U.S. Review: Raising the Bar Even Further

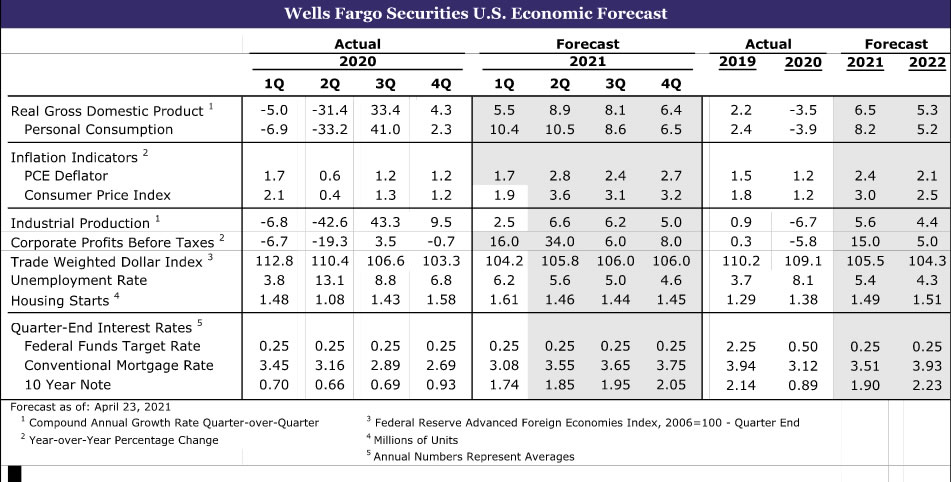

- This week’s lighter economic calendar allowed forecasters more time to assess the implications from the prior week’s blowout retail sales report. We have revised our forecast for Q1 growth up to a 5.5% pace from 4.8% previously, and growth for the year is now pegged at 6.5%, up from 6.4%.

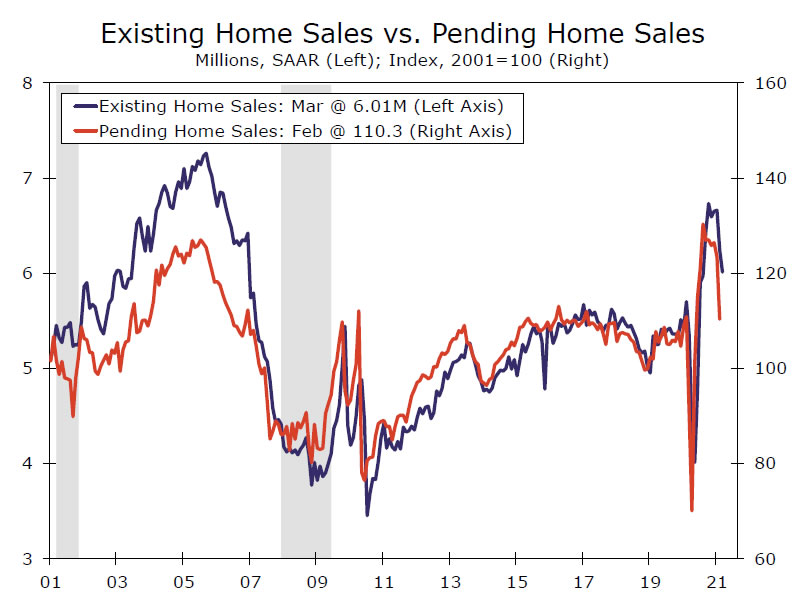

- Sales of existing homes fell 3.7% in March, but realtors are selling homes faster than ever and often well above the asking price. Inventories of homes remain near a record low, and the median price of an existing home surged 17.2% over the past year.

- Initial unemployment claims fell more than expected during the latest week, dropping to 547,000 claims—the lowest level since the pandemic began. The four-week moving average for the April survey week was 651,000, down from 751,750 from the March survey week, setting the stage for another strong employment report.

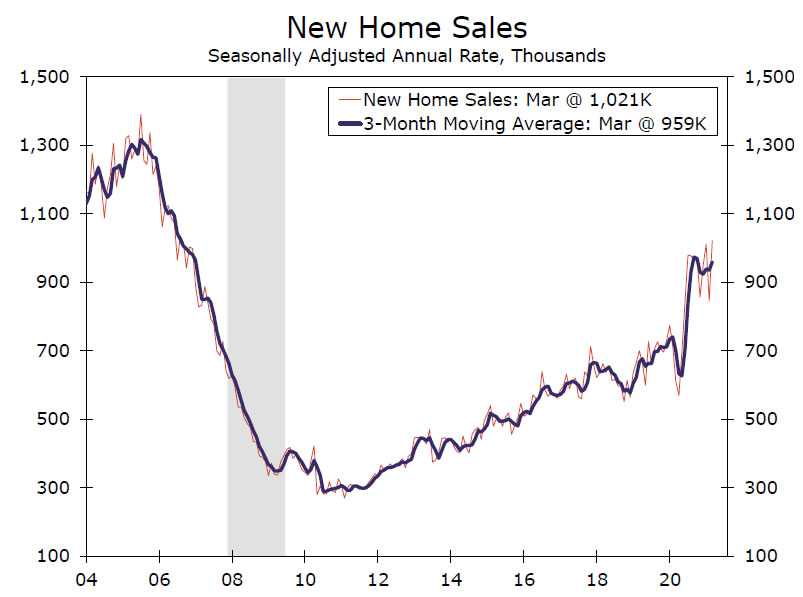

- New home sales surged 20.7% in March, and sales for February were revised significantly higher. Builders report exceptionally strong demand and are selling homes faster than they can build them.

