Sample Category Title

GBP/USD Analysis: Stranded In Narrow Range

The Pound showed high volatility against the US Dollar on Monday, as the pair was trading in the 1.4063/1.3941 area during this time. Strong bearish sentiment took over the market mid-session when the rate plunge 121 pips within a couple of hours.

It has since been moving in a narrow range, thus not being able to surpass the strong bounds of the 55– and 100-hour SMAs, the weekly PP and the 38.20% Fibo retracement. Given that the northern barrier is likewise limited by the 200-hour SMA and the monthly PP, the Sterling might fail to make big advances in either direction for a couple of hours.

It is expected that support surrenders soon, forcing the rate down to the weekly S1 at 1.3871. In case fundamentals do not disrupt the current market sentiment, the rate is unlikely to move above 1.40.

USD/JPY Analysis: Two Scenarios Possible

Weaker US Dollar put downward pressure on USD/JPY early on Monday, thus allowing the pair to plunge down to the 106.50 mark. The subsequent hours saw a slight recovery up to 117.00.

The rate's movement since mid-yesterday has been bounded between the 55-, 100– and 200-hour SMAs. It is likely that the direction of the breakout determines the US Dollar's movement during the following 24 hours.

Technical indicators are more supportive of the bearish scenario that should send the rate towards the weekly S1 at 106.00—a move that would likewise confirm the upper boundary of a short-term channel down.

On the other hand, a northern breakout of the 100-hour SMA and the weekly PP circa 107.00 is expected to result in a surge up to the 107.50 mark.

What To Expect From Powell’s First Major Speech

Jerome Powell is the new Fed chair replacing Janet Yellen after her term expired this month and without doubt market watchers are eagerly waiting to hear whether his views on the economy support the pre-existing monetary policy script. Therefore, Tuesday will see investors turning their ears to Powell's first major speech in front of the House Financial Services Committee, while on Thursday the new Fed boss will testify before the Senate Banking Committee.

Before Powell sits on the Fed chair, a surprising rise in wage growth last month triggered the stock-market melt-down as investors speculated that inflation would pick up sooner than expected and thus the Fed would start increasing interest rates faster than previously thought. Consequently, the 10-year US Treasury yields surged to four-year highs, but the dollar index oddly took a knock falling to three-month lows against a basket of major currencies, a phenomenon probably attributed to renewed worries over the twin deficits in the US following the approval of a two-year government spending plan and Trump's recent tax reforms aiming to deliver massive tax cuts to businesses. Now, the ball is in Powell's hands and markets want to confirm that his views on inflation and interest rates are in line with those of Yellen's as he has been so far seen as mister continuity, while most importantly they are curious to see how he will manage to express himself without causing any market turbulence.

Indeed, Powell, testifying on behalf of the FOMC committee before the Congress at 1500 GMT (prepared statement delivered at 1330 GMT) has no reason to hold a dovish stance as recent Fed remarks have sent clear hawkish messages. January's FOMC meeting minutes released on Wednesday revealed that the majority of the board members were sanguine that inflation, currently standing at 1.5% y/y, would gain steam this year and rise towards the Fed's 2.0% only in the medium-term. Besides that, policymakers decided to upgrade their economic projections made in December acknowledging that the country's positive economic performance, accommodative financial conditions and Trump's tax cuts, which are already in the pipeline, would unleash further growth. However, they judged that any rate hikes should come at a gradual pace in order to support a healthy expansion. Yet, the confidence vibes found in the minutes reinforced speculations that rates could pick up more than the three times the Fed currently predicts.

In case Powell holds a hawkish tone, potentially hinting that the Fed might use a more aggressive path to tighten monetary policy, traders might put more weight on his words than normal, setting off another round of stock market selloffs. Powell is not a stranger in the industry but he is new in the role and markets are expected to react more sensitively until they become more accustomed to his language patterns and way of thinking. Particularly, stock investors see the next pain threshold at 3.0% in terms of bond yields given that any break above this level would make equities less attractive compared to fixed income assets. In the previous week, the US 10-year Treasury yields topped at a four-year high of 2.95 in the wake of the Fed meeting minutes.

