By loading the video, you agree to YouTube’s privacy policy.

Learn more

By loading the video, you agree to YouTube’s privacy policy.

Learn more

US Treasury Secretary Steven Mnuchin tweeted that this round of trade talks in Beijing has concluded. He described the talks as “constructive”. And he looks forward to meeting Chinese Vice Premier Liu He in Washington next week to continue the “important” discussions.

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

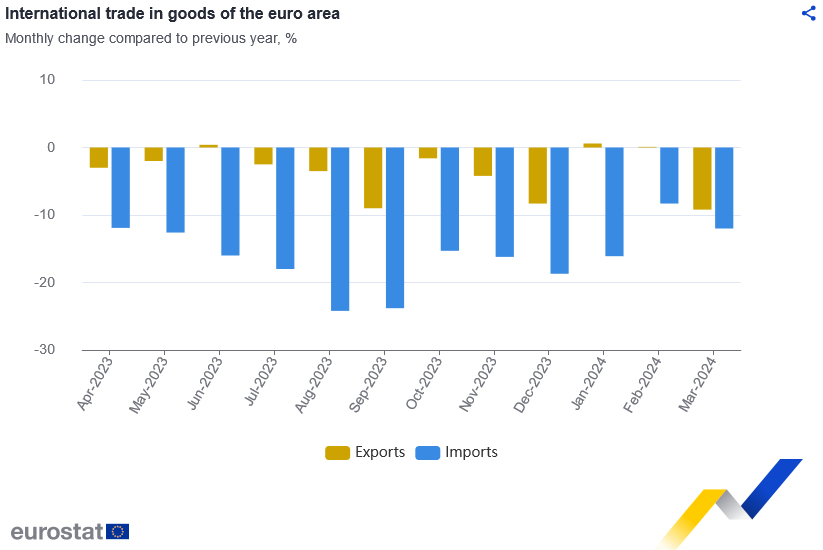

Eurozone goods exports fell -9.2% yoy to EUR 245.5B in March. Goods imports fell -12.0% yoy to EUR 221.3B. Trade balance recorded EUR 24.1B surplus. Intra-Eurozone trade fell -12.4% yoy to EUR 222.1B.

In seasonally adjusted term, goods exports rose 0.1% mom to EUR 237.7B. Goods imports fell -0.1% mom to EUR 220.4B. Trade surplus widened slightly from EUR 16.7B to 17.3B. Intra-Eurozone trade fell -0.5% mom to EUR 213.7B.

US initial jobless claims dropped -13k to 209k in the week ending July 6, below expectation of 221k. Four week moving average of initial claims dropped -3.25k to 219.25k.

Continuing claims rose 27k to 1.723m in the week ending June 29. Four-week moving average of continuing claims rose 5.75k to 1.695m.

US headline durable goods orders dropped -1.6% to USD 250.6B in February, below expectation of -1.2%. Ex-transport order rose 0.1%, also below expectation of 0.3%.

Trump indicated that US and China are “having some very good conversations” on trade. And China want to make deal “very badly” and “it could happen sooner than you think.” He added that’s “because they’re losing their jobs, because their supply chain is going to hell and companies are moving out of China and they’re moving to lots of other places, including the United States.” Additionally, China is “starting to buy our agricultural product again… starting to go with the beef and all of the different things, pork, very big on pork.”

The comments came just a day after Trump’s harsh criticism on China at the United Nations General Assembly. He said “not only has China declined to adopt promised reforms, it has embraced an economic model dependent on massive market barriers, heavy state subsidies, currency manipulation, product dumping, forced technology transfers and the theft of intellectual property and also trade secrets on a grand scale”. And, “as far as America is concerned, those days are over.”

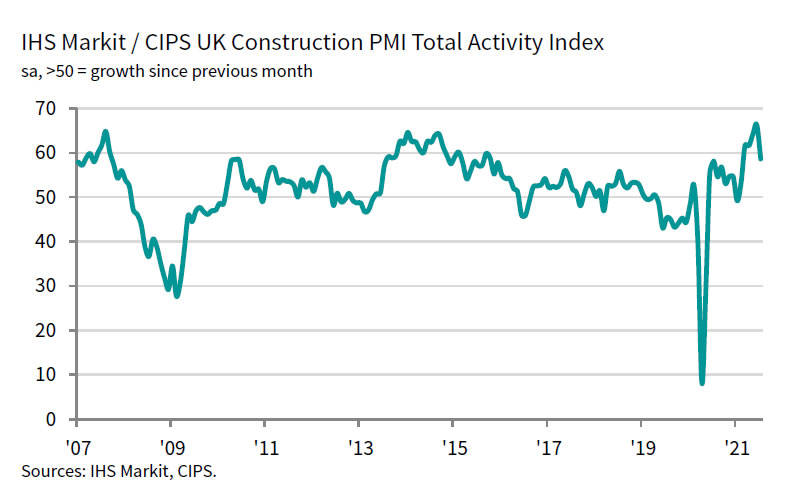

UK PMI Construction dropped to 58.7 in July, down sharply from June’s 24-year high of 66.3. House building remained best-performing category. Supply shortages led to another rapid rise in input prices.

