U.S. Review

Cracks in the Foundation?

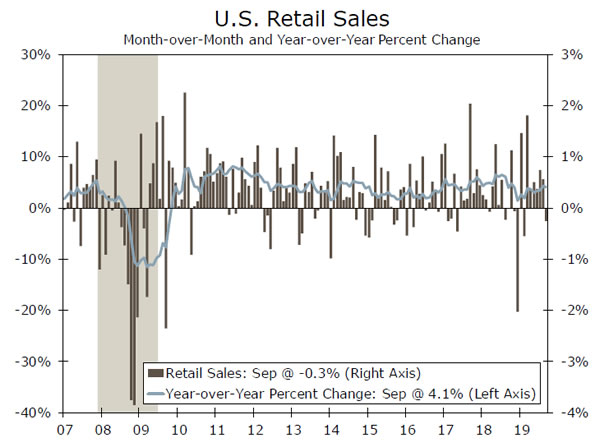

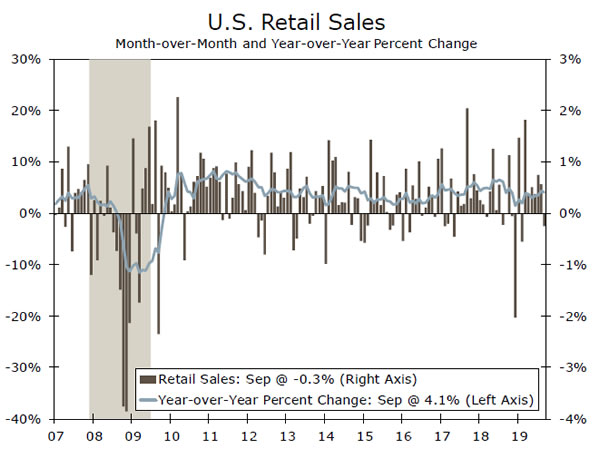

- Personal consumption is still on track for a solid Q3, but retail sales declined in September for the first time in seven months.

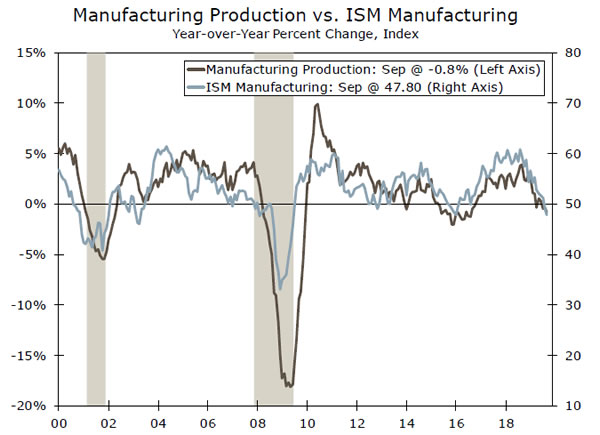

- Manufacturing data were certainly influenced by the GM strike, but output has now fallen in six months this year, and survey evidence has yet to point to a meaningful pickup.

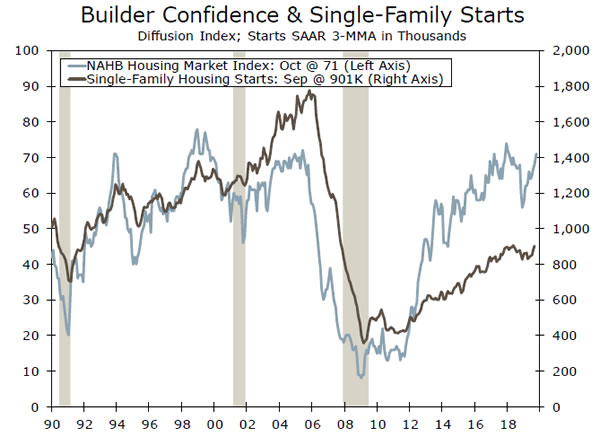

- Single-family housing starts rose for the fourth consecutive month. Housing should positively contribute to GDP growth in Q3 for the first time in almost two years.

