Live Comments

Eurozone Sentix Confidence Turns Positive, but Inflation Concerns Return

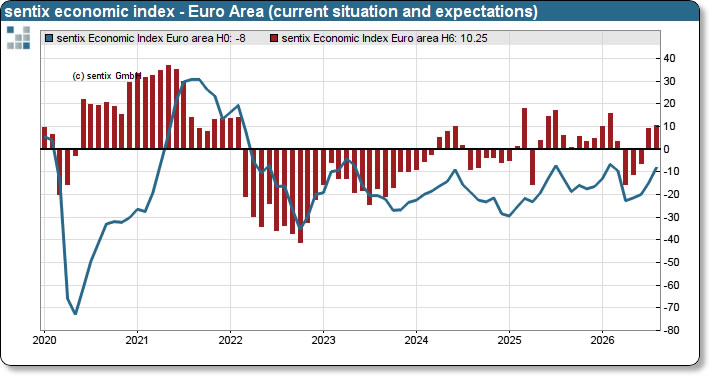

Eurozone investor confidence improved for a fourth straight month in August, reinforcing signs that sentiment is recovering alongside firmer economic data. Sentix Overall Index rose from -3.1 to 0.9, beating expectations of -1.3 and reaching highest level since February. Current Situation improved from -14.8 to -8.0, while Expectations edged up from 9.3 to 10.3. Sentix linked improvement to stronger-than-expected Q2 growth, recovering industrial production and confidence indicators, rising investment and government spending, as well as partial absorption of confidence shock from Iran war. Still, high energy costs and subdued order books continue to constrain recovery.

Improving growth picture is being accompanied by renewed inflation concern. Sentix Inflation Barometer deteriorated sharply from -13.75 to -29.25, indicating investors are again becoming more worried about price pressures after previous month’s improvement, although concern remains below extremes seen during height of Iran conflict. ECB Policy Barometer likewise fell from -8.25 to -15.25, showing markets expect a more restrictive policy environment. Combination of stronger activity and renewed inflation risks therefore argues against an early monetary-policy “all-clear.”

Germany showed a similar but more fragile improvement. Sentix Overall Index rose for a third month from -19.4 to -11.9, while Current Situation jumped from -39.8 to -28.3 and Expectations improved from 3.5 to 6.0. Recent 0.2% Q2 growth and firmer ifo confidence support stabilization case, but deeply negative current-condition reading shows underlying economy is still weak.

For ECB, broader message is two-sided: growth fears are easing just as inflation concerns are rebuilding, reducing urgency for a more accommodative policy turn.

Data Summary

Euro Area Sentix Investor Confidence

| Component | Current | Previous | Trend |

|---|---|---|---|

| Overall Index | 0.9 | -3.1 | Improved |

| Current Situation | -8.0 | -14.8 | Improved |

| Expectations | 10.3 | 9.3 | Improved |

Germany Sentix Investor Confidence

| Component | Current | Previous | Trend |

|---|---|---|---|

| Overall Index | -11.9 | -19.4 | Improved |

| Current Situation | -28.3 | -39.8 | Improved |

| Expectations | 6.0 | 3.5 | Improved |

Key Takeaways

- Eurozone Sentix Overall Index improved from -3.1 to 0.9 in August, marking a fourth consecutive monthly rise and highest level since February.

- Current Situation also strengthened from -14.8 to -8.0, while Expectations edged higher from 9.3 to 10.3, showing recovery is becoming broader but still led by forward-looking optimism.

- Sentix cited stronger Q2 growth, improving industrial production and confidence indicators, rising investment and government spending, and partial absorption of Iran-war confidence shock.

- Inflation concerns resurfaced sharply, with Sentix Inflation Barometer falling from -13.75 to -29.25, while Central Bank Policy Barometer weakened from -8.25 to -15.25.

- That combination of better growth and renewed inflation concern argues against an early monetary-policy “all-clear” from ECB.

- Germany also improved for a third consecutive month, but Current Situation at -28.3 still points to weak underlying conditions despite better expectations.

BoJ Opinions: Inflation Mission Changed to Preventing Inflation Overshoot

BoJ’s Summary of Opinions from July 30–31 meeting points to an important shift in policy thinking: debate is moving away from how to lift underlying inflation toward 2% and increasingly toward how to stop it from overshooting. One opinion captured change explicitly, saying focus of monetary policy has shifted from “lifting underlying CPI inflation to 2 percent” to “avoiding further upward deviation in underlying CPI inflation.” That does not mean immediate tightening is automatic, but it suggests reaction function is becoming more sensitive to upside inflation risks.