International Review: Bank of Canada Tightens Modestly, European Central Bank Stands Pat

- The Bank of Canada took an initial step toward removing monetary policy accommodation, while the European Central Bank kept all of its current accommodation in place.

- There are some small signs of green shoots in Europe, as the manufacturing PMI for April remained high and the services PMI rose back above 50 for the first time since August.

Interest Rate Watch: Looking for “Substantial” Clues

- Next week’s FOMC meeting is not expected to bring any major policy changes. We expect Chair Powell, however, to be pressed on what might constitute “substantial further progress” on the Fed’s employment and price stability goals in his press conference, as the timing around tapering asset purchases comes under more focus.

Topic of the Week: A Quicker Rebound

- Our best read suggests that first quarter consumer and business spending figures will now come in stronger than we had penciled in for our April 7 forecast update.

U.S. Review

Raising the Bar Even Further

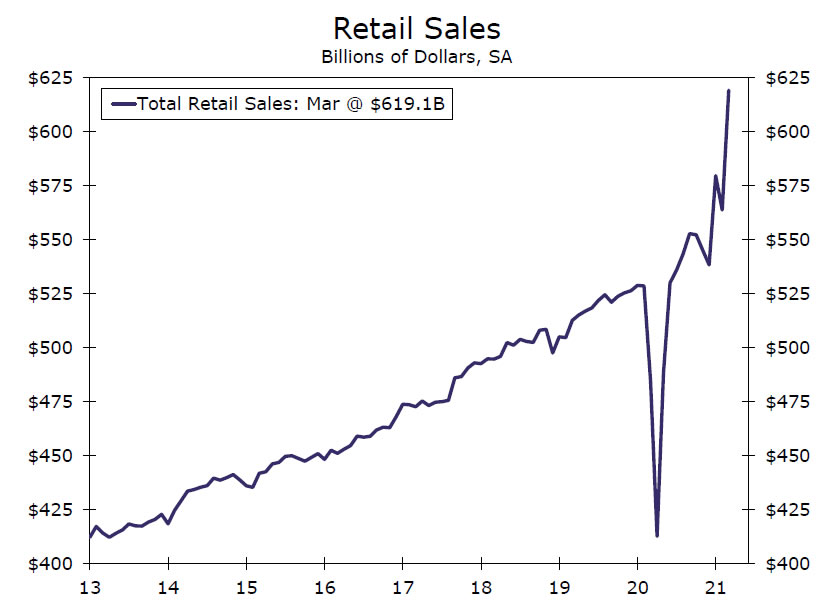

The parade of huge economic gains continued this week, with the biggest news again coming in the latter part of the week. April began with the blowout March employment report, which showed the economy adding 916,000 jobs and the unemployment rate falling to 6.0%. That was followed by a blowout 9.8% rise in retail sales and a 19.4% rebound in housing starts. This week saw jobless claims plummet to their lowest level since the pandemic began and ended with this morning’s spectacular new home sales report, which showed sales surging 20.7% to a 1.021 million-unit pace. The confluence of all of these stronger-than-expected reports has prompted us to raise our estimates for economic growth this year. The mini boom we were expecting is arriving early, and consumer spending and business investment both look to be stronger than our previous above-consensus forecast.

Our housing forecast was already fairly lofty, with new home sales expected to rise 9.9% and housing starts expected to rise 6.8% to 1.49 million units. We would raise our housing forecast further if we thought the industry could ramp up construction even more. As it is, the industry is extremely supply constrained, with housing lots, labor and lumber all posing significant constraints. We expect sales and new construction to moderate from their recent pace. Demand is not the problem, however. New home sales are every bit as strong as this morning’s headline-grabbing 20.7% increase suggests. Builders are selling out new communities in days and are often having to limit sales, even after raising prices. The strength in housing demand is rapidly approaching historic proportions, something the industry and regulatory environment are unprepared for.

