With investors significantly lowering their implied Bank of England rate path following the slowdown in June’s inflation numbers and the 25bps hike at the Bank’s latest meeting, the spotlight will now turn to the UK inflation data for July, due out on Wednesday at 06:00 GMT. Traders will be eager to find out whether their massive adjustment in their bets seems correct or not, leaving the pound vulnerable to volatile swings.

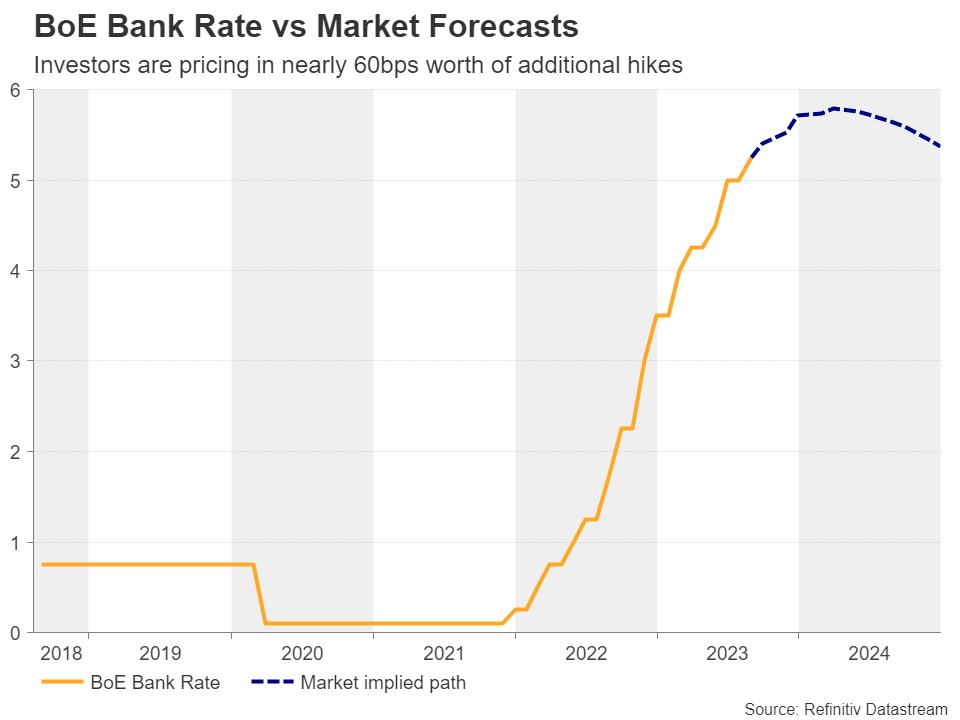

Investors see only two more 25bps hikes by the BoE

With inflation slowing more than expected in June, BoE policymakers decided to slow their tightening campaign at their latest gathering, raising interest rates by 25bps, a smaller increase than the half-point increment of the previous month. They also appeared less hawkish than expected, with Governor Bailey noting that he didn’t think there was a case for another 50bps hike.

Following the decision, investors massively slashed their rate-hike bets, and although they somewhat lifted again their implied path following Friday’s better-than-expected GDP data for Q2, they are still seeing a 20% probability for policymakers to stand pat at the next gathering, with the remaining 80% pointing to another quarter-point hike. As for thereafter, market participants are pricing in around 35 basis points worth of additional increases before the Bank ends its own tightening crusade.

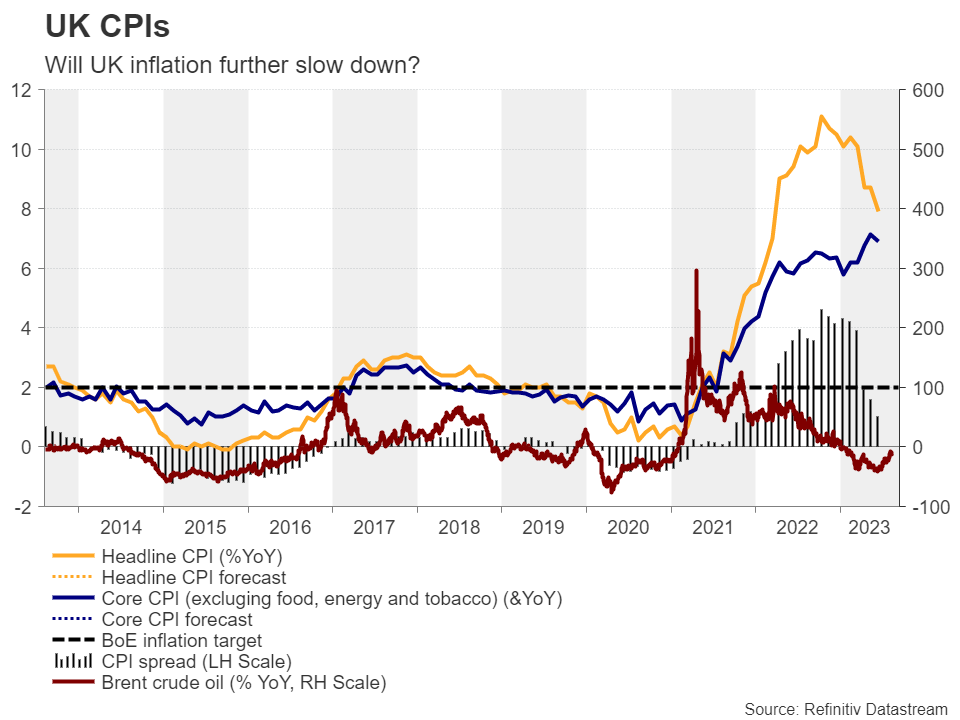

Inflation is expected to continue cooling

With all that in mind, this week, pound traders may pay close attention to the UK CPI numbers for July on Wednesday. The headline rate is expected to have dropped by more than a full percentage point to 6.8% year-on-year from 7.9%, while the core one is expected to have ticked down to 6.8% y/y from 6.9%.

