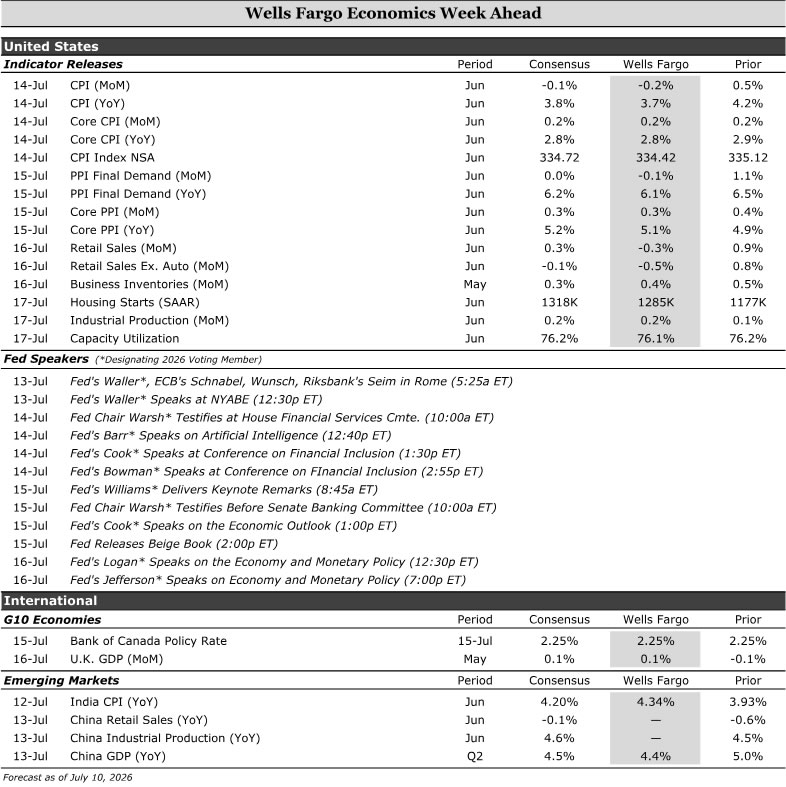

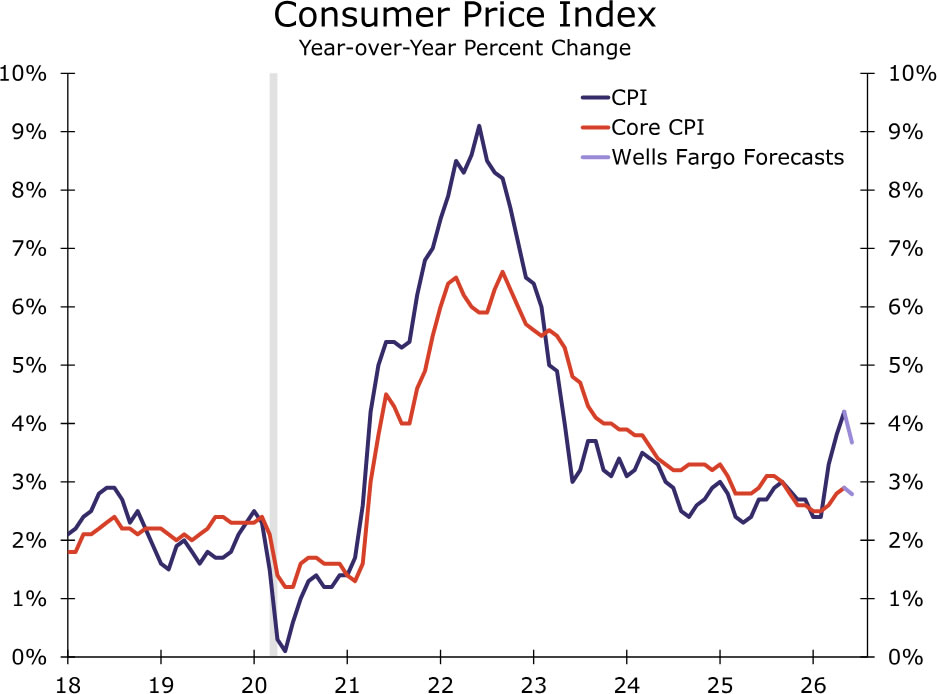

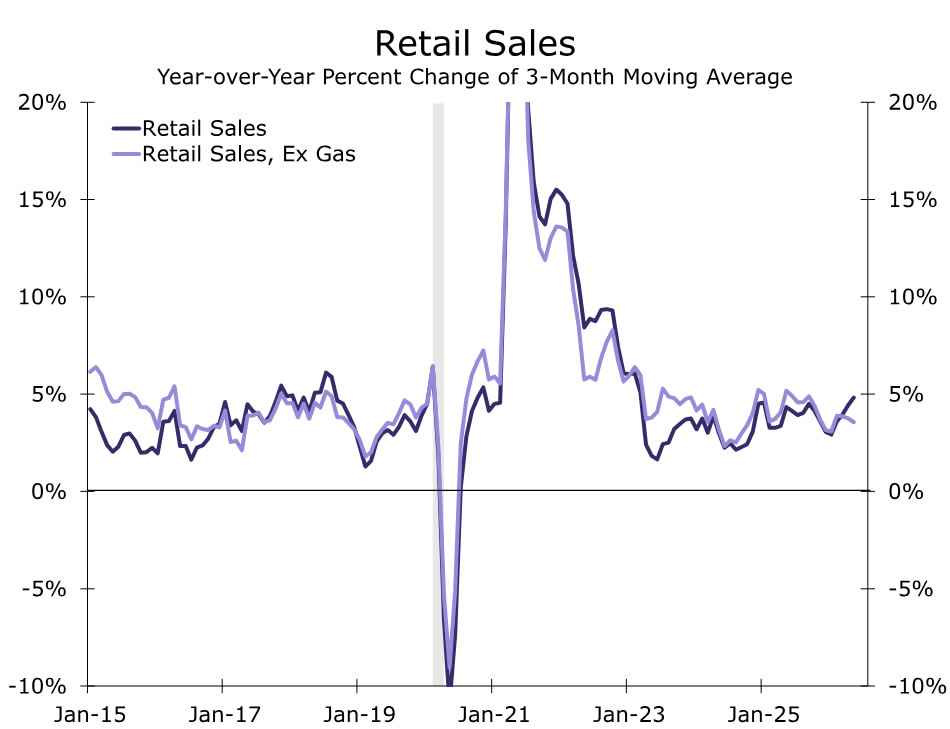

Next week’s headline CPI reading is expected to cool, largely reflecting a decline in energy prices. Retail sales are also expected to soften, driven in part by lower gasoline prices. While consumer spending has remained resilient, weakening fundamentals could become a headwind in the months ahead. We expect housing starts to rebound, but it will not be sign of renewed momentum in the housing market.

In Canada, we expect the BoC to leave rates unchanged. In the U.K., economic growth is expected to rise slightly with services being the largest contributor to growth. Among emerging markets, India’s CPI print is expected to move higher, complicating the Reserve Bank of India’s policy outlook. In China, we expect Q2 GDP growth to slow.

- United States: CPI (Tuesday), Retail Sales (Thursday), Housing Starts (Friday)

- G10 Economies: Bank of Canada Monetary Policy Meeting (Wednesday), U.K. Monthly GDP (Thursday)

- Emerging Markets: India CPI (Monday), China GDP (Wednesday)