- The lack of a pushback on market expectations from the Fed speakers gives us increasing confidence that the FOMC will cut the fed funds rate by 25 bps at its October 29-30 meeting.

Cracks in the Foundation?

Economic data largely came in below expectations this week, as evidence of a broadening slowdown continues to mount.

Personal consumption, which comprises roughly 70% of overall U.S. GDP, has proved remarkably resilient under the cloud of trade uncertainty and the darkening economic picture overseas. However, retail sales fell in September for the first time in seven months. The 0.3% decline in headline sales was dragged down by a sharp drop in auto sales, but the flat reading for control group sales (versus consensus expectations of a 0.3% increase) is one of the first concrete signs of a crack in the consumer sector. Leading indicators of consumer spending have been pointing to a slowdown—the Conference Board and University of Michigan surveys of consumer confidence have stalled and the pace of job growth has slowed—and we may finally be seeing it borne out in the hard data. Still, PCE is on track for a solid 2.4% rise in Q3, but we expect the deterioration in fundamentals will pull growth below 2% by Q4.

The manufacturing sector bore the brunt of the slowdown much sooner—and more deeply—and is showing minimal signs of picking up. Overall industrial and manufacturing production missed expectations in September, falling 0.4% and 0.5%, respectively. The GM strike was behind the 4.2% drop in autos and parts output, but even excluding autos, output was still down on the month and manufacturing has posted six monthly declines this year. GM and the UAW have reached a tentative agreement, but the nature of the approval process and the reporting calendar suggests manufacturing data will still see a major strike effect in October. That said, the biggest threat to the factory sector comes not from Detroit, but rather from overseas and from the political and policy maelstrom in Washington, D.C. Markets bounced on the “phase one” trade deal announced last Friday, but the details remain highly vague, and we suspect no major progress will be made until the Asia-Pacific Economic Cooperation (APEC) meeting in Chile in mid-November, if not even later.

The growing signs of a gradual slowdown in consumer spending indicate the economy is losing the biggest offset to the weakness in manufacturing and business investment, which are already outright declining. However, it has gained another. Housing, consistently the laggard in this expansion, is now arguably the strongest sector. Residential investment is nearly certain to positively contribute to GDP growth in Q3 for the first time in six quarters. The headline drop in housing starts in September was entirely due to the wildly volatile apartment data—which is in fact topping out a bit—but single-family starts rose for the fourth consecutive month, and the NAHB survey, a measure of homebuilder confidence, jumped to a 20-month high.

Still, housing directly comprises only around 4% of the economy, and its capacity to lift overall GDP growth is limited. The prospect of the economic malaise spreading from manufacturing to the consumer is a major driver of the 80% probability the market is pricing in for an October Fed rate cut. With the pre-FOMC meeting blackout period starting tomorrow, the lack of a pushback on market expectations from Fed speakers gives us increasing confidence that the FOMC will cut the fed funds rate by 25 bps at its October 29-30 meeting.

U.S. Outlook

Existing Home Sales • Tuesday

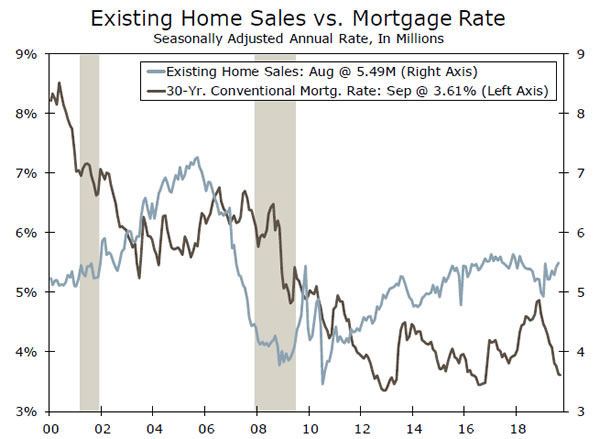

The effects of lower mortgage rates are becoming more noticeable in the housing market. Existing home sales beat expectations and rose 1.3% during August. Although the gain was somewhat modest by historical standards, resales have now risen in back-to-back months for the first time since 2017. Moreover, sales strengthened in every region except the West during August.

