Sample Category Title

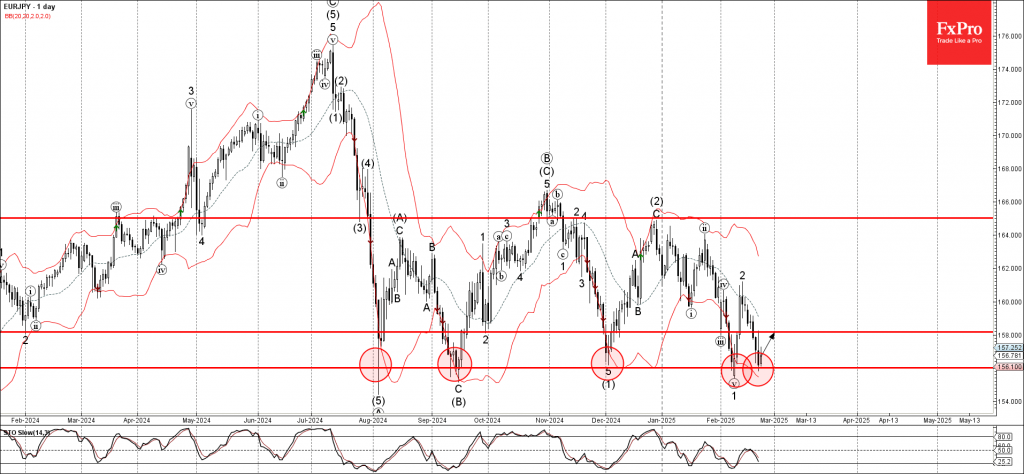

EURJPY Wave Analysis

- EURJPY reversed from the support zone

- Likely to rise to the resistance level 158.00

EURJPY currency pair recently reversed up from the support zone between the multi-month support level 156.00 (which has been reversing the pair from last August) and the lower daily Bollinger Band.

The upward reversal from this support zone is likely to form the daily Japanese candlesticks reversal pattern Piercing Line – if the pair closes today near the current levels.

Given the strength of the support level 156.00 and the bullish euro sentiment seen today, EURJPY currency pair can be expected to rise to the next resistance level 158.00.

Germany Moves to the Right, Euro Pares Gains

The euro rose as much as 0.55% on Monday but has pared most of these gains. In the North American session, EUR/USD is trading at 1.0467, up 0.11%.

Merz’s conservatives win German election

Germany has voted and Friedrich Merz is slated to become the next president. Merz’s conservatives came in first place, followed by the far-right AfD party. Merz’s first order of business will be the formation of coalition government, likely with the Social Democrats. The new government will need to improve the flagging economy and will have to contend with the Russia-Ukraine war on its doorstep and the new Trump administration which is giving Europe a cold shoulder.

German business climate remained unchanged in February at 85.2, shy of the market estimate of 85.8. Businesses indicated less optimism about current business conditions and confidence weakened among service providers, although manufacturers were less pessimistic.

There were no surprises from eurozone inflation for January, which came in at 2.5% y/y, unchanged from the initial estimate. This marked the highest rate since July 2024, largely driven by a sharp jump in energy costs. Monthly, core inflation fell 0.3%, in line with the market estimate and following a 0.4% gain in December. Core inflation gained 2.7%, confirming the initial estimate and ticking higher from the 2.4% gain in December. The core rate hasn’t moved in five straight months. Today’s inflation report indicates that inflationary risks remain which could complicate the ECB’s plans to reduce interest rates and kick-start the weak eurozone economy. The ECB meets next on March 6.

On Friday, US Services PMI for February disappointed and contracted to 49.7, down from 52.9 in January and below the market estimate of 53.0. This marked the lowest level since January 2023. The services sector, which has been the major driver of the US economy, showed strong growth until the end of 2024 and has weakened for two straight months. The Manufacturing PMI improved to 51.6, up from 51.2 and above the market estimate of 51.5.

