{kind=link}

- Canada, Japan and the UK to publish CPI data, but not the US.

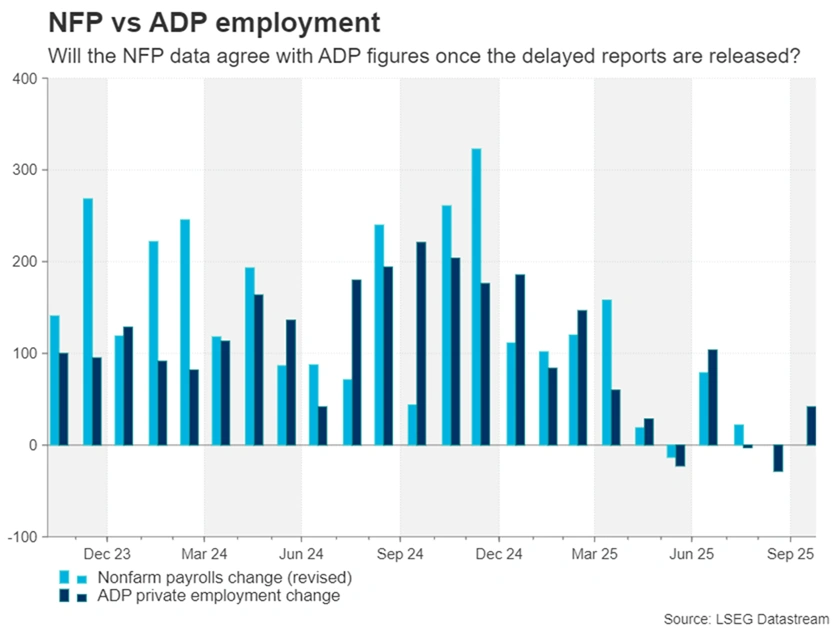

- US October jobs and inflation reports may never get released.

- New release schedule likely; FOMC minutes eyed in meantime.

- Flash PMIs to be watched amid renewed economic worries.

US government reopens: All eyes on revised schedule

The US government shutdown finally came to an end on Wednesday after 43 days, raising hopes that it won’t be long before the data blackout is also over. It is very likely that the various statistics agencies such as the Bureau of Labor Statistics and the Bureau of Economic Analysis will publish updated release schedules at the start of the week. But when the delayed data will start rolling again is yet to be determined.

Quite possibly, the September jobs report will be the first to see the day of light, maybe as early as the end of next week, as it’s thought that the data was already compiled before the government shut down. The same was true for the CPI report, which was the only exception by the BLS, prioritizing its release in late October.

Risk of no October data

However, there are doubts about the October data. The BLS may decide to forgo both the October payrolls and inflation figures to focus on the November data, as even then, they might have to be delayed slightly. Then there’s the question mark about whether it’s going to be possible to backfill the October numbers in the November or future reports.

For example, it would be very difficult for the BLS to collect data for the October CPI and unemployment rate, which is calculated from the household survey, when the month has already elapsed. Though, it might still be possible to backfill the nonfarm payrolls reading, which is prepared from the establishment survey.

A growing list of overdue releases

Investors will also want to learn how soon the initial jobless claims will return to the weekly agenda, as well as the schedule for the delayed October retail sales and PCE inflation, and Q3 GDP reports.

Any complications in the resumption of these key publications could weigh on expectations of Fed rate cuts, as it would provide the hawks with an excuse to stay on hold until there is a fuller picture on the US economy, following Chair Powell’s ‘driving in the fog’ remark.

Hence, the US dollar is more likely to go into consolidation than to extend its pullback in the coming week, while any positive data surprises could revive the bulls.

