- Market sentiment improves amid US-China trade talk optimism, despite concerns over tariff impacts on the global economy.

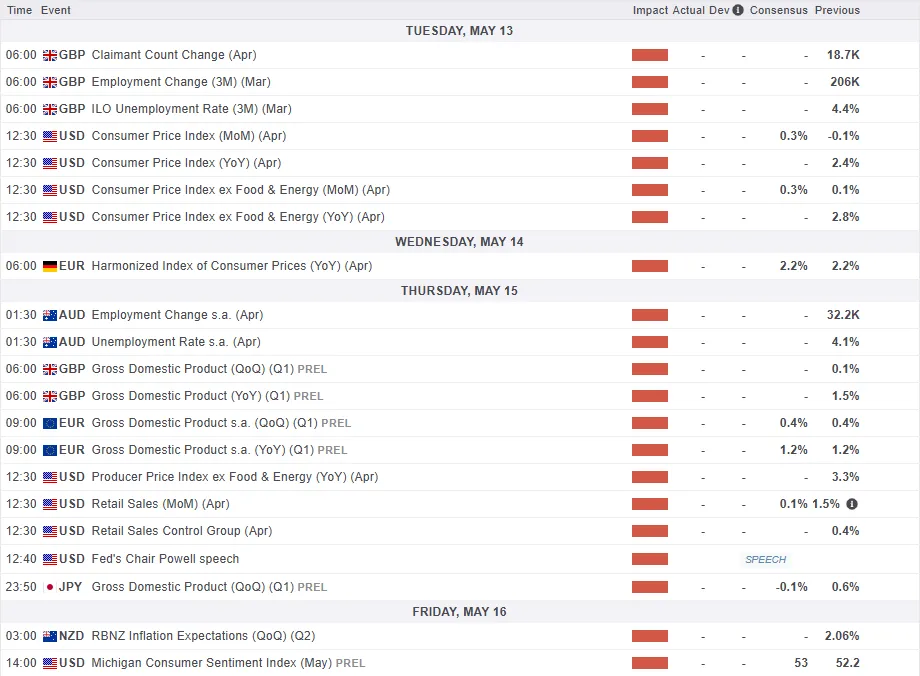

- Key economic data releases are expected across Asia, Europe, and the US, with a focus on inflation and retail sales.

- The US Dollar Index remains a focal point, showing a grind higher and influenced by trade talk developments.

- Federal Reserve’s stance on interest rates and potential inflation increases due to tariffs are closely monitored.

Wall Street indexes are looking to finish the week with gains after a shaky start earlier in the week. Improved sentiment and the pending US-China meeting over a potential trade deal this weekend has kept market participants on the optimistic side.

Companies continue to pull their earnings forecasts this week on the back of a number of uncertainties. This has led to US equities being a bit sluggish this week, as even though market participants are optimistic there remains a host of challenges that need to be overcome. Tariff clarity may also allow companies to gain a better sense of how their businesses may be affected moving forward.

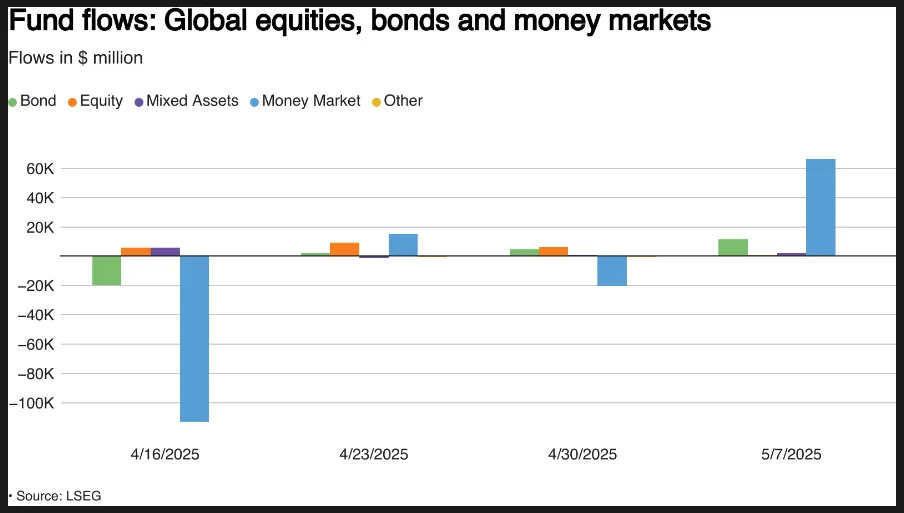

Despite the improving sentiment Global equity funds saw their lowest weekly inflows in four weeks, ending May 7, as worries over tariffs’ impact on the global economy and the outcome of U.S.-China trade talks weighed on investors.