U.S. Week Ahead

CPI • Tuesday

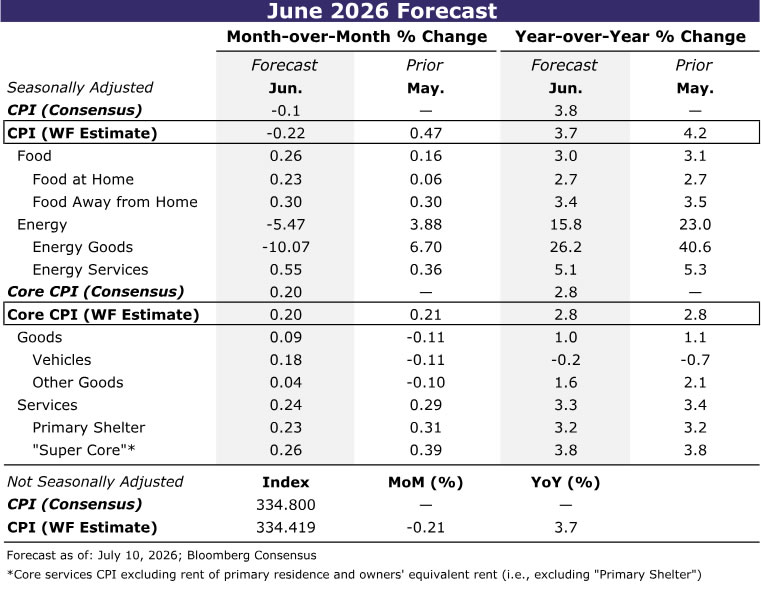

Inflation pressures eased for households in June thanks primarily to retreating gasoline prices. We estimate the CPI declined 0.2% over the month amid a ~10% drop in the price of energy goods. Food prices, however, are likely to have moved higher after a subdued May reading. Earlier increases in energy and transportation costs are still working their way through supply chains, while recently announced grocery price cuts won’t leave a mark on the data until July.

Excluding food and energy, we estimate the core CPI rose 0.2%. Core goods inflation is expected to firm, driven partially by vehicles. Outside of autos, the recent rate of disinflation in prescription drugs and tariff-sensitive categories may prove difficult to sustain as the trade policy shock fades further in the rear-view mirror.

Core services inflation, meanwhile, should moderate in June. Primary shelter inflation is due for some payback after May’s above-trend gain. Travel-related services also should provide some relief, with lower jet fuel costs contributing to softer growth in airfares. Medical services inflation likewise appears positioned to cool following unusually strong gains in hospital and physician services in May.

Taken together, June’s CPI report should point to some slowing in underlying inflation. While supply-side developments continue to generate volatility in a handful of categories, the broader data do not suggest inflation pressures are re-accelerating across the economy.

Retail Sales • Thursday

Lower gasoline prices should weigh on headline retail sales in June. We forecast overall sales to decline 0.3%, reflecting the roughly $0.50 drop in average pump prices during the month. While Tuesday’s CPI data will provide a more complete picture of households’ price exposure, energy prices should account for most of the weakness in nominal sales.

Outside of gasoline, high-frequency credit card data point to some moderation in spending, but we still expect underlying retail sales to rise modestly.

More broadly, underlying consumer spending has remained resilient this year. Larger individual tax refunds have helped offset the drag from higher energy costs, supporting household purchasing power. That said, consumer fundamentals appear less secure. Real disposable income growth has softened amid compounding inflation and a cooler jobs market forcing households to spend more of their income or rely on credit and/or wealth to sustain spending.

