{kind=link}

- Dollar strength dominates markets as risk appetite remains subdued.

- A Supreme Court ruling, geopolitics and Fed developments are in focus.

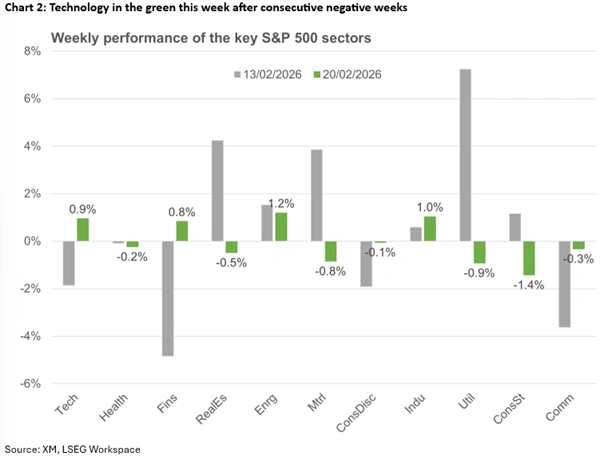

- Pivotal Nvidia earnings on Wednesday as investors question tech sector weakness.

- Yen and aussie diverge; both pound and euro could recoup their losses.

Dollar rally persists

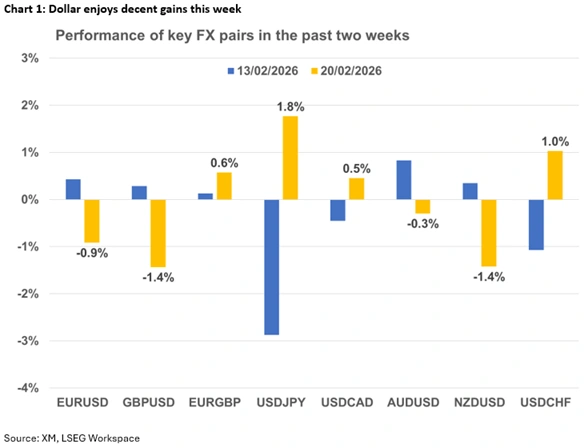

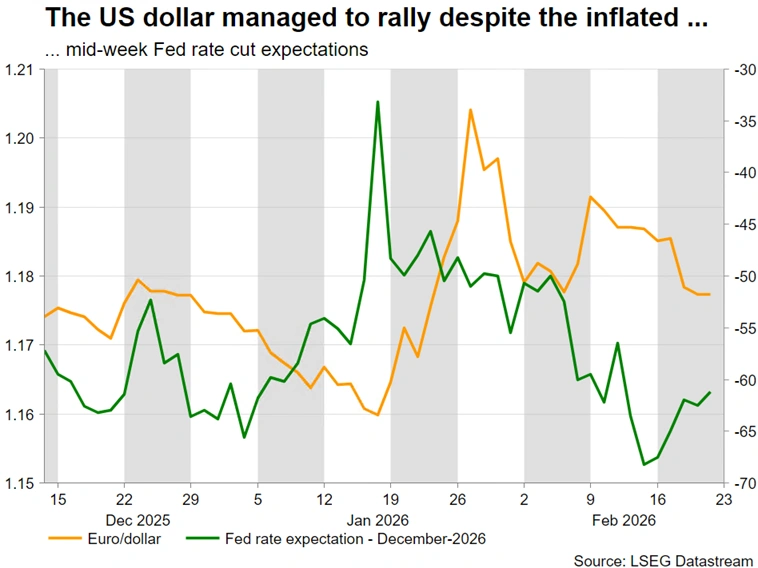

Despite markets pricing in additional easing from the Fed mid-week, the US dollar continues to perform strongly, posting gains across the FX spectrum, partly due to the geopolitical newsflow. Barring a major surprise on Friday with the announcement of the Supreme Court’s ruling on tariffs, this trend is likely to persist into the weekend if Friday’s key US data confirm the US economic strength and the lower inflationary pressures.

At the same, investors are trying to figure out the lingering weakness in US technology stocks. Is this a rotational shift into defensive and value stocks in anticipation of gradual US growth moderation, or just a temporary pause as companies adjust to the AI revolution? This dilemma will be partly answered on Wednesday, when Nvidia reports earnings after the US market closes. Unsatisfactory results and, more importantly, more conservative forward guidance could amplify the current weakness.