The latest housing data have been encouraging, but we expect resales likely pulled back a bit during September. The pending home sales index, which leads closings by a month or two, fell 2.5% during July and only registered a partial 1.6% rebound in August. That said, mortgage rates continue to trend downward and averaged 3.6% during September. Through the monthly volatility, improved buying conditions should continue to entice buyers back into the market, and we expect existing home sales to trend higher in coming months.

Previous: 5.49M Wells Fargo: 5.51M Consensus: 5.45M

New Home Sales • Thursday

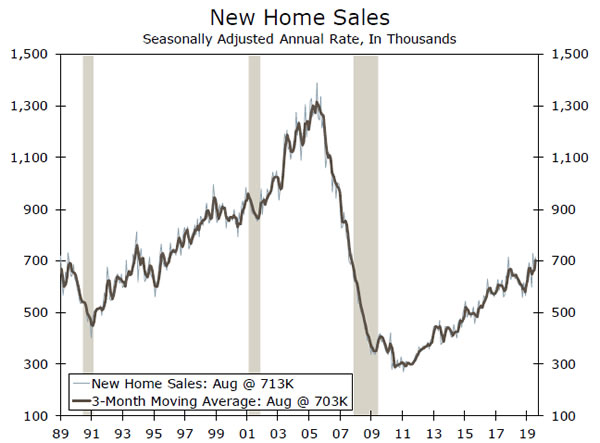

Lower mortgage rates have also been a boon for new home sales. During August, new home sales rose to a 713,000-unit pace, a 7.1% monthly surge. What’s more, sales are up 6.4% on a year-todate basis, reflecting a clear upward trend for the year. The improving pace, which was helped by builders offering substantial discounts, has helped clear inventories. Months’ supply, a measure of how quickly inventories would clear at the present sales-pace, came in at 5.5 months, down from 7.4 months in December.

Overall, we expect the recent upshift in new home sales to continue, with new sales benefiting from many of the same tailwinds currently lifting the market for existing homes. In addition, many builders have successfully shifted toward constructing more homes at lower price points, which will serve to satiate the fast-growing demand for entry-level homes and boost sales even further this year.

Previous: 713K Wells Fargo: 703K Consensus: 710K

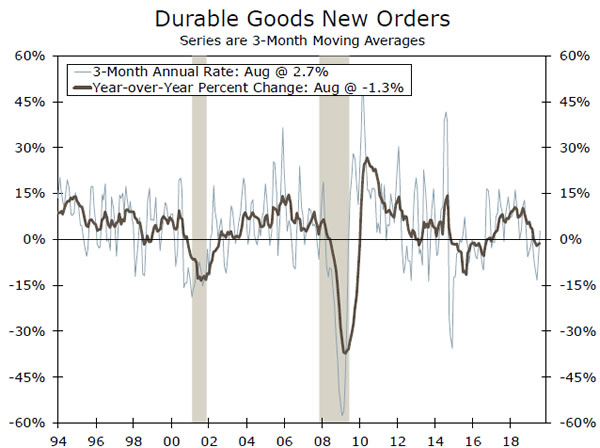

Durable Goods Orders • Thursday

Capital spending remains in the doldrums. The surprising 0.2% gain in durable goods orders during August was mostly the result of a substantial 15.4% jump in defense orders. Excluding the defense sector, orders fell 0.6%, which is more consistent with the deterioration in manufacturing PMIs and heated trade negotiations in August. Nondefense capex orders excluding aircraft also edged down during the month, which further reflects the downshift in private capital spending.

A number of factors will weigh on durable goods orders and capital spending more broadly over the coming months. Aside from Boeing’s 737 MAX issues still remaining unresolved and the strike at GM, trade uncertainty and languishing global economic growth have led to a slide in manufacturers and small businesses plans for capital spending, meaning durable goods orders should continue to struggle.