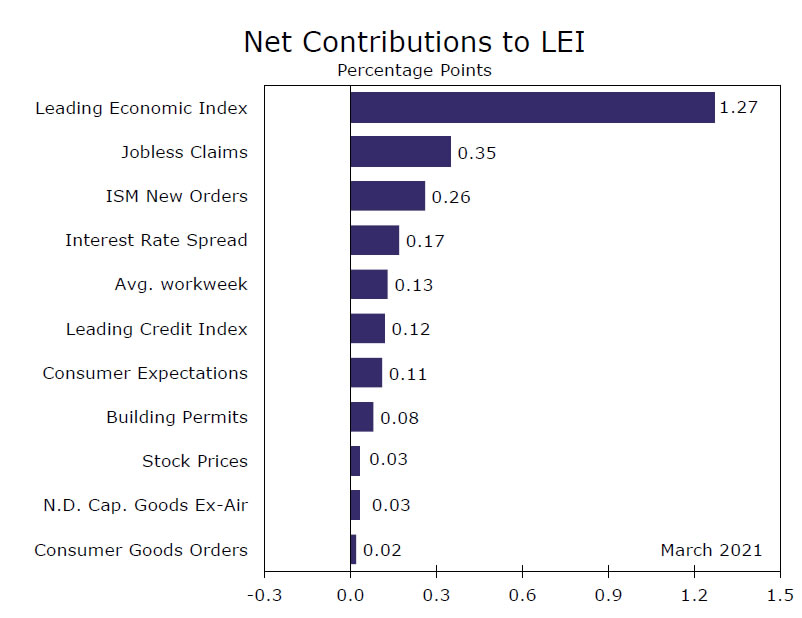

The Leading Economic Index (LEI) jumped 1.3% in March. Gains were broad-based, as the services and manufacturing sectors saw record-breaking improvement over the month. Improvement in initial jobless claims provided the largest boost, 0.35 percentage points, to the index over the month. Fewer people filing claims is good news for the economy, and first-time jobless claims finally dipped below 700,000 in the third week in March. Since then, claims have trended lower and recently hit a new pandemic low of 547,000 in the week ended April 16. Strengthening labor market conditions are setting the stage for strong employment and LEI reports next month.

ISM new orders contributed an impressive 0.26 percentage points to the LEI’s headline, as the index rose to 68 in March, its highest in just over 16 years. The manufacturing and services sectors had a stellar month, as the ISM manufacturing index rose to a 37-year high of 64.7 and the services index followed closely at 63.7. The manufacturing sector is facing some headwinds, however, as supply shortages and rising material costs have affected producers’ ability to meet demand. We expect supply constraints to ease modestly in the second half of this year.

Existing home sales slipped 3.7% in March, falling to a 6.01 million-unit pace. The decline was slightly larger than expected and comes one month after extreme weather severely cut into economic activity across Texas and other parts of the South and Midwest. Existing home sales reflect closings, which tend to occur 4-6 weeks after a purchase contract is signed. Pending home sales, which capture purchase contracts and lead existing home sales, dropped 10.6% in February. The steep decline in pending sales suggests existing sales may soften further in coming months.

Existing home sales fell in all four regions of the country in March, and would have likely been higher if there were more homes available for sale. The persistence of record-low inventories is largely due to the unusual circumstances brought on by the pandemic. With COVID keeping people at home, people found out they needed more space. More people wanted to buy homes but fewer wanted to sell. The imbalance in the supply and demand for housing has led to a surge in home prices, which are likely pushing some buyers to the sidelines. The median price of an existing home has risen 17.2% over the past year to $329,100. Prices for single-family homes surged 18.4% over the past year to $334,500, both marking new historic highs. For more information on our outlook for housing, please see Housing Chartbook: April 2021.

U.S. Outlook

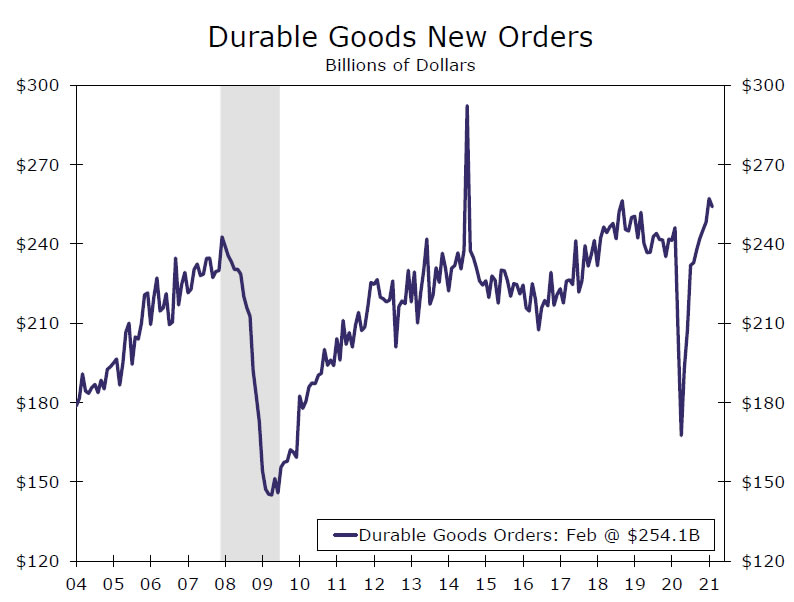

Durable Goods Orders • Monday

We expect new orders for durable goods continued to roll in last month and rose 3.5% compared to February. Record-low business and retail inventories amid a pickup in demand—retail sales posted the second-largest monthly gain on record in March—suggest durable orders were strong. Aircraft should provide another considerable lift to the headline this month, based on data from Boeing. Excluding aircraft, we forecast a still-strong but more modest 1.8% monthly gain. Ongoing supply issues are constraining production and delaying shipments, but to the extent they are also affecting orders, supply issues could be the source of a miss to the downside in March. A considerable pickup in manufacturing hiring last month, however, points to stronger activity and suggests labor shortages may at least be beginning to abate. Ultimately, once global supply chains normalize, we are forecasting a faster rebound for manufacturing than what occurred in the wake of the past two recessions.

