Sterling is apparently troubled by more Brexit chaos and weakens broadly. Firstly, ITV’s Robert Peston said it’s almost 100% certain that the UK government cannot make a deal with Northern Ireland DUP, and thus there will be no meaningful vote three (MV3) this week.

But more importantly, the Common speaker John Becrow just made a surprising statement in the Parliament. Simply speaking, Prime Minister Theresa May cannot bring the “same” motion, the Brexit deal that was defeated just last Tuesday, back for another meaningful vote.

That is, the same motion, or essentially the same motion, cannot be voted over and over again. This is a necessary rule to ensure the sensible use of the house’s time, and proper respect for what it decides.

Key quotes from John Bercow’s opening statement:

“If the government wishes to bring forward a new proposition that is neither the same nor substantially the same as that disposed of by the House on March 12, this would be entirely in order.

What the government cannot legitimately do is resubmit to the house the same proposition – or substantially the same proposition – as that of last week, which was rejected by 149 votes.

This ruling should not be regarded as my last word on the subject. It is simply meant to indicate the test which the government must meet in order for me to rule that a third meaningful vote can legitimately be held in this parliamentary session.”

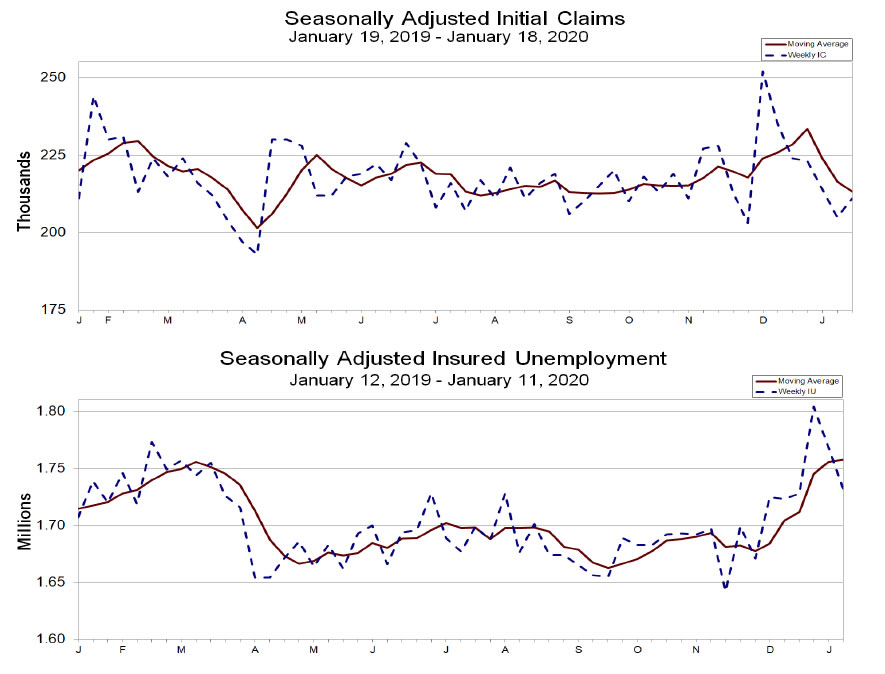

US initial jobless claims fall back to 231k, vs exp 240k

US initial jobless claims fell -33k to 231k in the week ending September 13, below expectation of 240k. Four-week moving average of initial claims fell -750 to 240k.

Continuing claims fell -7k to 1920k in the week ending September 6. Four-week moving average of continuing claims fell -10k to 1933k.

Full US jobless claims release here.