Previous: 0.2% Wells Fargo: -0.9% Consensus: -0.5% (Month-over-Month)

Global Review

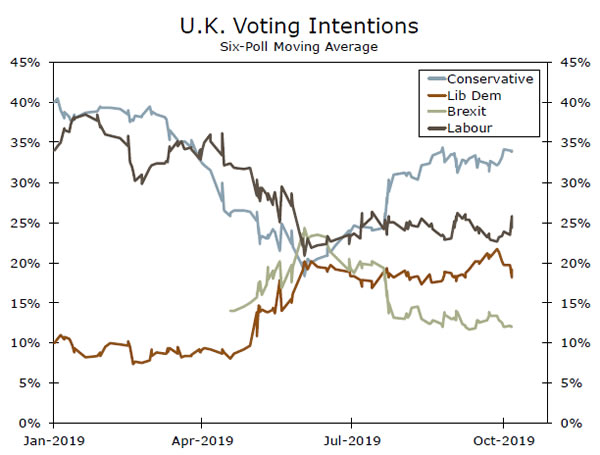

A Breakthrough on Brexit, or Another False Start?

- UK PM Boris Johnson and EU leaders announced they had struck a Brexit deal, an encouraging development ahead of the October 31 deadline by which the UK must either leave the EU or once again request an extension.

- The path forward is precarious, however, as the UK Parliament is set to vote on the deal in an emergency session on Saturday. The prospects for the deal’s passage remains far from assured.

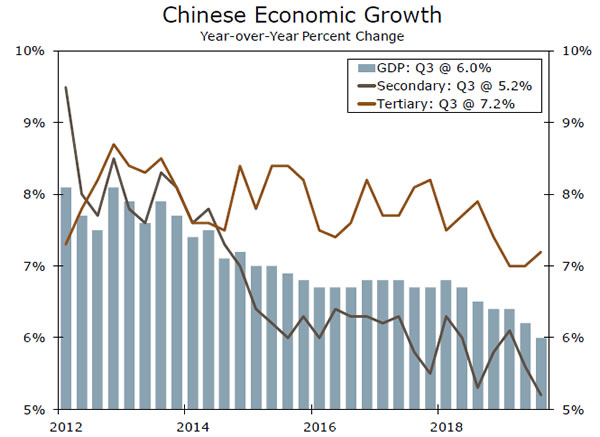

- Chinese Q3 GDP growth slowed further to 6.0% year-over-year, although September retail and industrial activity suggest the quarter ended on a firmer note. However, given a measured policy response, the overall growth slowdown should continue.

A Breakthrough on Brexit, or Another False Start?

Brexit headlines ran rampant this week, as optimism rose on the belief that there could be a light at the end of the Brexit tunnel. Specifically, Prime Minister Boris Johnson and EU leaders announced they had struck a deal acceptable to both parties, an encouraging development ahead of the October 31 deadline by which the UK must either leave the EU or once again request an extension. It is worth remembering, however, that this is not the first time a deal has been struck: Theresa May’s previous deal was also one between her government and the EU. Things came to a screeching halt in Parliament, where May was unable to find a majority to pass it.

Similarly, the biggest roadblock remaining for the current deal is one that can find a majority in the UK parliament. Specifically, the deal’s prospects may rest in the hands of the Democratic Unionist Party (DUP), a relatively small party from Northern Ireland that generally support Johnson’s conservative government. What exactly is it that the DUP are so concerned about? The answer is extremely nuanced, but lies mainly in the fact that the deal treats Northern Ireland significantly differently than the rest of the United Kingdom. Specifically, it implies that there will eventually be a customs border between Northern Ireland and the rest of the United Kingdom, with tariffs applied as needed for goods destined for or originating from Ireland

So where do things go from here? PM Johnson’s deal is set to be voted on this Saturday in an emergency Parliamentary session. If it passes, the UK would officially exit the EU on October 31, and could begin the next phase of the negotiations, namely what the United Kingdom’s relationship with Europe will look like going forward. Importantly, however, a rejected deal does not necessarily lead to a no-deal Brexit. Instead, the most likely next steps, in our view, would be that PM Johnson would ask the EU for an extension of the current October 31 Brexit deadline, probably around three months. We then think that an election would be held later this year, to be contested along Brexit lines.

