{kind=link}

Week in review

- Kevin Warsh nominated as the next US Federal Reserve Chair.

- Commodity markets saw a sharp reversal, with silver down 27%.

- Key focus for the week ahead: Alphabet and Amazon earnings.

- Central Banks (RBA, BoE, ECB) meet ahead of the January NFP report.

A blockbuster week for global markets with wild price swings, geopolitical risk, Central Bank meetings and a new Fed Chair nominated.

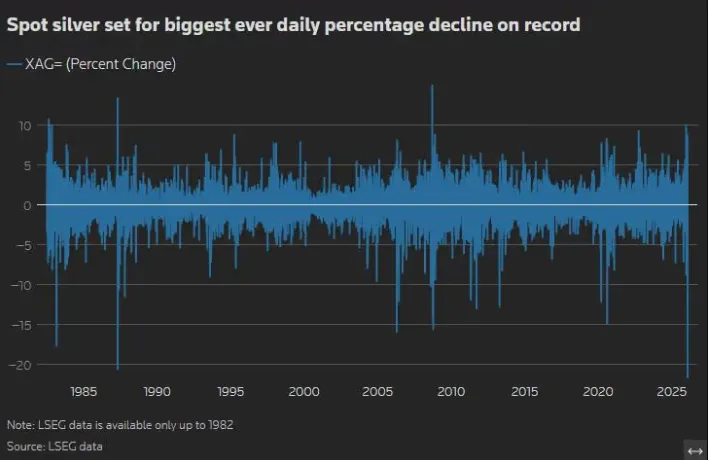

The starting point though has to be the stark reversal in commodity markets on Thursday and Friday which sent markets into a tailspin. At the time of writing, spot silver is down around 27% on the day, on track for their biggest daily drop on record, based on LSEG data available through 1982.

Source: LSEG

Gold on the other hand was down as much as 12%.

The selloff in commodities was driven largely by profit taking as well as a late renaissance for the US Dollar following the announcement by President Trump that Kevin Warsh has been tapped as the next chair of the US Federal Reserve.

Donald Trump mentioned he won’t ask Kevin Warsh (a candidate to lead the central bank) directly if he plans to cut interest rates. However, Trump believes Warsh naturally favors making it cheaper for people and businesses to borrow money.

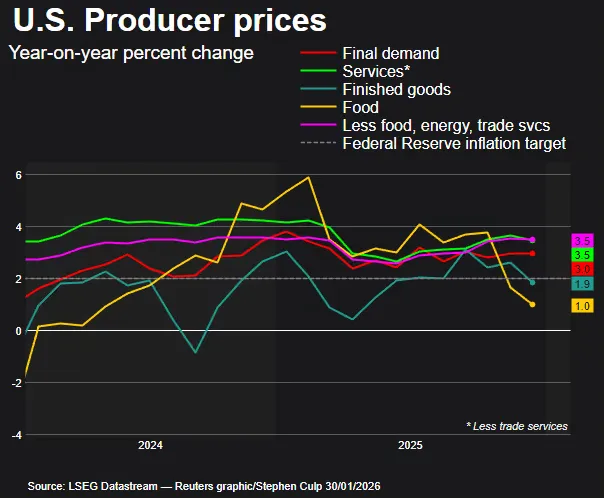

Adding to markets’ late week malaise was a strong US PPI print which came in above the 0.2% estimate of economists polled by Reuters, after an unrevised 0.2% gain in November. Businesses appeared to be passing on higher costs from import tariffs.

Source: LSEG

The stock market saw some mixed results today. Apple’s stock price dropped by nearly 1% after the company shared its latest financial report, which put some downward pressure on the US market.

Despite this drop, the S&P 500 index is still heading toward its first winning week in nearly a month. On a global scale, MSCI’s gauge of stocks that tracks stocks worldwide fell slightly today, but it is still on track to finish the week in the green and have its best month since September.

In Europe, stocks actually performed well with the pan-European STOXX 600 index closing up 0.64%. Strong earnings have helped propel the index to its biggest monthly gain since May. The index registered its seventh straight monthly gain, its longest streak since 2021.

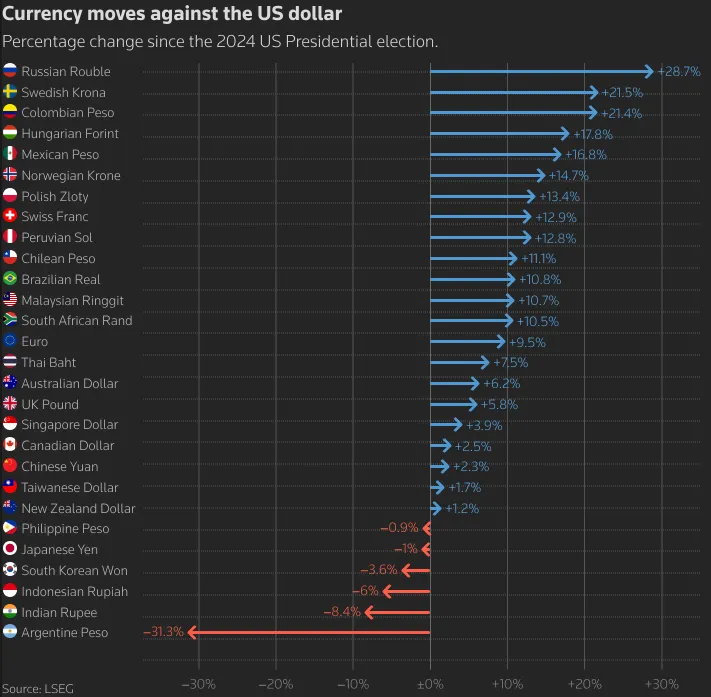

On the FX front, the US dollar got stronger today continuing to show signs of stabilizing after recent weakness. The dollar index which measures the greenback against a basket of currencies, rose 0.57% to 96.73, with the euro down 0.54% at $1.1904.