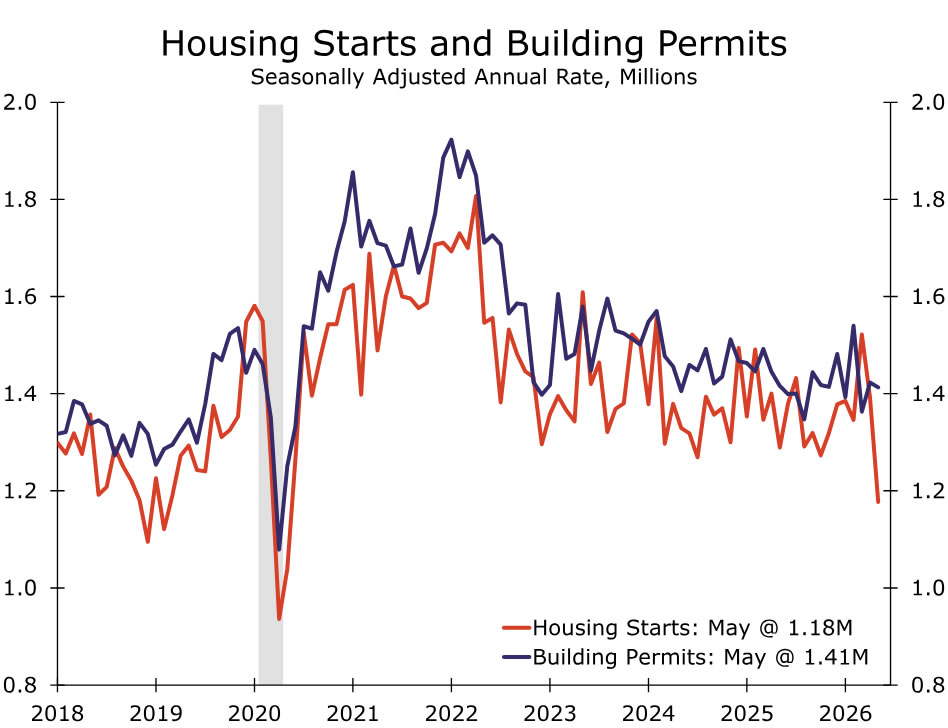

Housing Starts • Friday

We anticipate residential construction rose to 1285K in June, partially rebounding from the previous month’s pronounced decline. That’s not to say we believe housing starts are now on an upswing, only that May’s unusually sharp pullback likely overstated the downshift in activity that has been evident for much of the year. In our view, the recent decline in permits, which are down 2.6% year-to-date through May, is more reflective of the underlying trend.

The most recent NAHB Housing Market Index points in a similar direction. Builder sentiment edged lower in June, which suggests home builders are becoming increasingly cautious amid still-elevated inventory levels and lackluster pace of new home sales due to the challenging affordability backdrop. Meanwhile, high capital costs and soft apartment market conditions remain as a significant limitation on new multifamily development. All told, we expect housing starts bounced back in June. On balance, however, activity is still likely losing momentum.

