Here are the latest developments in global markets:

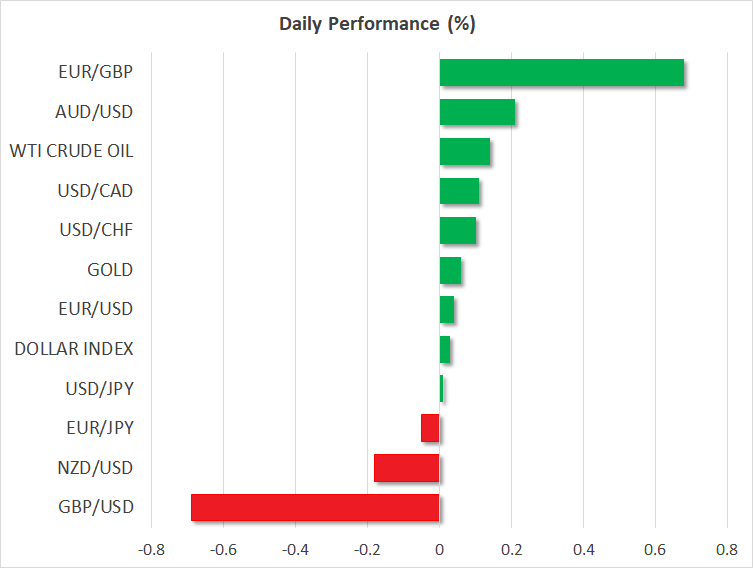

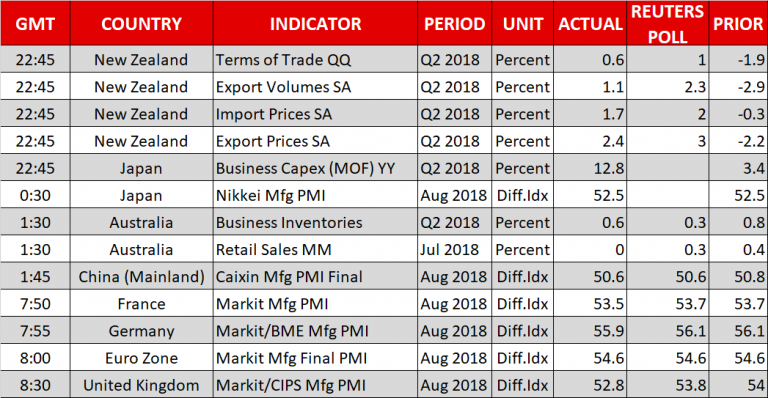

FOREX: Sterling opened with a gap down on Monday’s Asian session after EU chief Brexit negotiator Michel Barnier said he strictly opposes the UK’s offer on future EU-UK trade relations. Pound/dollar, which has come off from a 1-month high last week, recorded the fifth red month in a row. Today, the pair dipped by 0.64% and slipped below the 1.2900 handle, increasing negative momentum after the UK manufacturing PMI clocked in at 52.8 in August, below the forecast of 53.8. Also, euro/pound edged higher by 0.61%. The dollar’s index against a basket of six currencies steadied at 95.16 (+0.03%) and dollar/yen was also flat at 111.05 (+0.02%) after the US and Canada ended contentious trade negotiations without a deal on Friday; the US President Donald Trump said on Saturday there was no need to keep Canada in NAFTA. Euro/dollar traded higher by 0.11% at 1.1612, losing little from a downward revision in the final German manufacturing PMI for August. The Eurozone’s final manufacturing PMI was confirmed at 54.6 in the aforementioned month. In the antipodean space, aussie/dollar advanced by 0.24% following the touch on the 21-month low of 0.7165 earlier today before the RBA rate decision on Tuesday, while kiwi/dollar moved near 2-week lows (-0.14%). Finally, dollar/loonie headed higher by 0.12%.