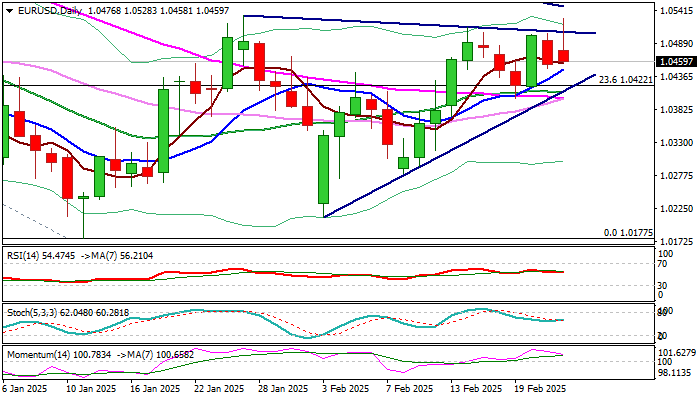

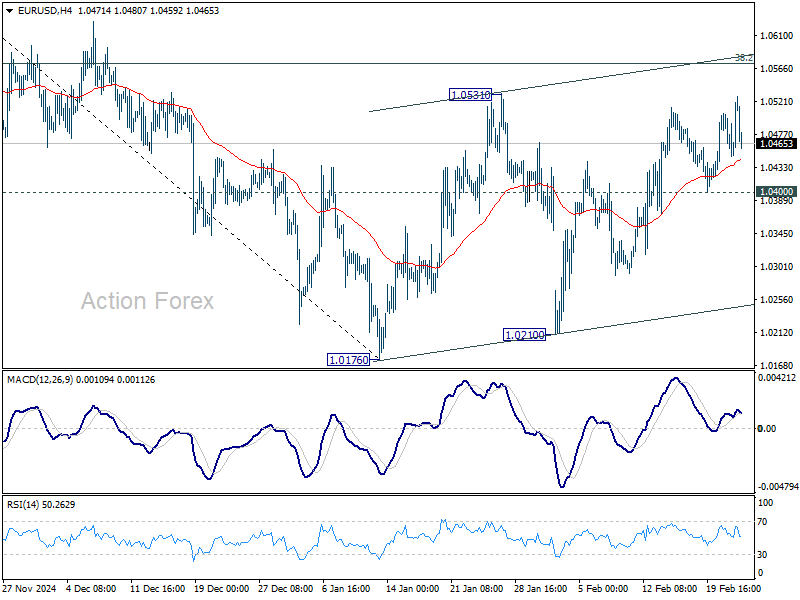

EUR/USD Technical

- EUR/USD tested resistance at 1.0474 and 1.0499 earlier.

- 1.0436 and 1.0411 are the next support lines

EUR/USD: Rejection Under Key Barriers Keeps the Downside Vulnerable

EURUSD hit one-month high (1.0528) in early Monday trading, in immediate reaction to German election results, but fresh gains were quickly reversed, mainly due to the lack of bigger election surprises.

Initial signs of recovery stall under significant barriers at 1.0533/73 zone (former top of Jan 27 / daily cloud top/100DMA/Fibo 38.2% of 1.1214/1.0177) would materialize if bulls repeatedly fail to clear this resistance zone and the price drops below 1.0400 pivot (Feb 19 trough/55DMA).

Conflicting daily indicators lack clearer direction signal, with little support from data showing that bloc’s inflation remains elevated, though near-term bias is expected to remain bullish while the price stays above rising 10DMA (1.0448).

Expect stronger signals on violation of either breakpoint (1.0400 at the downside and 1.0573 at the upside).

Res: 1.0506; 1.0528; 1.0547; 1.0573.

Sup: 1.0448; 1.0422; 1.0400; 1.0372.

Sunset Market Commentary

Markets

The German Parliamentary elections yesterday paved the way for Friedrich Merz of the winning CDU/CSU (28.6% of the votes) to take the initiative form a Grand Coalition with the Social Democrats of outgoing Chancellor Olaf Scholz even as the latter faced a sharp stack (16.4% of the votes, the worst outcome for the group in more than hundred years). In advance, this outcome was seen as the most market friendly with both traditional parties having the governing experience seen as the best combination to cope with economic and (geo)political challenges the country is facing. Even so, the reaction on European markets this morning/today was very guarded. Merz said the country needs an effective government as soon as possible. Still he suggested that this ‘as soon as possible’ probably still means two months of negotiations. Both parties are prepared to step up (targeted) fiscal spending. However, as the tree mainstream parties have no two third majority in Parliament, smaller parties including AfD, might complicate increasing spending on the likes of defense which needs a revision of the constitutional debt brake. While there might be ways to circumvent these debt brake issues, (FT suggests that current Parliament might already change the debt brake), the process might face a bumpy path. German yields opened the day even in slightly negative territory, but gradually the prospect for some fiscal stimulus further down the road triggered (admittedly) hesitant steeping of the German curve with yields changing between -1 bp (2-y) and +2.5 bps (30-y). The German DAX (+0.6%) outperforms the broader EMU indices (EuroStoxx 50 -0.5%). The euro in Asia trading looked like preparing an attack on the EUR/USD 1.0533 YTD top, but momentum already dwindled going into the start of European trading. At 1.047, the pair currently trades almost unchanged from Friday’s close. Whether it is related to the outcome of the German elections or to hope on a Ukraine ceasefire is unclear, but CEE currencies again outperform today.

