Here are the latest developments in global markets:

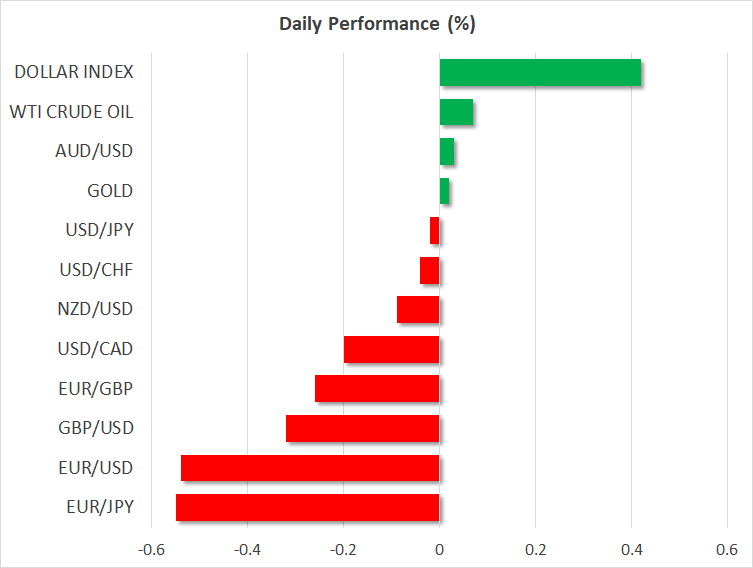

FOREX: The dollar maintained yesterday’s impressive rally against the Japanese yen, consolidating gains around 113.34 as the US confirmed a strong 4.2% q/q GDP growth in the second quarter, the highest since Q2 2016, signaling further rate hikes in the future. Monthly US durable goods orders printed a sharper increase in August than analysts thought, adding further spark to the greenback on Thursday. The dollar index head up to 95.28 (+0.41%) as the pound and the euro remained on the downside. Pound/dollar slipped to a two-week low of 1.3032 (-0.33%) after the final yearly Q2 GDP growth figure out of the UK was revised lower to 1.2%, from 1.3% in the second estimate, while the print for Q1 was also marked lower to 1.1% y/y. Final UK business investment readings were discouraging too, ending the second quarter in negative territory. Economic issues in Italy were the main drag on the euro today after the Italian government announced a budget deficit of 2.4% in 2019 which is below the 3.0% EU debt limit but above what markets expected. The flash core CPI figure for September out of the bloc disappointed as well, inching down to 0.9% in yearly terms from 1.1% expected and 1.0% seen in August. Euro/dollar dived to a more than a 2 ½ -week low of 1.1575 (-0.54%), euro/pound fell to 0.8877 (-0.25%), while euro/yen tumbled to 131.22 (-0.55%). In antipodean currencies, aussie/dollar and kiwi/dollar were moving in different directions, with the former improving to 0.7209 (+0.04%) and the latter decreasing to 0.6611 (-0.11%). Dollar/loonie was changing hands lower at 1.3016 (-0.18%), a day after the BoC Governor said that the economy is operating near capacity and that the central bank will continue to raise rates gradually. Moreover, he expressed optimism on NAFTA a few days before the October 1 deadline.

STOCKS: European equities were in the red at 1130 GMT with financial stocks led by Italian banks losing more than 1% following the announcement of a bigger-than-expected budget deficit. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 dropped by 0.83%. The Italian FTSE MIB was the worst performer diving by 4.11%, the German DAX 30 lost 1.44% and the French CAC 40 retreated by 0.93%. In the UK, the FTSE 100 inched down by 0.71%, while in the US futures tracking the S&P 500, Dow Jones and Nasdaq 100 were flat. In Asia stocks closed in positive territory, with Chinese and Japanese indices gaining around 1%.

COMMODITIES: Crude oil prices were in positive terittory amid evidence that Iranian crude exports were suffering from US sanctions, while investors feared additional losses in the coming months as the US is ready to kick off a second round of sanctions against Tehran on November 4. Data showed that purchases of Iranian crude oil by major Asian buyers fell to two-month lows in August. Yet, reports that Saudi Arabia is planning to increase production by up to 600k bpd in the coming months to offset supply shortages in Iran, limited gains in the market. WTI crude and the London-based Brent were last seen at $72.17/barrel (+0.07%) and $82.25 (+0.65%) respectively. In precious metals, gold steadied at $1,182.6/ounce after hitting six-week lows at $1,181.6 on Thursday.

Day Ahead: PCE inflation closely watched in US; Canadian GDP coming up

The most significant data release later today will be the US core Personal Consumption Expenditure (PCE) index for August, the Fed’s favorite inflation measure. It will be released alongside personal income and spending figures for the same month, at 1230 GMT, while at 1345 GMT the Chicago PMI will also come under review. Flash estimates for the core PCE rate support that inflation remained unchanged at 2.0% in yearly terms, however, on a monthly basis the measure is predicted to inch down to 0.1% from 0.2% previously. Meanwhile, both income and spending are projected to have risen by 0.4% m/m and 0.3% m/m, from 0.3% and 0.4% previously correspondingly.

Remaining in the US, at 1400 GMT, the University of Michigan will deliver final readings on consumer sentiment and inflation expectations for the month of September. Forecasts suggest the consumer sentiment index is to hold flat at 100.8. The survey related to inflation expectations will attract interest as well.

Following the US and the UK, Canada will publish GDP growth figures too. The Canadian economy is said to have expanded by 0.1% month-on-month in July from 0.0% in the preceding month. Any deviation from expectations could trigger some volatility in the loonie.

In energy markets, investors will keep a close eye on the US oil rig count issued by the Baker Hughes company at 1700 GMT. Potential increases in active drilling rigs are likely to add pressure to oil prices.

As of today’s public appearances, at 1130 GMT the Irish Central Bank Governor Philip Lane and the Deputy Governor at the Bank of England Dave Ramsden will have a talk about the economic outlook and monetary policy. The latter will be making comments at 1320 GMT as well. Later, Federal Reserve Bank of Richmond President Thomas Barkin and Federal Reserve Bank of New York President John Williams will be delivering speeches at 1530 GMT and 2045 GMT respectively. The ECB chief economist Peter Praet will be participating in a panel in Frankfurt at 1535 GMT.

On Sunday, the UK ruling Conservative Party will start its three-day annual conference in Birmingham to discuss political strategies. The event could be a challenging one for the UK Prime Minister as it comes a week after the EU rejected her Chequers Brexit plan, with May probably making efforts to persuade her counterparts that she is the appropriate leader to help the UK leave the EU. Brexit protesters, though, are not expected to take the back seat. May is scheduled to address the event early on Wednesday, though sterling could show some volatility on Monday in the wake of fresh Brexit headlines.