Hence, the new Fed chair is more or less anticipated to back statements expressed in January's FOMC meeting, highlighting the bullish outlook of the economy but since he would also like to keep financial markets calm, he will probably avoid indicating how fast should interest rates rise.

Turning to forex markets, encouraging remarks arising from Powell's speech could drive dollar/yen could back above to the previous high of 107.90, while if his comments really please investors, the pair could touch the 108 and 109 psychological marks.

On the other hand, a disappointing speech could pressure the pair towards the 106 handle, whilst in the worst scenario, dollar/yen could breach the previous low at 105.52 diving to fresh three-month lows, likely near the 104 key-area.

Sky Received Another Offer | European Markets And US Futures Higher | Cryptos In Green

Bull rally may not derail that easily

Fed chairman’s testimony could shock the financial markets

US core durable good number may drop to 0.4%

A green start to the week for the cryptocurrency markets

Investors have started to bet once again that the Fed’s monetary policy stance may not be that hawkish and perhaps the bull rally may not derail that easily. The S&P500 index has recovered most of its losses which occurred a few weeks ago and the Japanese markets have climbed to their best level which is not seen in more than three weeks. Looking at the daily chart of the S&P500 index from a technical perspective, the reverse head and shoulder pattern clearly stands out. The projection of this pattern, if fully played out, could easily push the price to another all-time high.

Nonetheless, how aggressive the pace of the monetary policy would be over in the US would remain a chief debate amidst investors. The new Fed chairman’s testimony has the potential to shock the financial markets as investors are not expecting any hawkish stance from him. Mr Powell, the new Fed Chairman, would have to stick to the script and he needs to assure the market that the path for the interest rate hikes would be a gradual one.

For currency traders, traders are wary of placing any large bets ahead of the new Fed Chairman’s testimony and the upcoming US NFP data. The US core durable good number is expected to show a drop to 0.4% from the previous number of 0.7%. Any increase in the purchase orders in this data would send the signal that manufacturers are less wary off interest rate hikes and the business sentiment is strong. We also have the consumer confidence data due later which could bring some swings in the dollar index. The forecast is an improvement in the consumer confidence from its previous reading of 125.4, the forecast is for 126.2.

As for the Euro, the chances are that we may get a break to the upside and provided that the new Fed Chairman does not ruffle any feather, the central bankers' speciality. Yesterday’s dovish comments by the ECB’s president pushed the euro lower against the dollar, catching out a few overeager bulls. However, at the same time, the president also ruled out any currency war with the US on F.X policy, this leaves the door open for the euro bulls. A strong German CPI number would mean that the ECB would face more pressure from Bundesbank to wind down the tents of easy money sooner than later.

Gold

The precious metal is struggling to hold on to gains despite the weaker dollar. Overall, it does appear that the traders have a bullish bias towards the shinning metal and looking at the overall bets, it appears that traders are planning for an upside move ahead of the Fed chairman’s testimony. Inflation qualms would continue to support the metal as traders use the yellow metal to hedge their risk against inflation.

Cryptocurrency

A green start to the week for the cryptocurrency markets, partly fuelled by Turkey’s proposition of introducing its own national cryptocurrency. Perhaps talks from the European Commission on how to regulate cryptos will provide headwinds to this bullish momentum. However, it generally seems that crypto traders have grown wiser when it comes to filtering what they read about this new asset class in the news.

SKY Gets Another Bid

Sky PLC, a pay television broadcasting service, received another bid but this time not from Rupert Murdoch’s company. Comcast Corp decided that they see a value play in acquiring Sky and the company jumped into the fray by challenging 21st Fox Inc and Walt Disney’s offer. The cash offer of 12.50 pounds per share from Comcast has set the bar really high for Fox.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2331

