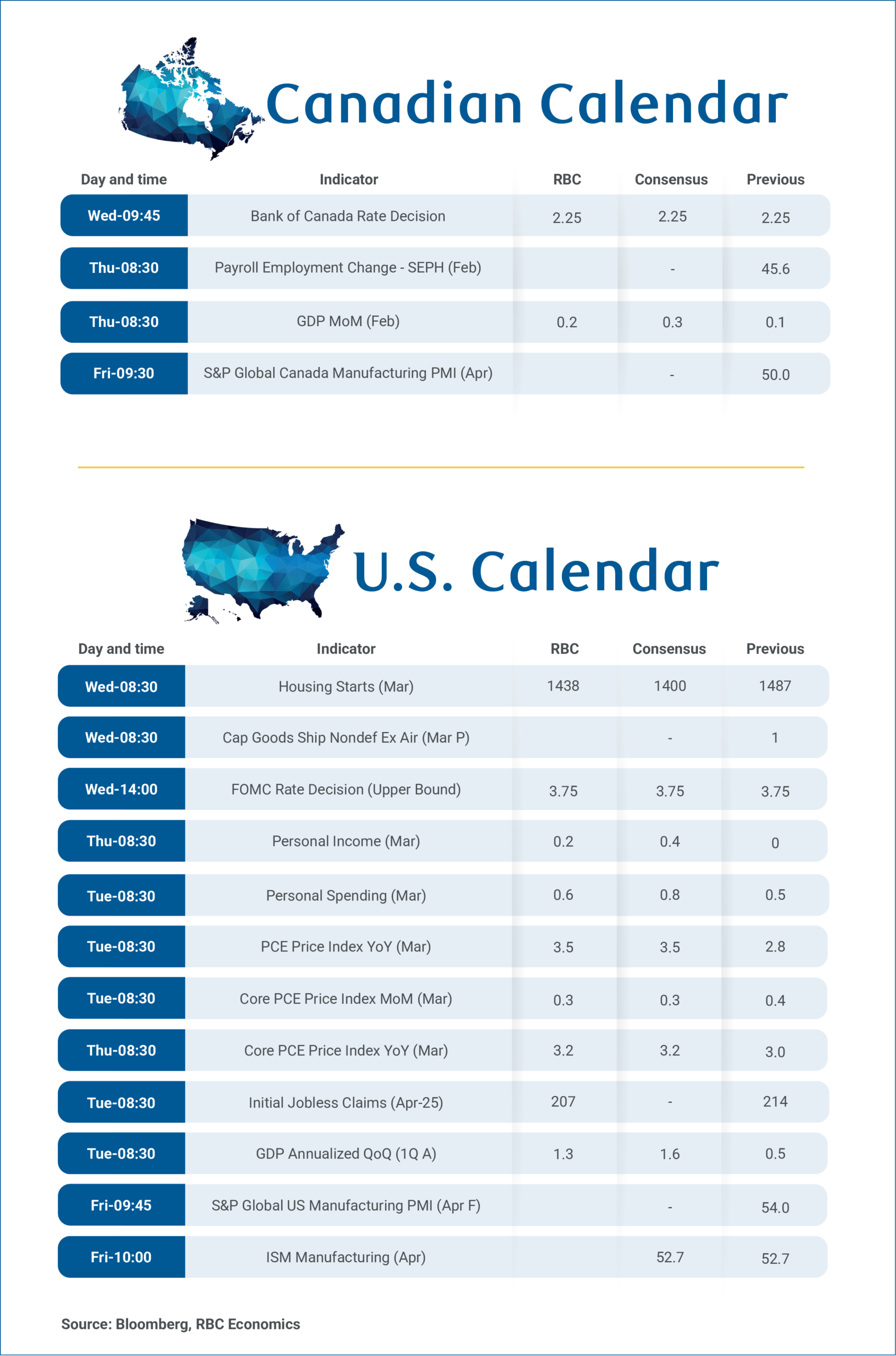

The focus will be on the Bank of Canada’s decision on interest rates on Wednesday amid rising consumer prices, followed February’s gross domestic product print on Thursday.