US markets are looking for direction after a rather abrupt risk-off repositioning on Friday. This sell-off was partially triggered by disappointing US data (PMI’s). We look out whether uncertainty due to the Trump announcements/ policy at some point might become negative for the US economic exceptionalism narrative. The jury is still out. The Trump administration taking several measures against China including targeting investment in (strategic) US sectors and other trade-related measures, suggest that the trade war is at risk of further escalating rather than cooling down. US equities at the open show only a highly unconvincing rebound after Friday’s sell-off (Nasdaq +0.1% vs 2.20% decline on Friday). The rebound in US yields is also negligible after Friday’s decline of +/- 7.0 bps. Regarding the data later this week, in the US we look out for US consumer confidence (conf. board tomorrow) and the January PCE price deflators (Friday). At the end of this week EMU member states, including Spain, France and Germany will already publish preliminary February CPI data.

News & Views

The German Bundesbank in its monthly bulletin projected slight growth in the first quarter of this year following a 0.2% Q/Q decline in Q4 2024. Factors like high uncertainty, increased financing costs, and low capacity utilization still weigh on investments, but recent improvements in order intake could support demand. Exports might perform better, especially if there are anticipatory effects due to potential US tariffs. Private consumption and services are expected to continue supporting the economy. The German national bank also backed the case to raise the debt brake (which limits public deficits to 0.35% of GDP). "Binding fiscal rules make a very important contribution to ensuring solid state finances. In principle, however, it is entirely justifiable to adapt the debt brake's borrowing limit to changing conditions when the public debt ratio is low.".

The Belgian debt agency conducted its first regular OLO-auction of the year. They raised a combined €3.04bn by tapping OLO 102 (€0.71bn 2.7% Oct2029), OLO 73 (€1.28bn 3% Jun2034) and OLO 76 (€1.05bn 1.9% Jun2038). The auction bid cover was a good 2.39. Earlier this year, the BDA raised €7bn via a new 10-yr syndicated deal (OLO 103 3.1% Jun2035). Two more syndications, one with a 5-yr tenor and one with a longer-dated one (long 20y, 2046? long 25y, 2051?) are expected later this year. With regards to 2025 funding, the debt agency plans to issue €42bn of OLO’s to cover the lion’s share of the €44.65bn gross borrowing requirement.