The resistance at 1.2370 is still intact and the bias is neutral within the 1.2260 - 2370 range. The intraday outlook is neutral.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2370 | 1.2460 | 1.2260 | 1.2210 |

| 1.2460 | 1.2560 | 1.2210 | 1.2090 |

USD/JPY

Current level - 107.01

The overall bias remains negative below 107.20, but an eventual break through that area will challenge again 107.90 highs.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.20 | 108.30 | 106.40 | 105.40 |

| 107.90 | 110.40 | 105.40 | 102.40 |

GBP/USD

Current level - 1.3978

The dip below 1.4000 signals a reversal at 1.4060 and the bias is bearish below 1.4000, with a risk of further depreciation towards 1.3850. Trigger on the downside is 1.3950.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4060 | 1.4280 | 1.3950 | 1.3760 |

| 1.4150 | 1.4340 | 1.3850 | 1.3620 |

GBPUSD Remains In Bearish Correction, Next Support 1.38 Key Level

GBPUSD posted a red day on Monday, while after the sharp upward rally ended the day below its opening level. The price struggles within the 20 and 40 simple moving averages in the daily timeframe and the short-term technical indicators are bearish and point to more weakness in the market.

Looking at the daily timeframe, the Relative Strength Index (RSI) is moving in the positive territory near the 50 level but is flattening. Also, the MACD oscillator is falling below its trigger line, however, is still holding above the zero line.

If price continues the downside retracement and extends its losses, it could open the door for the 1.3800 strong psychological level, which overlaps with the 23.6% Fibonacci retracement level of the upleg from 1.2100 to 1.4345. If there is a fall below the latter level, there would be scope to test the next immediate support of 1.3660.

Conversely, if cable penetrates the 20-day SMA, it could then move towards the 1.4150 resistance level, taken from the peak on February 16. A break above the aforementioned obstacle could take the price towards the 1.4280 resistance barrier.

Dollar Falls Though Not By Much, All Eyes On Powell

Here are the latest developments in global markets:

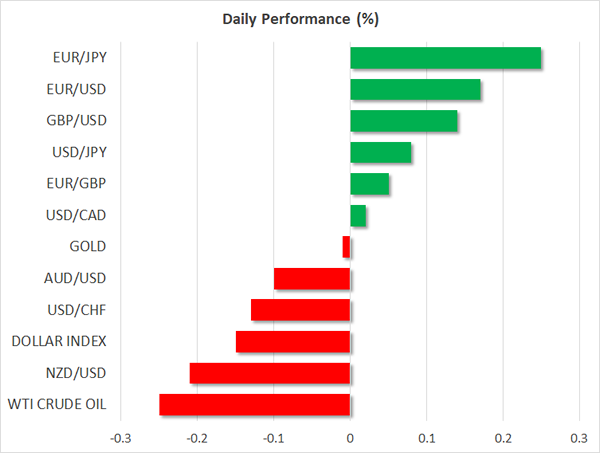

FOREX: The dollar index was down by around 0.15% as market attention was firmly on Fed chief Jerome Powell's testimony before Congress.

STOCKS: The Japanese Nikkei 225 and Topix indices rallied to finish the day higher by 1.1% and 0.9% respectively, pushing Japanese equities to their highest in three weeks. Hong Kong's Hang Seng, however, traded lower by 0.8%. At 0810 GMT, futures tracking the major European indices were broadly in the green, though not by much. Futures on the Dow, S&P 500 and Nasdaq 100 were all down by around 0.1%, after yesterday's strong equity performance in the US that saw the Dow, S&P 500 and Nasdaq Composite all rise by more than 1%.

COMMODITIES: WTI and Brent crude were down by 0.25% and 0.2%, at $63.77 and $67.39 per barrel respectively ahead of today's API weekly report on US crude inventories. Gold was not much changed at $1,334 per ounce.

Major movers: Dollar eases as markets remain cautious ahead of Powell's remarks; kiwi loses ground on trade numbers

Despite the dollar's decline, the relevant index that gauges the greenback against the currencies of six major US trading partners still stood at a distance to the three-year low of 88.25 that was recorded around mid-February.

Powell's testimony could determine the US currency's short-term direction. Market participants have at the moment priced in less that three quarter percentage point interest rate hikes that the latest Fed dot plot projected. It remains to be seen whether the new Fed chief's comments will incentivize market participants to revise those expectations. In his comments on Monday, Fed Governor Randal Quarles made it clear that a sustained period of higher growth might justify higher interest rates, but not at such a pace that would act to the detriment of economic activity.