Previous: -1.2%; Wells Fargo: 3.5%; Consensus: 2.4% (Month-over-Month)

FOMC Monetary Policy Meeting • Wednesday

We do not expect the Federal Open Market Committee (FOMC) to announce any major policy changes at the conclusion of its policy meeting on Wednesday. For more detail of what we expect, please see our Interest Rate Watch section.

Previous: 0.25%; Wells Fargo: 0.25%; Consensus: 0.25% (Fed Funds Rate, Upper Bound)

Q1 Real GDP • Thursday

We updated our forecast for first quarter real GDP growth and now expect the U.S. economy expanded at a 5.5% annualized rate. See the Topic of the Week section for details behind our upward revision.

Previous: 4.3%; Wells Fargo: 5.5%; Consensus: 6.5% (Quarter-over-Quarter, Annualized)

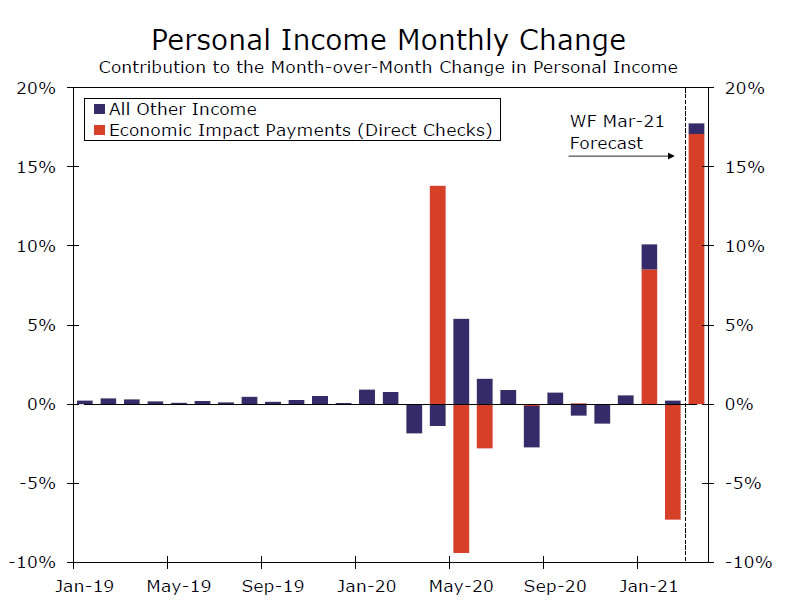

Personal Income & Spending • Friday

All signs suggest that personal income and spending surged in March. Income received a significant lift from the latest round of direct checks designated under the American Rescue Plan. We estimate nearly 80% of the latest round of checks reached bank accounts in March based on data from the Bureau of the Fiscal Service. Checks were more than double the size of January’s, and by our estimates, contributed 17% to income growth and were responsible for nearly all of the monthly gain we forecast. Excluding government transfers, personal income likely rose a more modest 0.7%. Regardless, the income story is still very much one of fiscal transfer. As was the case with the monthly surge in January (when a bulk of the December checks were sent) and payback in February, we expect the same to unfold in March and then April. Still, the stimulus to date has more than offset lost income from wages and salaries, and through the monthly noise, it will leave consumers in a generally optimal position to spend as the economy continues to reopen.

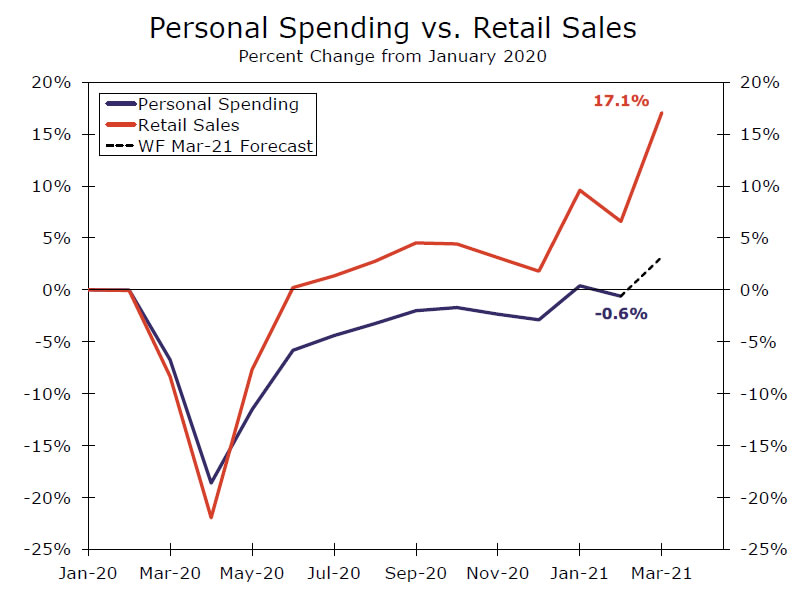

The double-digit pop in income also likely provided a sizable lift to personal spending during the month. Retail sales surged in March, with every type of retailer reporting stellar sales growth. We forecast the more-encompassing personal spending data, which includes the much larger and more depressed services sector, advanced nearly 4% during the month. High-frequency data on visits to retail locations and proxies for services activity specifically, such as seated diners from OpenTable and people passing through TSA check points, suggest the service sector is reawakening. We are of the opinion that as vaccinations continue to pick up, more consumers will come out in droves as pent-up demand for many services temporarily shelved for more than a year is unleashed. Trillions in excess household savings should provide added cushion to consumer spending, though our bullish call on consumption this year does not rely on a large draw-down in accumulated savings.