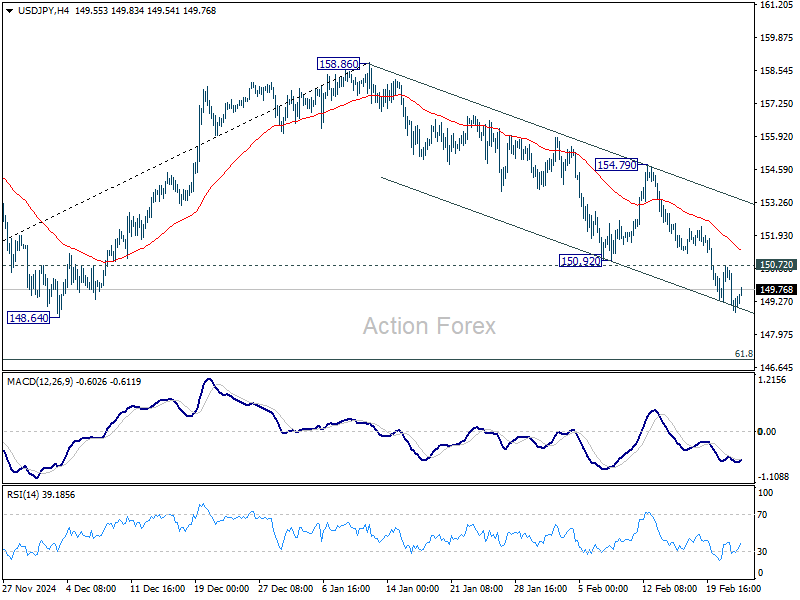

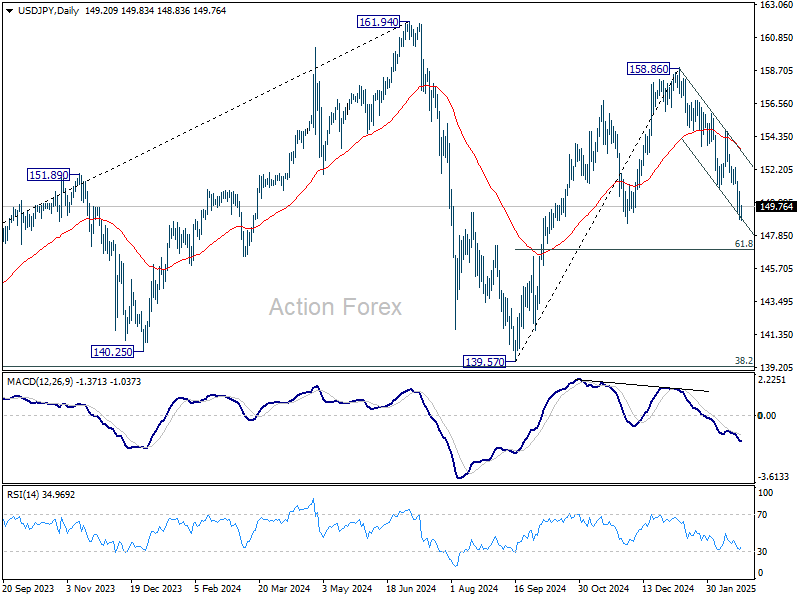

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.55; (P) 149.65; (R1) 150.37; More...

Intraday bias in USD/JPY stays on the downside with 150.72 minor resistance intact. Fall from 158.85 is seen as the third leg of the pattern from 161.94 high. Deeper decline should be seen to 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, above 150.72 resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

