Canadian Highlights

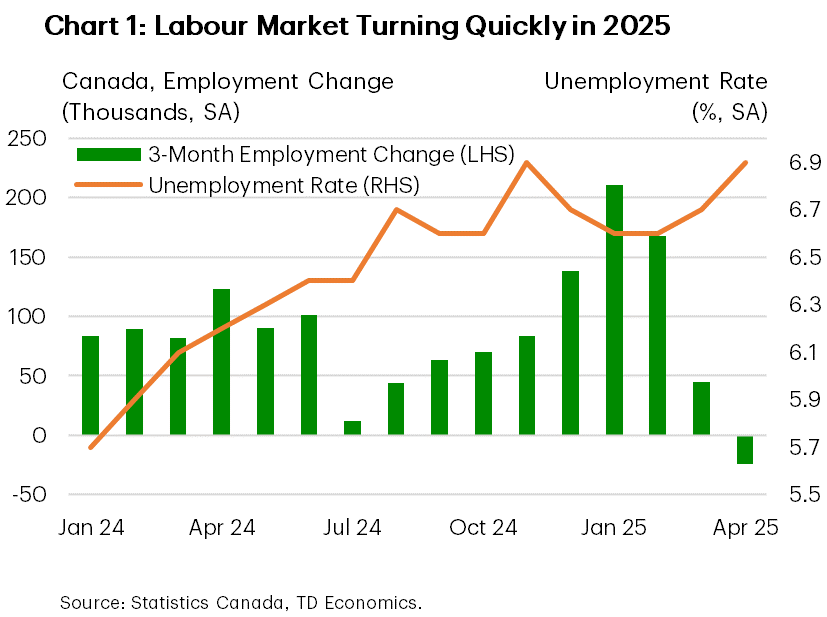

- Canadian monthly employment data are notoriously volatile, but the trend since January has been toward softer job creation and a rising unemployment rate.

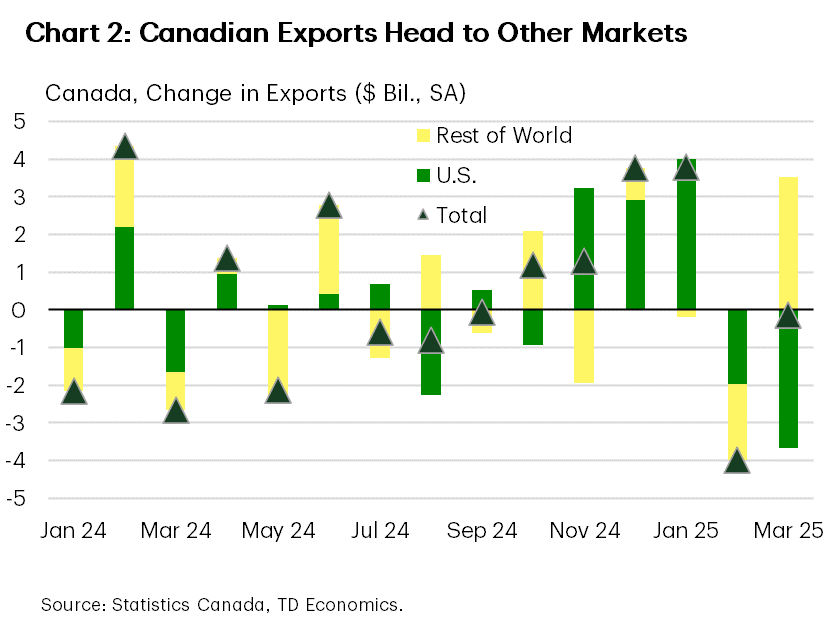

- Data show an increased share of Canadian goods heading to the U.S. in March were traded under the CUSMA agreement, avoiding tariffs.

- Softening growth and some positive developments on trade limit the upside risk to inflation, opening the door for the Bank of Canada to cut its policy rate.