Case for holding policy steady in July rested largely on transmission lags rather than diminishing appetite for normalization. One member estimated that rate hikes take roughly one to one and a half years to weigh on inflation and economic activity, arguing that BoJ should first assess impact of previous increase. Yet several opinions simultaneously stressed that underlying CPI inflation is approaching, or becoming anchored around, 2%, while financial conditions remain accommodative. On that basis, members argued it remains appropriate to continue raising policy rate and reducing monetary accommodation as conditions warrant.

More hawkish part of discussion concerned pace and size of future hikes. One opinion said tightening could proceed “faster than market expectations” if economic activity, prices and financial conditions justify it. Another argued global environment has entered “a new phase” in which BoJ should respond more nimbly to overseas financial conditions and discuss size of a rate hike rather than adhering to a predetermined pace. Most forceful warning was that waiting carries its own risk: if inflation overshoots, BoJ could later be forced into “rapid and substantial” hikes, delivering what member described as a “double shock” to economy and households.

BoJ therefore appears to be moving from normalization driven by confidence in reflation toward normalization increasingly shaped by risk management against excessive inflation. Middle East developments, expansion in AI-related demand, foreign-exchange moves and rising medium- to long-term inflation expectations were all cited as factors requiring close attention. July hold should therefore not be read as retreat from tightening. If upside price risks strengthen while activity holds up, debate may shift quickly from whether BoJ hikes again to how fast — and by how much — it should move.

Key Takeaways

- BoJ’s policy debate is shifting from creating durable 2% inflation toward preventing inflation from overshooting.

- July hold reflected desire to assess lagged effects of previous hike, with one opinion estimating transmission takes around one to one and a half years.

- Several members still judged financial conditions accommodative and argued BoJ should continue raising policy rate as underlying CPI approaches 2%.

- One opinion warned pace of hikes could become “faster than market expectations” if economic activity, prices and financial conditions justify it.

- Debate is also broadening from timing to size of future hikes, with one member saying BoJ has entered a “new phase” requiring more nimble policy.

- Strongest hawkish argument was that waiting too long could force rapid and substantial hikes later, creating a “double shock” for economy and households.

- Middle East developments, AI-related demand, foreign-exchange moves and rising medium- to long-term inflation expectations are key upside risks to watch.

