Here are the latest developments in global markets:

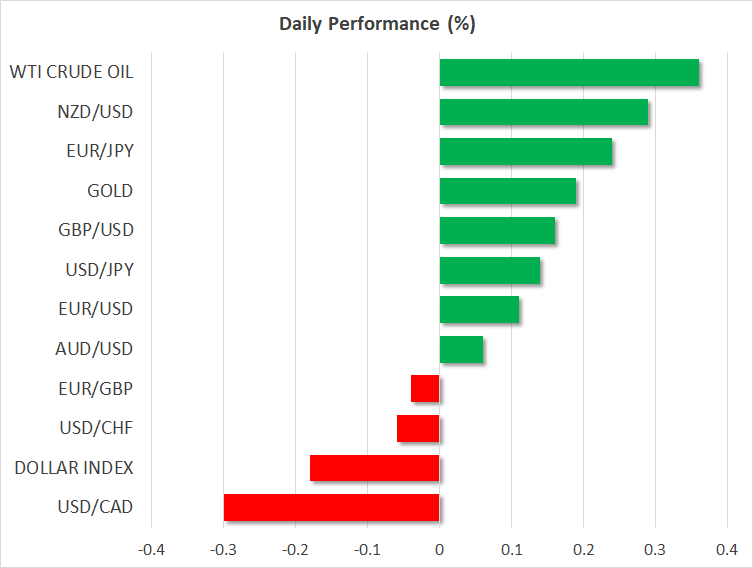

FOREX: The US dollar index is nearly 0.2% lower on Tuesday, looking set to extend the modest losses it recorded yesterday. The safe-haven Japanese yen is also on the back foot, as the risk-aversion emanating from Turkey subsided somewhat, for now at least. Conversely, the euro and pound are a little higher, attempting to recover some of their latest losses. The Turkish lira – which has been at the epicenter of attention lately – is also trading higher today, catching its breath following a sharp selloff in recent sessions.

STOCKS: Wall Street closed lower on Monday, as concerns over the deepening crisis in Turkey kept a lid on investors’ risk appetite. The Dow Jones fell by 0.50%, while the S&P 500 and Nasdaq Composite dropped by 0.40% and 0.25% respectively. It seems that market worries over Turkey may have taken a back seat for now though, considering that futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open today. Meanwhile, Asia was mixed on Tuesday. Although Japan’s Nikkei 225 (+2.28%) and Topix (+1.63%) advanced, buoyed by a weaker yen, the Hang Seng in Hong Kong underperformed (-0.82%). In Europe, futures markets are pointing to a higher open for all the major benchmarks.

COMMODITIES: Oil prices are higher on Tuesday, with WTI advancing by 0.36% to $67.56 per barrel, and Brent gaining 0.24% to trade at $72.93/barrel. The uptick appears to be owed to the latest OPEC report suggesting Saudi Arabia reduced its production in July. In precious metals, gold is up by nearly 0.2% on Tuesday, recovering some of the losses it posted in the previous session, when it touched a 20-month low of $1,191/troy ounce. The technical break confirms the negative trend is back in force, with the next major support area being around $1,180. That said, note that bearish sentiment on gold appears to be at extreme levels, which likely renders prices vulnerable to a so-called “short-squeeze”. Given the extent of negative bets, any piece of gold-friendly news could lead to an outsized positive reaction, as numerous investors rush to either cover or unwind their short positions.

Major movers: Yen pulls back as Turkey jitters take a back seat for now

After trading in risk-off mode over the past few sessions amid worries that the crisis in Turkey could spill over into other economies, markets appear to have calmed down a little on Tuesday. The Turkish central bank took some steps to enhance liquidity yesterday, which although falling short of addressing the bigger issues in the troubled economy, still appear to have “done the trick” for now – providing some much-needed relief to the Turkish lira and risk-sensitive assets.

Hence, the reactions in the FX market today are largely the opposite of what transpired over recent days. Namely, the yen and the dollar that have acted as safe-havens in this turmoil are pulling back, while the euro and the pound are attempting a modest recovery. That said, the magnitude of these corrective moves is relatively modest compared to the much-larger movements that unfolded as the Turkish saga gained traction, which implies this calm may only be a “breather” in the bigger picture, and that the situation has not changed materially. Indeed, considering the lack of concrete action by Turkish authorities, and the fact that the US-Turkey standoff shows no signs of relenting, it wouldn’t be surprising to see risk aversion stage a comeback before long.

Euro/dollar is higher by a modest 0.1% on Tuesday, attempting to post a second day of advances, but still hovering near the one-year low it touched yesterday. The euro has been very sensitive to developments in Turkey, after recent reports suggested that large European banks could be exposed to Turkish loans that are liable to default amid the deepening crisis. Thus, the risk premium on the euro appears to be on the rise, which in combination with the dollar attracting some haven flows, likely explains the recent move lower in euro/dollar.

The yen is pulling back across the board, down by 0.13% versus the dollar and by 0.24% against the euro today. Meanwhile, the British pound is higher, ahead of the release of the UK employment data. It’s probably going to be a big and exciting week for the pound, not least due to the Brexit negotiations resuming on Thursday.