Tim Moore, Economics Director at IHS Markit:

“July data marked the first real slowdown in the construction recovery since the lockdown at the start of this year. It was unsurprising that UK construction companies were unable to maintain output growth at the 24-year high seen in June, especially with widespread supply shortages and constrained capacity to take on additional orders…

“Long lead times for materials and shrinking sub-contractor availability were cited as factors holding back work on site… Another rapid increase in purchasing costs was linked to global supply and demand imbalances, but many firms also noted that local issues had amplified inflationary pressures. These included a severe lack of haulage availability, continued reports of Brexit trade frictions, and greater shortages of contractors due to exceptionally strong demand.”

ECB’s Consumer Expectations Survey for February indicated continuing decline in consumers’ median inflation perceptions over the past 12 months, marking a fifth consecutive month of decrease, settling at 5.5% down from 6.0% in January.

Furthermore, median expectations for inflation over the next 12 months have dipped to 3.1% from 3.3%. This level is the lowest recorded since the onset of Russia’s conflict with Ukraine in February 2022.

Expectations for inflation three years ahead remained stable at 2.5%.

BoE MPC member Megan Greene expressed concerns today during a seminar about the economic repercussions of ongoing tensions in the Middle East. Highlighting the region’s significance, Greene pointed out the risks associated with an energy price shock and other supply side disruptions, which could complicate the inflationary landscape further.

“I do think that what’s going on in the Middle East does pose a risk,” Greene remarked. “I’m worried about the sort of an energy price shock and other supply side shock, which obviously follow a number of supply side shocks we’ve seen over the past couple of years, and what that might do to inflation expectations.”

Greene also addressed the challenges involved in reducing inflation to the Bank’s target of 2%, noting that the final steps in this process are particularly challenging. “The ‘last mile’ of the journey towards hitting the 2% inflation target was the hardest part,” she stated.

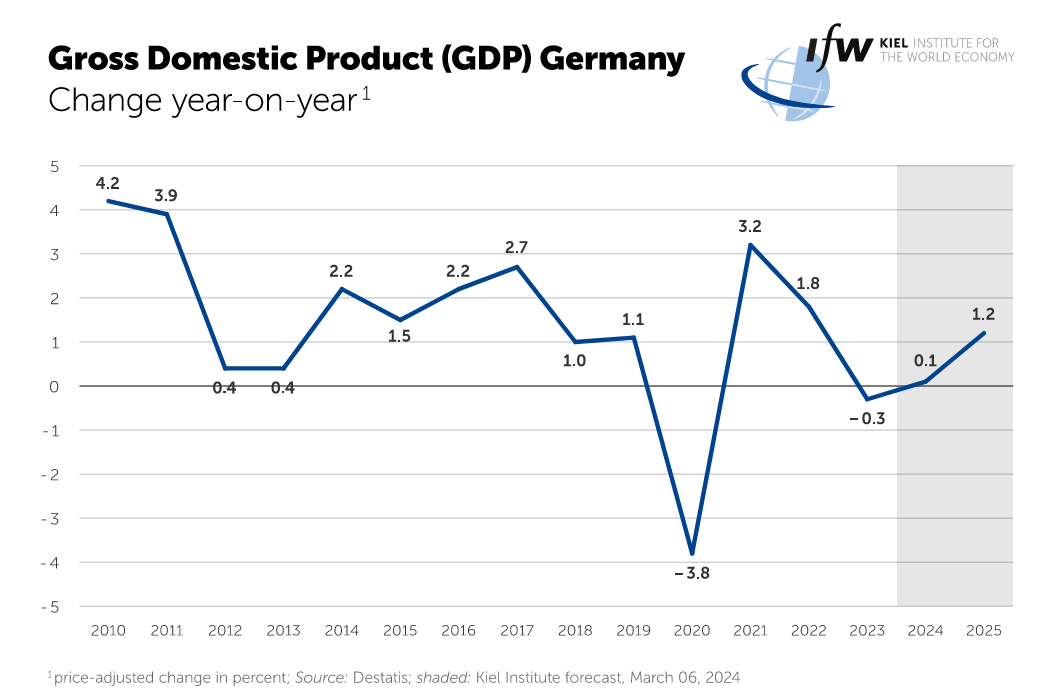

Kiel Institute for the World Economy significantly downgraded its growth expectations for German economy, projecting a mere 0.1% increase in 2024, a sharp downward revision from its previous forecast of 0.9%. Slight improvement is anticipated in 2025, with growth expected to accelerate to 1.2%. On the inflation front, decline to 2.3% is projected for this year, down from 5.9% in 2023, with further reduction anticipated to 1.7% in 2025. Unemployment rate is expected to marginally decrease from 5.8% in 2024 to 5.6% in 2025.