We expect the BoC will hold interest rates unchanged for a fourth consecutive meeting, but policymakers will be watching the impact of higher energy prices on inflation closely. Headline CPI growth looks likely to rise above the 1% to 3% inflation target range in April for the first time since December 2023.

But there is nothing that BoC interest rate policy can do to influence the global price of oil. And lags in the impact of interest rates on the economy mean the central bank needs to set monetary policy based on where inflation will be in the future, not just where it is today.

We expect the BoC will be cautious about adding to near-term affordability challenges created by a supply-driven surge in fuel costs as long as inflation expectations and broader inflation pressures (outside of energy price increases) remain contained.

Inflation expectations did edge higher in the BoC’s Business Outlook Survey, but further signs of easing in “core” measures in March should leave the central bank flexibility to focus on incoming data against its recent projections.

Q1 GDP growth is tracking broadly in line with the Bank’s January forecast with recent data pointing to a modest pickup in momentum following a softer start to the year. Labour market conditions have also shown signs of stabilization, but with the unemployment rate still at levels that wouldn’t imply underlying inflation pressures building.

This combination suggests limited urgency for further policy adjustment in the near term. Our base case forecast assumes rates remain on hold through 2026 with gradual increases beginning in 2027 as the economy continues to normalize.

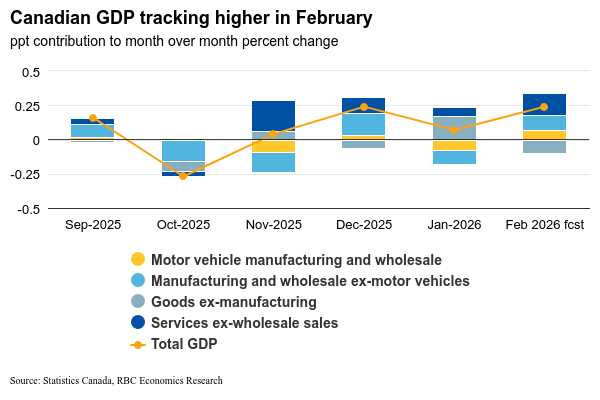

Growth in goods and services to hold up GDP

We expect real GDP to increase by 0.2% in February in line with Statistics Canada’s advance estimate. Industry data points to continued growth in goods and services sectors with manufacturing and wholesales recovering as earlier auto production disruptions faded. Retail volume also continued to increase in the month (+0.3%), highlighting ongoing resilience in consumer spending.

Partially offsetting these gains is non-conventional oil and gas extraction in Alberta that appears to have pulled back in February. Housing-related activity also remained a drag with home resales continuing to decline, albeit at a slower pace.

Early indicators for March suggest growth momentum has been maintained into the end of Q1. Hours worked edged higher by 0.2%, alongside other signs of steady economic activity. Advance manufacturing sales rose 3.5% in March—in part reflecting higher petroleum prices, but also consistent with further recovery in auto production from earlier disruptions. Excluding petroleum and related products, advance wholesale sales also rose 1.3%, driven by higher machinery, equipment, and supplies sales

Taken together, data for Q1 are tracking between our forecast of 1.3% annualized growth and the BoC’s January projection of 1.8%.

U.S. Fed also seen on hold

The U.S. Fed will also be watching the impact of the conflict in the Middle East on inflation closely but is expected to leave interest rates unchanged for now. Higher oil prices are putting pressure on both ends of the Fed’s mandate – higher gasoline prices are cutting into household purchasing power (threatening to slow consumer spending, with negative implications for labour markets) but also pushing headline inflation higher. And broader core inflation measures in the United States remain elevated with the core PCE deflator expected to rise to 3.2% year-over-year in March. We continue to expect the central bank to hold interest rates at current levels through the end of this year.

- We expect U.S. GDP rose 1.3% (annualized rate) in Q1 following a 0.5% increase in Q4. Consumer spending growth appears to have slowed from 1.9% in Q4, but government spending likely rebounded following a drop in Q4 due to a federal government shutdown, and business investment likely continued to rise.

- We expect a 0.6% increase in March personal spending, but with much of the gain reflecting increased prices (surge in gasoline prices due to conflict in the middle east.) We look for real consumer spending to edge up 0.2%. Both headline and core PCE price deflator growth is expected to tick higher on a year-over-year basis in March.

{kind=link}