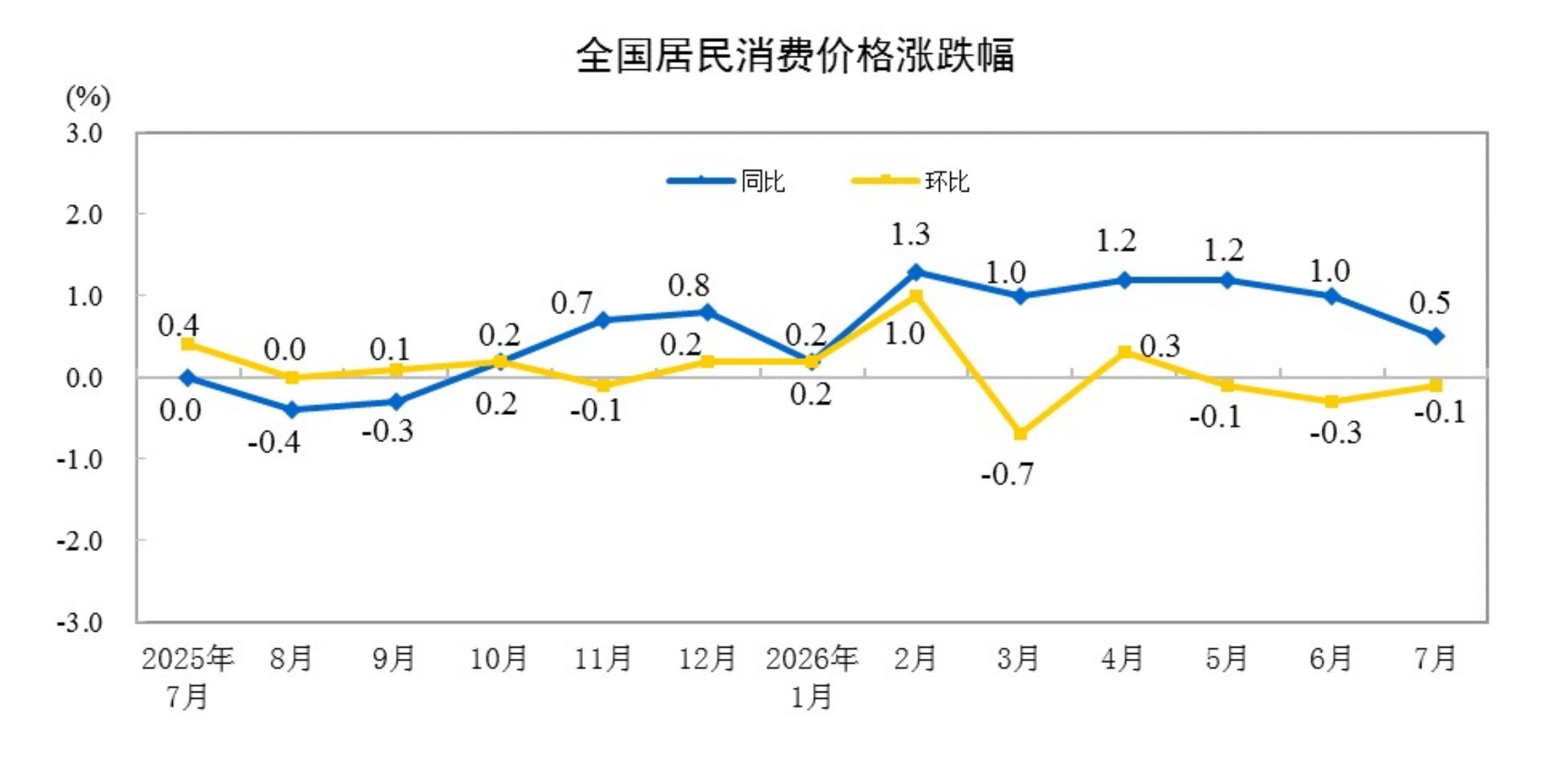

China Inflation Misses at 0.5% in July as Goods Prices Weaken, Services Hold Up

China’s consumer inflation slowed more than expected in July, but underlying breakdown was less uniformly weak than headline suggested. CPI eased from 1.0% to 0.5% y/y, below 0.8% consensus, while monthly CPI improved from -0.3% m/m to -0.1%, still missing expectations for a 0.2% increase. Food prices fell -1.5% y/y, while non-food inflation stood at 0.9%. Goods prices rose just 0.2% y/y, compared with a firmer 0.7% increase in services.

Monthly figures showed an even clearer split. Goods prices fell- 0.6% m/m, while services rose 0.4%, suggesting weakness was concentrated in merchandise rather than spreading evenly across economy. Food prices were unchanged overall, with pork rising 4.1% and fresh vegetables 1.3%, partly offset by a -3.8% drop in fresh fruit. Among non-food categories, education, culture and recreation rose 1.0%, while transportation and communication fell 2.2%.

Taken together, July data point to uneven rather than outright collapsing price pressure. Weak goods inflation and another negative monthly CPI reading still argue that domestic pricing power is limited, but resilience in services tempers a simple deflation narrative.

Alongside PPI slowing from 4.1% to 3.5% y/y, below 3.9% forecast, figures should leave Beijing room to support growth while keeping focus on whether services inflation can broaden into a more durable recovery in domestic demand.

Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| CPI m/m | -0.1% | 0.2% | -0.3% |

| CPI y/y | 0.5% | 0.8% | 1.0% |

| PPI y/y | 3.5% | 3.9% | 4.1% |

Key Takeaways

- China CPI slowed from 1.0% to 0.5% y/y in July, undershooting 0.8% forecast, while monthly CPI improved from -0.3% to -0.1% but remained below expectations for a return to growth.

- Headline weakness was not broad-based. Goods prices rose just 0.2% y/y and fell 0.6% m/m, while services prices increased 0.7% y/y and 0.4% m/m.

- Food prices fell 1.5% y/y, although monthly food prices were unchanged. Pork prices rebounded 4.1% m/m, while fresh fruit prices dropped 3.8%.

- PPI inflation slowed from 4.1% to 3.5% y/y, also below 3.9% forecast, pointing to easing upstream price pressure.

- Overall picture is one of uneven reflation rather than outright deflation: weak goods pricing and softer producer inflation contrast with firmer services prices.

- Data leave Beijing room to support growth without creating an immediate inflation constraint.