Sample Category Title

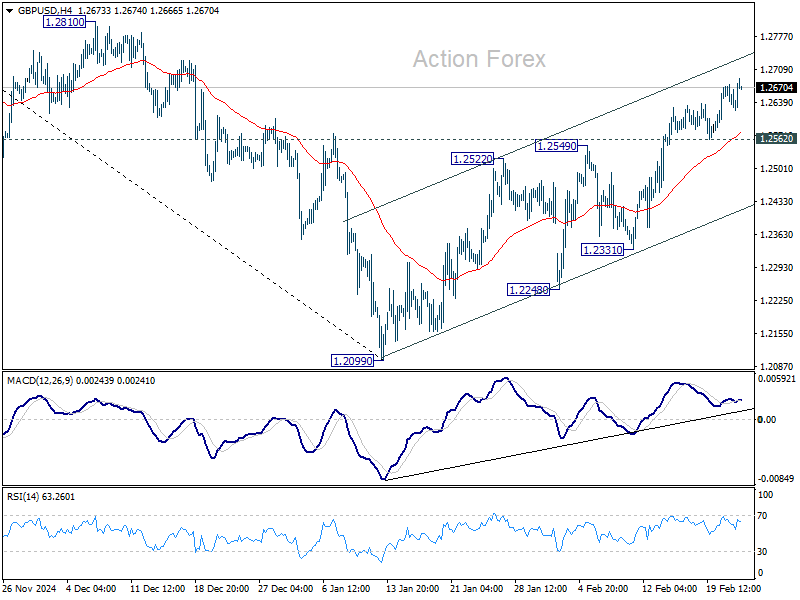

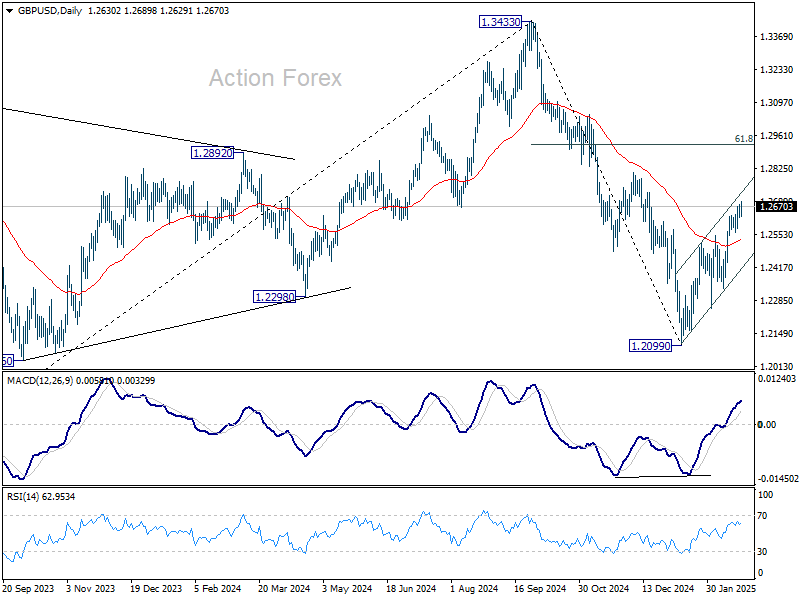

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2615; (P) 1.2647; (R1) 1.2669; More...

Intraday bias in GBP/USD remains on the upside as rise from 1.2099 is in progress. Further rally should be seen to 1.2810 resistance first. Firm break there will target 61.8% retracement of 1.3433 to 1.2099 at 1.2923 next. On the downside, below 1.2562 minor support will turn intraday bias neutral again first. But another rise will remain in favor as long as 1.2331 support holds, in case of retreat.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