Attention is also on Thursday's release of the core personal consumption expenditures (PCE) price index for January, this being the Fed's preferred inflation measure, while revised US Q4 2017 growth figures are due on Wednesday.

Dollar/yen was 0.1% higher at 107.00. This compares to the 15-month low 105.55 from February 16. Euro/dollar was up by 0.2% at 1.2340, ahead of key eurozone data releases as well as Sunday's Italian elections – the outcome of the German SPD's vote on whether to seal a coalition deal with Chancellor Merkel's conservatives will be known on the same day. Pound/dollar traded higher by 0.15% at 1.3984 in a week with increased Brexit-related interest that will culminate with a speech by UK PM Theresa May on Britain's future relationship with the EU on Friday.

The kiwi eased versus the greenback after the country recorded its biggest monthly trade deficit in more than a decade. Kiwi/dollar was down by 0.2% at 0.7289. Aussie/dollar also traded lower, though by only 0.1% at 0.7848.

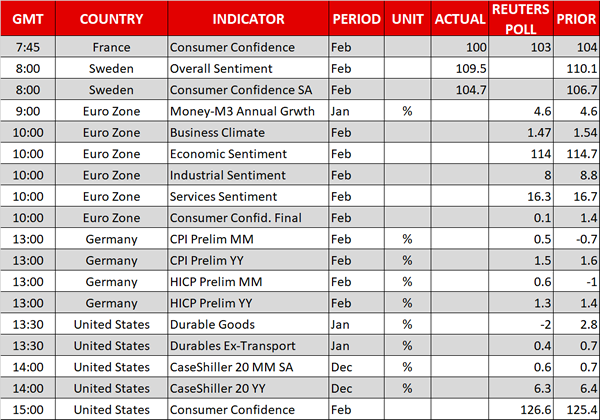

Day ahead: Powell's testimony the highlight, with eurozone business & consumer confidence surveys, German inflation, US durable goods & consumer confidence also on the agenda

The economic calendar has a number of releases that could spur positioning in the markets, however Jerome Powell's first congressional testimony is viewed as the event having the greatest capacity to lead to sharper movements, not just in currency markets, but also in fixed income and equity markets.

Of most interest out of the eurozone will be numerous surveys gauging business sentiment and consumer confidence during the month of February; all of them will be coming from the European Commission's Directorate-General for Economic and Financial Affairs and are due at 1000 GMT. Barring no exception, the surveys are anticipated to reflect a decline in February, mirroring the recent easing in the German ZEW and Ifo surveys, as well as the euro area's PMI readings.

German preliminary inflation figures for the month of February are scheduled for release at 1300 GMT. These come a day ahead of the eurozone's respective figures, which would constitute the last inflation input ahead of the ECB meeting on March 8 and thus the markets might assign a larger weight on them than would otherwise be the case.

Out of the US, durable goods orders for January are due at 1330 GMT, with a reduction in orders being projected relative to December. At 1400 GMT, the CaseShiller indices gauging house prices during the month of December will be made public, while data on consumer confidence for the month of February will be released at 1500 GMT. The consumer confidence index is expected to rise to 126.6, coming closer to November's 18-year high of 128.6.

However, the data might lose their spark on the face of Jerome Powell's first monetary policy testimony before Congress set to take place at 1500 GMT. The hearing comes at a sensitive time following increasing volatility in equity markets. Invariably, the new Fed chief aims at avoiding to say something that would unsettle markets, and it is likely that Powell would not deviate from this. His speech will be release earlier (at 1330 GMT). Another hearing in Congress featuring Powell is on the agenda on Thursday.

Swedish central bank First Deputy Governor Kerstin af Jocknick will be holding an opening speech at the exhibition titled “Sveriges Riksbank 350 years old – from banknote ban to negative interest rates” at 0900 GMT. Fellow Riksbank Deputy Governor Henry Ohlsson will be discussing the Swedish central bank's tasks and his view of Swedish and international economic developments at 1700 GMT.

