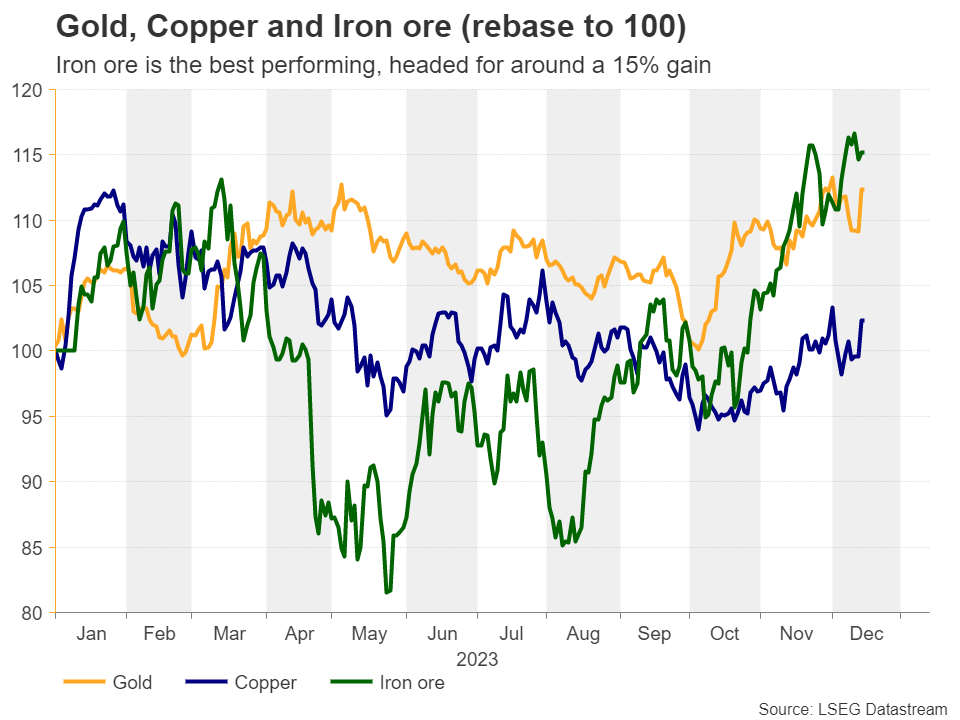

- Gold enters uncharted territory twice in 2023

- Fed policy to remain gold’s main driver in 2024

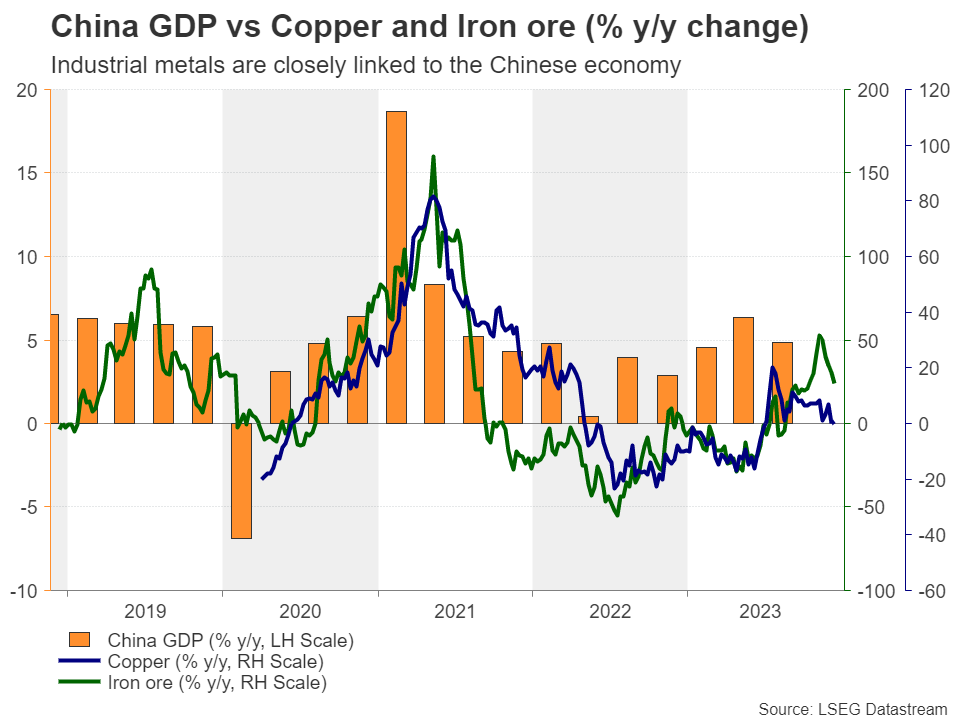

- Industrial metals to stay locked on China

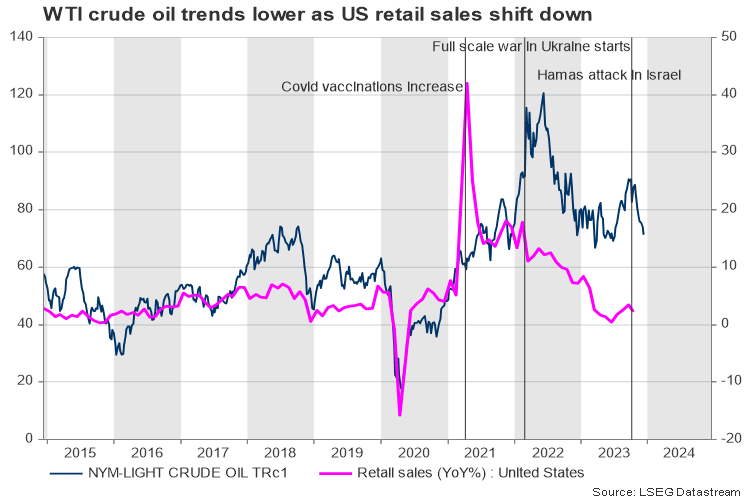

- Easing demand, OPEC+ supply, and geopolitics will shape crude oil

Fed rate cut expectations fuel gold

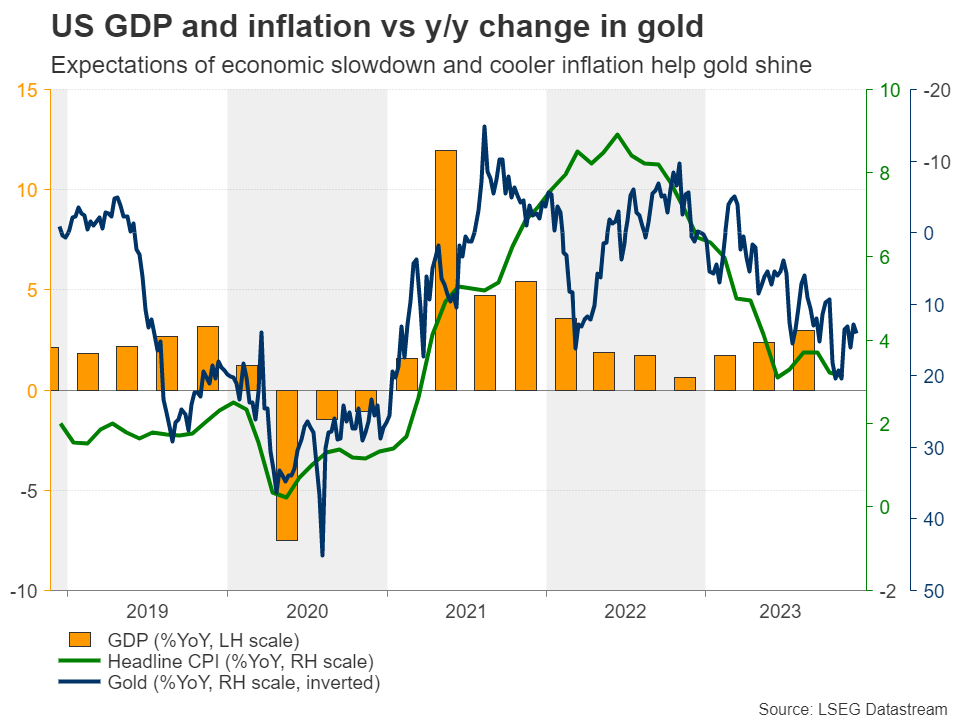

After a dull 2022, gold staged a decent comeback in 2023, entering uncharted territories twice and appearing to be headed for a more than 10% yearly gain. The only period where the precious metal trended lower was between May and early October, but after hitting a six-month low of $1,810 on October 6, the bulls took charge and drove the metal to a new record of around $2,145 in early December, although it corrected lower thereafter.