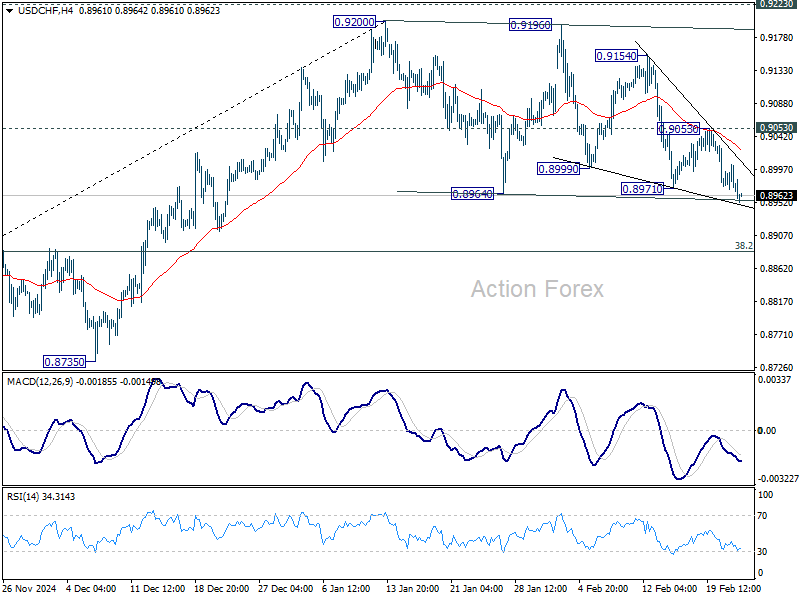

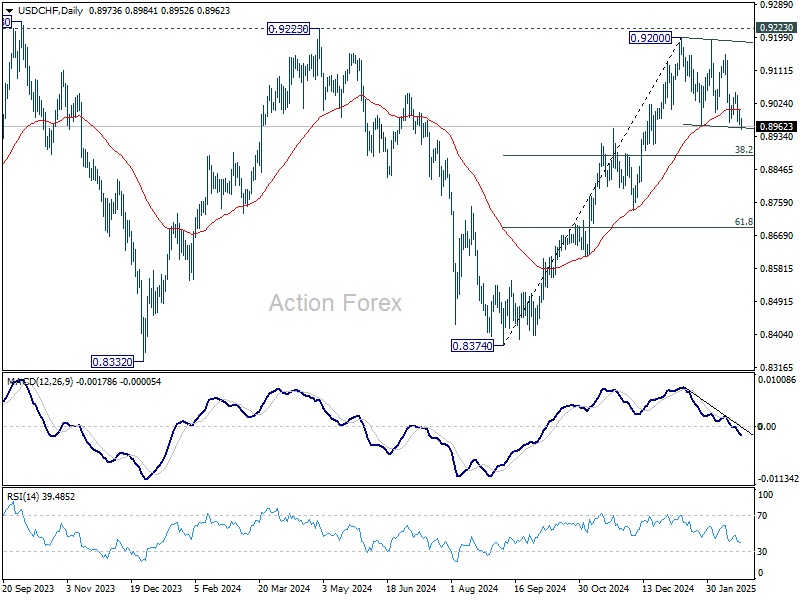

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8962; (P) 0.8984; (R1) 0.8999; More…

Intraday bias in USD/CHF remains neutral. Consolidation pattern from 0.9200 might extend with deeper decline. But larger rally is still expected to continue as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

German Election – A Positive Outcome for Markets and the Economy

The German election makes a two-party government between the conservative CDU/CSU and the Social Democrats (SPD) the most likely result (75%), which is a positive outcome for the German economy. Markets have also reacted positively to the news by strengthening the euro by 0.6% during Asian trading hours while DAX futures have climbed 1.1%. The conservative chancellor Friedrich Merz is certain to become the next chancellor as his party emerged as the biggest one with 28.6% of the votes. A majority government with the Social Democrats is possible because two parties fell below the 5% threshold for entering the parliament, namely the FDP at 4.33% and the BSW at 4.97%. This gives 328 seats to the CDU/CSU and SPD, above the 315 needed for a majority. A two-party "Grand coalition" government is a positive outcome because decision making is easier than in a three-party government. A new government will likely take office in two months' time.

The far-right Alternative for Germany (AfD) became the second largest party with 20.8% of the votes, which is double the votes it got in the last election but at the same time in line with election polls. Being the sole party who has certainly refused to change the constitutionally enriched "debt brake" to allow more debt we see the chance of a reform being 60%. Such a reform requires a two-thirds majority and the CDU/CSU, SPD, Greens, and The Left have 76% of the votes. The reform will depend on the CDU as they have given mixed signals, which is the reason we estimate 70% chance of it happening (see next page for details).

