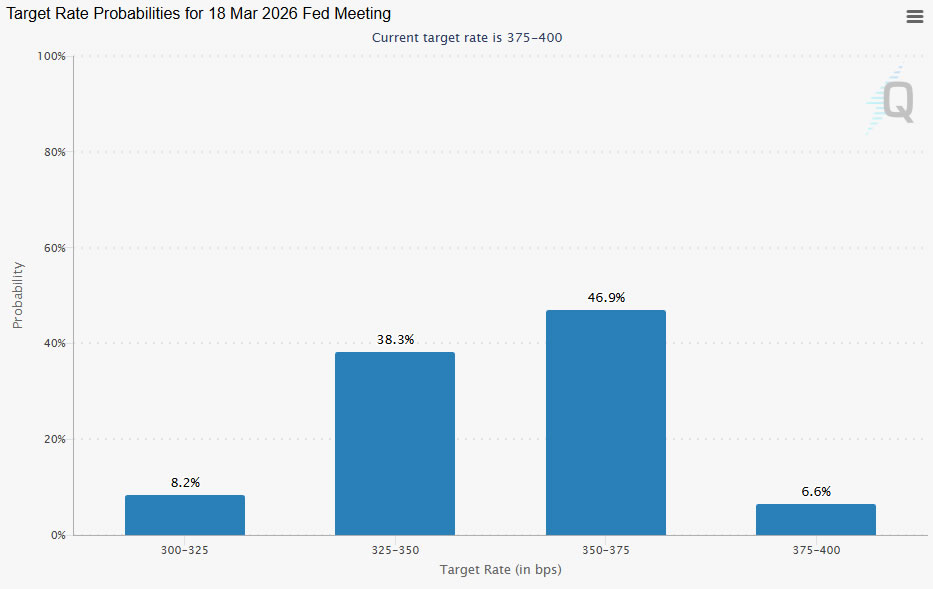

The next two weeks could change that. The December 10 FOMC meeting is clearly a consequential one—not because of the cut itself, which markets assume—but because of the updated economic projections and the new dot plot. These will effectively set the tone for how aggressively the Fed expects to—or is willing to—ease through early 2026.

In parallel, the following week’s heavy-weight data—NFP and CPI—will give markets a more concrete read on whether pricing pressures are merely stabilizing at a still-elevated level, and whether the deterioration of job market is already in the rear mirror. For equities, “bad news is good news” still applies, but only up to a point. Softer data would strengthen the case for earlier or deeper Fed cuts, thereby supporting valuations.

Fed fund futures, meanwhile, reflects a lot of uncertainty. The odds of another 25bps cut by March sit just under 50%, essentially a coin toss. That pricing highlights how divided the market is on whether the Fed pauses in Q1 or continues easing. Until that gap closes one way or the other, equities could remain reactive rather than directional.

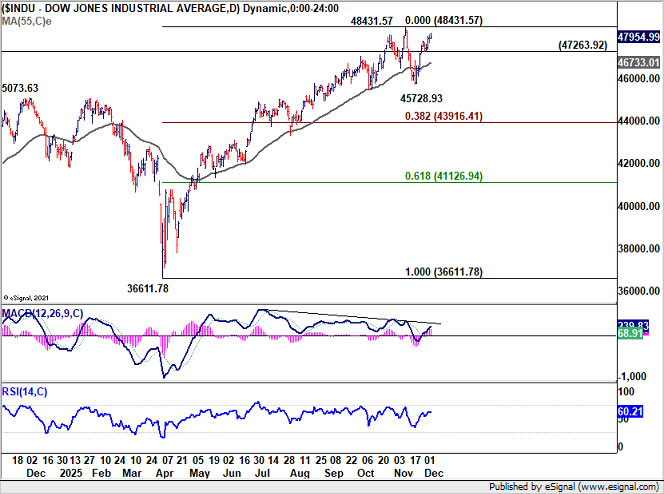

Technically, for DOW, break of 48,431.57 will resume the long term up trend to 78.6% projection of 28,660.94 to 45,701.29 from 36,611.78 at 49,510.32, or even further to 50k psychological level in the near term. However, on the downside, break of 47,263.92 support will suggest that corrective pattern from 48,431.57 has started a third leg, and would target 47,528.93 support again.