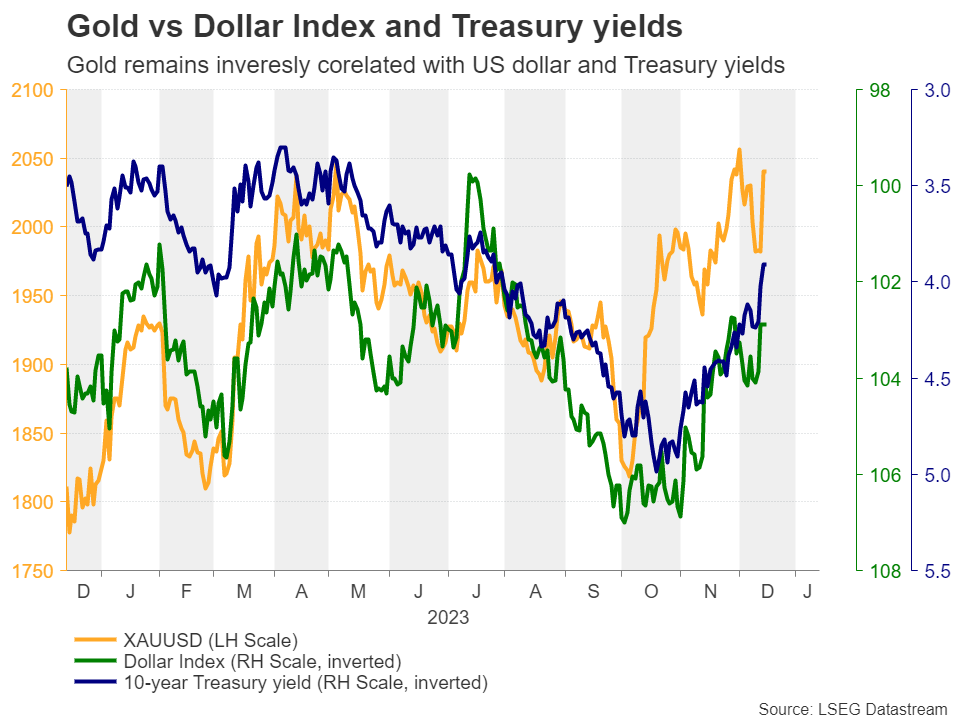

The May-October slide was the result of stronger-than-expected US data triggering a rally in both Treasury yields and the US dollar. That said, the conflict between Israel and Hamas put a floor to the slide, with the rebound evolving into a strong short-term uptrend as US data began to soften, suggesting an economic slowdown ahead. Combined with inflation cooling faster than expected and the Fed revising its dot plot lower in December, this allowed investors to pencil in sharp rate cuts, which reduced the opportunity cost for holding the precious metal.