Previous: -7.1% & -1.0%; Wells Fargo: 17.7% & 3.8%; Consensus: 20.0% & 4.3%

International Review

Bank of Canada Tightens Modestly, European Central Bank Stands Pat

In a widely expected move, the Bank of Canada (BoC) adjusted its monetary policy stance at this week’s meeting, saying that from late April it would reduce its weekly pace of net Canadian government bond purchases to C$3 billion per week, from the current pace of C$4 billion per week. The central bank also held its policy interest rate steady at 0.25%.

Canada’s vaccine rollout has lagged behind the United States’, and it has had to deal with a new wave of COVID infections. The BoC acknowledged this new wave but still said it expects the economic recovery to be stronger than it forecast in January. In particular, Q1-2021 GDP growth looks to be much stronger than expected. For full-year 2021, the BoC forecasts GDP growth of 6.5% (compared to a forecast of 4.0% in January) before GDP growth moderates to 3.7% in 2022 and 3.2% in 2023.

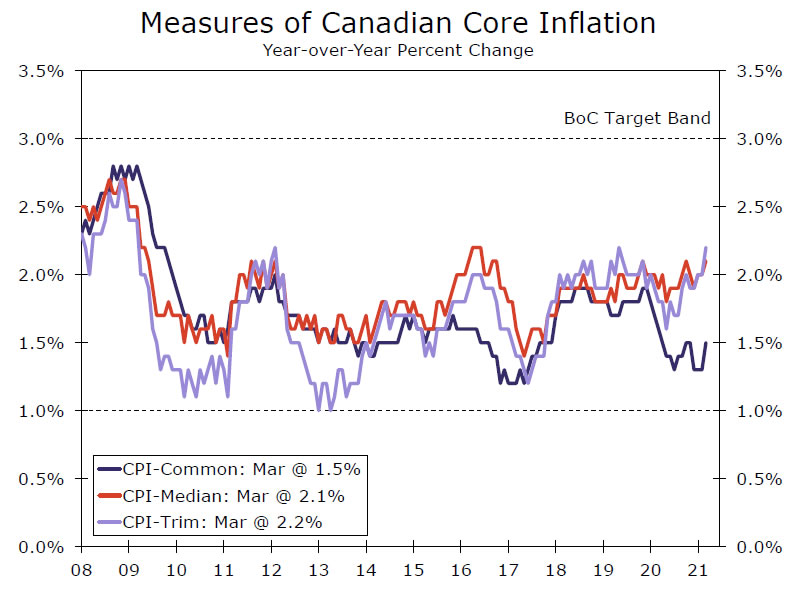

Given the stronger growth profile, the Bank of Canada now sees spare capacity within the economy being absorbed sometime during the second half of 2022, earlier than its January forecast of 2023. That earlier return to the economy’s productive potential is significant, as the BoC has said it will not raise interest rates until economic slack is absorbed. Accordingly, the updated projections signal the possibility of rate increases beginning in the second half of next year (which would be in line with our own forecast for an initial rate hike in Q3-2022). With underlying inflation measures close to or above the central bank’s 2% target, inflation is another reason to expect a further move toward Bank of Canada monetary tightening over time.

The European Central Bank (ECB) also met this week, and it signaled that it is a long way from following the BoC in tapering asset purchases. The ECB kept its policy rates unchanged, reaffirmed its pace of asset purchases under the pandemic emergency purchase programme (PEPP) and maintained its policy of reinvesting maturing securities until at least the end of 2023. The relative dovishness of ECB makes sense when contrasting the two economic outlooks. In Canada, the BoC expects the output gap to have closed by the middle of next year, and inflation is already near the sweet spot of 2%. In Europe, it will likely take at least 1-2 years longer to close the output gap, and inflation remains mired below 2% just like it was before the pandemic.

Interestingly, it is hard to pin this divergence entirely on Europe’s slow vaccine rollout, as most major European countries have administered about as many COVID vaccine doses as Canada. Fiscal support in Canada has generally been more robust, however, and its strong trade linkages with the booming U.S. consumer should also provide a tailwind. In the previous expansion, the Federal Reserve and the Bank of Canada led the way on monetary policy tightening, and it appears increasingly likely that the ECB will again follow.