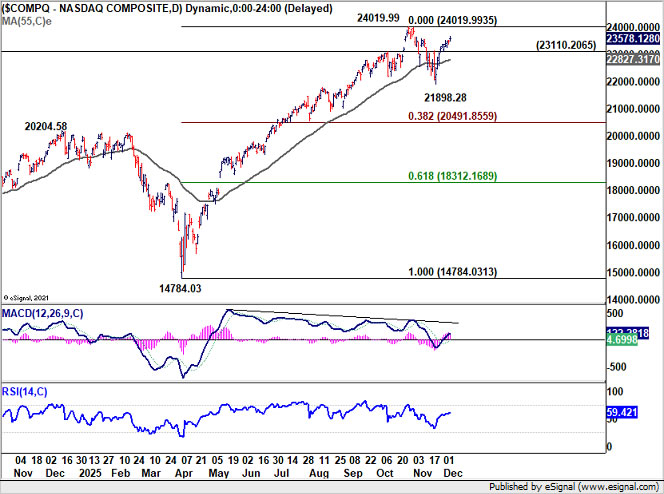

Similarly, break of 24,019.99 will resume NASDAQ’s up trend to 100% projection of 10,088.82 to 20,204.58 from 14,784.03 at 24,899.78. However, on the downside, break of 23,110.20 support will extend the corrective pattern from 24,019.99 with another falling leg to 21,898.28 support again.

So the question remains: will Santa deliver? The answer hinges on whether next week’s Fed projections and the following week’s CPI/NFP releases provide markets with the confidence they currently lack. Until then, optimism is warranted—but caution still rules the edges of the rally.

Yields Surge on Fears of a Politicized Fed; Dollar Struggles to Keep Up

US Treasury yields displayed far more resilience last week than many had expected. Instead of extending the slide toward October low of 3.947, the 10-year yield reversed and closed firmly at 4.139. Part of that rebound reflects improved risk appetite globally, as investors rotated out of safety and back into equities. But that alone does not fully explain the recovery, given the market’s growing conviction that the Fed will cut rates next week.

A deeper driver may be emerging: the market is beginning to price in a wider range of political and policy outcomes for 2026. The looming transition at the Fed has injected some unmistakable uncertainty that extends beyond the typical macro data cycle. Chair Jerome Powell’s term ends next year, and reports increasingly suggest that President Donald Trump intends to appoint his top economic adviser Kevin Hassett as the next Fed chief.

Hassett is widely perceived as a strong monetary dove, and the prospect of a Fed leadership more aligned with the White House introduces non-trivial risks for bond markets. Investors fear that a politically influenced Fed could lean too heavily into easing—even in an environment where inflation remains above target—potentially setting the stage for a renewed inflation cycle.

That anxiety may explain why longer-dated yields are refusing to break lower despite softer labor market signals. The bond market is effectively hedging against the possibility that the Fed’s medium-term reaction function becomes less restrictive and less focused on price stability. In other words, yields are reacting not just to economic data, but to institutional risk.

A further wrinkle is the idea that Hassett could operate as a “shadow Fed chair” in the months before formally taking office. Markets fear that his comments—rather than Powell’s—may become the unofficial guide for rate-expectation pricing. That would add volatility to an already delicate policy transition.

Against this backdrop, Dollar remains soft but not outright collapsing. Most of the weakness last week stemmed from improving global risk sentiment rather than any direct Fed repricing. Dollar selloff against European majors has slowed towards the end of the week, while yield support offers a partial offset. Still, the greenback retains a heavy tone as long as political uncertainty lingers.

Technically, 10-year yield may be completing a head-and-shoulders bottoming formation (ls 3.992; h: 3.947; rs: 3.988). Break of 4.162 will complete the pattern and be the first important sign of bullish trend reversal.