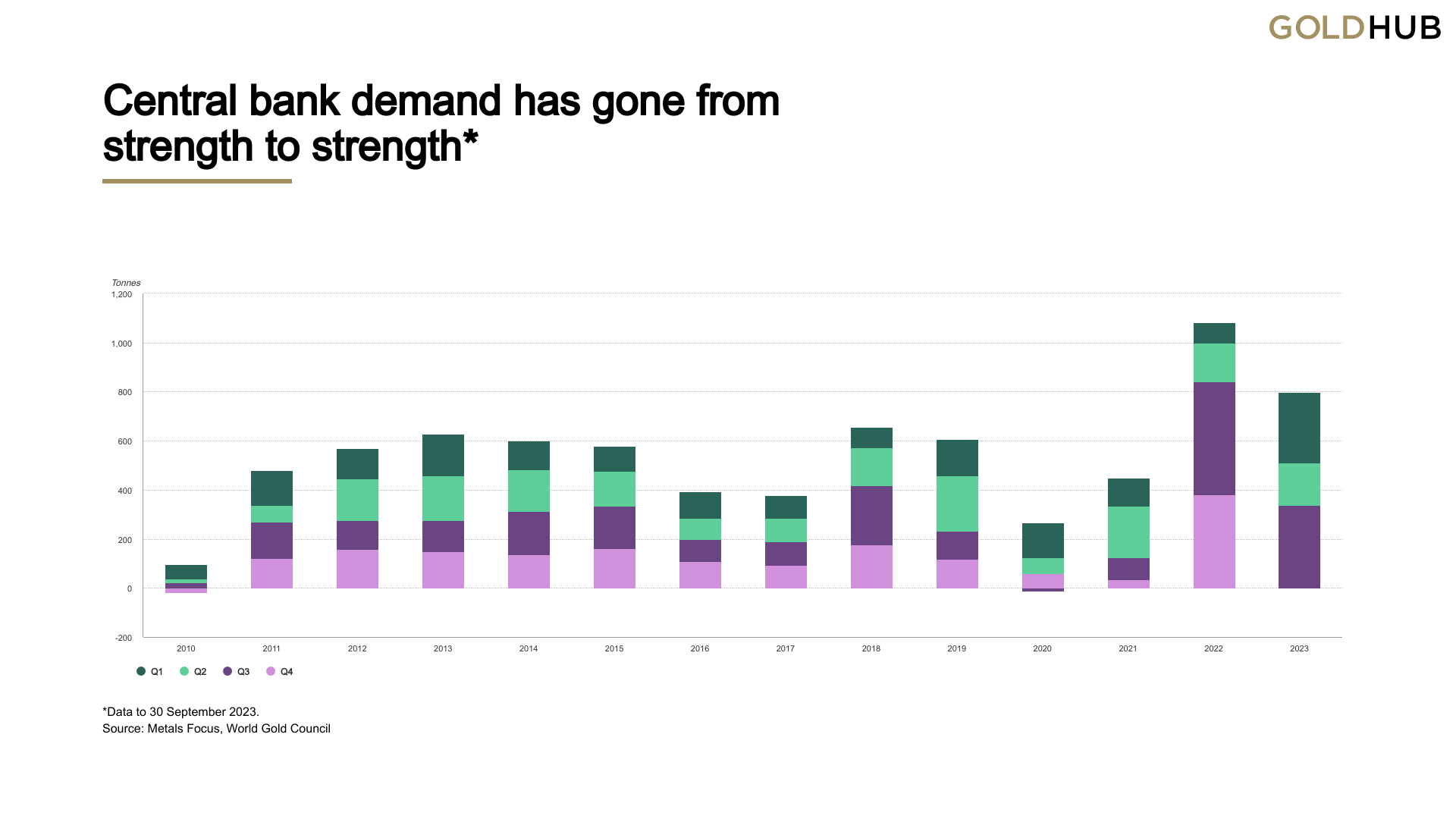

Record buying by central banks also helps

Another supportive factor for the yellow metal was that central banks have expanded their bullion reserves by 337 tons in Q3, resulting in a net 800 tons of gold during the first three quarters of 2023, which constitutes a record for a Q1-Q3 period. Surging consumer prices may have triggered a rush to gold by central banks as a store of value. However, even with inflation cooling down, the trend may continue due to concerns about a global economic slowdown that may require monetary easing, which could result in currency devaluation. Thereby, gold can be used as a hedge against depreciating currencies.