G10 Week Ahead

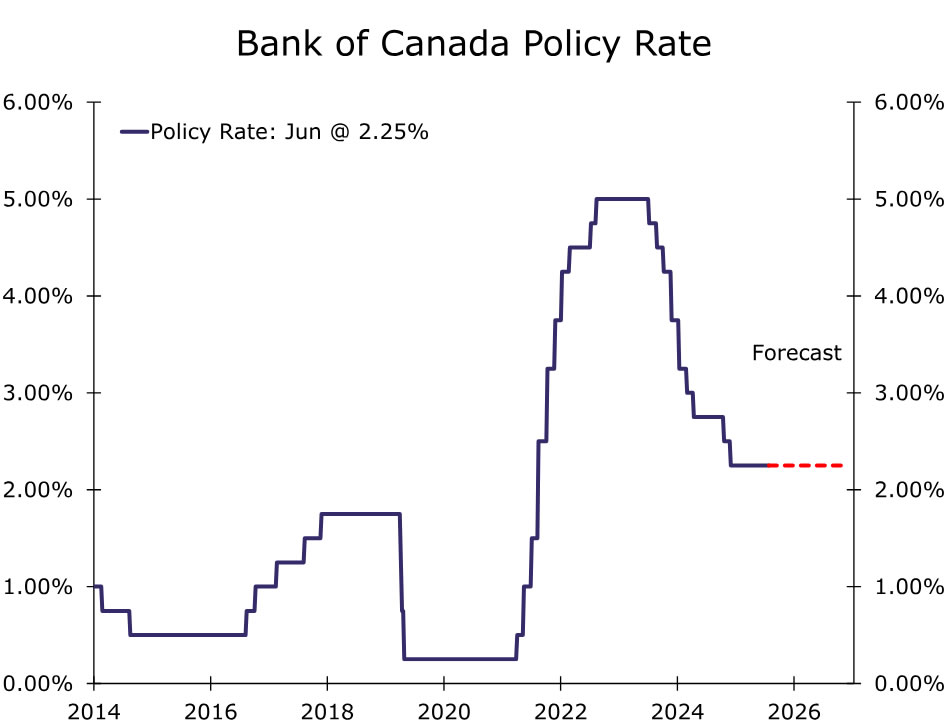

Bank of Canada Monetary Policy Meeting • Wednesday

We expect the Bank of Canada (BoC) to remain on hold next week, leaving the policy rate unchanged at 2.25%. Since the June meeting, the backdrop has been somewhat mixed. Following a softer-than-expected Q1 GDP print, monthly GDP rebounded in April, though purchasing manager surveys point to some moderation in activity through June. The latest employment report showed a modest headline gain and a decline in the unemployment rate to 6.5%, but underlying labor market conditions remain uneven.

At the same time, underlying inflation pressures remain relatively contained. Headline inflation has moved higher alongside rising oil prices, but measures of core inflation have shown little sign of broadening price pressures that would require a near-term policy response. While developments in the Middle East and the resulting path for energy prices remain an important upside risk to inflation, the BoC is likely to look through commodity-driven price increases unless they begin to feed more meaningfully into underlying inflation trends.

Recent survey data reinforce that view. The BoC’s latest Business Outlook Survey showed inflation expectations remain generally well anchored. While average inflation expectations over the next two years moved higher, one-year-ahead expectations continue to trend lower and five-year expectations were largely unchanged. Taken together, the data should give policymakers confidence that inflation expectations remain contained even as headline inflation faces near-term energy-related pressures.

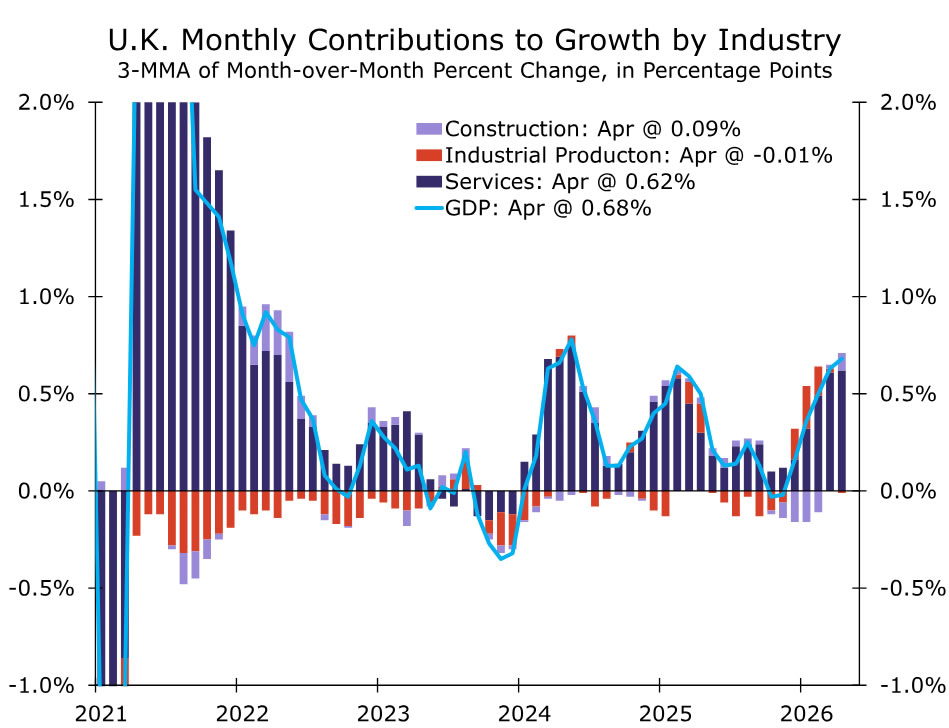

U.K. GDP • Thursday

Next week’s U.K. GDP release will provide another indication of whether growth is holding up despite a softer survey backdrop. We expect GDP to rise 0.1% month-over-month in May, with services activity remaining the primary driver of growth and manufacturing providing some support following stronger orders and front-loading activity in recent months.