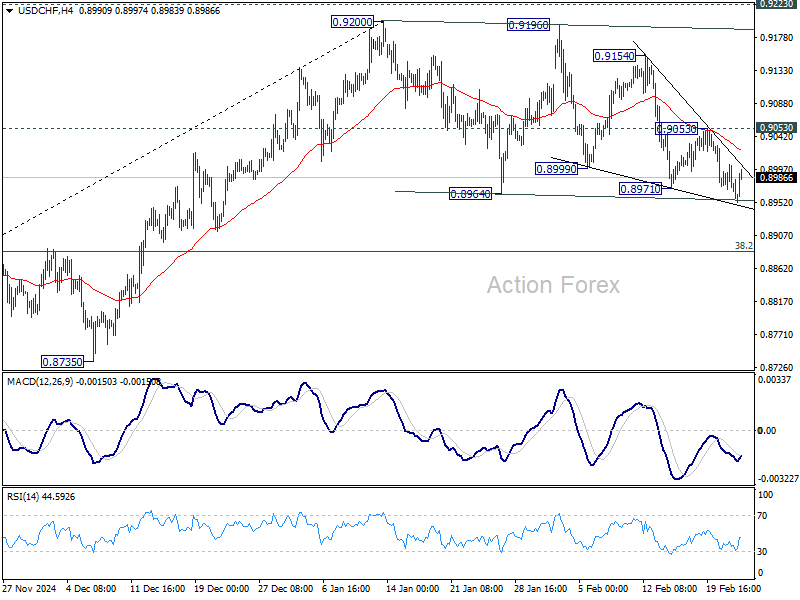

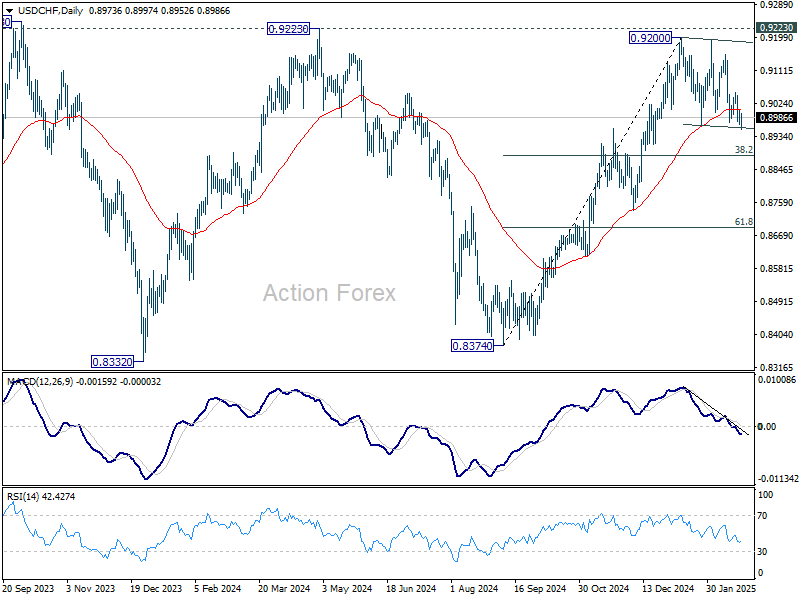

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8962; (P) 0.8984; (R1) 0.8999; More…

Intraday bias in USD/CHF stays neutral and outlook is unchanged. Consolidation pattern from 0.9200 might extend with deeper decline. But larger rally is still expected to continue as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, above 0.9053 will bring retest of 0.9200 resistance. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

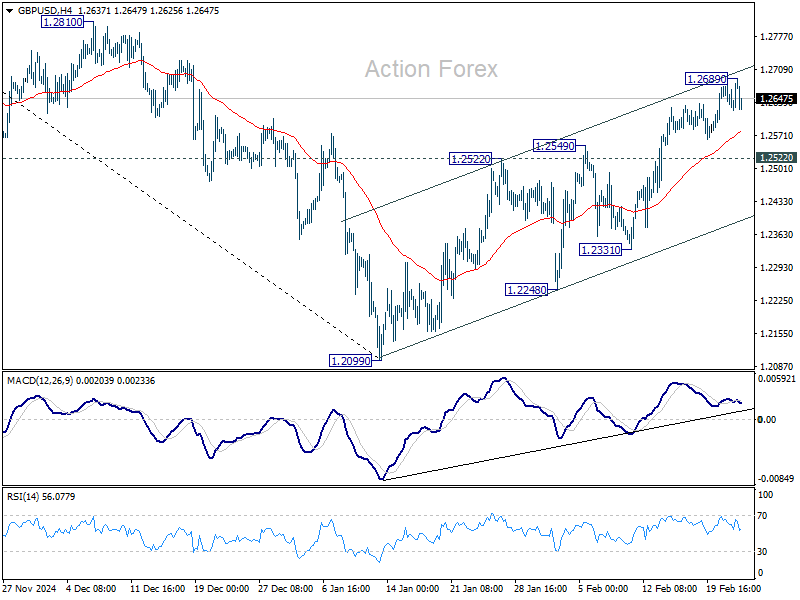

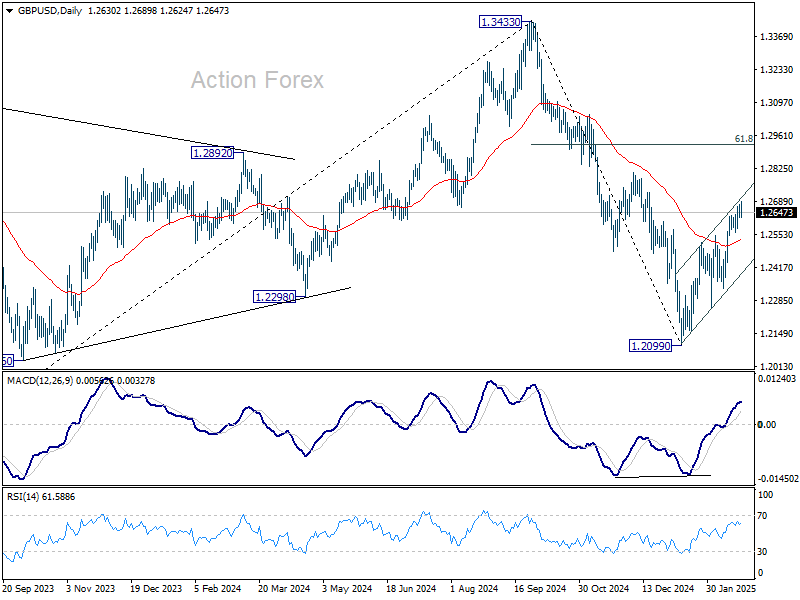

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2615; (P) 1.2647; (R1) 1.2669; More...

