Live Comments

Canada Jobs Surge 75K as Unemployment Falls to Two-Year Low

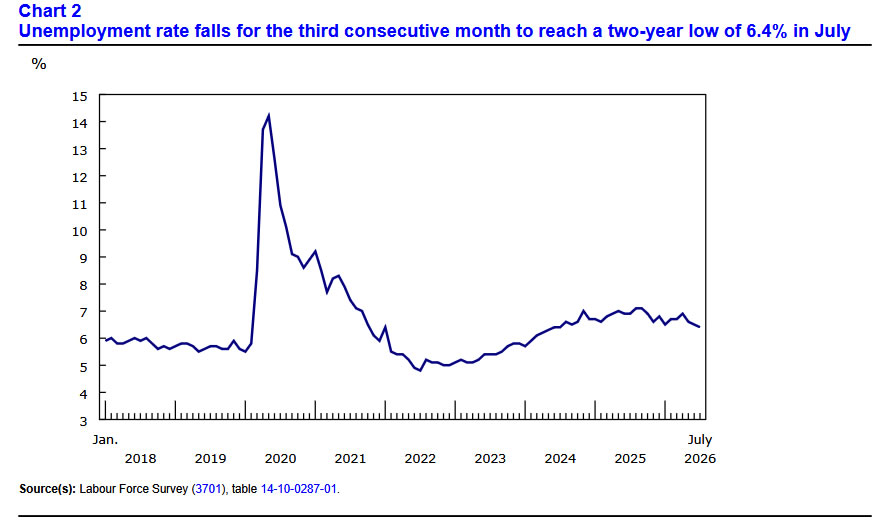

Canada's labor market delivered a strong upside surprise in July, with employment rising 75.1K, far above expectations of 17.8K and accelerating sharply from 18.2K in June. Employment rate edged up 0.1 percentage point to 60.9%, while unemployment rate unexpectedly fell from 6.5% to 6.4%, against expectations for no change. That was lowest unemployment rate since July 2024 and marked third consecutive monthly decline, with rate now down 0.5 percentage point since April.

Job gains were also spread across several important private-sector industries. Wholesale and retail trade added 21K positions, finance, insurance, real estate, rental and leasing gained 18K, professional, scientific and technical services added 17K, while construction employment increased 16K. Those gains were partly offset by declines of -15K in public administration and -9.6K in agriculture.

Wage pressures nevertheless continued to cool, with average hourly earnings growth slowing from 3.3% to 2.8% yoy.

Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Employment Change | +75.1K | +17.8K | +18.2K |

| Unemployment Rate | 6.4% | 6.5% | 6.5% |

| Employment Rate | 60.9% | — | 60.8% |

| Average Hourly Wages y/y | +2.8% | — | +3.3% |

Key Takeaways

- Canada added 75.1K jobs in July, more than four times expectations of 17.8K and sharply above June's 18.2K increase.

- Unemployment rate fell from 6.5% to 6.4%, reaching lowest level since July 2024. It has now declined for three consecutive months and by 0.5 percentage point since April.

- Employment rate increased from 60.8% to 60.9%, reinforcing strength of headline employment gain.

- Job creation was relatively broad, led by wholesale and retail trade (+21K), finance and real estate-related industries (+18K), professional and technical services (+17K), and construction (+16K).

- Public administration shed 15K jobs and agriculture lost 9.6K, providing some offset to private-sector strength.

- Wage pressures continued to moderate despite stronger hiring. Average hourly wage growth slowed from 3.3% to 2.8% y/y.

US Non-Farm Payrolls Contract -23k. Revisions Expose Deeper Labor Market Weakness

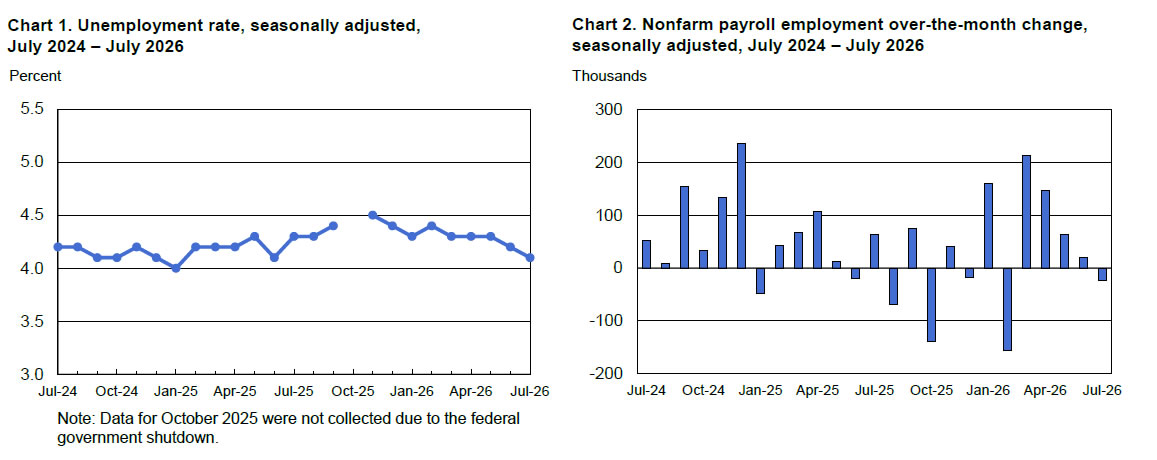

US labor market delivered a major downside surprise in July, with nonfarm payrolls falling -23K, far below expectations for an 85K increase. Weak headline was compounded by another round of substantial downward revisions: May payroll growth was cut from 129K to 63K, while June was revised from 57K to just 20K, leaving combined employment gains 103K lower than previously reported. July weakness was concentrated in local government education and retail trade, while health-care employment continued to trend higher. Taken together, latest figures suggest deterioration in hiring is considerably more pronounced than earlier estimates indicated.