Fed in the spotlight, light data calendar

The Fed is unable to support risk appetite as it appears to be stuck in limbo. The chances of a rate cut under Chair Powell have diminished, predominantly due to the recently strong US data releases, and the continued attacks from the US President essentially limiting Powell’s willingness to meet Trump’s demand. This probably means that Fed meetings may lose some of their market-moving potential until June, with investors focusing instead on Kevin Warsh’s nomination hearings.

The process is currently stalled at the Senate Banking Committee, where senators are frustrated about the Fed probe against Powell over the Fed HQ renovation costs. Despite Treasury secretary Bessent’s optimism, no date for Warsh’s hearing has been set, gradually raising the probability of Powell remaining in position beyond May 15, and upsetting the robust rate cut expectations. This may sound far-fetched, but concerns appear credible given that Powell testified at the Senate Committee on Banking three months before taking office in February 2018.

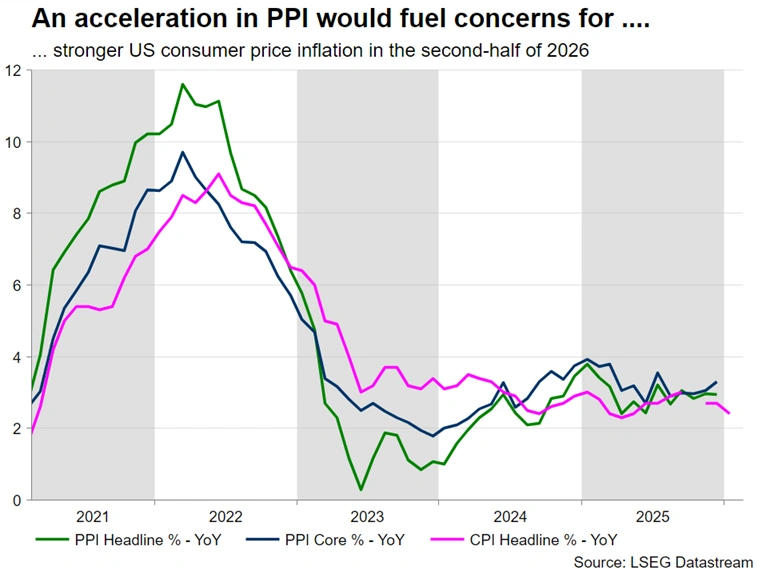

Meanwhile, Fedspeak continues at full throttle. Investors tend to react more favourably to dovish rhetoric, limiting the dollar’s upside momentum. Next week’s data calendar is rather light, with Tuesday’s CB Consumer Confidence and Friday’s Producer Price Index report providing further insight into the economic trends. Interestingly, two-, five- and seven-year US Treasury auctions will take place next week. Investors are focusing on the level of foreign demand, with this week’s moves in US yields suggesting interest in Treasuries.

Wildcards could dent risk sentiment

If the Supreme Court judges refrain from publishing their tariff ruling on Friday, there are two additional ‘decision’ dates next week, Tuesday and Wednesday, February 24 and 25, respectively. The focus here is not just on the fate of tariffs, which if needed will be reimposed using different legislation, but on whether Trump will be allowed to act independently on such issues, ignoring Congress. This is key, since a loss of majority in either chamber at the November midterm elections would complicate Trump’s ability to govern.

Additionally, should the ruling strike down tariffs, the Trump administration might have to return some tariff revenue that has already been collected, which would blow a fresh fiscal hole into an already big federal deficit. Hence, a ruling announcement could prove extraordinarily market-moving across asset classes.