In terms of defence spending and support for Ukraine, the election outcome was not the best scenario because the far-right (Afd) and the Left party combined secured 34.3% of the votes. Therefore, they will be able to block off-budget defence funds and legislation that requires two-thirds majority. Yet, with a less fragmented Parliament and a two-party government Germany's presence in the EU will likely be stronger compared to the previous government, which is positive news.

Because the majority for a "Grand coalition" is so slim (13 seats) Merz might want to include the Green party in a coalition to not be pressured by SPD the members who are the least aligned with his policies, so it is 75% certain that we get a Grand coalition and 25% chance of a "Kenya" government. Since the BSW came so close to the 5% threshold there will likely be a recount of the votes to make sure the preliminary result is correct. We must wait for that before the results are 100% final.

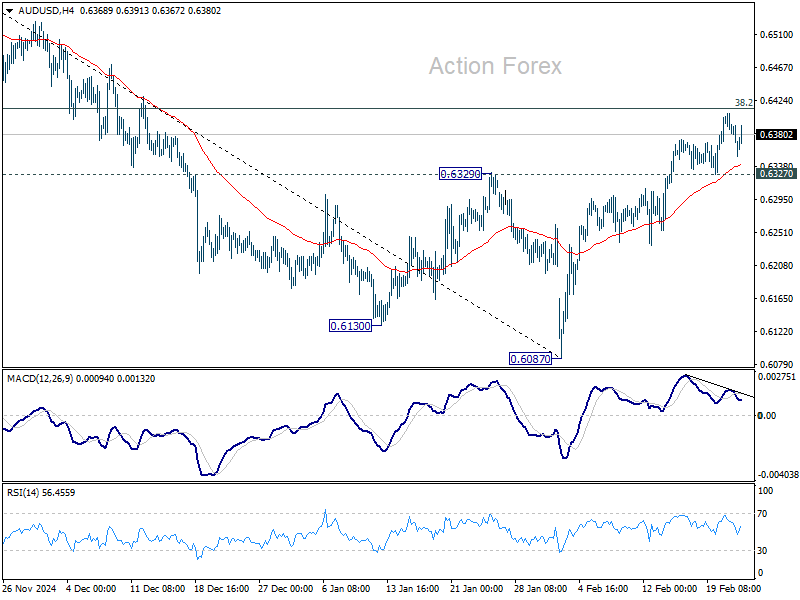

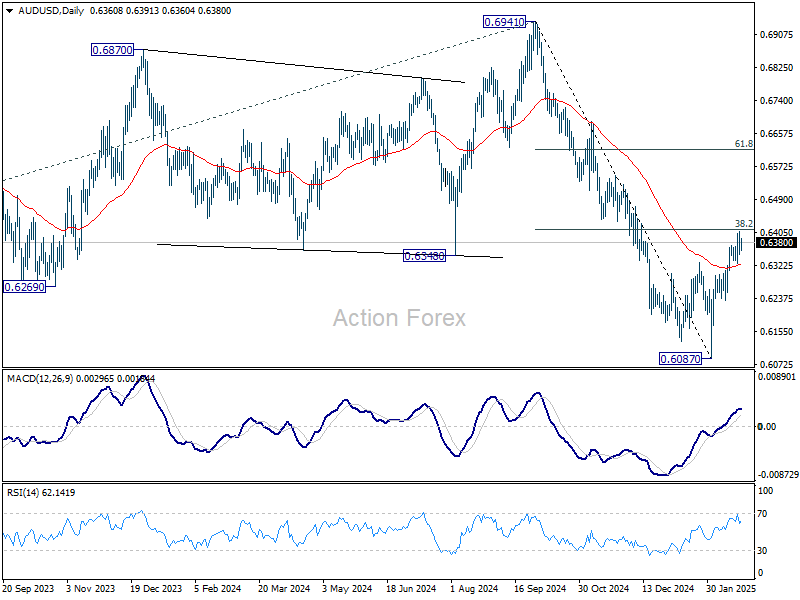

AUD/USD Daily Report

Daily Pivots: (S1) 0.6336; (P) 0.6373; (R1) 0.6393; More...