Elsewhere, commodity-linked currencies are also enjoying a bid today, with the aussie, kiwi, and loonie, all trading higher against their US counterpart.

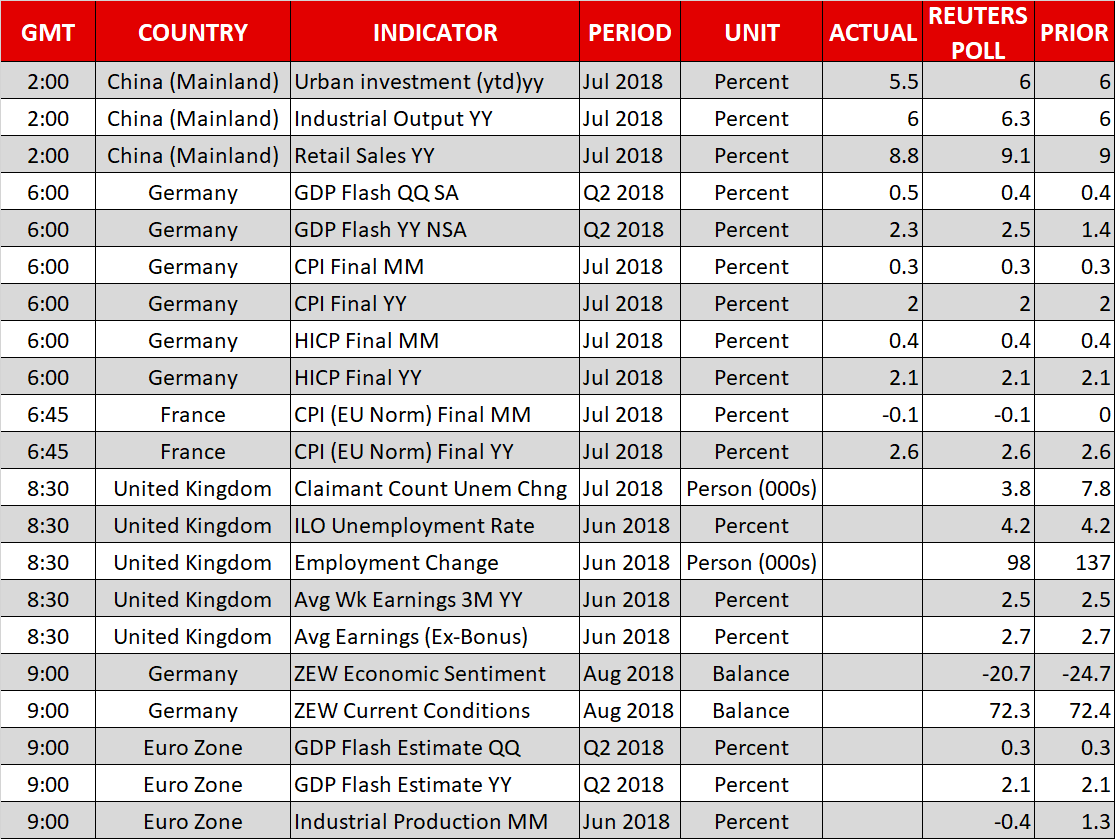

Day ahead: UK jobs report due; German ZEW survey and updated eurozone GDP also out; Turkish drama remains in the forefront

Tuesday’s calendar features important data on employment out of the UK, while Germany’s ZEW surveys on business sentiment, as well as updated GDP figures out of the eurozone are also on the agenda. In the meantime, any Turkey-related developments will be closely watched.

The UK’s jobs report for June, as well as July’s unemployment claimant count are due at 0830 GMT. June’s unemployment rate is anticipated to remain at the multi-decade low of 4.2%, with the number of jobs created during the three months to June projected to stand at 98k, below May’s 137k, but still at relatively healthy levels. However, the lion’s share of attention is yet again expected to fall on wage growth numbers: average weekly earnings are forecast to have risen by 2.5% on an annual basis in the three months to June, the same as in May. Excluding bonuses, the measure is again anticipated to match May’s pace of growth of 2.7% y/y. A data-beat, especially on the wage growth front, may lead to an outsized gain in pound/dollar relative to the decline in case of a miss, as it might fuel views for an overextended selloff in previous days.

ZEW’s surveys on business morale in Germany, the eurozone’s largest economy, will be released at 0900 GMT. The economic sentiment index is projected to show an improvement in August, though still remain in negative territory, while the current conditions index is anticipated to weaken on the margin relative to July’s print.

Eurozone’s second estimate of Q2 GDP growth is also due at 0900 GMT. No revisions are expected relative to the preliminary readings which pointed to 0.3% quarterly and 2.1% annual growth rates during the quarter, constituting a deceleration compared to Q1’s respective figures of 0.4% and 2.5%. Additionally, the numbers on June’s eurozone industrial production will be made public at the same time.