LSEG Lipper data shows that investors purchased just $856 million in global equity funds that week, a sharp drop from the $6.13 billion invested the previous week. European equity funds remained popular, drawing $12.81 billion in net inflows for the fourth week in a row.

Asian funds also attracted $3.32 billion in net inflows. However, U.S. equity funds faced net outflows for the fourth straight week, losing $16.22 billion during the same period.

Source: LSEG

Gold enjoyed a rollercoaster week breaching the $3400/oz handle on Tuesdays before edging lower for the rest of the week to trade around the $3340/oz mark at the time of writing.

Oil prices started the week under pressure with a significant gap to the downside after the OPEC + meeting last weekend. Rumors began to swirl that Saudi Arabia would be okay with lower oil prices and that the group may look to be more aggressive with increasing its production and output.

Thanks to the improving sentiment Oil prices did edge higher for the majority of the week. Brent is trading higher for the week as it looks to snap a two week losing run which sent Brent to fresh lows around the 58.60 a barrel mark.

On the FX front, the US Dollar regained its bullish momentum on Thursday but has struggled to keep up the momentum on Friday. This has left the US Dollar index largely flat for the week.

The Dollar’s Friday weakness has helped the likes of EUR/USD and GBP/USD recover some of Thursday’s losses. The Swiss Franc remains one to watch as Swissie strength continues to be of concern to the Business community which is adding pressure on the Central Bank.

Markets will shift their attention to trade talks between the US and China this weekend. On Friday US President Trump posted on TruthSocial saying he thinks 80% tariffs on China would be fair. This was followed by the President saying that it’s up to Treasury Secretary Bessent.

President Trump’s trade advisor Peter Navarro confirmed what we already expect, this weekend will be an interesting one for global markets.

The Week Ahead: US-China trade talks to drive sentiment

The week ahead has several important data releases lined up. However, with US-China talks taking place over the weekend and the first trade deal already completed, markets may shift their attention to tariff updates, which could take the spotlight away from the economic data.

Asia Pacific Markets

Japan’s economy is set to shrink by 0.1% in the first quarter of 2025, down from a 0.6% rise in the last quarter of 2024. Household spending and more foreign tourists are boosting private consumption, but low external demand is holding growth back. The impact of rushing exports before tariffs has been smaller for Japan compared to other big exporters. Imports have shown a recovery. Due to weak growth, the Bank of Japan is likely to hold off on any rate hikes for now.

China’s inflation data for April will be shared this weekend, and consumer prices are expected to stay at -0.1% year-on-year, the same as March. Producer prices are likely to remain negative for the 31st month in a row. Deflation could get worse because of tariffs, forcing exporters to find new markets. China will also release its April credit data in the coming week. Credit growth has been improving this year, but April’s numbers are unlikely to reflect the latest measures by the People’s Bank of China to ease monetary policy. More time will be needed for the effects to be felt and transmitted through the data.

Europe + UK + US

The Federal Reserve has made it clear they’re not rushing to lower interest rates. They acknowledge that trade uncertainty could lead to both higher unemployment and inflation. April’s inflation data, due next week, is expected to show that inflation remains high. There may also be signs of early price increases as tariffs start to impact costs. By June, these price hikes could become more noticeable, as it takes time for goods to be shipped, stored, and finally sold in stores or online.

Retail sales are in focus this week. March was strong as people bought big-ticket items early, fearing tariff-related price hikes. This may continue in April for car sales, but worries about inflation, job security, and falling wealth could hurt non-essential spending. Key data like the Michigan sentiment index and industrial production are also due.

If we travel over the pond to the UK, the job market is cooling but not weakening significantly after recent tax hikes. Last month’s drop in payrolls will likely be revised higher. Unemployment is expected to rise, though the data isn’t always reliable. Wage growth should slow, mainly due to earlier high comparisons, with pay pressures easing later this year.

February’s GDP jumped 0.5%, and even with a possible dip in March, first-quarter growth looks solid. This surge is partly due to volatile manufacturing data. Growth in the second quarter is likely to slow but should remain steady, helped by government spending.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week – US Dollar Index (DXY)

This week’s focus remains on the US Dollar Index.

The index which finally closed above the psychological 100.00 level last week looked on course for a positive close heading into Friday.

The index did not push on though and remains above the 100.00 mark at the time of writing but has pulled back significantly from the weekly high at 100.61 which is a resistance area.

The DXY has been making its way higher on a daily timeframe printing higher highs and higher lows but it has been a grind to say the least.

Positive developments on US-China trade talks could lead to a significant rally to the upside and could serve as the jolt in the arm the US Dollar has been waiting for.

Immediate resistance rests at 100.61 before the 101.80 and 102.16 levels come into focus.

If a deeper pullback takes place, support rests at 100.00 before the 99.57 and 99.00 handle comes into focus.

US Dollar Index (DXY) Daily Chart – May 9, 2025

Source: TradingView.Com (click to enlarge)

{kind=link}