The dollar was still on track for a second straight weekly decline and third straight monthly drop.

Source: LSEG

The Week Ahead

For the week starting February 2, 2026, markets face a critical junction as the “Magnificent Seven” earnings season continues alongside pivotal central bank decisions and the January US jobs report.

Big Tech Earnings: Alphabet and Amazon

Investors are laser-focused on whether AI investments are beginning to yield significant returns or if capital expenditure (capex) is rising too quickly.

- Alphabet (Wednesday, Feb 4):

- Expectations: Analysts expect Q4 earnings to grow 22.4% to $2.63 per share, with revenue rising 15.5% to $111.4bn.

- The Big Question: Capex is expected to have surged by over 90% to $27.3bn. Markets will look for guidance on 2026 spending; if it exceeds the projected $89.8bn without clear revenue growth, the stock could face pressure.

- Market Sentiment: Options markets imply a potential 5.5% post-earnings swing. Resistance is seen at $350.

- Amazon (Thursday, Feb 5):

- Expectations: Forecasts suggest revenue of $211.3bn (up 12.5%). The key metric will be AWS (Cloud) revenue, projected to grow 21.1% to $34.9bn.

- Market Sentiment: Shares are currently in a “symmetrical triangle” consolidation. A break above $250 would signal a bullish trend, while disappointing AWS growth could send the stock toward support at $220.

US Labor Market: The January Jobs Report

The headline event of the week arrives on Friday, Feb 6 (Saturday morning AEDT).

- Non-Farm Payrolls (NFP): After a soft December (+50k jobs), January is expected to see a slight improvement with 70,000 jobs added.

- Unemployment Rate: Expected to hold steady at 4.4%.

- Market Impact: A stronger-than-expected report could bolster the US Dollar, especially following the nomination of Kevin Warsh as the next Fed Chair, who is perceived as less “dovish” than his predecessors.

Central Bank Decisions (The “Thursday Double-Header”)

Both the Bank of England (BoE) and the European Central Bank (ECB) meet on Thursday, Feb 5.

- BoE: Markets expect rates to stay on hold at 3.75%. However, with UK unemployment at a multi-year high (5.1%), traders will hunt for signals of a rate cut later in Q1 or Q2.

- ECB: Also expected to pause. The focus remains on whether the Euro (EUR/USD) can sustain its breakout above the $1.19 level.

Asia-Pacific: RBA Interest Rate Decision

Closer to home, the Reserve Bank of Australia (RBA) meets on Tuesday, Feb 3.

- The Outlook: Following higher-than-expected trimmed mean inflation (3.4%) and a falling unemployment rate (4.1%), the market has aggressively priced in a 75% chance of a 25bp rate hike.

- The ASX 200: The local index is hovering just 2% below its all-time high (9115.2). A hawkish RBA could create headwinds for the index, though materials and energy sectors remain a source of strength.

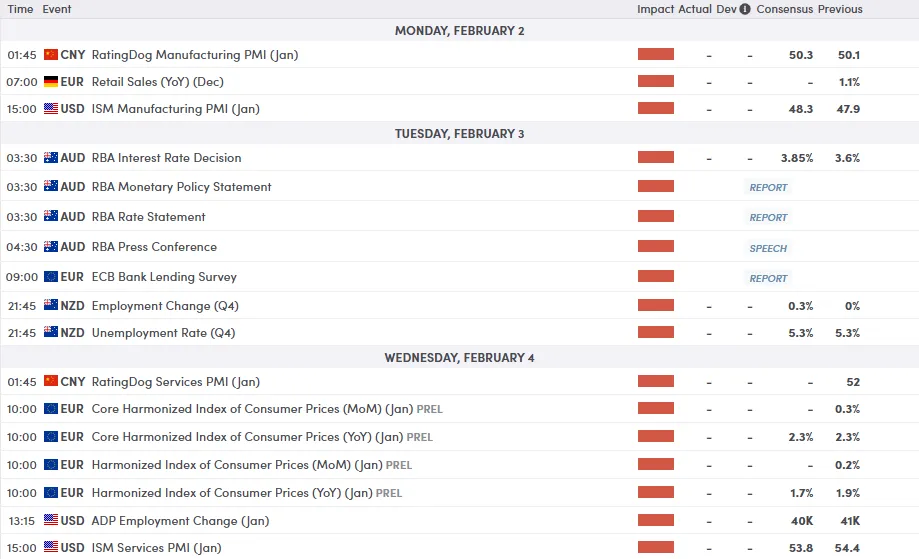

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week – US Dollar Index (DXY)

From a technical perspective, the US Dollar Index (DXY) has made a late week recovery printing a bullish engulfing daily candle close on Friday.

The index has closed above a key resistance level at 96.90 which does bode well for further upside.

The question now is whether the rally is sustainable?

The US dollar is facing several other problems. Conflicts around the world (geopolitics), concerns about how much money the US government is spending (fiscal risks), and the possibility that different countries might work together to lower the dollar’s value (FX intervention) have all been weighing on the Dollar.

If the US DOllar is able to overcome these in the short-term, immediate resistance rests at 97.70 before the 200-day MA comes into focus at 98.62.

A move lower from current prices faces support at 96.37 before this weeks lows around 95.50 comes into focus.

US Dollar Index (DXY) Chart, January 30, 2026

Source:TradingView.Com (click to enlarge)