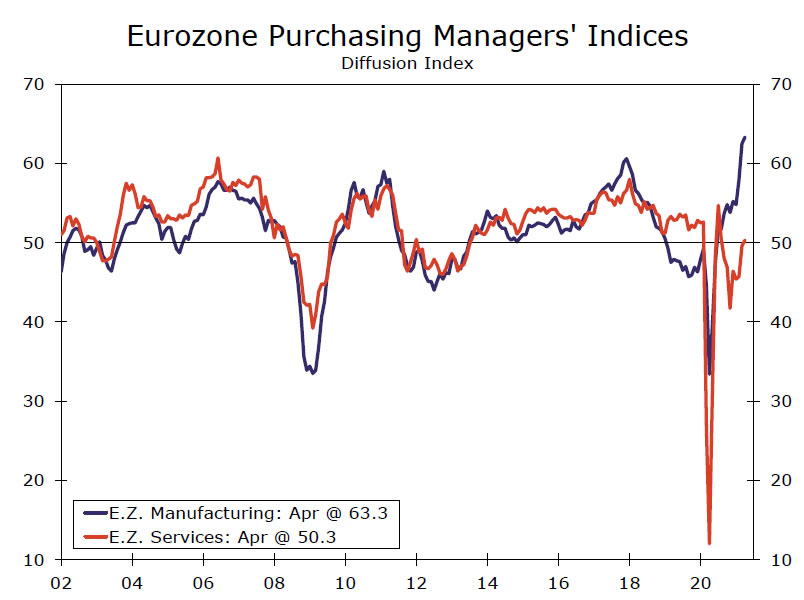

The purchasing manager indices (PMIs) released this morning for Europe signaled reason for optimism as well as additional evidence for how far behind the Eurozone is on a relative basis. The Eurozone manufacturing PMI increased 0.8 points to 63.3, which was yet another all-time high. With goods consumption in many countries still elevated and supply chains still struggling to keep up, a booming manufacturing sector in Europe is consistent with other economies. The same April PMI measure in the U.S. was 60.6 and 60.7 in the United Kingdom.

On the service sector side, the European PMI rose to 50.3 from 49.6. Although this is a fairly modest increase, it is encouraging because 50 is the demarcation line between expansion and contraction. This was the first print above 50 for the Eurozone service sector PMI since August 2020, and the composite index is now at its highest level since July 2020. Unlike the manufacturing sector, however, the U.S. and U.K. service sector PMIs were much higher in April at 63.1 and 60.1, respectively. We anticipate that the next couple months readings will show a broader recovery in Europe, as better weather and vaccine catch-up take hold.

International Outlook

Bank of Japan Policy Meeting • Tuesday

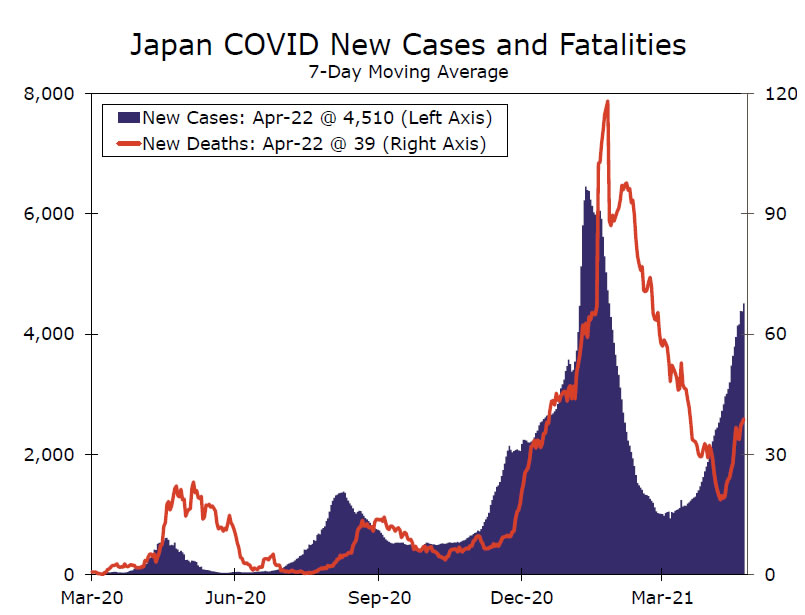

To date, Japan has managed to keep its COVID case and fatality counts much lower than the United States and Europe. That said, Japan’s vaccination drive has only recent begun, and COVID cases have started to creep higher in recent weeks. In response, Japanese Prime Minister Yoshihide Suga has called for placing Tokyo and some other major population centers under another state of emergency.

Compared to other major developed economies we forecast, we have made relatively minor revisions to our GDP growth forecast for Japan since the start of the year. Recent developments create some near term downside risks for the Japanese economy, and with core inflation already right around 0%, the Bank of Japan’s extraordinarily easy monetary policy is unlikely to change anytime soon.

Previous: -0.10%; Wells Fargo: -0.10%; Consensus: -0.10% (Policy Balance Rate)

