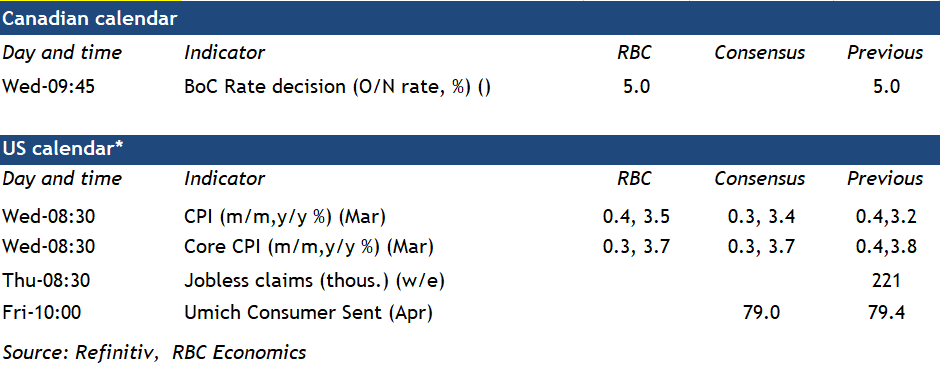

The Bank of Canada is widely expected to leave interest rates unchanged for a sixth consecutive policy decision on Wednesday. We expect the wording of the policy statement to leave options open for how long it plans to leave interest rates at current levels before pivoting to cuts.

Economic data since the last interest rate decision have been mixed. Gross domestic product growth in early 2024 is tracking substantially above the central bank’s forecast in January for a 0.5% Q1 increase. But that follows a string of softer readings by our count. GDP per person declined for six straight quarters to Q4 in 2023. Labour markets have continued to soften with the unemployment rate rising to 6.1% in March and job openings declining. Business bankruptcies have spiked higher, mounting debt service costs are cutting into household purchasing power, and wage growth has shown further signs of slowing.

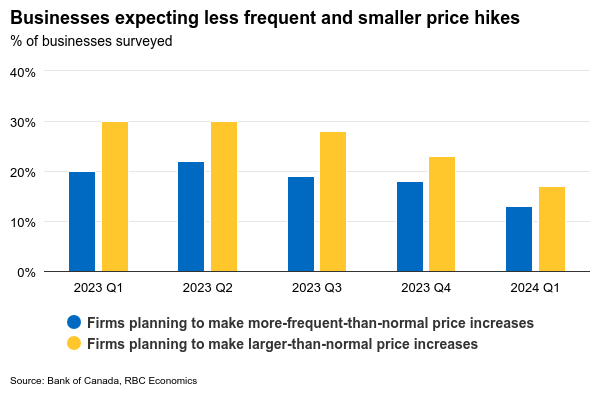

Most importantly for the BoC, inflation numbers have looked significantly better. Price growth year-over-year held below the top end of the 1% to 3% target range for a second straight month in February. The closely watched three-month rolling average of the central bank’s preferred core median and trim measures slowed to an annualized 2.2%. The Q1 Business Outlook Survey showed businesses expected inflation to continue to edge lower with further signs that business pricing strategies (planned frequency and magnitude of price changes) are normalizing. Resilience in early-2024 GDP data gives the BoC time to hold the line on interest rates for a little longer, but with most other economic data showing signs of softening, our base case assumption is that the BoC will be in a position to shift to cuts around mid-year.

Week ahead data watch

The U.S. Federal Reserve will be watching Wednesday’s March inflation print closely for signs that a resilient U.S. economy is reigniting inflation pressures following upside surprises in February and January. We expect a tick higher in year-over-year price growth to 3.5% (from 3.2% in February) but driven largely by an increase in gasoline prices. We expect core (excluding food and energy) price growth to edge down to 3.7% from 3.8% on a 0.3% month-over-month (seasonally adjusted) increase.

{kind=link}