Rally could continue in 2024, but downside risks may intensify in H2

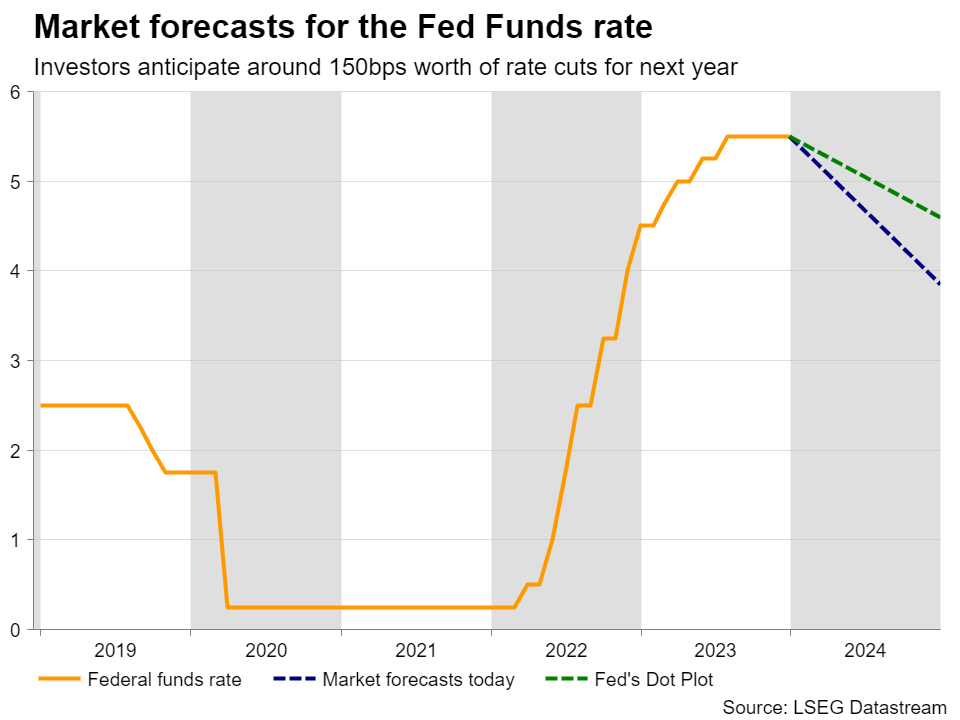

With that in mind, expectations of massive rate cuts by the Fed next year and solid central bank purchases are likely to allow gold to continue shining in 2024 as Treasury yields and the dollar stay pressured, with geopolitical uncertainty perhaps still permitting some safe haven flows periodically.

Nonetheless, there are downside risks to that outlook and the most recognizable may be the market getting proved wrong about penciling in so many rate reductions. Even if the Fed starts cutting during the first half of the year, data may begin to suggest that the economy is not doing as bad as initially feared, and thus policymakers may not proceed with as steep a rate-cut path as the market currently implies for the rest of the year. Thus, as they face reality, investors may begin to lift their implied path, which could prove positive for the US dollar and Treasury yields, and thereby result in a correction in gold.

Another risk towards the end of 2024 may be the US presidential election in November. Eleven months is too distant a horizon for the markets to start focusing on this event, but as time goes by, it may be difficult to ignore the risk of a possible impact the outcome may have. Opinion polls are showing former Republican President Donald Trump neck and neck with incumbent Democrat Joe Biden, with the former favoring spending cuts, but also aggressive tax cuts, which is an inflationary measure. This may increase the risk for the Fed to opt for a higher interest-rate path than the market currently anticipates, thereby exerting more pressure on gold towards the end of the year.

Industrial metals to stay closely linked to China

Iron-ore has been the best-performing industrial metal in 2023, but it was not a smooth sail north throughout the year, with the metal falling sharply during the second quarter on concerns surrounding the Chinese economy, the metal’s largest importer. Nonetheless, Chinese authorities have implemented a series of stimulus measures to heal their wounded economy, with the positive effect being reflected in some of the recent data sets. This may have been the main driver behind the rally in iron ore prices from August onwards.

Copper did not feel to the same extent the heat of concerns surrounding the performance of the world’s second largest economy, although China imports over 60% of the metal’s global traded volume. That said, this metal did not stage as strong a recovery as iron ore did during the last quarter of 2023, only returning slightly above the levels it began the year.

Looking ahead, if some optimism around China’s recovery is maintained, both metals may continue to benefit, with monetary policy easing around the globe providing a helping hand. The main risks are a continued slowdown in China, perhaps driven by its battered property sector, and central banks not loosening monetary policy as much as currently anticipated by the market.

Oil slides as global demand fizzles

Despite the ups and downs, crude oil prices retained a sideways trajectory, slumping back to their 2023 lows in the final quarter of the year.

Israel’s invasion in Gaza distracted the world’s attention away from the war in Ukraine, evoking memories of the oil crises in the 1970s. But its impact on energy markets has been relatively feeble and temporary as Israel is not an important global oil player and Iran’s direct involvement has not occurred yet despite ongoing tensions in the Middle East.

Instead, declines in crude stocks, OPEC’s production cuts, and hopes for growing oil consumption in China had been a dynamic bullish cocktail throughout the year, lifting WTI crude up to a one-year high of $95 at the end of September.