Eurozone Q1 GDP • Friday

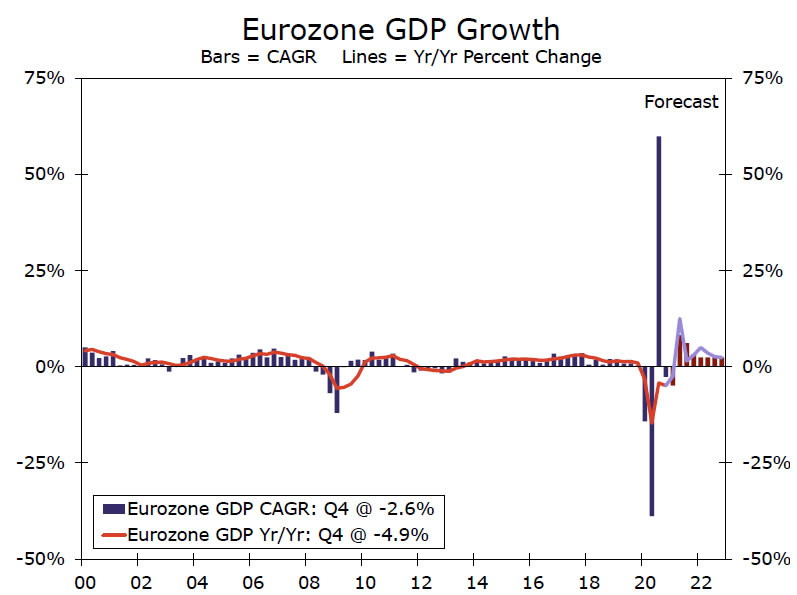

When Eurozone real GDP growth is reported next week, it will likely show the bloc’s economic output contracted for the fourth time in the past five quarters. The first quarter was a tough one for continental Europe as many countries struggled to keep COVID at bay amid a vaccine rollout that has significantly lagged the United States and United Kingdom. We project that the Eurozone economy was about 6% smaller in Q1-2021 than it was in Q4-2019. In comparison, the U.S. economy appears to have “only” contracted about 1% over the same time period.

Fortunately for Europe, we believe the worst is behind it. Better weather should help in the fight against COVID as it did last year when real GDP growth accelerated to a breathtaking 60% annualized rate in Q3-2020. And after a few stumbles, Europe’s vaccination efforts have begun to pick up steam. There is good reason to believe that by the time cold weather returns in the fall, most European countries will have vaccination rates closer to where the United States and United Kingdom are now.

Previous: -0.7%; Consensus: -0.8% (Quarter-over-Quarter)

Mexico Q1 GDP • Friday

Mexico’s economic performance in Q1-2021 likely sat somewhere in between the Eurozone’s further deterioration and America’s acceleration. The pickup in growth in the United States led by the consumer should benefit Mexico’s economy, given the strong trade linkages between the two countries, but it may not have had a material impact until late in the first quarter and should become more evident in Q2.

The recent retreat in U.S. Treasury yields should also benefit the Mexican economy going forward. Treasury yields nearly doubled over the first few months of the year, but over the past month or so, they have come off their highs. Since March 8, the peso has appreciated about 7% against the U.S. dollar. If U.S. yields hold at these levels or resume their ascent at a much more gradual pace, this should take some heat off of the Bank of Mexico and could allow for a slower pace of monetary policy tightening over the remainder of the year.

Previous: 3.3%; Consensus: 0.1% (Quarter-over-Quarter)

Interest Rate Watch

Rapidly Strengthening Data Ahead of April FOMC Meeting, but Is It “Substantial”?

Next week’s FOMC meeting is not expected to bring any policy changes or, in our view, even hint that changes may occur soon. Data since the March 16-17 meeting show that the recovery has shifted into a higher gear, which should result in an upgrade to the committee’s assessment of the economy. However, committee members have made it very clear via the dot plot and public statements that they do not intend to raise the fed funds rate anytime soon.

Less clear, however, is what conditions will lead to a scaling back asset purchases. Currently, the Fed is buying $80 billion worth of Treasury securities and $40 billion worth of mortgage-backed securities every month. It has said it will continue to do so until it sees “substantial further progress” on its employment and price stability goals. With tapering to occur before changes in the fed funds rate and activity picking up speed, what may constitute “substantial” improvement?

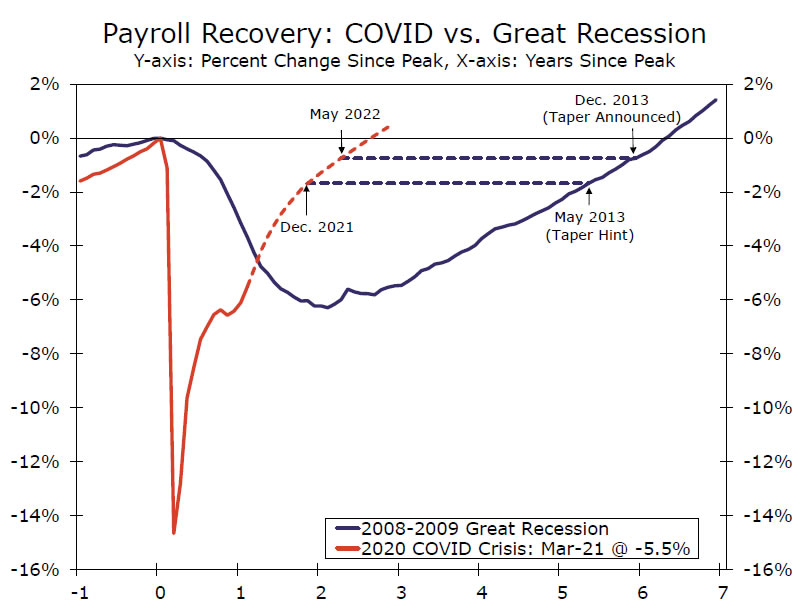

The lead-up to the last episode of tapering offers some guideposts. Whether looking at job losses or the inclusiveness of progress, the labor market’s recovery still has some ground to make up before it is in a similar position to when the FOMC first floated and eventually announced tapering in 2013. For example, payrolls are 5.5% below their pre-COVID peak compared to 1.7% below their 2008 peak when former Chair Bernanke first publicly contemplated scaling back purchases in May 2013.