Moritz Schularick, President of the Kiel Institute, pointed to a “whole range of factors” currently dampening sentiment and economic performance in Germany. These include global economic slowdown impacting exports, ECB’s restrictive monetary policy expected to extend into the next year, and German government’s austerity measures, which Schularick believes are being implemented at an inopportune time, fostering additional pessimism.

Stefan Kooths, Head of Economic Research at the Kiel Institute, added that despite gradual recovery expected over the year, the overall economic dynamism in Germany remains subdued. He underscored the emergence of signs indicating that structural issues are mainly to blame for the economic slowdown, with private investment falling short, partly due to the significant uncertainty provoked by current economic policies.

In an interview with the Financial Times, ECB Chief Economist Philip Lane indicated that, barring major surprises, there is sufficient evidence to “remove the top level of restriction” in June, suggesting an initial reduction in the 4.00% deposit rate. He noted that the forthcoming data over the next few months will guide ECB in determining the pace at which further restrictiveness can be eased.

Lane acknowledged that the path to disinflation will be “bumpy and gradual.” He framed the debate for this year by stating that ECB still “needs to be restrictive all year long,” but within this “zone of restrictiveness,” there is potential to “move down somewhat.”

He added, “We don’t need the data to say normalization is a lock. What we do need the data to say is: is it proportional, is it safe, within the restrictive zone to move down.”

Looking ahead to next year, Lane mentioned that discussions about the “normalization” of monetary policy will be more pertinent when wage growth has visibly decelerated and the inflationary impacts of current fiscal measures have diminished.

UK unemployment rate was unchanged at 4.1% in the three months to October, matched expectation. However, wage growth was rather impressive. Average weekly earnings including bonus rose 3.3% 3moy, above expectation of 3.0% 3moy. Average weekly earnings excluding bonus also rose 3.3% 3moy, above expectation of 3.2% 3moy. Wage growth was indeed fastest since 2008. Also claimant count rose 21.9k in November, above expectation of 13.2k.

Boston Fed President Susan Collins highlighted that recent rise in long-term yields implies some tightening of financial conditions. “If it persists, it likely reduces the need for further monetary-policy tightening in the near term,” she noted in a speech yesterday.

Such market dynamics further bolstered Collins’ perspective on the current tightening cycle led. “This reinforces my view that we are very near, and perhaps at, the peak federal funds rates for this tightening cycle,” she stated, indicating that the cycle could be nearing its zenith.

However, Collins maintained a flexible stance on the future course of action, and clarified, “I would not take further tightening off the table yet.”

Weighed in on yesterday’s CPI data, which revealed that September’s headline inflation held steady at 3.7% and core inflation eased to 4.1%. Collins said, “Today’s CPI release is a reminder that restoring price stability will take time.”

Canada’s retail sales value fell -0.2% mom to CAD 66.4B in March, slightly worse than expectation of -0.1% mom. Sales were down in seven of nine subsectors and were led by decreases at furniture, home furnishings, electronics and appliances retailers.

Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -0.6% om.

Advance estimate suggests that that sales increased 0.7% mom in April.

Kansas City Fed President Jeffrey Schmid expressed confidence that inflation will gradually return to Fed’s 2% target “over time”. But he also emphasized the importance of patience, saying, “I am prepared to be patient as this process plays out.”

Schmid highlighted the necessity of curbing demand growth to allow supply to catch up, which is essential for closing the imbalance driving inflation.

Regarding Fed’s balance sheet, “I didn’t really think we should have slowed the runoff,” Schmid said. “I think there was room to continue to run off like we were doing.”

Over 50 retailers in UK sent a joint letter to Chancellor of the Exchequer Sajid Javid, urged him to fix the “broken” business rates system. The letter was coordinated by the British Retail Consortium.

The letter urged four fixes, including a freeze in the business rates multiplier; fixing transitional relief, which currently forces many retailers to pay more than they should; introducing an ‘Improvement Relief’ for ratepayers; ensuring that the Valuation Office Agency is fully resourced to do its job.

Helen Dickinson, Chief Executive of the BRC said:”These four fixes would be an important step to reform the broken business rates system which holds back investment, threatens jobs and harms our high streets. The new Government has an opportunity to unlock the full potential of retail in the UK, and the Prime Minister’s economic package provides a means to do so.

