If we don’t see any major geopolitical developments today, we could see a lackluster moves in US equities and the currency markets. The focus is tentatively shifting back to the Fed and markets are nervous that the sudden rise with oil prices could derail some dovish bets.

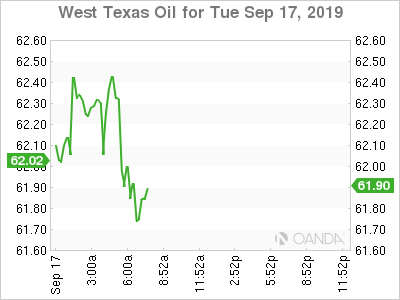

The aftermath of the worst disruption to world oil supplies on record saw oil prices tentatively ease from their recent highs as traders try to determine the longer-term impact of the drone attacks on Saudi Arabia’s oil facilities. The shock loss of 5% of global crude production has markets focused on how soon Saudi Aramco can bring back production and if we will see the US or other countries use their respective strategic reserves. The latest update shows Saudi Aramco’s initial calculation on the damages may have been to optimistic and some customers expecting early October deliveries will likely see shipments later in the month.

Crude prices will also closely react to how Saudi Arabia and the US will retaliate with Iran. The base case remains for a tit-for-tat response, which could mean strategic strikes, but not a full-blown military war. The Kingdom seems set on securing global support and the situation will remain tense over the next couple of days as UN investigators will look to confirm where the drones. It is unlikely we will see any action from the Saudis until forensics teams are completely done with their assessments. It seems that WTI clean break of its stubborn 3-month range of $50-60 a barrel will be major support that could see an eventual test of the $70 level.

Fed

Today, the Fed begins their two-day policy meeting and markets are widely expecting a 25bps rate cut this week, with the dot plot falling, as Fed Chair Powell struggles to maintain his case for a mid-cycle adjustment. Powell will probably reiterate the Fed will do what it can to sustain the expansion and that will keep the possibility for QE to be announce over the next couple meetings if one of the major geopolitical risks blows up.

The job market is starting to show some weakness, the global slowdown is not showing any signs of stabilization and Treasury curve is not in order. At the very least, we should see a 25bps cut tomorrow and one more either in October or December. Markets are starting to get used to Powell’s policy mistakes and we will be surprised if he ever decides to be preemptive in delivering stimulus. You get a better bang for your buck if you start strong and if he stumbles into an easing cycle, he will be criticized for taking so long and losing some policy effectiveness.

US-Japan Trade

It seems President Trump is not taking any chances with a third lingering trade war. The Trump administration signaled they are close to an initial trade accord over tariffs with Japan. A deal is expected over the coming weeks, but as markets have seen before with China, nothing is done until it is signed. Japan is adamant that they do not want Trump to slap any new tariffs on $50 billion of Japanese cars.

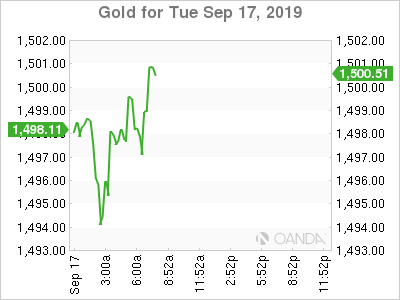

Gold

Gold is not holding onto its weekend gains as well as oil as market participants take off some positions ahead of the Fed meeting. Gold is set to rip higher if Powell does not deliver a policy mistake tomorrow. He needs to deliver at least a 25bps rate cut, not dismiss QE is a possibility, and the dot plots need to fall down enough to convince markets we are in an easing cycle.