Fed minutes and flash PMIs are the scheduled highlights

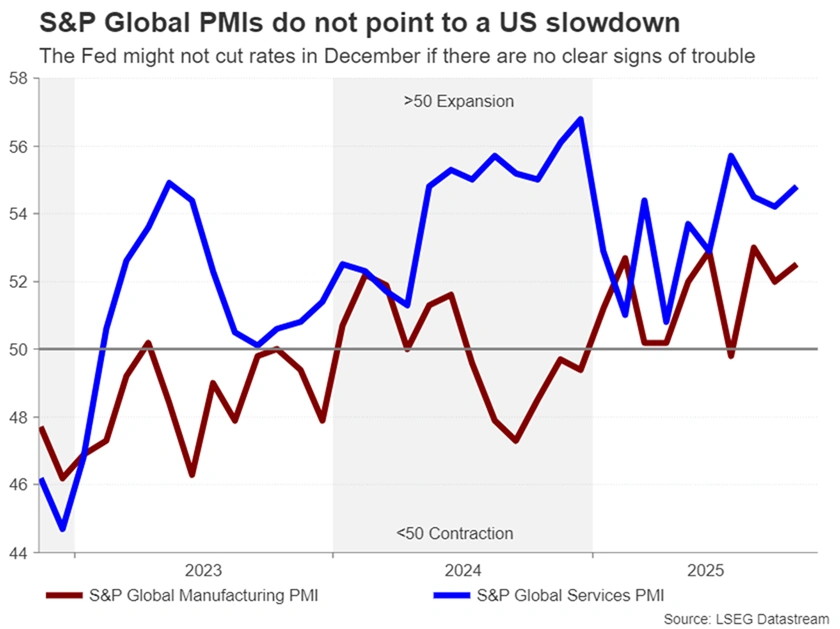

In terms of the regular releases, the New York Fed’s and Philadelphia Fed’s manufacturing surveys are out on Monday and Thursday, respectively, while S&P Global’s flash PMIs for November due on Friday will be vital for filling in the gaps.

With the markets’ rate cut expectations not currently aligned with the Fed’s own outlook, the dollar will be sensitive to any indications that the US economy is either slowing sharply or that the recent soft jobs readings were a false flag. On the other hand, if the PMIs continue to point to stagflationary conditions, this would knock sentiment as well as the dollar.

Also on next week’s agenda are the minutes of the Fed’s October policy meeting. Most Fed policymakers have already expressed their views since that meeting, so the minutes are not anticipated to spur much reaction. Nevertheless, should the divisions among FOMC members appear to be widening, this could cast a fresh cloud of uncertainty over the rate path.

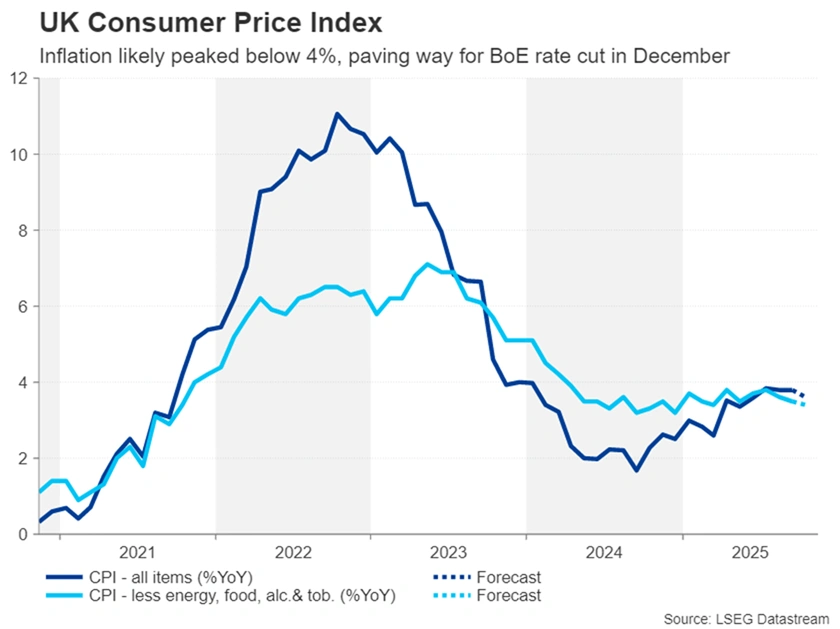

Will UK CPI boost BoE rate cut bets?

Across the pond, there is a bit more certainty surrounding the odds of the Bank of England cutting rates in December. Only a few weeks ago, many investors were not anticipating further UK rate reductions before spring 2026. But the last CPI report was a game-changer, as it eased fears of inflation spiking above 4.0%. With employment and GDP figures also coming in below expectations in the past week, traders have upped their bets of a 25-bps cut in December to about 80%.

The spotlight now firmly lies on next week’s CPI prints for October, and to a lesser extent, the November 26 budget. Headline inflation remained unchanged at 3.8% y/y in September, while core CPI dipped to 3.5% y/y. A further moderation in Wednesday’s October update would cement expectations that the BoE will trim rates next month, likely pressuring the pound.

