Here are the latest developments in global markets:

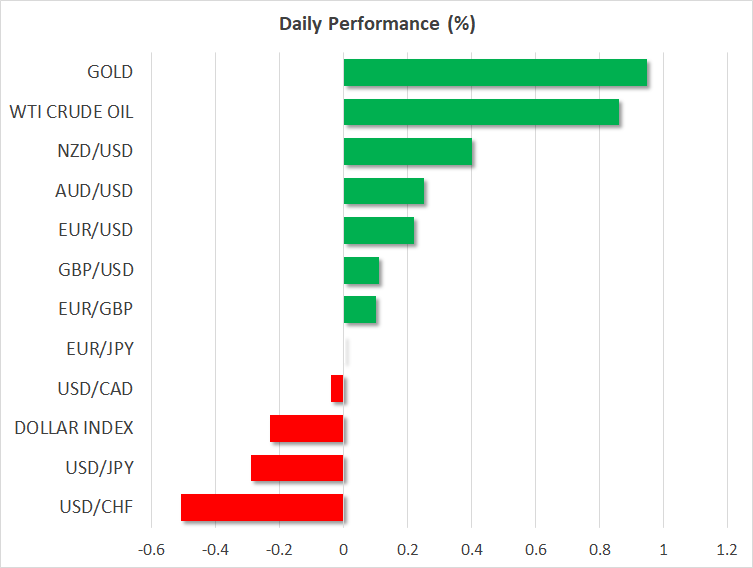

- FOREX: After starting the day with a gap down at 1.3082, pound/dollar managed to turn positive during the early European session, rallying to 1.3170 (+0.12%) mainly due to a weaker dollar. Brexit uncertainties continued to linger in the background as the talks between Brexit negotiators failed to break the Irish deadlock on Sunday, though some officials showed optimism that a deal could be agreed in coming weeks. The yen attracted further demand in the face of rising geopolitical tensions between US and Saudi Arabia, sending dollar/yen to a one-month low of 111.61 (-0.38%). Euro/dollar regained ground to trade slightly below the 1.1600 handle (+0.24%) despite headlines stating that the Italian government budget approval could shift to Tuesday. Euro/pound climbed by 0.13% and is set to record the third green day. In the antipodean sphere, aussie/dollar jumped by 0.21% and kiwi/dollar traded higher by 0.40%. Dollar/loonie was flat around 1.3016. Dollar/Turkish lira was the worst performing pair today, losing 1.35% in the day.

- STOCKS: European shares were mixed at 1130 GMT. The pan-European STOXX 600 declined by 0.15%, while the blue-chip Euro STOXX 50 climbed by an equivalent percentage as telecommunications soared (+1.63%). The Spanish IBEX 35 fell by 0.08%, while the German DAX 30 and the Italian FTSE MIB gained by 0.33%. The British FTSE 100 and the French CAC 40 were weaker by 0.04% and 0.06% respectively. In Asia, the majority of stocks closed strongly negative, while futures tracking US indices such the S&P 500, Dow Jones and Nasdaq 100 reduced their overnight losses but still pointed to a negative open.

- COMMODITIES: Oil prices started the day on the upside following news that the US is ready to punish Saudi Arabia with sanctions if the country proves responsible for the disappearance of a Saudi journalist that resided in the US. The Saudi government threatened to take counter-actions as well. WTI crude was up by 0.83% at $71.93 and Brent was higher by almost 1.00% at $81.27. In precious metals, gold hit 3-month highs at $1233.26/ounce before it slipped back to $1229.

Day Ahead: Geopolitics & Brexit eyed; US retail sales, New Zealand & Chinese CPI next in focus

Appetite for riskier assets remained loose on Monday as geopolitical tensions and Brexit uncertainties took the centre stage, while economic differences between Italy and the Eurozone will likely keep investors busy today as well.

In geopolitics, the US President threated to act with “very powerful” consequences against Saudi Arabia as the kingdom has been unable to provide a convincing explanation so far about the disappearance of the Washington Post columnist Jamal Khashoggi who is believed to have been murdered on October 2 inside Saudi Arabia’s consulate in Turkey. Trump warned that if the nation proves responsible of the incident he will move forward with sanctions, causing a similar reaction from the Saudi government on Sunday which warned to take greater actions in case the US implements economic sanctions. Should tensions intensify in coming sessions, oil prices could advance even further amid fears oil supply in the Saudi region could be limited in the face of economic restrictions.