Recent activity data have been mixed. GDP rose 0.7% in the three months through April, but monthly GDP contracted 0.1% month-over-month in April as services output declined. Forward-looking indicators suggest growth momentum remained modest in May. The services PMI fell into contraction territory for the first time since April 2025, while construction activity remained weak. Although manufacturing may provide some near-term support, recent strength could obscure underlying softness in the broader economy if services continue to ease. Early June survey data offer little sign of a rebound, pointing to subdued growth through Q2.

An upside surprise in GDP would indicate that activity has remained more resilient than confidence indicators suggest. Uncertainty in the Middle East remains elevated, raising the risk that higher energy prices feed through to U.K. households through the Ofgem price cap mechanism. Combined with persistently sticky services inflation of 3.6% year-over-year, these potential second-round inflationary pressures remain a key concern for BoE policymakers. As such, we continue to expect the BoE to deliver two 25 bps hikes this year.

EM Week Ahead

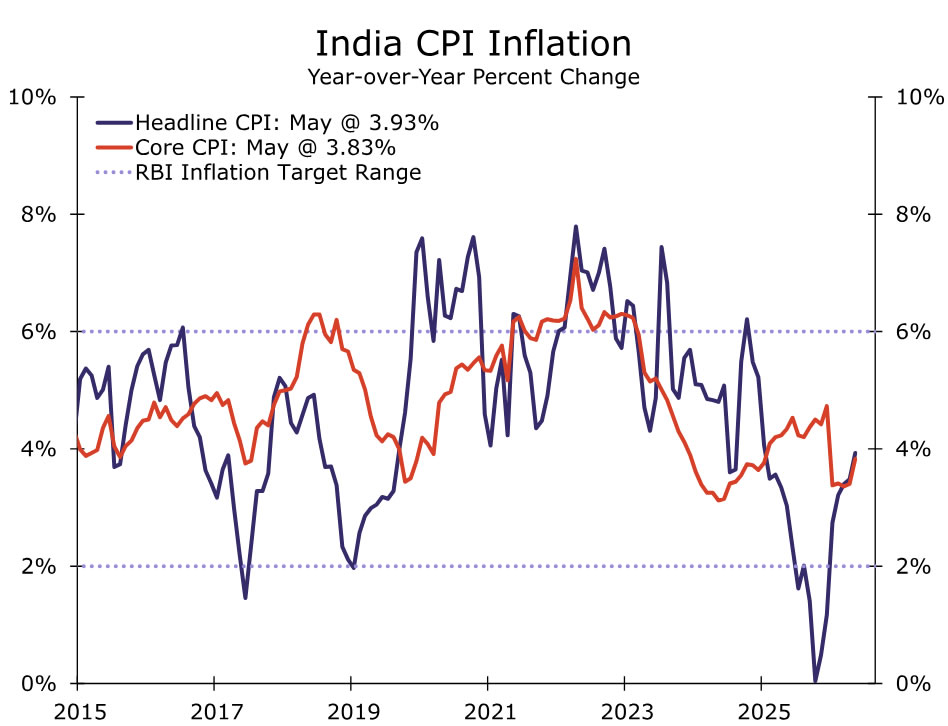

India CPI • Monday

India’s June CPI release is due next week, and we expect headline inflation to rise to 4.34% year-over-year (from 3.93% in May), driven mainly by food and energy prices. Core inflation (excluding food, fuel and light) also firmed to 3.83%, though inflation pressures have yet to become clearly broad-based.

The Reserve Bank of India (RBI) has so far maintained a “wait-and-watch” approach, but its latest projections point to rising inflation pressures alongside softer growth. At its latest meeting, the RBI kept the policy rate on hold at 5.25% and lowered its 2026 growth projection to 6.6%, while revising inflation higher, with CPI expected to average 5.1% in 2026 and peak at 5.9% in Q3. The RBI’s updated forecasts underscore a more challenging inflation-growth trade-off. A war-driven increase in crude import costs could widen the current account deficit, while a weaker rupee compounds imported inflation. El Niño risks further amplify upward pressure on food prices.

