Financial markets are eagerly awaiting the beginning of the Fed’s easing cycle. While the US economy enters the 11th year in the current expansion, global economic slowdown worries, a neverending trade war, and deflationary pressures have the Fed poised to deliver an insurance cut this month and possibly more in the following meetings to ensure a soft landing.

The most anticipated event of the week is Fed Chair Powell’s two days of testimony on Capitol Hill. Despite a robust labor market, the US economy is slowing down, as global growth concerns remain elevated as trade tensions show no immediate signs of easing. Equities could fall under pressure if Powell commits to only one rate cut and if he is content on waiting to see if inflation continues to stabilize and if the risks to the economy improve. The Minutes will also be released in the afternoon and should be rather dovish, but will likely take a backseat to Powell.

- Powell to reiterate Fed will act as appropriate (signalling the July meeting is live)

- Souring global trade and risks to the outlook could raise 2019 Fed rate cut expectations from 2 to 3

- Stocks receiving some support from renewed trade talk momentum

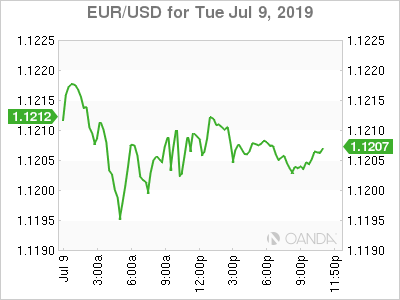

The fate of the US stock market will continue to rely on a strong dovish commitment by the Fed, continued progress with the US-China trade war and for the upcoming earnings season to keep on targeting a strong fourth quarter rebound. The dollar is potentially poised to finally breakout of its tight range against the euro on expectations the Fed will be delivering more rate cuts than the other major central banks going forward.

Trade War

Trade updates have been quiet since the G20 sideline meetings between President Trump and Xi. Markets were relieved that the two leaders resumed negotiations, with the US holding off on delivering new tariffs and reducing pressure on Huawei, while China resumed purchases of agricultural goods and the continuation of existing US tariffs.

Today, US and Chinese officials continued negotiations over the phone, in what is expected to shortly yield an in-person meeting. Both sides are politically motivated to wrap this up. China initially thought they would be better waiting out Trump, but now that it seems he is likely to get re-elected. China will try to persuade him to agree on more purchases of US goods in exchange for the limited changes on structural reform.

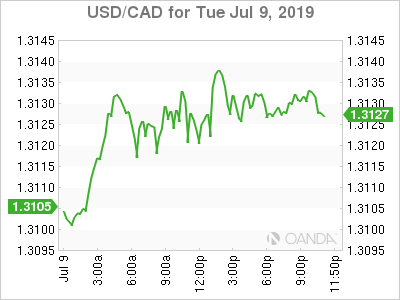

CAD

Bank of Canada is the last central bank that needs to go full dove. Canada’s economy is starting to show signs of weakness, but they should be able to wait a couple more months before having to signal the economy is in need for stimulus. Inflation and GDP remain strong, while the consumer and trade have softened. Currently markets are pricing in a 24% chance of a rate cut at the October 30th meeting.

Earnings Season

Another earnings season is upon us and this should be a very disappointing one with negative growth around 2.3% and possible further cuts to guidance. So far we have seen a severe cut to guidance from the world’s largest chemical maker, BASF. Levi Straus reported disappointing earnings that missed the lowest estimate, while Pepsico continued its string of strong results. Next week the financial report and the health of the consumer will closely be watched. In order for markets to remain confident with US stocks the US consumer needs to remain strong.

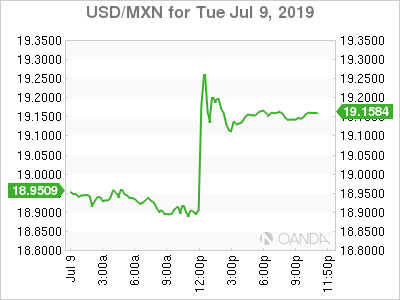

MXN

Minister Carlos Urzua surprise resignation sent the peso tumbling, marking the first major resignation in Andres Manual Lopez Obrador’s government. Urzua was well respected and his criticism of the AMLO administration highlights a growing skepticism for the government’s policies. Assistant Finance Minister Arturo Herrera was named Urzua’s replacement, a strong pick, but unlikely to dissuade the overall concerns with the Mexico’s leadership. The peso could remain vulnerable in the short-term as risks for further sovereign downgrades are growing.

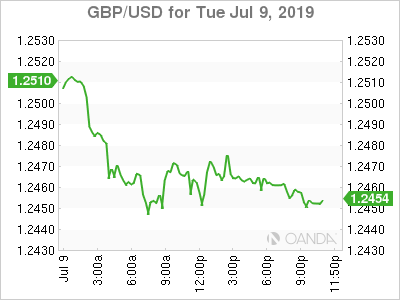

GBP

The British pound fell earlier in Europe after a survey showed economist feel the BOE will not change policy until the second quarter in 2021. Parliament was busy in debating amendments in what was supposed to possibly take the no-deal risk off the table. The amendment that did pass will require Parliament to gather every two weeks to provide updates on North Ireland, making it impossible for a new PM to suspend Parliament in order to deliver a no-deal Brexit.

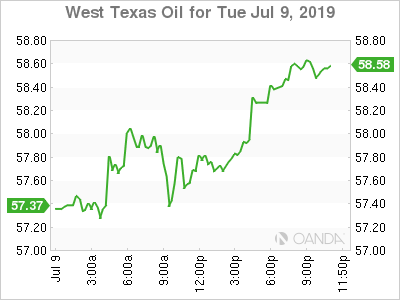

Oil

West Texas Intermediate crude surged after the weekly API oil inventories posted a third consecutive strong draw. Crude stockpiles fell 4.97 million barrels last week, possibly suggesting demand has been improving. Energy markets could continue to rise if Fed Chair Powell’s testimony to Congress reinforces bets that will cut rates will begin with the July 30-31 meeting and that more risks to the economy would likely warrant further cuts.

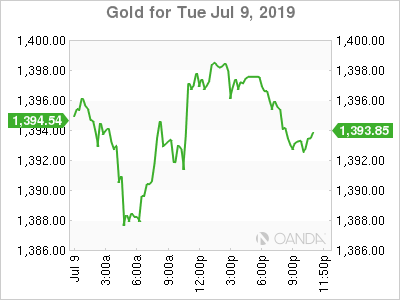

Gold

Gold is slightly softer on the stronger dollar that stemmed from the better-than-expected employment report that lowered Fed rate cut bets. The bull case for bullion remains intact as stimulus is coming from the big four central banks (Fed, ECB, PBOC, and BOJ). Earnings weakness is also expected to support the yellow metal as we start to see further cuts to guidance.