Intraday bias in GBP/USD is turned neutral with current retreat. But further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0436; (P) 1.0474; (R1) 1.0499; More...

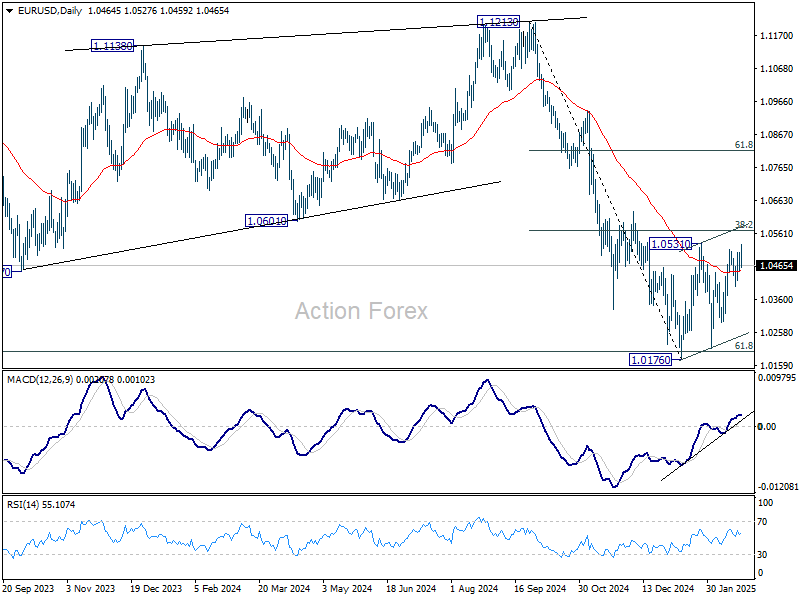

EUR/USD's rally attempt today quickly lost momentum and intraday bias stays neutral. Outlook is unchanged that price actions from 1.0176 are forming a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Euro Fades After Brief German Election Boost

Euro’s brief post-election rally faded quickly, as investors welcomed CDU/CSU’s victory but remained cautious due to lingering uncertainties around coalition formation and fiscal policy. While a relatively centrist government comprising CDU and the Social Democrats would provide stability, challenges surrounding the "debt brake" reform and defense spending continue to cloud the outlook.

A coalition with the Greens and Social Democrats would likely be the most market-friendly outcome. However, even with these three parties combined, they fall short of the two-thirds parliamentary majority needed to reform the "debt brake", which limits Germany’s structural budget deficit to 0.35% of GDP. Meanwhile, far-right AfD remains excluded from coalition talks, as Friedrich Merz has ruled out working with them.

This situation presents a fiscal dilemma for Germany, particularly given geopolitical uncertainties. The government faces pressure to increase both defense spending and broader fiscal stimulus, but policy divisions persist. The Left Party favors loosening the debt brake, but only for social and economic spending, not for increased defense expenditure. These divisions could complicate budget negotiations and delay much-needed investment decisions.

Bundesbank weighed in on the debate today, backing an increase in the government's deficit cap, citing the need for higher public investment while Germany’s debt ratio remains low. In its monthly report, the Bundesbank argued that adapting the debt brake's borrowing limit to current economic conditions is justified, but also stressed the importance of reviewing fiscal priorities and ensuring efficient use of financial resources.

In the currency markets, trading remains subdued, with major pairs and crosses confined within Friday’s ranges. Canadian, Australian, and New Zealand dollars are the strongest performers, while Yen is the weakest, followed by Swiss Franc and British Pound. Euro and Dollar are mixed in the middle.