Other parts of report were mixed, but did little to offset payroll disappointment. Unemployment rate unexpectedly fell from 4.2% to 4.1%, versus expectations for no change. But decline came alongside another drop in labor force participation from 61.5% to 61.4%. Participation has now fallen 0.7 percentage point since January, while employment-population ratio has declined 0.5 point over same period.

Meanwhile, average hourly earnings growth slowed sharply from 0.3% to 0.1% mom, missing expectations of 0.3%. Combination of weaker hiring, declining participation and softer wage growth paints a considerably less reassuring picture than lower unemployment rate alone would suggest.

Report should substantially raise hurdle for Fed to hike rates in September. This week's employment indicators had already sent conflicting signals, with weak ADP hiring and contracting ISM Services Employment offset by stronger manufacturing employment and historically low jobless claims. NFP now tilts balance decisively toward labor-market weakness, while softer wage growth reduces one source of inflation concern.

Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Nonfarm Payrolls | -23K | +85K | +20K |

| Unemployment Rate | 4.1% | 4.2% | 4.2% |

| Average Hourly Earnings m/m | +0.1% | +0.3% | +0.3% |

| Labor Force Participation Rate | 61.4% | — | 61.5% |

| May–June Combined Revision | -103K | — | — |

Key Takeaways

- Nonfarm payrolls unexpectedly fell 23K in July, badly missing expectations for an 85K increase and marking outright employment contraction.

- Weakness extended well beyond July. May was revised down from +129K to +63K and June from +57K to +20K, cutting previously reported employment growth by 103K combined.

- Unemployment rate unexpectedly fell from 4.2% to 4.1%, but this was accompanied by a decline in labor force participation from 61.5% to 61.4%.

- Labor force participation has now fallen 0.7 percentage point since January, while employment-population ratio has declined 0.5 point, making lower unemployment rate less reassuring.

- Average hourly earnings slowed from 0.3% to 0.1% mom, well below expectations of 0.3%, adding evidence that labor-related inflation pressure is easing.

- Employment declined in local government education and retail trade, while health-care employment continued to trend higher.

- Report significantly raises hurdle for a September Fed hike. Negative payroll growth, large downward revisions and softer wages challenge hawkish argument that labor market remains strong enough to comfortably absorb further tightening.

China Exports Rise 23.9% YoY as High-Tech Demand Defies Tariffs

China's exports remained a major source of economic strength in July, supported by booming global demand for high-tech products even as growth moderated from June's rapid pace. Exports rose 23.9% yoy in US dollar terms, slowing from 27.0% but beating expectations of 22.2%. Imports also remained strong, though growth eased from 36.0% to 27.5%, broadly matching forecasts. Trade surplus consequently narrowed from $125.6B to $112.5B, but still exceeded expectations of around $107B.

High-tech manufacturing continued to drive export performance. Semiconductor exports nearly doubled in value over first seven months of year, while overall high-tech exports surged 40.7%. Chip exports alone jumped 117% yoy in July, while cars, electric vehicles, batteries and other advanced manufacturing products also recorded strong overseas demand. But strength was increasingly uneven: ceramic exports plunged 28.3% and toy shipments fell 9.7%, highlighting widening divergence between advanced manufacturers benefiting from global AI and electrification investment and traditional industries facing much softer demand.

Trade with US also remained resilient, with Chinese exports rising 17% yoy in July, accelerating from around 14% in June. However, part of that strength likely reflected exporters front-loading shipments ahead of higher US tariffs, raising questions over whether current growth can be sustained. Exports to EU increased 16%, providing another source of external support. With domestic consumption and investment still subdued, exports remain crucial to China's growth outlook, but increasing dependence on high-tech demand and escalating trade barriers leave external sector exposed to both global technology cycle and further protectionist measures.

Data Summary

| Indicator | July 2026 | Expected |

|---|---|---|

| Exports (yoy, USD) | +23.9% | +22.2% |

| Imports (yoy, USD) | +27.5% | +27.9% |

| Trade Surplus | $112.5B | $107B |

| Exports to US (yoy) | +17.0% | — |

| Exports to EU (yoy) | +16.0% | — |

| High-Tech Exports (Jan–Jul, yoy) | +40.7% | — |

| Semiconductor Exports (Jan–Jul, value) | Nearly +100% | — |

| Chip Exports (July, yoy) | +117% | — |

Key Takeaways

- China's exports grew 23.9% yoy in July, slowing from 27.0% in June but comfortably beating expectations of 22.2%. External demand remains an important support for economy amid subdued domestic consumption and investment.

- Imports increased 27.5% yoy, down from 36.0% in June and broadly matching expectations, while trade surplus narrowed from $125.6B to $112.5B.

- AI and advanced manufacturing remain major engines of export growth. High-tech exports surged 40.7% during first seven months of 2026, while semiconductor exports nearly doubled in value.

- July chip exports surged 117% yoy, while auto exports increased by more than 50%, highlighting strength in sectors benefiting from global AI infrastructure spending and China's advanced manufacturing expansion.

- Performance remains uneven. Ceramic exports fell 28.3% and toy exports dropped 9.7%, showing traditional industries are not sharing equally in export boom.

- Exports to US accelerated to 17% yoy, but some strength likely reflected front-loading ahead of higher US tariffs, making it harder to extrapolate July's pace into coming months.

- Overall, trade data remain supportive for China's growth, but increasing reliance on high-tech exports and mounting protectionism create risks for sustainability of export-led momentum.