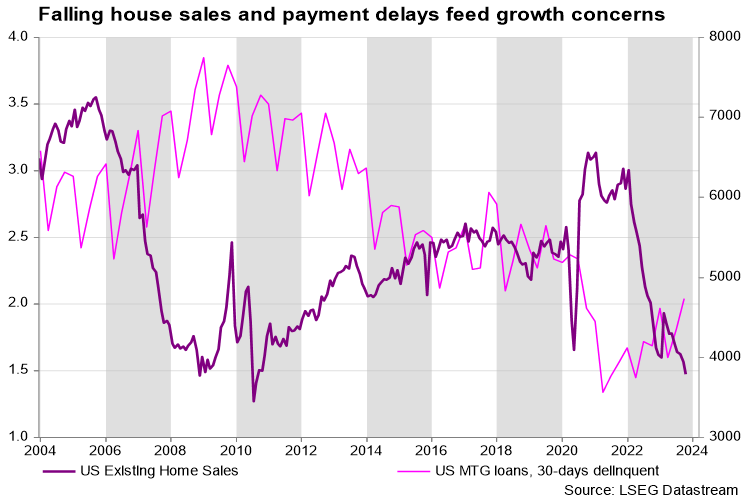

The oil rally, however, did not last long as recession fears became more pronounced, squeezing prices back to the 2023 floor of $64-$70. Following a year of rate increases and high prices, analysts are still wary of lagged rate hike effects, having revised their demand projections downwards a couple of times recently considering that consumers could adopt more careful spending habits in 2024.

Presently, the downtrend in the US house sales and the moderate increase in aggregate delinquency rates in the third quarter is a warning sign of fizzling economic growth. Testifying before the Senate, big US banks protested against the proposed new capital requirements (known as Bassel III endgame), arguing the measures could unjustifiably create more risks to the financial system while calling the lack of economic analysis for consumer regulations alarming even though there is no evidence banks are undercapitalized.

Nevertheless, the growth jitters may not necessarily sink the US economy if the unemployment rate stays near record low levels and the falling inflation boosts real wage growth. Potential rate cuts by global central banks could further enhance consumers’ and businesses’ purchasing power, preventing a hard landing.

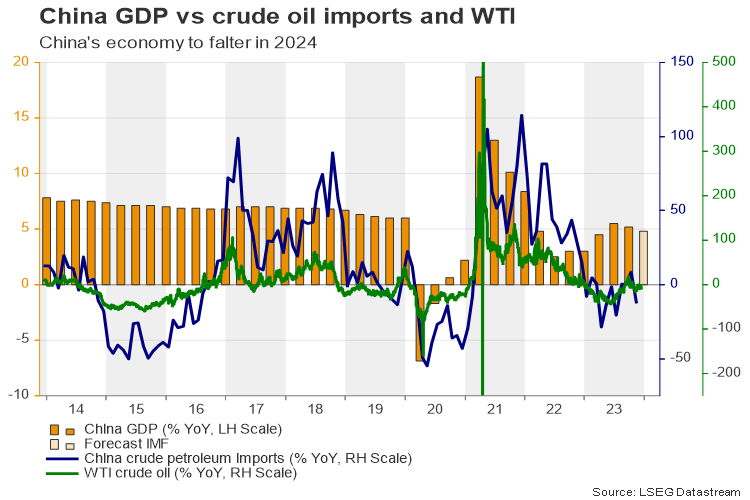

Energy demand from China not encouraging

China, the world’s oil demand engine, could also be an important card for the energy market although its consumption has been less impressive than expected this year and Moody’s negative outlook revision cast a pall over its 2024 picture.

Top officials have pledged to step up fiscal stimulus amid the persisting property slack and flagging consumer confidence, though they dropped the word “forceful” when mentioning monetary easing, backing a more flexible and targeted approach instead. That created some concerns about whether the government can restate its 5.0% GDP target in 2024 given that the reopening boost and the weak comparisons have already run their course.