Nevertheless, the much more important hurdle lies in 4.2 cluster resistance level, with 4.200 resistance as well as 38.2% retracement of 4.629 to 3.947 at 4.207. As long as this level holds, outlook for 10-year yield will stay neutral at best.

However, firm break of 4.2 could easily push 10-year yield to 61.8% retracement at 4.368 and above. And that could be a strong indication of some serious underlying repricing.

Dollar Index gyrated lower last week to close at 98.99. The break of 55 D EMA (now at 99.13) argues that rebound from 96.21 might have completed at 100.39 already.

Deeper fall is now in favor to 98.03 support. Decisive break there will confirm this bearish case, and bring retest of 96.21 low.

In case of another rise, strong resistance is still expected from 38.2% retracement of 110.17 to 96.21 at 101.54 to limit upside.

Markets Flip Toward RBA Tightening—Aussie Extends Gains, Loonie Strengthens Too

Commodity currencies finished last week as clear outperformers, buoyed by firmer risk sentiment and strong domestic catalysts. Aussie led the major currencies, reflecting a dramatic shift in how markets now view next year’s RBA policy path. What only recently looked like a debate between “cut or hold” has quickly evolved into early pricing of outright tightening.

The turnaround in expectations has been striking. Just two weeks ago, traders were split on whether the RBA might cut rates by May. But with inflation showing signs of re-accelerating, and national accounts revealing an economy gaining momentum into year-end despite the headline miss. Markets have swung decisively toward the view that the RBA will need to tighten, not ease, in 2026.

Household spending and private demand were firmer than anticipated, reinforcing concerns that underlying inflation pressure may not fade as quickly as policymakers hoped, or even re-emerge. That was enough for investors to conclude that rate cuts are effectively off the table, while the risk of multiple hikes is now starting to be priced in from February onward.

Loonie also impressed, albeit through a very different catalyst. The late-week surge stemmed from another strong jobs report, marking the third consecutive upside surprise. November’s employment gains and the sharp drop in unemployment signal that the economy is finally moving past the drag created by earlier US tariff distortions.

For the BoC, the message is now crystal clear: the easing cycle is over. After delivering 275bps of cuts—one of the largest cycles among major central banks—the BoC signaled in October that policy was already near the lower bound of neutral. The latest labor-market data cement expectations that rates will remain on hold until at least 2027 unless growth deteriorates sharply.

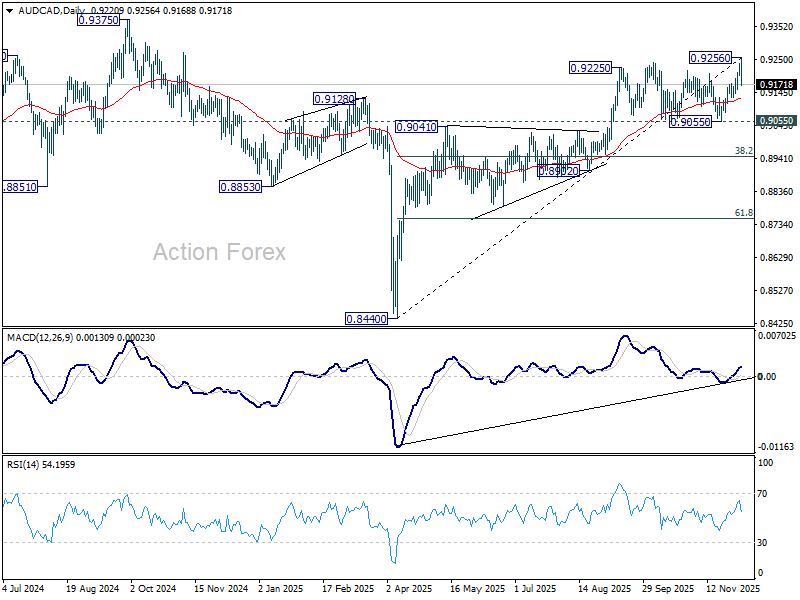

Despite the solid macro backdrop for both currencies, AUD/CAD price action reflects a market pausing for breath. The cross briefly edged to 0.9256 before reversing sharply, hinting that a short-term top is already in place. Profit-taking near major resistance added to the pullback.