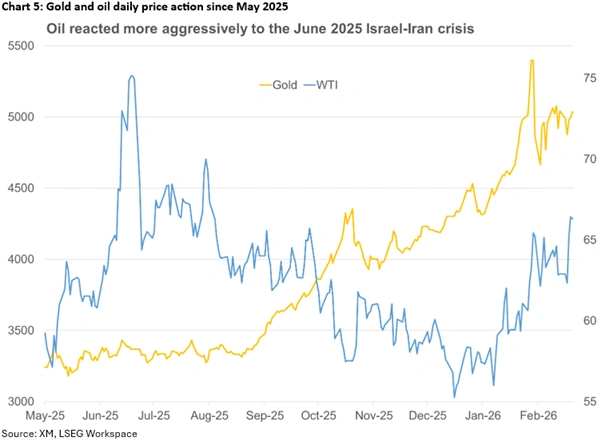

At the same time, there are numerous reports about an imminent US strike on Iran, despite the positive newsflow regarding the ongoing negotiations. Gold and oil are poised to further benefit from an escalation but the aftermath matters. Should Iran retaliate, potentially drawing Israel into the crisis, market reaction could resemble the June 2025 price action, when both the dollar and gold got a sizeable boost, but oil was the clear protagonist, skyrocketing to $80. Interestingly, gold has been struggling to reclaim the $5,000 level, potentially suffering from the Chinese holiday and the persistent strength of the US dollar.

The Yen and the Aussie are under close market scrutiny

Certain currencies could be in the spotlight next week. In particular, the yen continues to attract market interest, as the post-election rally appears to be reversing after testing the 152 zone.

Japanese PM Takaichi is preparing for her second term, with investors gradually questioning the implementation of her pre-election promises and their impact on the debt burden. The leader of Ishin, the junior coalition partner, has touted the idea of using the vast foreign exchange reserves to cover funding needs without tapping the bond market, but the implementation of this idea might not be so straightforward.

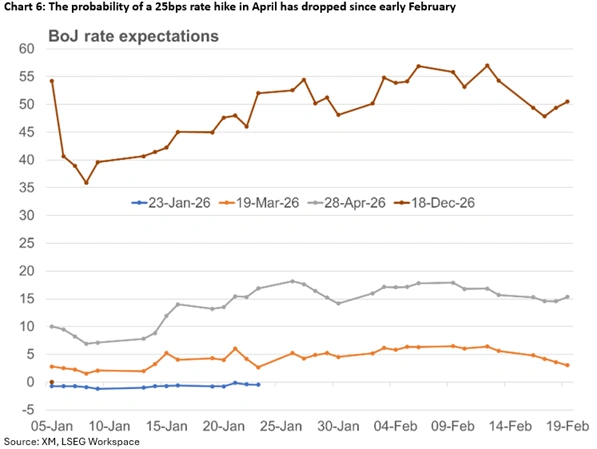

In the meantime, speculation is rife about the timing of the BoJ’s next rate hike. With the data softening lately, a weaker-than-forecast Tokyo CPI on Friday may further dent the chances of a rate move at the April meeting. Notably, it will be interesting to see whether the recent Takaichi-Ueda meeting could alter the BoJ’s current stance going forward. Should this occur, coupled with concerns about the planned aggressive fiscal spending, the door for a dollar/yen rally would be wide open.

Similarly, the aussie remains in the headlines due to the RBA’s hawkish stance and for successfully resisting the current US dollar strength. Following a robust set of labour market prints, the focus shifts to next week’s monthly inflation figures. The last CPI report before the March 17 meeting could go a long way into sealing expectations for a May rate hike, potentially even prompting the RBA to indirectly ‘announce’ this move at the next gathering, and helping aussie/dollar break above the early February 2022 high of 0.7157.

Both the pound and Euro could see increased volatility

Despite the potent retail sales figures, the pound has had a difficult week. Soft data have been added to the recent dovish BoE meeting and last week’s short-term political unrest, pushing the probability of a March rate cut to 78%. That said, despite the myriad of issues, the pound has not fallen off a cliff, partly benefiting from positioning. A potential drop below the 1.3400 zone in pound/dollar, though, could mark the beginning of a sizeable correction.

Positioning appears to be a major issue in euro/dollar as there is an exceptionally large short position against the dollar. This could explain the euro’s recent difficulty in taking advantage of the inflated Fed rate cut expectations.

It has been a quieter period for the eurozone, with data prints unable to materially challenge current ECB rate expectations, keeping the doves quiet. The highlight of next week’s calendar is Friday’s German preliminary CPI report. A very weak print could rejuvenate the ECB doves, mostly to no avail, thereby denting the euro’s appeal.

However, the burning issue appears to be rumours about Lagarde stepping down before November 2027. Could a German finally take the ECB helm, or could a less hawkish option could be explored, ensuring a smooth transition into the new era, and avoiding a rally in the euro? Notably, an early departure by Lagarde would mean that, for the first time ever, both the Fed and ECB heads will be selected/replaced in the same period, adding a rare level of uncertainty to markets.