Chinese Growth Still on a Slowing Path

The latest readings on the health of the Chinese economy indicate that economic growth remains on a steadily slowing path. For Q3, GDP rose 1.5% quarter-over-quarter and slowed to 6.0% yearover- year. Growth in tertiary (or service sector) activity firmed modestly to 7.2%, while growth in secondary (or industrial) activity slowed noticeably, to just 5.2%.

While the indications were for an overall growth slowdown in Q3, the quarter appeared to end on a slightly more encouraging note. Retail sales rose 7.8% year-over-year, while industrial output jumped 5.8%. This past week also saw a quickening in the September CPI to 3.0% year-over-year, and a firming in money and loan growth. That said, we continue to believe that Chinese fiscal and monetary policy will be calibrated to cushion the economic slowdown rather than prompt a growth upswing. Accordingly, we see Chinese GDP growth slowing further, to 5.8% in 2020 and 5.6% in 2021.

Global Outlook

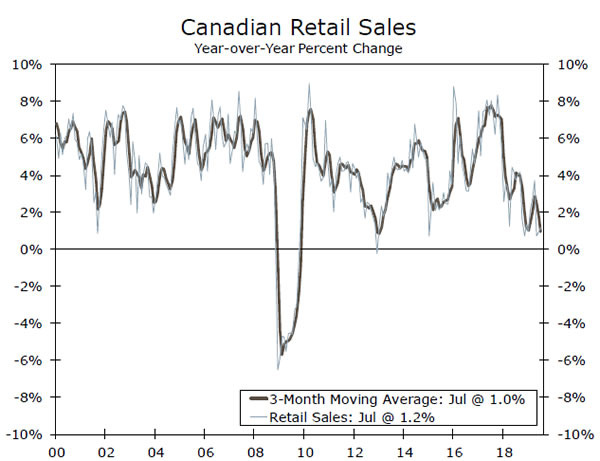

Canadian Retail Sales • Tuesday

Retail sales in Canada have decelerated sharply from their peak in late 2017, and at present are up just 1.2% year-over-year. This jives with Canadian consumer spending growth, which also remains relatively slow at just 1.4% over the year in Q2, but does not square with labor market data. Employment growth is up a solid 2.4% yearover- year, and it has not just been part-time workers; full-time employment growth in Canada has risen 2.2% over the past year. Furthermore, Canadian average hourly earnings growth was 4.3% year-over-year in September, more than a percentage point stronger than in the United States.

Why has the strong Canadian labor market not translated into faster consumption growth? Perhaps the answer lies in Canadian household debt levels, which are much higher than they are in the United States. If households are devoting more income to servicing their debt, this could be offsetting the gains they are seeing in employment and earnings growth.

Previous: 0.4% (Month-over-Month)

South Korea Q3 GDP • Wednesday

A few months ago, we published a report that examined how some of the world’s most China-dependent economies were performing in light of the U.S.-China trade war. South Korea was one of these countries, as nearly 8% of the country’s total value added is derived from final demand in China. Since then, we learned that real GDP growth in South Korea bounced back a bit in Q2, rising 2.0% yearover- year from 1.7% in Q1.

The recent stabilization in South Korean growth is encouraging, as it ostensibly signals that China’s slowdown remains manageable. Although, that may be true, much of the recent improvement in South Korea likely stems from the government’s fiscal stimulus efforts. Government consumption in South Korea rose at a 2.5% annualized pace in Q2, and 7.3% year-over-year. Stronger export and/or investment numbers in next week’s GDP print would be a more encouraging sign.