Oil traders will be paying attention to the API's weekly data on crude stocks due at 2130 GMT.

In equities, corporations continue to release quarterly earnings reports, though the markets' focus is expected to be on what Powell has to say later on Tuesday.

Brexit developments are also gathering attention as UK PM Theresa May prepares to deliver a speech on the nation's relationship with the EU after Brexit later in the week. In politics, NAFTA negotiations, which have entered their seventh and final round, will also be attracting interest.

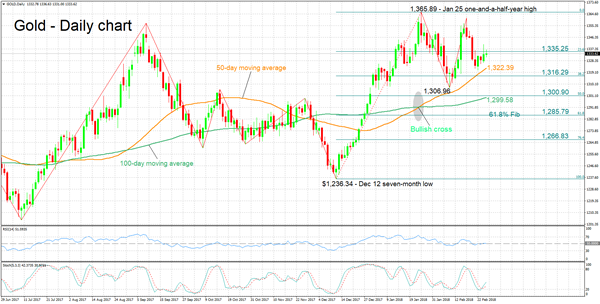

Technical Analysis: Gold looking neutral in short-term; bullish signal by stochastics in very short-term

Gold has to a significant extent been moving sideways over the last trading days, with the RSI hovering around the 50-neutral perceived level and projecting a neutral picture in the short-term. However, the stochastics are giving a bullish signal in the very short-term as the %K line has crossed above the slow %D one and both lines are heading higher.

A catalyst driving the US currency higher – for example a comment by new Fed chief J. Powell that is perceived as dollar-supportive by markets – is expected to lead to weakness in the dollar-denominated precious metal, with the area around the current level of the 50-day moving average at 1,322.39 potentially acting as support. This area also encapsulates the 38.2% Fibonacci retracement level of the December 12 to January 25 upleg at 1,316.29.

A weaker greenback on the other hand, could lend support to gold. In this scenario, resistance might come around the 23.6% Fibonacci point at 1,335.25. Price action is at the moment taking place not far below this level; stronger bullish movement would start to increasingly shift attention to late January's one-and-a-half-year high of 1,365.89.

Lastly, it should be mentioned that there are other risk events throughout the week that could keep the safe-haven perceived yellow metal elevated, even in the face of a stronger dollar; Brexit developments, Italian elections, the German SPD's decision on whether to re-enter a collation with Chancellor Merkel's conservative bloc.

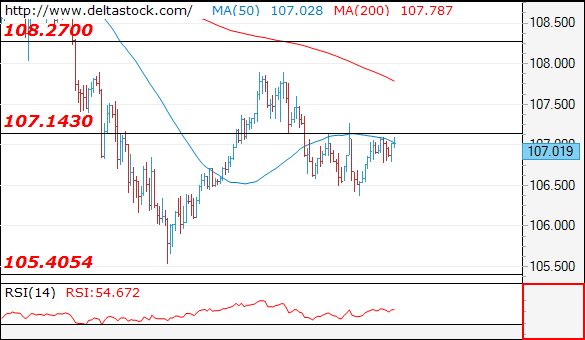

Technical Outlook: USDJPY – Fresh Attempts Higher Not Ruled Out While 10SMA Holds

The pair is trades within narrow range around 107 handle on Tuesday, awaiting Powell’s testimony for fresh signals.

Strong downside rejection on Monday (106.37) left long-tailed daily candle which suggests that fresh attempts above 107.00 cannot be ruled out.

Bullishly aligned near-term techs support the notion, but sustained break above 107.00 and regain of 107.31 (Fibo 61.8% of 107.90/106.37 downleg) is needed to confirm scenario and expose key barriers at 108 zone (21 Jan high / falling 20SMA).

Broken daily 10SMA (106.86) offers initial support and holds today’s action, keeping near-term bullish bias in play.

However, daily studies remain in firm bearish setup and maintain downside risk which could intensify on return and close below 10SMA.