A further slowdown in consumer prices is also supported by the S&P Global PMIs for the month, which suggested further cooling of inflationary pressures. However, considering the upside risk posed by the rebound in the year-on-year change of oil prices, should the headline rate fall as the forecast suggests, the core rate may fall more than anticipated.

Pound may slide, but upside risks remain

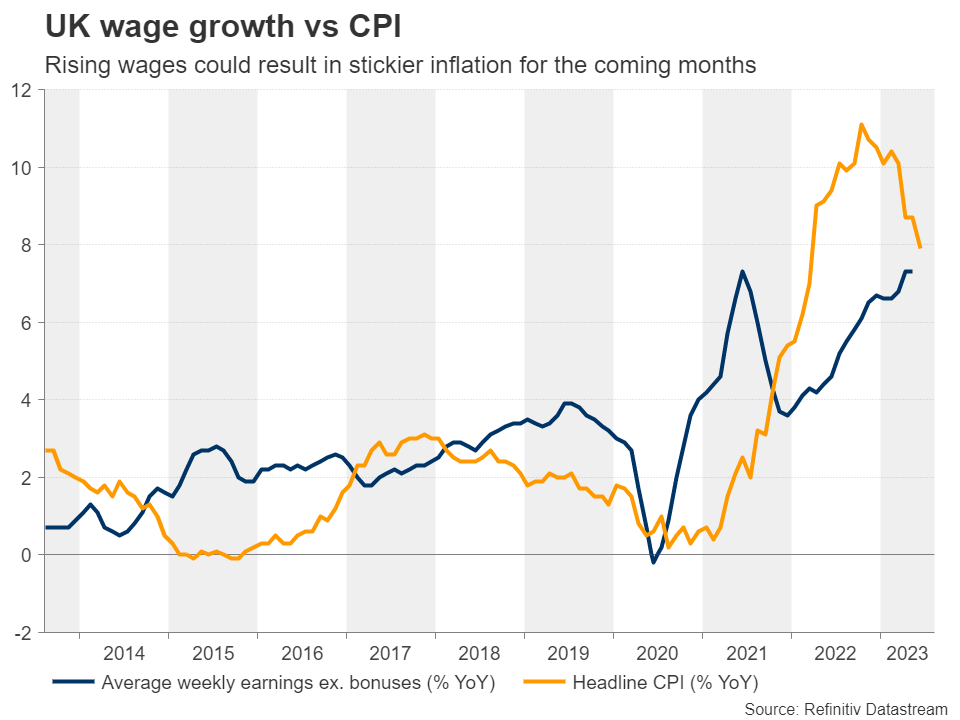

This could add credence to investors’ choice to lower their BoE implied rate path and may further hurt the pound. However, with inflation still running more than triple the Bank’s 2% objective, it will be hard to imagine that the BoE’s job will be done with only two more quarter-point hikes. After all, Tuesday’s employment report is forecast to reveal accelerating earnings growth during the month of June, and strong wage growth is something that can translate into stickier consumer prices in the months to come.

Therefore, although the pound may suffer for a while longer due to a further slowdown in inflation, but also due to a potential slump in Friday’s retail sales for July, there may be some upside risks in the medium term. At a time when other central banks are signaling the end of their own tightening crusades, investors may realize that the BoE still has work to do and thus, they could start adding back some more basis points worth of rate increments to their implied rate path.

Pound/kiwi uptrend poised to continue

This could help the pound rebound and continue its prevailing uptrend, especially against currencies whose central banks have already signaled that they are done raising rates, like the kiwi. The RBNZ announced the end of its own tightening cycle back in May, it held rates steady in June, and it is widely expected to stand pat this week as well.

As both the pound and the kiwi have risk-linked characteristics, those risk-related forces are offset by one another in pound/kiwi, with the main driver of the pair being the divergence in monetary policy expectations between the BoE and the RBNZ.

Just last week, pound/kiwi emerged above the key resistance (now turned into support) zone of 2.0925, signaling the continuation of the prevailing uptrend that’s been in place since the beginning of February. Even if the pair pulls back due to a miss in the UK inflation data, the bulls could recharge from near the 2.0925 zone and slowly take the action all the way up to the 2.1680 zone, marked by the high of March 9, 2020.

For the outlook to turn bearish, the pair may need to fall, not only below the uptrend line drawn from the low of February 3, but also below the key support zone of 2.0485. Such a move would confirm a lower low on the daily chart, perhaps setting the stage for declines towards the 2.0345 and 2.0150 territories.

{kind=link}