Previous: 2.0% Consensus: 2.0% (Year-over-Year)

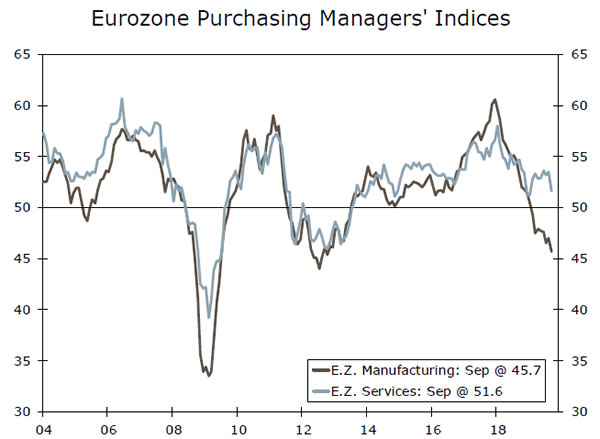

European Central Bank Meeting • Thursday

Since the European Central Bank (ECB) last met in September, the economic data have if anything gotten worse. The purchasing manager indices for September were dreadful, with the services index falling 1.9 points from August. Meanwhile, the manufacturing PMI also declined and is now testing the lows reached during the worst of the 2011-2012 European sovereign debt crisis.

We do not think the ECB will ease policy further at this upcoming meeting, but do we think another 10 bps rate cut is coming in December. Past that, we are skeptical the ECB will do much more, as its policy capacity with typical monetary policy tools, like rate cuts and QE, are clearly running low. At present, the Eurozone is running a consolidated budget deficit of about 1%, with some countries, such as Germany, in surplus. It looks increasingly likely that any meaningful positive policy shock will need to come from the fiscal side of the equation.

Previous: -0.50% Wells Fargo: -0.50% Consensus: -0.50% (Deposit Rate)

Point of View

Interest Rate Watch

Some of All Fears Subsides

Going into the fall it looked as though financial markets were going to fight a wall of worry, as issues such as the China trade negotiations, Brexit and the manufacturing slowdown continued to stoke uncertainty and threaten to the pull the economy into a recession. Such talk has now faded considerably as some semblance of a truce has opened in trade negotiations and the odds of a hard Brexit have subsided. Signals from the manufacturing sector are also no longer universally negative and manufacturing payrolls are proving resilient despite temporary setbacks at Boeing and GM. Moreover, home sales and new home construction are perking up, which should feed through to retail sales, financial services and building products producers.

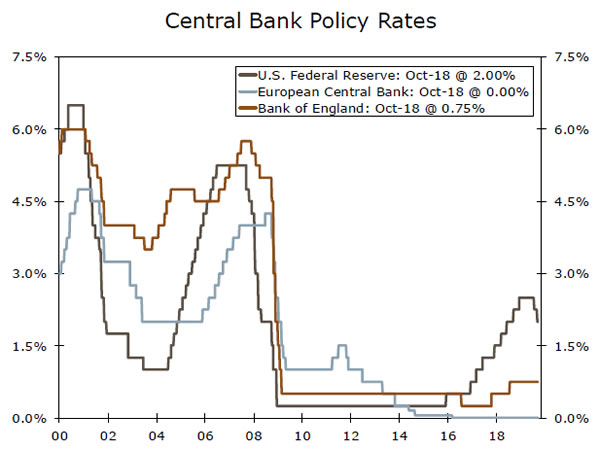

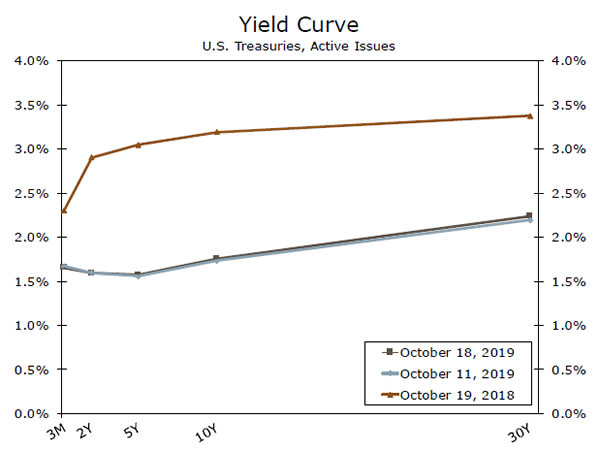

The less ominous economic picture has pulled bond yields higher and further normalized the yield curve. The Fed’s decision to purchase $60 billion a month of T-bills has helped pull the yield on the three-month bill back below the yield on the 10-year note. The yield curve still has some kinks in it, as there are plenty of doubters about the Fed’s intentions to cut the federal funds rate further. To be certain, comments by certain Fed officials, including Chicago FRB President Charlie Evans, suggest this month’s decision is not baked in the cake. Several Fed presidents feel uncomfortable cutting interest rates with the unemployment rate so low and the CPI, and several alternative measures of inflation, recently showing more signs of life.