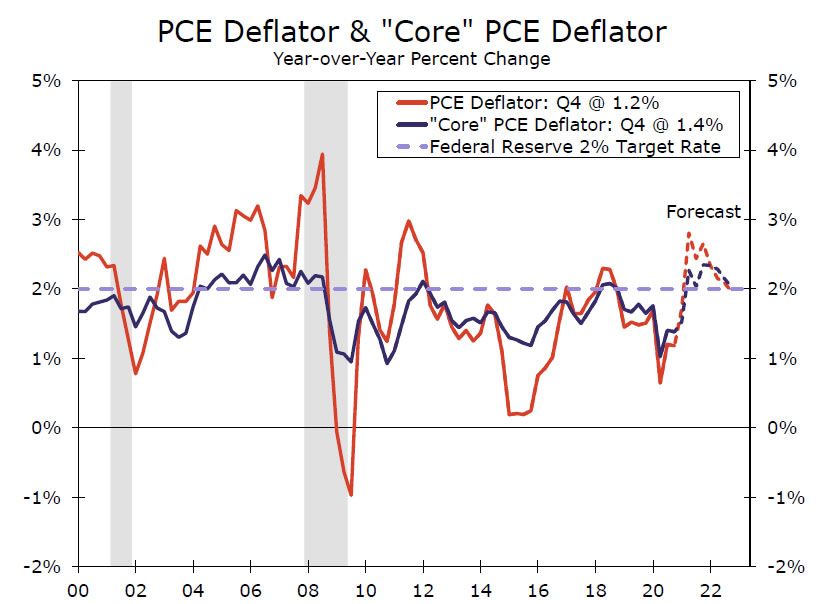

On the inflation front, the Fed remains further from its goal as well. Core PCE inflation has averaged only 1.4% since February 2020, compared to 1.6% between the start of the Great Recession and when the FOMC announced tapering in December 2013.

In our view, the Fed will need to see at least the same degree of progress as it did in 2013 when it first floated and then eventually announced tapering. The committee has taken a more outcome-based approach to policy where it needs to see rather than merely forecast improvement in the economy, and is looking for inflation to run a little over 2% in order to average that pace over time. Under our forecast, payrolls do not recover to the same degree as when tapering was first hinted in 2013 until December of this year, while core PCE inflation does not convincingly surpass 2% until the fourth quarter of this year. Along with what we suspect is a desire to feel more assured the pandemic really will be coming to a close later this year, we believe any hint on tapering will not come at next week’s meeting and remains months away.

One minor technical policy adjustment to watch for will be a potential 5-bp increase on the interest rate paid on excess reserves (IOER). This should not be construed as foreshadowing policy tightening ahead, but rather a “plumbing” adjustment to alleviate the downward pressure on short-term rates from excess liquidity in the banking system at present. For more on our expectations for next week’s FOMC meeting, see our April Flashlight for the FOMC Blackout Period.

Topic of the Week

A Quicker Rebound

Our above-consensus GDP forecast for this year is driven by a number of factors, but two major factors stand out. The first is a turning point in the battle with COVID thanks to vaccine distribution. The second is a robust fiscal policy response that, among other things, add to the excess savings households have accumulated, which should help sustain spending over the coming quarters. Both of these expectations are coming to fruition so quickly that some of the growth we expected later this year has arrived early and will likely materialize in a faster rate of GDP growth in the first quarter than we initially expected.

The battle against the virus is far from won, as is evident in rising case counts around the world, particularly in parts of Asia. While there are still some trouble spots in the United States, new case counts here remain much lower than they were during last winter’s surge. Both mobility data and soaring consumer confidence point to the fact that American life is returning to normal…and not as gradually as most market-watchers expected.

The Bloomberg economic surprise index, which gauges the extent to which actually data exceed or fall short of expectations, shot up from 0.27 as recently as mid-March to 0.49 at last check; this near doubling of the index attests to this run of better-than-expected data.

Source: Google, Bloomberg LP and Wells Fargo Securities

A Faster GDP Growth Rate in the First Quarter

On the stimulus side, many households received stimulus checks in January (from the December relief bill) and again in March (from the American Rescue Plan). Next week, we will get official figures from the U.S. Commerce Department about exactly how much household income rose in March, but there is already hard data, which shows that households certainly were spending during the month. The March retail sales report showed the second-largest monthly increase on record, with gains in every single store type as consumers resumed in-person shopping.

Business spending has been stronger too with core capital goods orders several percentage points above where they were before the pandemic hit. In fact, the bounce-back has been much quicker than most businesses expected. That is evident in the long wait times for many items and picked over inventory at various points throughout the supply chain.

Our best read suggests that first quarter consumer and business spending figures will now come in stronger than we had penciled in for our previous forecast update. Some of that strength will likely be offset by a draw-down in inventories, which will likely be a bigger drag on headline GDP growth. We now expect the economy grew at an annualized rate of 5.5%, with double-digit percentage spending increases in both personal consumption and business fixed investment being offset by a drag from inventories.