Against this backdrop, we continue to see policy risks skewed toward tightening. We maintain our view for two rate hikes this year, one in Q3 and one in Q4, bringing the Repurchase Rate to a terminal rate of 5.75%.

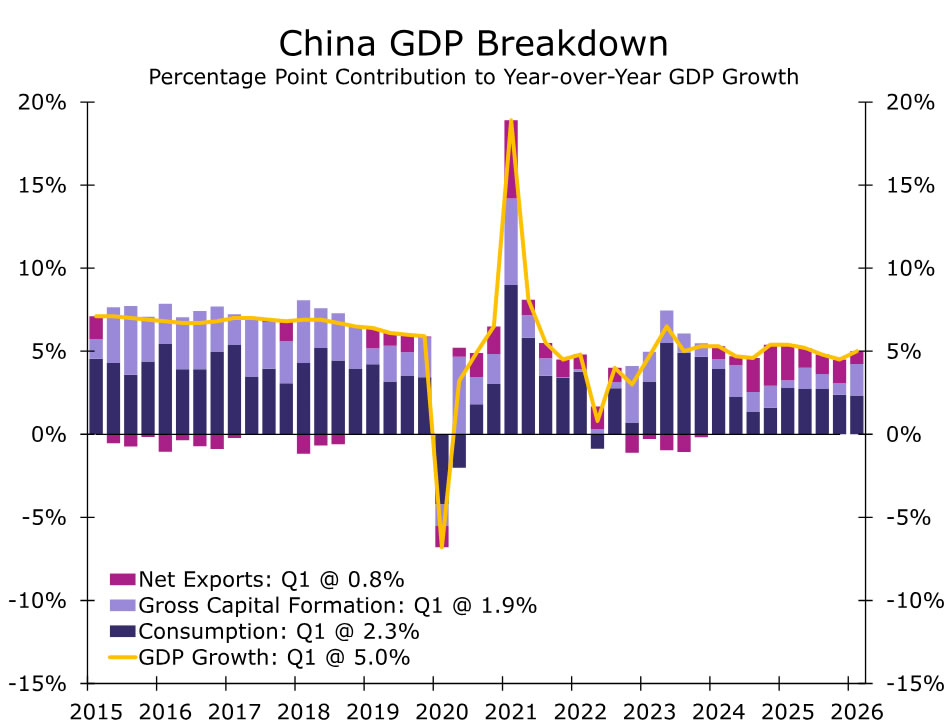

China GDP • Wednesday

China’s Q2 GDP release is due next week, alongside June data for industrial production and retail sales, and should provide a clearer picture of the extent of the economy’s loss of momentum during the second quarter. We expect GDP growth to slow to 4.4% year-over-year, down from 5.0% in Q1.

The underlying details are likely to highlight continued divergence across sectors. Industrial activity appears to have held up relatively well, supported by external demand and technology-related production. Recent PMI data point to some resilience in manufacturing, suggesting that factory activity has remained broadly stable. That said, export-driven strength has likely only partly offset weak domestic demand and ongoing pressures in the property sector. On the consumer side, momentum remains soft. Retail sales likely continued to struggle in June, consistent with a still-subdued services backdrop. Robust exports, particularly those linked to global AI demand, have helped cushion the impact of trade disruptions and higher energy costs stemming from geopolitical tensions, but have not been sufficient to drive a broader domestic recovery.

Looking ahead, domestic demand is likely to remain constrained by weak consumer confidence and ongoing challenges in the property sector. While the upcoming data should reinforce the case for additional targeted stimulus, we do not expect policymakers to shift toward broad-based easing. Against this backdrop, we continue to forecast China’s GDP growth slowing to 4.5% in 2026 and 4.3% in 2027.

{kind=link}