Intraday bias in AUD/USD stays neutral for the moment. On the downside, firm break of 0.6327 support will suggest that the corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Intraday bias will be turned back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413 will pave the way back to 61.8% retracement at 0.6615, even still as a correction.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6505) holds.

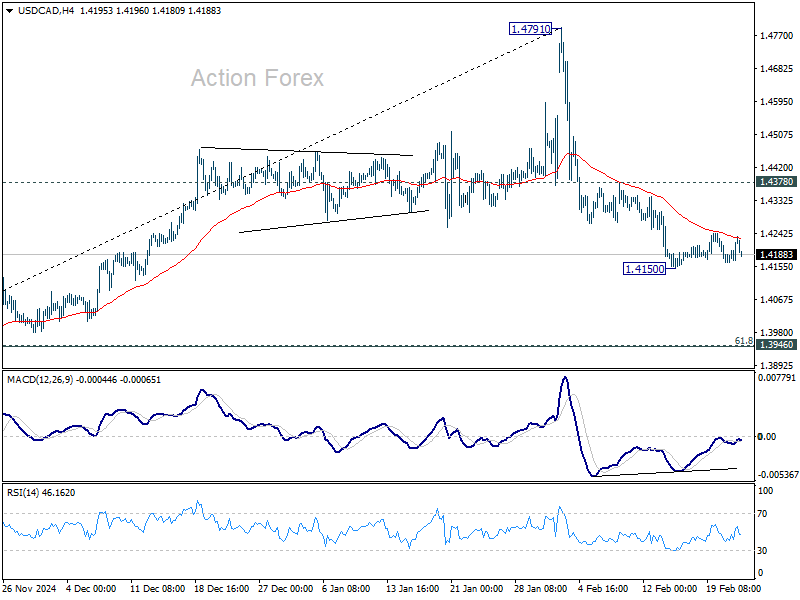

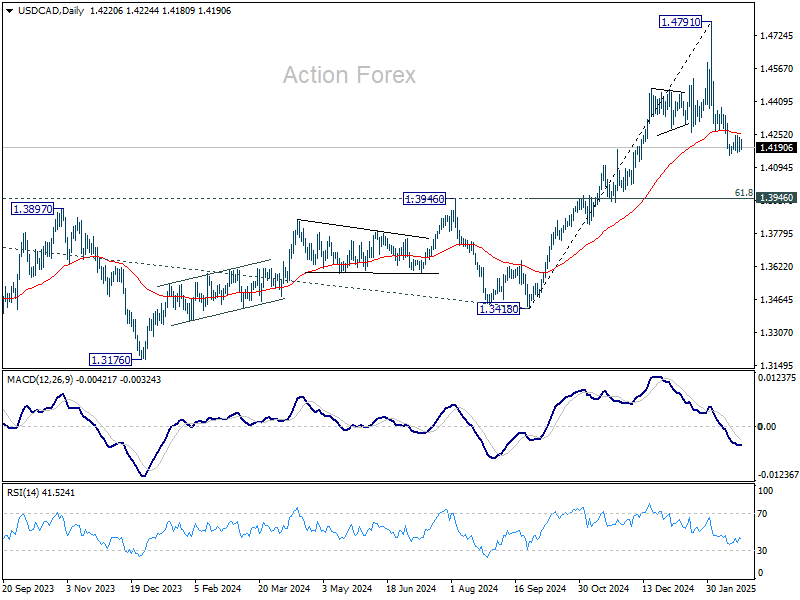

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4183; (P) 1.4210; (R1) 1.4251; More...

Intraday bias in USD/CAD remains neutral and more consolidations could be seen above 1.4150. Further decline is expected with 1.4378 resistance intact. Fall from 1.4791 is seen as a correction to rally from 1.3418. Break of 1.4150 will target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942).