US data on July’s import and export prices will be hitting the markets at 1230 GMT. Additionally, the New York Fed will be issuing its Q2 household debt and credit report at 1500 GMT.

Meanwhile, the Turkish drama remains front and center, with any developments, which have proven to have implications for emerging and developed markets alike, to be monitored by traders.

In energy markets, weekly API data on US crude stocks are due at 2030 GMT.

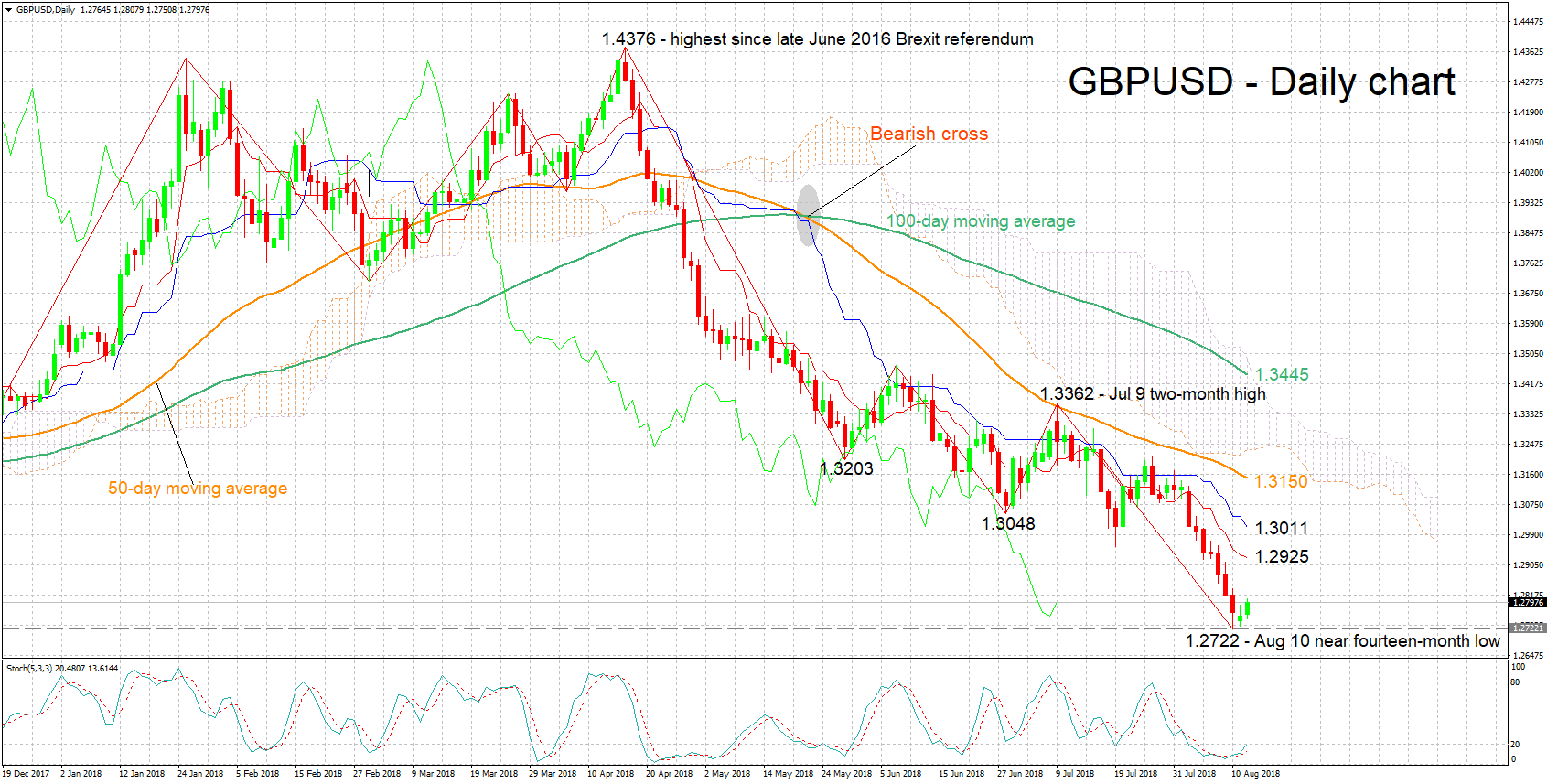

Technical Analysis: GBPUSD short-term bearish though stochastics may be pointing to changing sentiment

GBPUSD has gained some ground after touching its lowest since late June 2017 of 1.2722 on Friday. Still, the Tenkan- and Kijun-sen lines remain negatively aligned in support of a bearish bias for the pair. The Chikou Span, though, may be pointing to an oversold market. In addition, the stochastics are giving a bullish signal in the very short-term, as the %K line has moved above the slow %D one.

Upbeat UK data later today are likely to boost the pair. Given a conclusive break above the 1.28 level, additional resistance may come around the current level of the Tenkan-sen at 1.2925, including the 1.29 round figure.

On the downside and in case of disappointing data, support could be met around last week’s near 14-month low of 1.2722, with the 1.27 handle lying not far below.

{kind=link}