U.S. Highlights

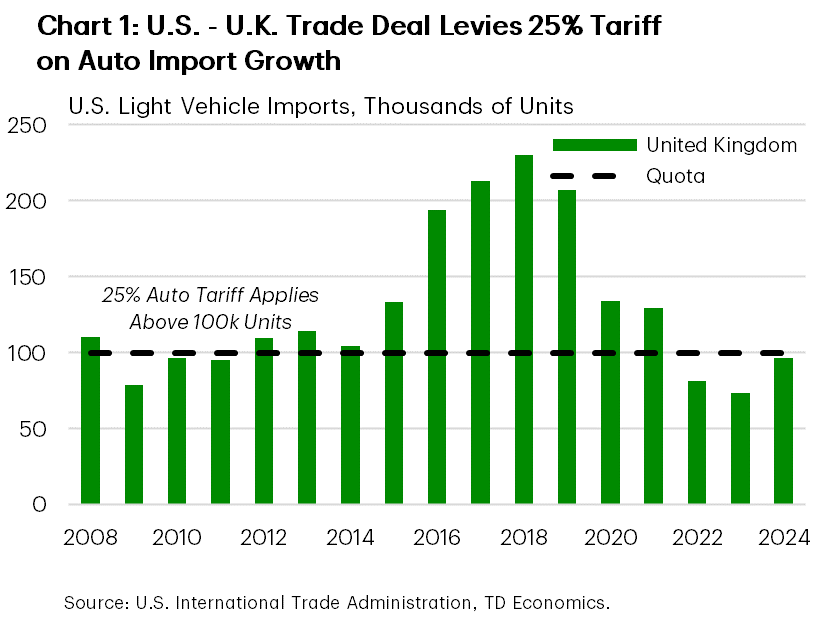

- The U.S. announced a trade deal with the U.K. to reduce several product-specific tariffs, although the 10% reciprocal tariff faced by the U.K. remained in place.

- Formal trade negotiations with China are expected to begin this weekend in Switzerland, as the third largest trading partner of the U.S. remains subject to 145% tariffs.

- The Federal Reserve left interest rates unchanged for the third time this year. Chair Powell noted that it would take time to discern the effects of tariffs on the economy.

Canada – Mr. Carney Goes to Washington

After winning the election last week, Prime Minster Carney travelled to Washington to meet President Trump. The bar was relatively low heading into the meeting, so it was notable for simply being unremarkable. The timing was appropriate though, as March trade data showcased the key economic issue facing the incoming Canadian government – how to diversify trade when there is a superpower next door.

Trade discussions with our southern neighbour are likely to take time and involve renegotiating parts of the CUSMA trade agreement signed in 2018. On the agreement, policymakers were likely keenly aware of President Trump calling it “great for all countries”, before noting that it can be renegotiated or terminated. For the outlook, as long as the uncertainty about tariffs and trade agreements persists, it will hang like a cloud over the economy.

The deceleration is apparent in the labour market. The economy added a modest 7k jobs in April, and those gains were largely thanks to temporary federal election jobs. The private sector has shed jobs for two months in a row. Canadian monthly employment data are notoriously volatile, but the trend has been toward softer job creation since the escalation in trade tensions. As employment growth has petered out, the unemployment rate has steadily crept higher, reaching 6.9% in April. The unemployment rate is now matching its high from November 2024, before a burst of late-year hiring showed some temporary relief for the labour market (Chart 1). Pull the history back further and, excluding the pandemic period, the 6.9% unemployment rate is the highest since January of 2017. It is also apparent that tariffs are behind the deceleration in the labour market, with trade-exposed sectors behind the recent slowdown in hiring – the manufacturing sector has lost 43k jobs over the past three months.

Looking ahead, the challenges are apparent. Part of the lift to first quarter activity was due to American firms attempting to front-run tariffs by stockpiling imports ahead of the new duties. Canadian exports to the U.S. grew nearly 7% per month between November and January, before falling nearly 10% through March once they were applied. However, two silver linings emerged in the March data. First, the steep decline in exports to the U.S. was offset by a rise in shipments to the rest of the world (Chart 2). Secondly, roughly 50% of Canadian goods heading to the U.S. were CUSMA compliant in March, up from the 38% averaged in 2024 and 40% last March. The increased compliance means avoiding the 25% tariff and reducing the economic impact. Nonetheless, as long as the uncertainty about the trade relationship persists, firms are understandably cautious. With the malaise hanging over the economy its unlikely things will turn a corner soon.

Faced with the prospect of domestic activity continuing to soften, we see the Bank of Canada having an opening to cut its policy rate by 25 basis points in June, bringing it down to 2.5%. The risk of higher inflation remains, but there are a few reasons for optimism that the worst-case scenario won’t materialize. First, a greater share of Canadian products have become CUSMA compliant (offsetting the risk of supply chain snarls), retaliatory tariffs have been restrained, and a stronger dollar offset rising cost pressures.

U.S. – The First of Many?