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

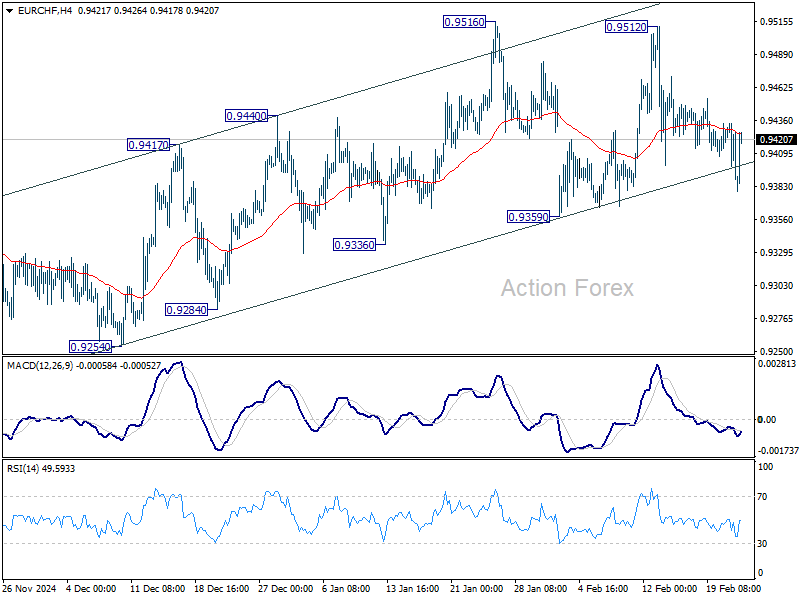

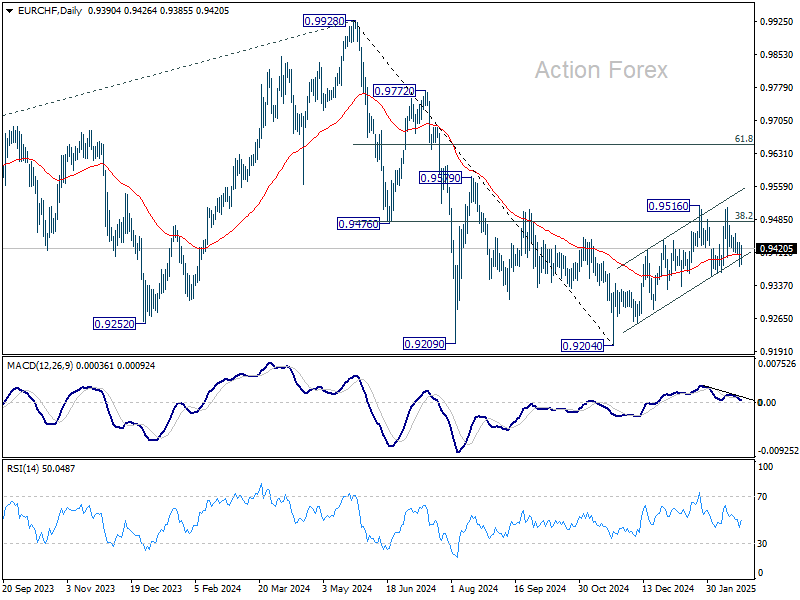

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9370; (P) 0.9403; (R1) 0.9425; More....

Intraday bias in EUR/CHF stays neutral as range trading continues. On the downside, firm break of 0.9359 will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