Res: 107.19, 107.31, 107.54, 107.90

Sup: 106.86, 106.37, 106.10, 105.54

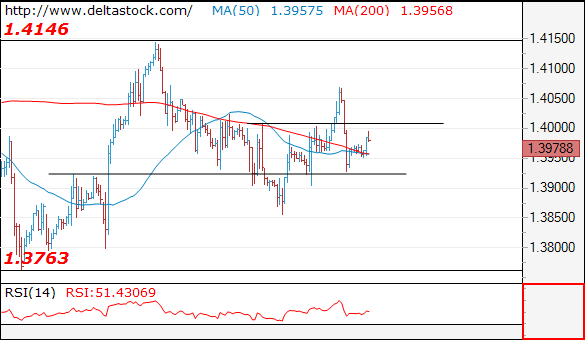

Technical Outlook: GBPUSD Holds In Tight Range Under 1.40 Barrier

Cable holds within tight range on Tuesday, capped at 1.40 barrier, following strong upside rejection at 1.4067 yesterday and close below 1.40, which left bearish daily candle with long upper shadow that weighs on today's action. Daily MA's are in neutral setup but momentum studies are positive, keep in play hopes for fresh attempts through 1.40 pivot (psychological barrier/50% of 1.4144/1.3856/daily Tenkan-sen) which repeatedly capped upside attempts in past few sessions. Firm break here would generate bullish signal for further retracement of 1.4144/1.3856 downleg, while repeated failure would keep the downside vulnerable. Return below Monday's low at 1.3928 would soften near-term structure and risk return to 1.3856 (low of 22 Feb). With no events from the UK scheduled today, focus will turn towards a number of data from the US and the speech of Fed Chairman Powell.

Res: 1.4000, 1.4034, 1.4067, 1.4100

Sup: 1.3952, 1.3928, 1.3904, 1.3856

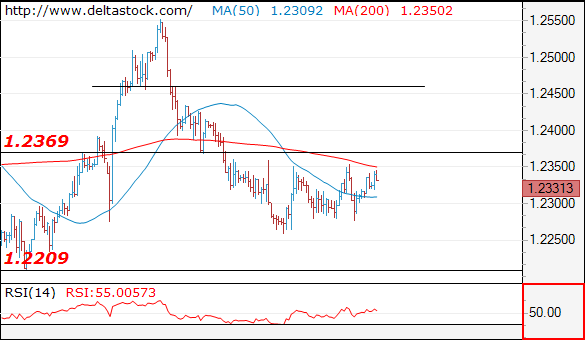

Technical Outlook: EURUSD Ticks Higher But Remains Within Range Ahead Of Powell’s Testimony

The Euro stands at the front foot in early European trading on Tuesday, as dollar eases ahead of key event today, the testimony of Fed Chairman Powell. Fresh strength pressures again the top of 1.2260/1.2360 congestion which extends into fifth day, following strong rejection at 1.2355 yesterday. The resistance is reinforced by 30SMA (currently at 1.2347) and converged 10/20SMA's (1.2359/67) with sustained break here needed to generate initial bullish signal. At the downside, range floor at 1.2260 marks initial support which guards pivots at 1.2205/1.2173 (09 Feb low / Fibo 38.2% of 1.1553/1.2555 ascend) loss of which will be bearish. Powell's speech today is highly anticipated as traders are looking for fresh signals about the pace of US monetary policy tightening, which could be boosted on more hawkish tone from Powell. On the other side, a number of market participants expect milder tone from Fed chief, who will be probably optimistic on the economic outlook, but would require more patience on inflation growth which moves with lower than expected pace towards central bank's projected level. Overall expectations see balanced view from Powell which wouldn't provide stronger direction signal for the dollar if that turns to be the case. Any stronger hawkish steer from Fed today would boost dollar and risk deeper pullback of EURUSD pair from recent double-top at 1.2537/55. Conversely, dovish stance would depress dollar and risk return to its new three-year low. The Euro also faces several releases of important economic indicators this week, along with political events, Italian election and decision of leading political parties in Germany about coalition deal which would help Angela Merkel to secure a fourth term as chancellor.

Res: 1.2346, 1.2360, 1.2372, 1.2407

Sup: 1.2308, 1.2277, 1.2260, 1.2205