STOCKS: European equities were mixed on Monday as worries about US trade policy kept investors cautious. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.11% and 0.07% respectively at 1040 GMT. The German DAX 30 was down by 0.16%, while the French CAC 40 inched up by 0.04%. The Italian FTSE MIB and the UK’s FTSE 100 were the best performers, gaining 0.55% and 0.81% respectively. In Asia, equities closed in the negative territory, while US markets will remain closed today for the Labor Day holiday.

COMMODITIES: Oil prices edged higher today with West Texas Intermediate (WTI) crude adding 0.2% to its performance, hovering around $70 per barrel, while Brent’s oil reached an almost 2-month high at $78.22 before slipping back to $78 per barrel (+0.50%). In precious metals, the price of gold remained near its opening level, marginally above $1,200/ounce despite worries over US-Sino tensions and inconclusive trade talks between the US and Canada.

Day ahead: Trade drama and Brexit to feed risk aversion; RBA decides on interest rates

US and Canadian markets will be closed for the Labor Day holiday on Monday, while the economic calendar will be light in terms of data releases, leaving investors fully concentrated on the trade drama and the Brexit noise during the day.

Friday’s NAFTA deadline passed without any agreement between the US and its neighbor Canada, with the US President warning on Saturday he may terminate the trade pact entirely if the Congress interferes with negotiations which resume on Wednesday. Meanwhile, he showed interest to sign a bilateral deal with Mexico after the two countries were said to have secured a preliminary trade deal last week. This week, markets will face another deadline on September 6, the day the US prepares to unleash tariffs on $200 billion Chinese imports, considered as the largest hit to Beijing in the multi-month US-Sino trade battle so far. But the failure to renew the NAFTA deal, raised fears that Washington will not pull back this time either, leaving import tariffs to go ahead, a move that would add another layer of uncertainty to the trade story and therefore further pressure to riskier assets such as stocks.

On the Brexit front, the bearish sentiment returned as well after the EU Brexit negotiator, Michel Barnier noted that he is strongly opposed to the British Prime Minister’s proposals on the future EU-UK trade relations, fueling concerns that a deal won’t be achievable by October’s 18-19 EU summit in Brussels. Yet, more Brexit headlines could follow until that day, as EU leaders are planning to discuss the topic at their summit in Austria on September 20, with the pound expected to register further pivot turns in the wake of new developments. Meanwhile in the UK, a spokesman to the British Prime Minister told reporters on Monday that the Chequers proposals are the only credible and negotiable Brexit plan while regarding monetary issues, he confirmed that the Bank of England’s chief Mark Carney will leave his office in 2019 despite being asked to stay in the role until 2020.

In Australia, the focus will shift to monetary policy and the Reserve Bank of Australia’s (RBA) rate decision due on Tuesday at 0430 GMT. Forecasts are for the central bank to keep interest rates unchanged at the record low of 1.5%, for the second year in a row, pointing to rising global trade risks and still-subdued wage growth in Australia. While a no change decision is already priced in, traders will read the rate statement and listen to the RBA’s governor, Philip Lowe’s remarks later in the same day at 0930 GMT for more clues on how policymakers assess the Australian economic conditions. Earlier at 0130 GTM, current account readings for the second quarter are expected to give direction on what investors should expect from Australia’s Q2 GDP growth figures released on Wednesday. Note that retail sales showed no growth in July, missing expectations for an expansion, while business inventories in the three months to June increased by more than analysts expected.

Italy will remain under the spotlight in the Eurozone after Fitch ratings reaffirmed its overall BBB rating on the economy, but downgraded its outlook from stable to negative, citing the government’s potential fiscal reforms as risks to Italy’s financial credibility. On September 27, the government will form new fiscal and economic growth targets, while on October 15, a draft budget will be sent to the European Commission.

Developments in Turkey will be of interest ahead of the central bank’s rate decision on September 13. Analysts believe that policymakers will continue to raise rates despite the Turkish President’s calls to keep borrowing costs low.

{kind=link}