However, there might be some support for sterling on Friday should the October retail sales numbers and flash PMIs for November suggest there is still some momentum in the UK economy.

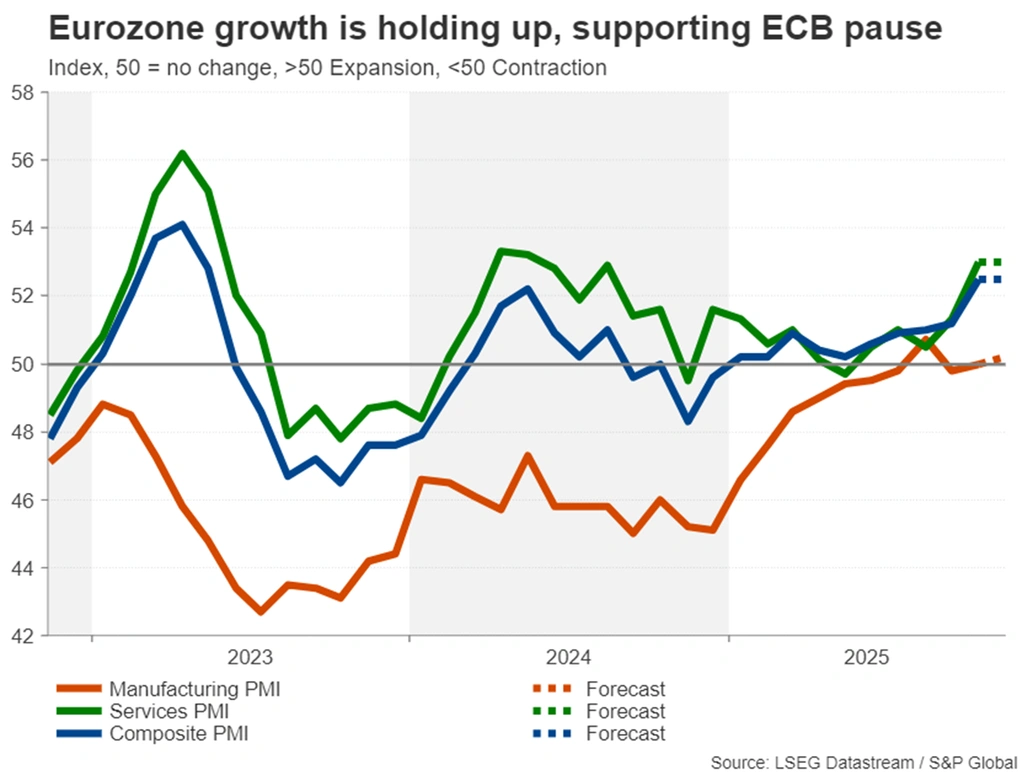

Eurozone PMIs to pose no threat to ECB pause

The flash PMIs will be the primary data point for the euro area. The recent PMI and GDP readings out of the Eurozone have been surprisingly solid, bolstering the view that the European Central Bank is done cutting rates.

Friday’s preliminary PMIs for November are unlikely to change much regarding the rate outlook. Yet any further improvement in economic activity, particularly if both the manufacturing and services gauges hold above 50, could give the euro a small leg up against the US dollar.

Ahead of the PMIs, the final estimates of October CPI are due on Wednesday.