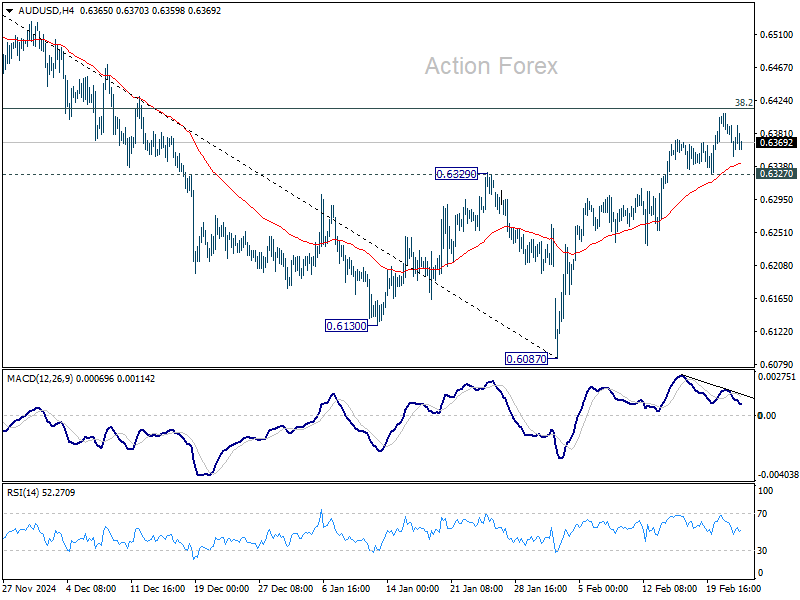

Technically, a major focus is whether the risk market selloff last week would extend today, and its impact in the forex markets. As for AUD/USD, firm break of 0.6327 support will suggest that corrective rebound from 0.6087 has completed ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Deeper decline would then be seen back to retest 0.6087, with prospects of resuming the whole fall from 0.6941.

In Europe, at the time of writing, FTSE is down -0.01%/ DAX is up 0.85%. CAC is down -0.22%. UK 10-year yield is up 0.0207 at 4.597. Germany 10-year yield is up 0.020 at 2.493. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -0.58%. China Shanghai SSE fell -0.18%. Singapore Strait Times fell -0.06%.

Eurozone CPI finalized at 2.5% in Jan, core CPI holds at 2.7%

Eurozone headline inflation was finalized at 2.5% yoy in January, ticking up from 2.4% yoy in December. Core CPI, which excludes energy, food, alcohol, and tobacco, remained unchanged at 2.7% yoy.

The largest contributor to Eurozone inflation was the services sector, which added 1.77 percentage points (pp) to the overall rate. Food, alcohol, and tobacco contributed 0.45 pp, while energy added 0.18 pp, and non-energy industrial goods accounted for 0.12 pp.

At the EU level, CPI was finalized at 2.8% yoy. The lowest inflation rates were seen in Denmark (1.4%), Ireland, Italy, and Finland (all 1.7%), indicating softer price pressures in some core economies. On the other hand, Hungary (5.7%), Romania (5.3%), and Croatia (5.0%) recorded the highest inflation levels, underlining regional imbalances in price stability.

Compared to December, inflation fell in eight EU member states, remained unchanged in four, and rose in fifteen.

German Ifo unchanged at 85.2, businesses waiting to see how things develop

Germany’s Ifo Business Climate Index was unchanged at 85.2 in February, falling short of expectations for a rise to 85.8. The data reflects that businesses are still "skeptical" about the outlook, "waiting to see how things develop", according to the Ifo Institute.

Current Assessment Index dropped from 86.0 to 85.0, missing the forecasted 86.5. However, Expectations Index showed slight improvement, rising from 84.3 to 85.4, exceeding the consensus of 85.2.

Sector-wise, the manufacturing index improved from -24.8 to -22.1, and trade sentiment rebounded from -29.5 to -26.2. The construction sector also saw a marginal improvement, rising from -28.1 to -27.6. However, services weakened, falling from -2.2 to -4.3.

New Zealand retail sales rises 0.9% qoq in Q4, ex-auto sales jumps 1.4% qoq

New Zealand's Q4 retail sales volume rose 0.9% qoq to NZD 25B, surpassing expectations of 0.6% qoq. Excluding autos, sales jumped 1.4% qoq, well above the 0.3% qoq forecast.

Sales volume growth was broad-based, with 10 of 15 industries posting gains. The largest increases came from electrical and electronic goods (+5.1%), department stores (+4.2%), and accommodation (+7.6%). Meanwhile, food and beverage services rose 2.3%, but pharmaceutical and other retailing declined -3.4%.

Retail sales value climbed 1.4% qoq to NZD 30B, with 11 of 15 sectors reporting gains. Price effects were evident, particularly in accommodation (+11%), food and beverage services (+3.3%), and department stores (+2.9%).

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0436; (P) 1.0474; (R1) 1.0499; More...

EUR/USD's rally attempt today quickly lost momentum and intraday bias stays neutral. Outlook is unchanged that price actions from 1.0176 are forming a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.