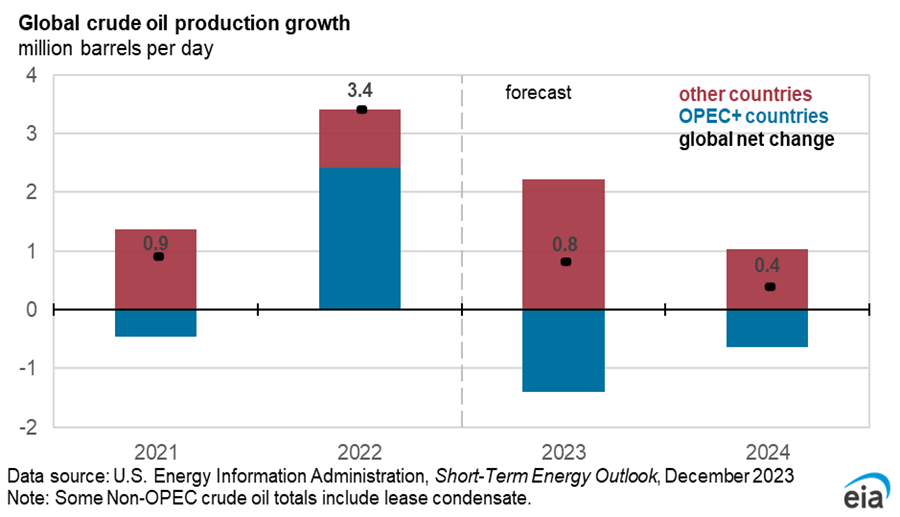

OPEC+ could be the main driver

OPEC, the US Energy Information administration, and the International Energy Agency share the same view of slower demand growth next year, with the former setting its forecast higher at 2.25mln bpd versus the 1.34mln bpd and 1.1mln increase set by the other two respectively. According to forecasts the oil market could shift into a small surplus early next year due to weakening demand, and OPEC+ exporters have already agreed to voluntary output cuts that lifted total curbs up to 2.2 mln bpd for the March quarter.

However, investors are not convinced OPEC and its allies can stay committed to the supply cut plans. The most recent virtual ministerial meeting was initially postponed as some African exporters pushed back against supply reductions following a year of underinvestment. Then, OPEC officials said that output cuts will be announced by individual members rather than the secretariat, making deviations likely, especially as forecasts for higher US supply threaten the oil cartel’s market share.

A price competition through a war of production could be possible between OPEC+ members and the US ahead of the US election. Biden would ideally want to keep fuel prices cheap to balance inflation pressures and fix his damaged political profile. On the other hand, Russia is facing a fiscal breakeven oil price of $114bbl according to the S&P Global commodity insights in the face of its military activities and heightened tariffs. Saudi Arabia’s equivalent is around $85/bbl based on IMF estimates, while any prices below $40/bbl could increase the odds of a debt crisis in regions such as Iran and Angola.

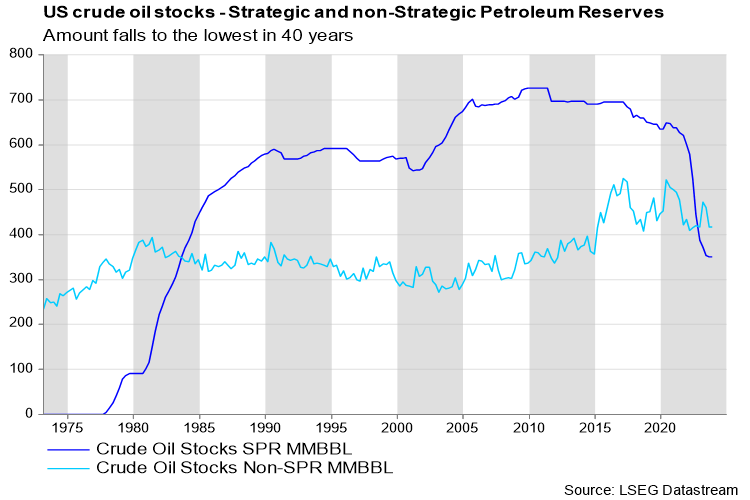

That said, the US might be relatively more vulnerable in such a battle as Biden’s administration sold more than 40% of the nation’s strategic petroleum reserves to keep a lid on fuel prices during the post-pandemic period. Efforts to refill the nation’s reserves could create adverse effects, creating more demand for oil and therefore new tailwinds for crude prices.

Geopolitics to keep investors on toes

Last but not least, geopolitical risks in the Middle East cannot be underestimated. Although investors have downgraded the tensions to a regional issue, there is no breakthrough in the Israel-Hamas war so far, and Iran’s support to militant extremist groups such as Hezbollah and Hamas and its uncertain nuclear program leaves the energy market exposed to a broader conflict that could consequently create new tailwinds.

{kind=link}