- IMF to revise up Chinese growth from 5.8% to around 6% after phase-one deal.

- Data on industrial production and retail sales underpin growth of at least 6% in Q4 and early 2020. We see more upside in Chinese equities.

- Signing of a phase-one deal is still on track for early January. Xi Jinping will not join Davos meeting, which could have been a Xi-Trump signing opportunity.

- USD/CNY treads water around 7-level. We look for more downside in 2020.

Growth estimates revised higher following phase-one deal

Following the US-China phase-one deal, the IMF is set to revise its China GDP forecast higher for 2020 to around 6% from 5.8%. This was the message from the new IMF Director Kristalina Georgieva in an interview with Caixin. We have also seen other houses revise their forecasts higher on the back of the deal. Consensus seems to be forming around 6% growth in 2020. The signal coming out of the recent China Economic Work Conference was also that the new growth target for 2020 will be around 6%. It will not be revealed officially, though, until the National People’s Congress starting on 5 March.

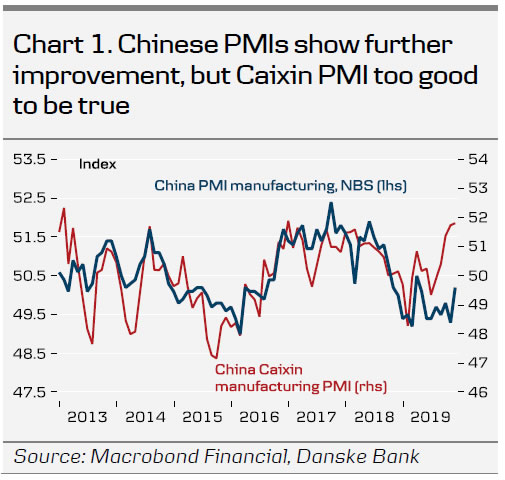

Data on industrial production surprised to the upside rising to 6.2% y/y in November from 4.7% y/y in October. As chart 1 shows, it points to GDP growth towards the top of the 6-6½% target range and lowers the risk of GDP growth falling below 6%. Chinese retail sales for November were also released this week and they showed an increase to 8.0% y/y from 7.2% y/y in October. The data is volatile, though, and more generally shows a picture of stabilisation in the 7-8% range over the past six months.

China refrained from lowering the policy rate (Loan Prime Rate) this week in a sign that it is reluctant to ease policy further. However, efforts are being made to get more credit through to the private sector, which continues to be starved of credit access. The State Council, China’s cabinet, called on banks to cut financing costs by 0.5 percentage points next year for small and micro businesses. It also instructed five of the country’s largest state-owned commercial banks to increase the value of loans made to these companies by at least 20% next year.

Comment. We saw the first sign of a turn in the Chinese business cycle in October, see China Weekly Letter – Is the Chinese business cycle turning?, 10 October 2019. However, a continued moderate recovery has hinged on a de-escalation of the US-China trade war and this is exactly what we got with the phase-one deal. Our GDP forecast for 2020 has been 6.0% for some time based on the assumption of easing trade tensions and increasing effects of the policy stimulus. We stick to this view and now see risks as more balanced after having been mainly to the downside.

We expect China to hold back on further stimulus but at the same time continue to take structural steps to improve credit availability for the private sector, especially small companies which have struggled to get funding from state-owned banks in the past.

Global stock markets have cheered the positive development on the trade front and signs of a turn in the business cycle. The same is the case in China, where the broad CSI300 index has increased to a new cycle high. We see more upside in the coming quarters.

Phase-one deal on track for signing in January

The news flow on the finalisation of the phase-one deal has been quite limited but the message is still that a deal is going to be signed in early January. US Treasury Secretary Stephen Mnuchin said to CNBC on Thursday that he was ‘very confident‘ the deal will be signed as scheduled. The detailed content of the agreement will be made public after the deal is signed according to Gao Feng, a spokesman from the Chinese commerce ministry.

Chinese President Xi Jinping is not going to attend this year’s Davos meetings scheduled for 21 to 24 January. It eliminates an option for a face-to-face meeting between Xi and US President Donald Trump, which could have been an opportunity for signing the deal. The plan is still that Chinese Vice-premier Liu He will sign the deal in Washington with US Trade Representative Robert Lighthizer in early January.

Comment: It is interesting that Xi apparently is not going to meet Trump at Davos. It leaves the impression that while China wants to close one battle with the US, the trade war, China is clearly unhappy about US confrontation with China in many other areas such as technology, Hong Kong and Xinjiang. A signing ceremony would also attract more attention to a trade deal, which is not popular among all circles in China. It has been negotiated on the back of what is seen as US bullying and in some respects it rewards Trump as China commits to buy a specific and large amount of agricultural goods, which is clearly against the principle of market economics and most likely in violation of WTO rules. After the phase-one deal is signed the two sides will move to phase-two talks immediately. These will be much more difficult, but we could see sub-deals as part of phase-two.

USD/CNY treads water but should fall further in 2020

The CNY has traded in close correlation with developments in the US-China trade war. When Trump pushed the tariff button once again over the summer, USD/CNY jumped higher from below 6.90 to close to 7.20. But since the phase-one talks starting in the autumn the CNY has regained some of the lost territory. Following the announcement of the phase-one deal USD/CNY dropped but has since been treading water around the 7-level awaiting further developments.

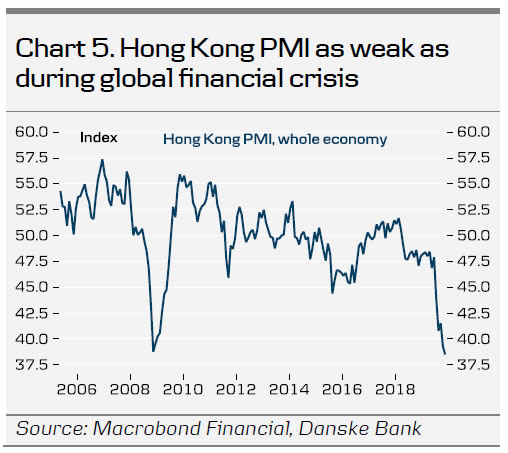

Comment. We look for further downside in USD/CNY towards 6.8 in 2020 due to our view of easing trade tensions and moderate recovery in China. It will probably not be such a straight line as we depict in chart 5, though, as we expect bumps in the road in trade talks.

Other China news this week:

5G is the big thing in China now, with a focus on unlocking further digital development and the internet-of-things. State media writes frequently on the benefits and opportunities of 5G.

At the celebration of the 20-year anniversary of its return to Chinese rule, Xi Jinping praised Macau as a good example of ‘one country, two systems’.

{kind=link}