Brexit fears resurfaced during the weekend too after the UK Brexit Secretary Dominic Raab failed to resolve differences related to the Irish backstop at his meeting with the EU Brexit negotiator, Michel Barnier in Brussels. While markets were positive that Sunday’s meeting between the sides could bring progress before EU leaders gather on Wednesday, some key issues involving mainly the Irish border remained open, with the spokesman of the junior coalition party of PM May’s government admitting that a no-deal Brexit is “probably inevitable”. The UK Prime Minister will attend the summit on Thursday.

Meanwhile in the EU, the Italian government faces a deadline to submit its budget draft to the European Commission today and investors will be eagerly waiting to see whether Rome will stick to its initial fiscal demands which aim for a deficit of 2.4% of GDP in 2019 compared to a previous commitment of 0.8%. The cabinet is expected to hold a meeting at 1500 GMT later today. Should the EU disagree with the budget, Italy would need to revise it and submit it before EU finance ministers express their opinions on December 3. In the meantime, any headlines supporting that Italy might not get away with its proposals could weigh heavily on the euro.

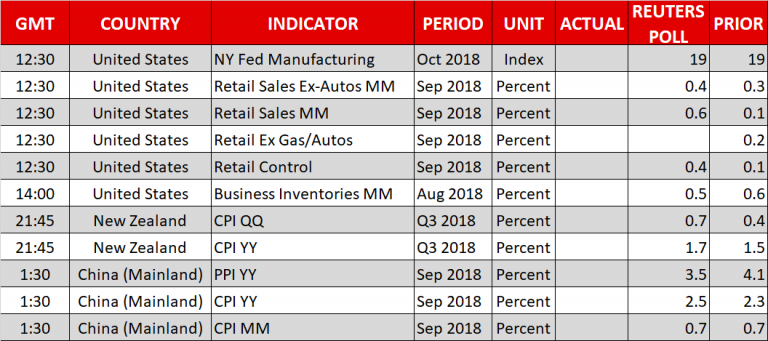

Turning to data releases, US retail sales will feature the calendar at 1230 GMT, giving some evidence on consumers’ buying appetite. According to analysts, retail sales are forecasted to have grown by 0.6% month-on-month (m/m) in September after increasing by 0.1% in August. In the absence of volatile automobiles, the core equivalent is expected to gain 0.1 percentage points and pick up to 0.4%. If the numbers rise higher than projected, marking the seventh consecutive positive month, the dollar may recoup earlier losses amid increasing confidence that the Fed will deliver another rate hike in December.

Separately, September’s retail control and the New York Fed Manufacturing index for the month of October will come into light at the same time, while at 1400 GMT, US business inventories for the month of August may attract some interest as well.

Elsewhere, New Zealand will see the release of CPI figures at 2145 GMT, probably helping the battered kiwi to gain some strength in case the figures surprise to the upside, even if the RBNZ is not considering any rate hike until 2020. Consensus is for the headline CPI to come closer to the central bank’s 2.0% midpoint target, inching up to 1.7% y/y in the third quarter from 1.5% in Q2. Quarter-on-quarter, inflation is seen higher as well, at 0.7% compared to 0.4% seen previously.

Staying in the Tasman sea, the Reserve Bank of Australia will be publishing minutes of its October policy meeting at 0030 GMT on Wednesday. Although the central bank messaged that the next move in rates is up rather than down, it also said that the it will remain patient until 2020 as inflation is anticipated to reach the 2.0% target only gradually due to the slow wage growth progress. RBA policymakers have cited US-Sino trade conflicts as another risk to Australia’s economic growth.

In Asia, Chinese CPI and PPI data will be closely watched at 0130 GMT, with the aussie expected to react negatively if Chinese inflation dissapoints and vice versa. Expectations are for the headline CPI to rise by 2.5% y/y in September, faster than in August when it stood at 2.3%. In contrast, PPI is said to drop by 0.6 points to 3.5% y/y.

{kind=link}