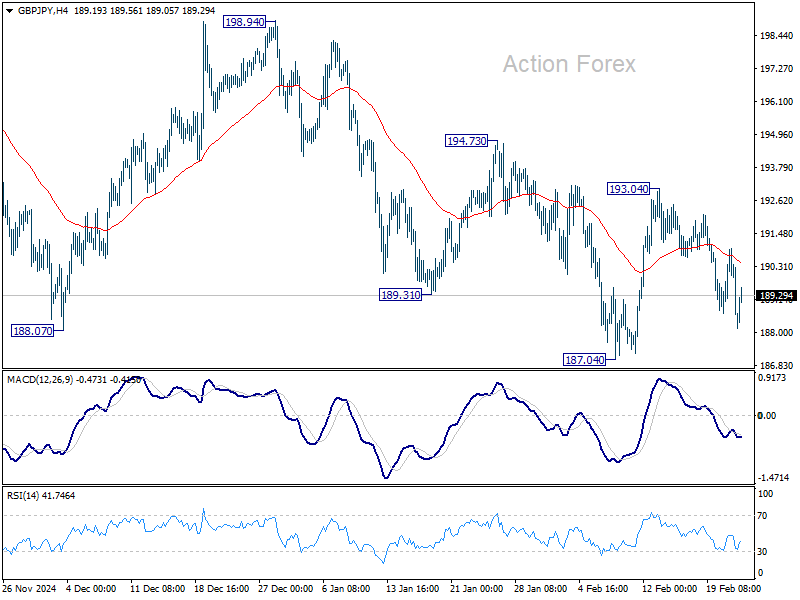

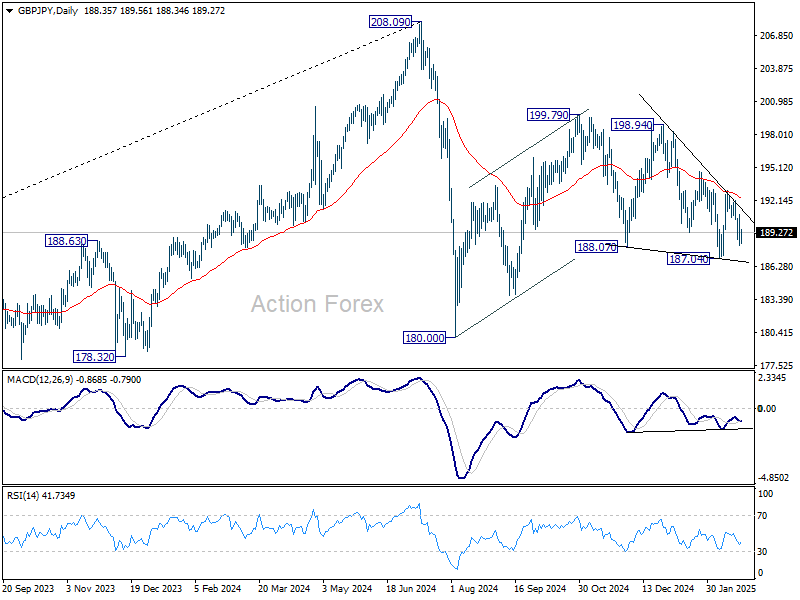

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.51; (P) 189.22; (R1) 190.30; More...

Intraday bias in GBP/JPY remains neutral for the moment. Risk will be mildly on the downside as long as 193.04 resistance holds. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