A batch of mixed economic data was released from Japan today. Industrial production rose 1.3% mom in July, well above expectation of 0.3% mom. Growth was supported by increased production of cars and chemicals, which offset decline in oil products. The somewhat solid rebound in production offered a hopeful sign that manufacturers are weathering global slowdown and escalation of US-China trade war so far.

On the other hand, retail sales dropped -2.0% yoy in July, much worse than expectation of -0.6% yoy. The contraction raised concerns that momentum of domestic demand was much weaker than originally expected. In particular, consumption could be further strained by the planned sale tax hike later in the year.

Also released, unemployment rate dropped to 2.2% in July, beat expectation of 2.3%. Housing starts dropped -4.1% yoy, versus expectation of -5.4% yoy. Tokyo CPI slowed to 0.7% yoy in August, down from 0.9% yoy, missed expectation of 0.8% yoy.

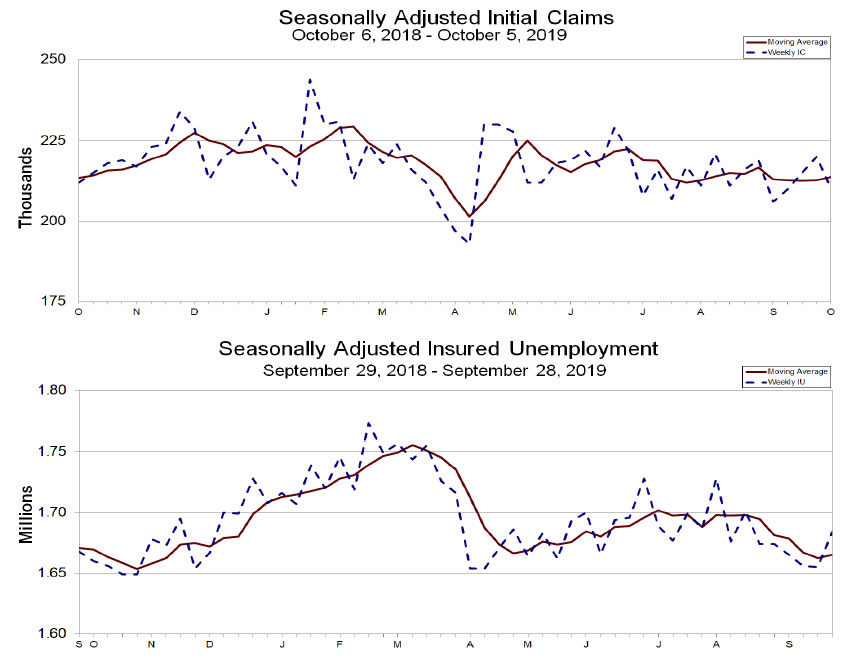

US initial jobless claims dropped -10k to 210k in the week ending October 5, below expectation of 217k. Four-week moving average of initial claims rose 1k to 213.75k. Continuing claims rose 29k to 1.684m in the week ending September 28. Four-week moving average of continuing claims rose 2.5k to 1.665m.

Bundesbank President Jens Weidmann told the Welt am Sonntag newspaper, “I do not rule out higher inflation rates.” He added, “In any case, I will insist on keeping a close eye on the risk of an excessively high inflation rate and not only on the risk of an excessively low inflation rate.”

He also said that the emergency asset purchase program, known as PEPP, must end when the Covid-19 crisis is over. “The first P stands for pandemic and not for permanent. It’s a question of credibility,” he added.

On the plan of stimulus exit, “the sequence would then be: first we end the PEPP, then the APP is scaled back, and then we can raise interest rates,” he said.

ActionForex.com was set up back in 2004 with the aim to provide insightful analysis to forex traders, serving the trading community for over a decade. Empowering the individual traders was, is, and will always be our motto going forward.

Contact us: contact@actionforex.com

© ActionForex.com © 2024 All rights reserved.

EU & UK held construction technical-level Brexit discussions, but more time needed

As noted in a brief statement by European Commission, EU chief Brexit negotiator Michel Barnier held “constructive technical-level talks” with UK over the weekend. However, “a lor of work remains to be done” and technical level discussions will continue on Monday. Barnier is set to brief EU27 minutes at the General Affairs Council on Tuesday.

On the other hand, UK Prime Minister Boris Johnson’s spokesperson said “The Prime Minister said there was a way forward for a deal that could secure all our interests … but that there is still a significant amount of work to get there and we must remain prepared to leave (without a deal) on October 31.”

Reuters quoted a unnamed EU diplomat saying that “differences persist on customs” regarding the Irish border. And, there are “small chances” for a text to be ready for EU summit this week. More time is needed to continue to discussions. European Commission President Jean-Claude Juncker also said in an interview that “it’s up to the Brits do decide if they will ask for an extension… “But if Boris Johnson were to ask for extra time – which probably he won’t – I would consider it unhistoric to refuse such a request.”