In the near term, consolidation looks more likely than continuation. A deeper dip toward the 55-day EMA at 0.9127 is possible, particularly if risk appetite wobbles or if investors reassess the pace of RBA tightening. A break of the EMA would not alter the broader trend but would reinforce the view that the pair needs more time to establish a base.

Bigger-picture momentum, however, remains constructive. As long as 0.9055 support holds, the rise from the 2025 low at 0.8440 remains intact, and another leg higher is favoured at a later stage. The timing—and strength—of that move will depend on how aggressively markets lean into RBA hike expectations in early 2026.

Only a firm break of 0.9055 would suggest that AUD/CAD is no longer trending, opening a deeper pullback toward the 38.2% retracement of 0.8440 to 0.9256 at 0.8944. Until then, dips remain part of a broader bullish structure anchored by relative central-bank divergence.

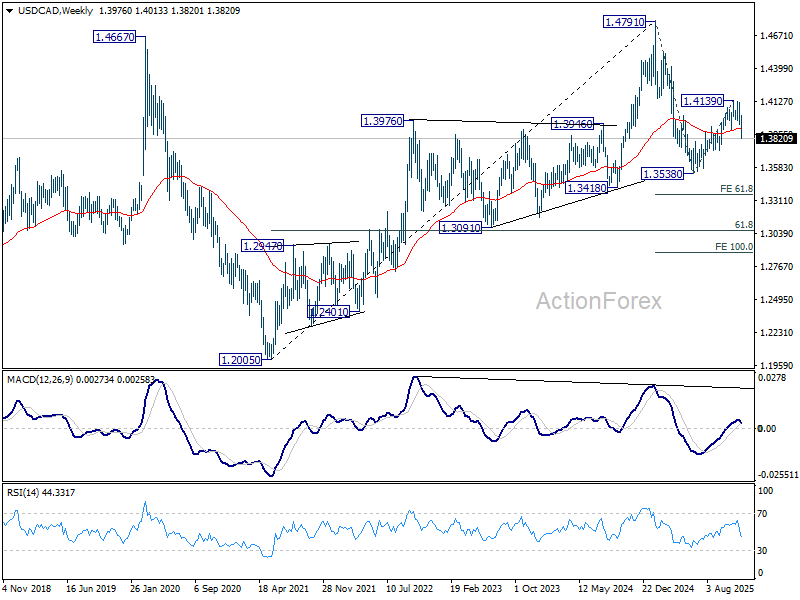

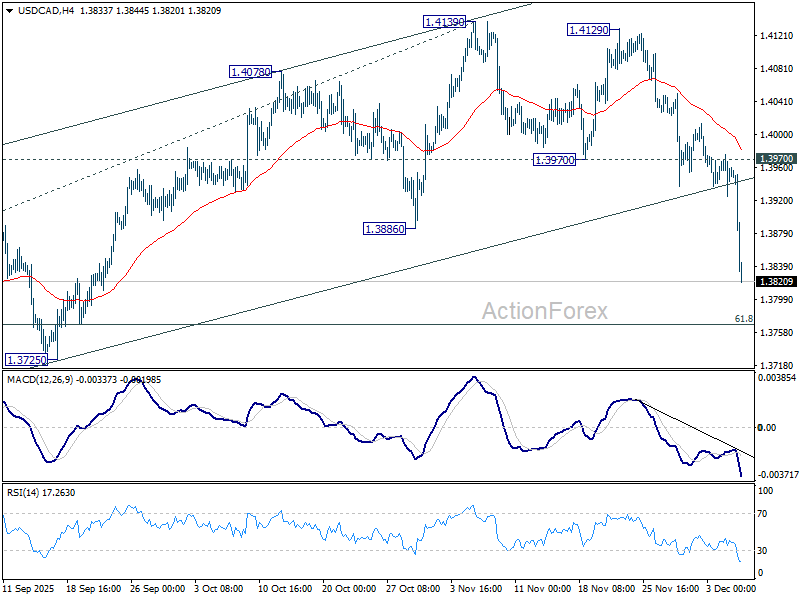

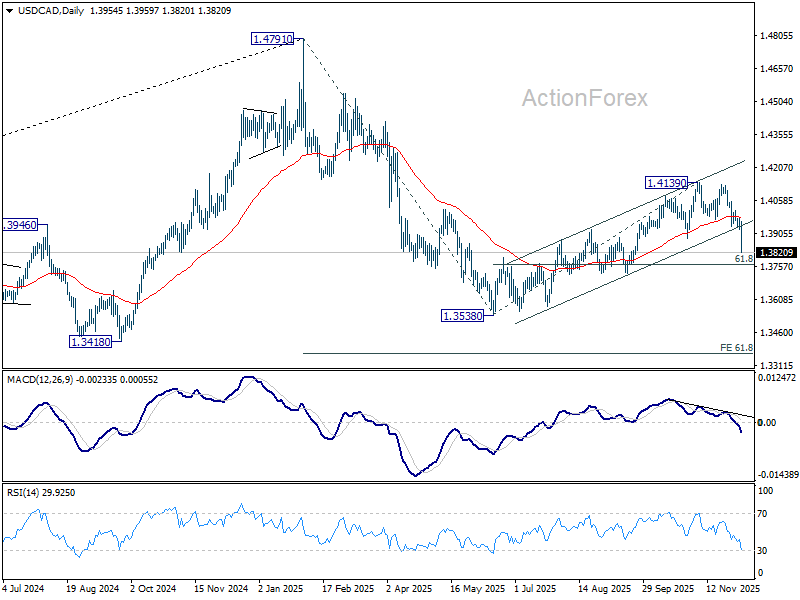

USD/CAD Weekly Outlook

USD/CAD’s steep decline last week suggests that rise from 1.3538 has already completed at 1.4139. Initial bias remains on the downside this week for 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low. For now, risk will stay on the downside as long as 1.3970 support turned resistance holds, in case of recovery.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it’s just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

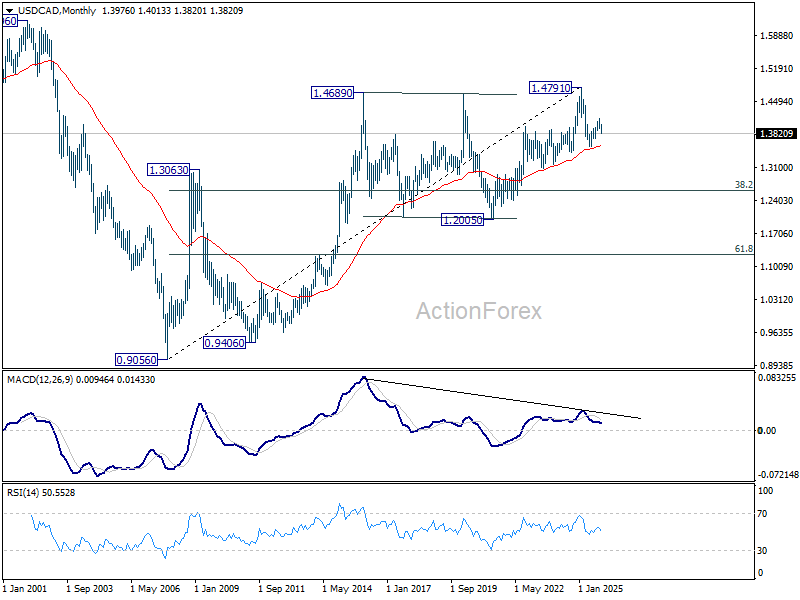

In the long term picture, rising 55 M EMA (now at 1.3567) remains intact. Thus, up trend from 0.9056 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction. to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.