We continue to expect the Fed to cut the federal funds rate two more times. The first quarter-point cut will likely be at the October 29-30 meeting but might be delayed given the timing of Brexit. Fed Chair Powell does not appear to be put off by the reportedly low unemployment rate and feels the Fed has yet met its maximum employment objective. The Fed has spent a great deal of time in recent years meeting with folks outside of Wall Street to listen to the views and concerns about the economy. They seem to view the greatest risk of a policy mistake today would be not cutting short-term rates enough to offset slower global growth rather than cutting them too much and stoking some future inflation.

Credit Market Insights

Foreign Holdings of Treasuries Surge

Data released by the U.S. Treasury Department on Wednesday showed $70.5 billion of net foreign capital flowed into the United States in August. This was driven by a $122 billion net inflow of private foreign capital, which was somewhat offset by $51 billion in net sales by foreign official institutions. Wednesday’s report also showed foreign buyers held a record $6.86 trillion worth of U.S. government bonds. The 3.4% increase in August was the largest monthly increase in nine years. This jump coincided with a rise in the amount of negative yielding debt, which peaked at more than $17 trillion in late August, according to the Bloomberg Barclays index. While foreign official institutions account for the majority of foreign Treasury holdings, August’s increase was primarily due to private buyers.

Overall foreign capital inflows have slowed through August, but foreign buying of U.S. Treasury securities has increased $448.3 billion compared to last year’s pace through August. While this is likely driven by higher U.S. interest rates and a strong dollar, it also helps illustrate the perceived resilience of the U.S. economy in the face of slower growth abroad. There is good reason to believe that the U.S. may be better insulated from the global manufacturing slowdown. As one of our recent reports points out, the industrial sector in the U.S. accounts for a much smaller share of output and employment compared to other developed economies.

Topic of the Week

Brexit Update: Key Takeaways from “The Deal”

A new Brexit deal has been reached, and is set to be voted on this Saturday in an emergency Parliamentary session. However, the Democratic Unionist Party (DUP) has indicated it will not support the deal in its current form. The DUP’s 10 votes may not seem like a lot, but the support of a small group of Conservative lawmakers is contingent upon DUP support. Recall also that Prime Minister Boris Johnson lost his parliamentary majority weeks ago. What exactly is it that the DUP are so concerned about? The answer is extremely nuanced, but lies mainly in the fact that the deal treats Northern Ireland significantly differently than the rest of the United Kingdom. Specifically, it implies that there will eventually be a customs border between Northern Ireland and the rest of the UK, with tariffs applied as needed for goods destined for or originating from Ireland. In addition, the DUP do not feel as though they will have enough of a say in the arrangements. In practice, the deal offers Northern Ireland a right to veto these arrangements down the road, but the DUP does not have sufficient seats in Stormont (Northern Ireland legislative body) to reject the arrangements if it desires to.

Without the DUP’s support, PM Johnson will likely not be able to pass the deal and probably be forced to ask for an extension of the October 31 deadline, probably around three months. We then think that an election would be held later this year, to be contested along Brexit lines.

Crucially, however, the fact that the UK and EU reached a deal changes the calculus and scenario analysis meaningfully if an election takes place. The deal struck seems to have the support of at least a critical mass of Conservative MPs, so if they win a majority in Parliament, they may be able to simply push this deal through without having to worry about the interests of other factions. Of course, it is still possible that some Conservatives could scupper the deal even if the party wins an outright majority in any new election. However, while this caveat curbs our optimism somewhat, we do now see a higher chance of an eventual “deal” outcome.