The first full week of May looked like it may provide a modest respite for financial markets, as economic data releases were limited and the Federal Reserve’s decision on Wednesday was short on surprises. However, this proved to be short-lived as the White House announced a preliminary trade deal with the U.K. on Thursday. The S&P 500 ended the week roughly unchanged at time of writing, while the 10-year U.S. Treasury yield rose 4 basis points to 4.36%.

The preliminary trade deal between the U.S. and U.K. (see here), included a full exemption on Section 232 steel and aluminum tariffs for the U.K., in addition to an annual exemption on automotive tariffs for the first 100k units imported (Chart 1). The market reaction to the agreement was relatively tame, as the 10% baseline reciprocal tariff remained in effect. The President noted that this would likely be the global floor for reciprocal tariffs, and that other nations may see levels above this even after negotiations have concluded. It is unclear whether this would be acceptable to other nations. If they take a harder stance during upcoming negotiations, it could delay a broader resolution to the current state of elevated trade tensions.

The EU also outlined a list of goods this week that would be subject to retaliatory tariffs. The list covers nearly a third of U.S. exports to the region. These tariffs would be levied if negotiations do not result in “a mutually beneficial outcome and the removal of U.S. tariffs”. Chinese officials also called on the U.S. to “be prepared to correct its erroneous actions and cancel its unilateral tariff increases”, ahead of the planned start of formal negotiations with the U.S. this weekend. Early on Friday the President floated the idea of lowering the tariff rate on China to 80%, but no final decision has been made. With less than two months until the 90-day suspension of U.S. reciprocal tariffs expires and dozens of deals yet to be made, time will remain of the essence on the trade front in the weeks ahead.

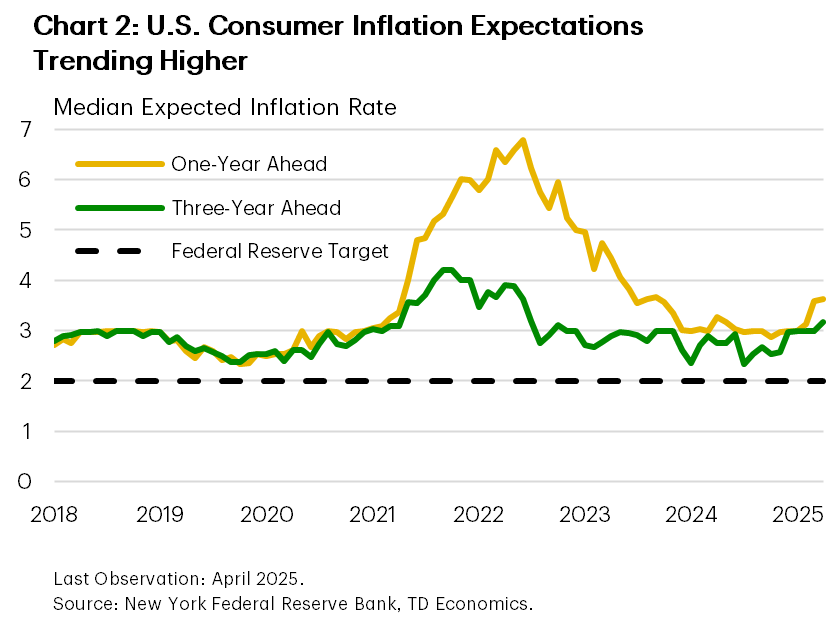

The Federal Reserve pointed to the clouds hanging over the economic outlook in its rate decision on Wednesday. It was the third meeting in a row where the FOMC left the federal funds rate unchanged. During his press conference, Chair Powell highlighted the likelihood that current trade policies would push the unemployment rate and inflation to deviate from the Fed’s dual mandate. However, he also noted that uncertainty remains elevated with respect to the magnitude of the deviation, meriting caution in monetary policy decisions at this time. With survey-based measures of inflation expectations remaining elevated in April (Chart 2), the Fed’s caution would appear prudent at this time.

Next week, we’ll receive a first look at inflation data for April with the CPI data release, in addition to April retail sales. Although neither is expected to be materially influenced by tariff impacts yet, they will provide a pulse check on consumer and price trends. Also on the docket for next week is the reconciliation bill markup for the House Ways & Means Committee, which could provide insight on the specific tax cut provisions being considered by Congress. Although fiscal policy may not fully offset the influence of tariffs on the economy this year, it could help to prevent a more material slowdown.

{kind=link}