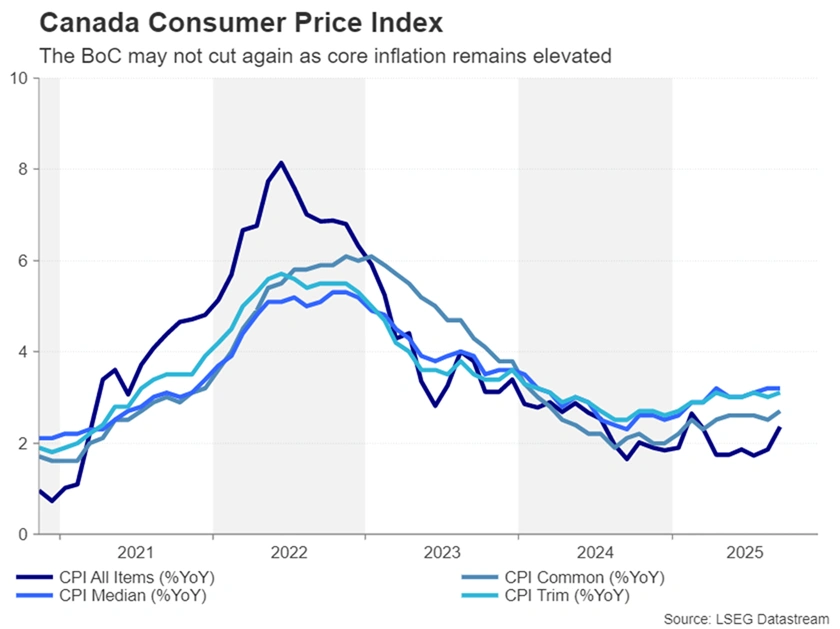

Will Canadian CPI thwart the Loonie’s rebound?

The Bank of Canada may soon join the ECB in going on pause. Although the central bank lowered rates at its last policy meeting, the tone from Governor Tiff Macklem was unusually neutral.

Employment numbers for October supported Macklem’s comment that interest rates are “about the right level”, as Canada’s labour market added more than 60k jobs for the second straight month.

Investors see just a one-third probability of one more rate cut by the BoC over the next year and Monday’s CPI data for October is unlikely to move the needle much. And with the Canadian dollar posting a decent rebound over the past week, any upside surprises in inflation could worsen dollar/loonie’s pullback.

Busy week looms for the Yen

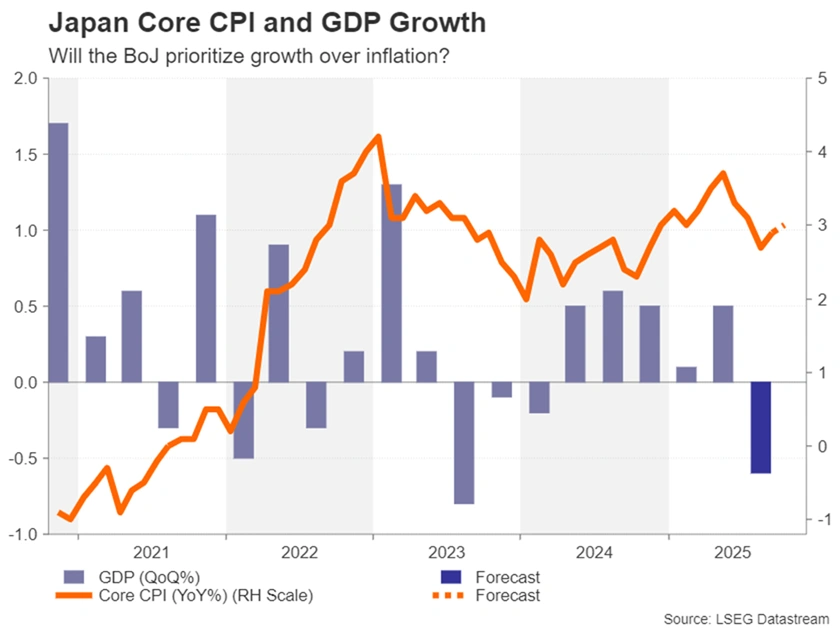

In Japan, consistently above 2.0% inflation has not been enough to convince the Bank of Japan to hike interest rates aggressively. Policymakers continue to fret that wages are not yet growing sustainably fast enough to keep inflation around 2.0%. The new government seems to agree and Prime Minister Sanae Takaichi has openly called on the BoJ to prioritize growth, questioning whether Japan has truly exited deflation.

But the BoJ hasn’t been completely sidetracked by the political pressure and policymakers have hinted that a hike is on the way, although the timing is less clear.

One reason for the caution is the negative impact the trade uncertainty, and the resulting drag on exports, is expected to have had on third quarter growth. Data out on Monday is forecast to show the Japanese economy contracted by 0.6% q/q in Q3.

However, Friday’s CPI report will probably back the need for more tightening. Core CPI is projected to have edged up in October to 3.0% y/y.

Other releases will also be watched such as machinery orders (Wednesday), trade (Wednesday) and flash PMIs (Friday). Hence, an overall strong batch of data could offer the battered yen some much needed relief, especially versus the greenback, where a breach of the 155 level risks government intervention to prop up the currency.