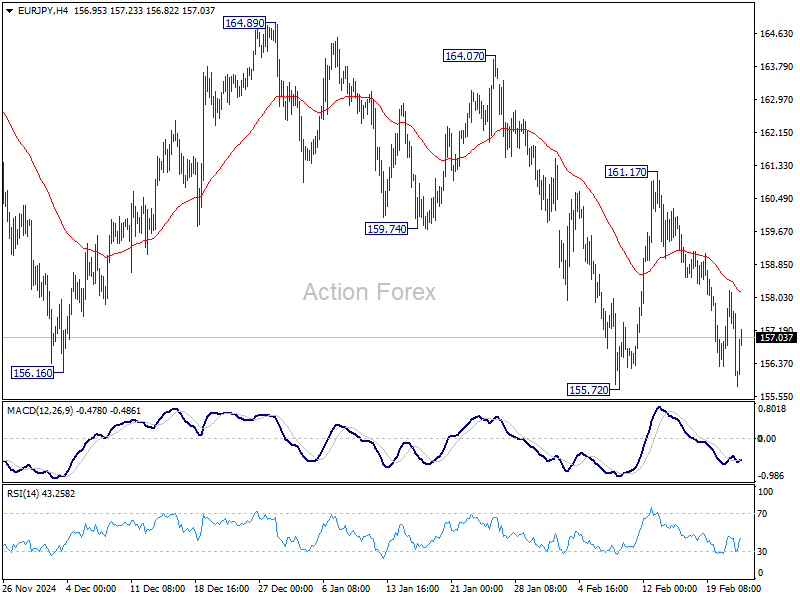

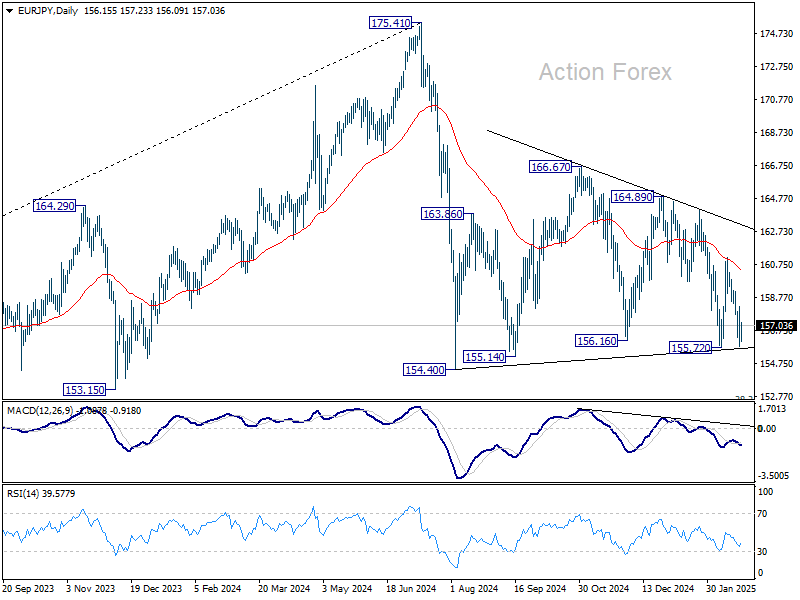

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.27; (P) 156.74; (R1) 157.67; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the downside, firm break of 155.72 will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

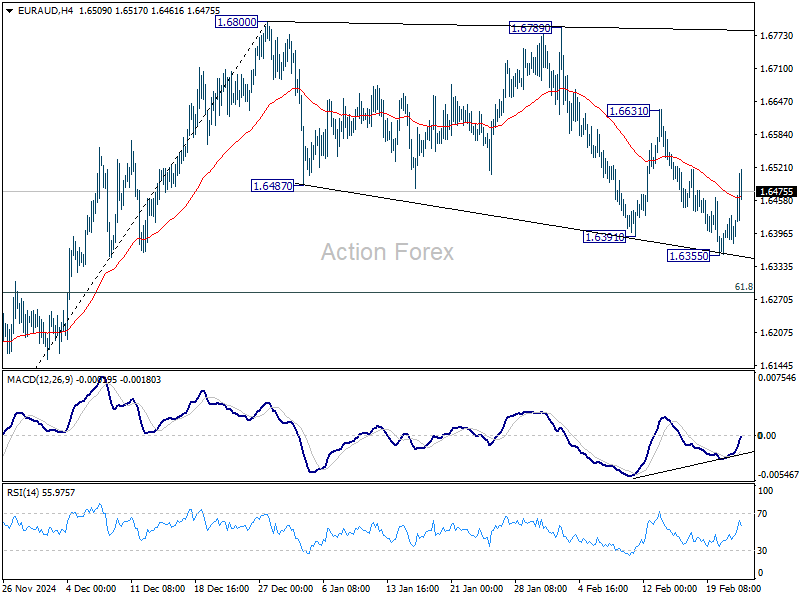

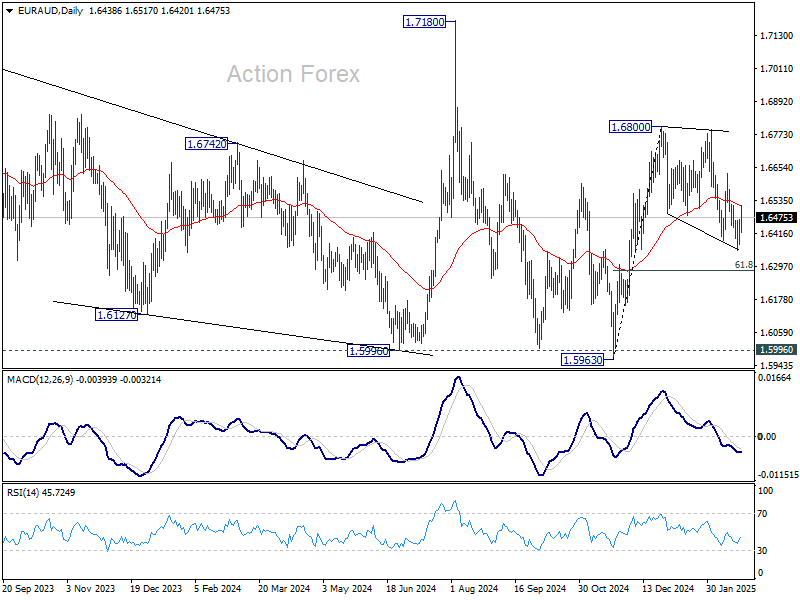

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6402; (P) 1.6436; (R1) 1.6492; More...

Intraday bias in EUR/AUD remains neutral for the moment. Corrective pattern from 1.6800 could still extend and break of 1.6355 will target 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, firm break of 1.6631 resistance will suggest that the correction has likely completed, and rise from 1.5963 is finally ready to resume.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

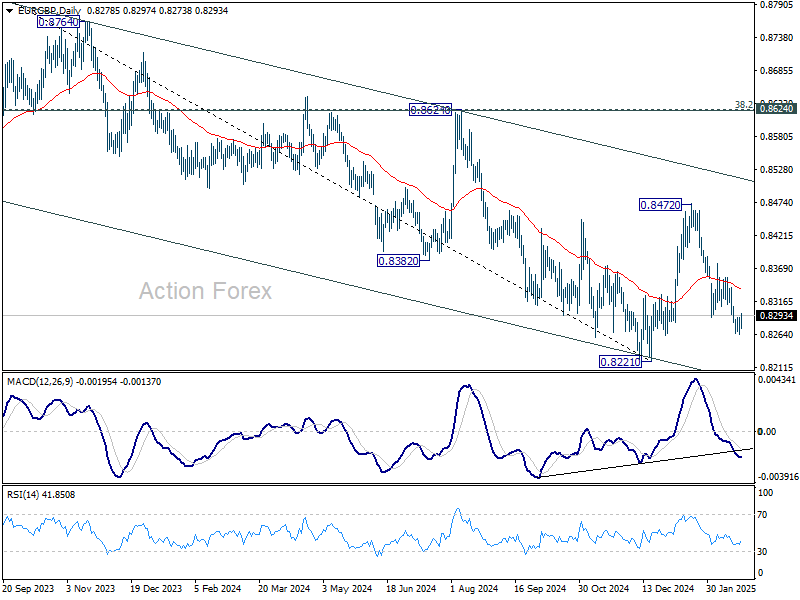

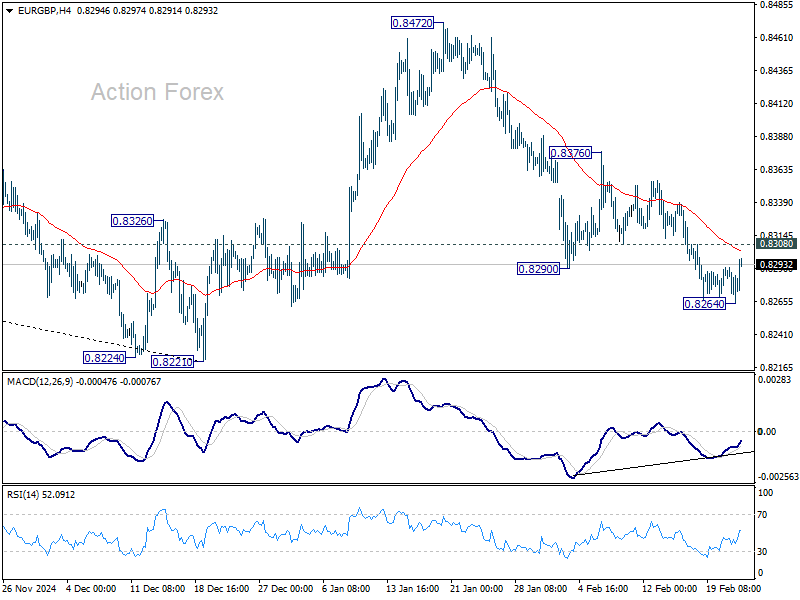

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8266; (P) 0.8279; (R1) 0.8293; More...

Intraday bias in EUR/GBP is turned neutral first with current recovery. Another fall is expected as long as 0.8308 minor resistance holds. Below 0.8264 will resume the whole decline from 0.8472 to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.