Sample Category Title

Changing Investment Landscape

The European stocks started the week near flat, while German companies gave back early gains, boosted by the idea – hope – that the new German government will relax spending rules and announce a special defence spending budget that could go up to 200bn euros to take its own security in its own hands for the first time since the WWII. The military spending in Europe is becoming a major investment theme – unfortunately – and should also be complemented with massive spending in technology and industry. As such, BAE systems gained nearly 4% yesterday, the German Rheinmetall jumped more than 6.40% (and has doubled in value since the election). Overall, the defence themed funds are amassing an increasing amount of funds since the war in Ukraine started and inflows are seen accelerating as European countries face limited options to rebuild their militaries.

But

Every penny spent on defence is one less penny spent elsewhere, and the latter could accelerate rotation toward the European equities. We agree that the US technology stocks – and their products – are much more exciting than military output. But even there, things are getting pretty political. Apple’s Tim Cook announced yesterday to spend as much as half a billion USD domestically over the next four years and hire 20’000 workers in the US to produce AI servers. Apple eked out a meager 0.63% - in quite a bearish session for the rest of the market – BUT geopolitically-backed investment motives could destroy investor value in the medium to long run.

Zooming out, the major US indices traded in the red on Monday, and selloff accelerated into the session end. The S&P500 slipped below the 50-DMA and closed below the 6000 mark. Nasdaq 100 also cleared its own 50-DMA. Microsoft fell more than 1% on news that they cancel some leases for US data center capacity raising concerns that the company could be in an oversupply position – and overestimated demand previously. That obviously casts a terrible doubt in AI investors’ minds given that the past two years’ rally is mostly based on the expectation that the demand will explode, and the companies would rather struggle with limited capacity rather than overcapacity. As such, Nvidia took a 3% hit yesterday. The company will report its Q4 earnings tomorrow.

Inside China

As the US tech companies announce plans to invest in the US to please Trump, Chinese equivalents do the same. Alibaba announced that it would spend more than $50bn in AI infrastructure in the next three years. The shares dropped 10% in New York yesterday. Yet dips could be interesting opportunities to strengthen long positions in Chinese technology giants. Alibaba’s cloud service will certainly benefit from the latest developments, while Cambricon Technologies – the leading AI chip designer in China – continues to push higher. The stock is up by more than 280% since September. By judging on how Nvidia performed over the past two years, the rally could develop further. Zooming out, the CSI 300 index recovered a part of early losses on news that Donald Trump told a government committee to crack down on Chinese investment in US tech, energy, and other critical sectors and is pushing Mexico to slap tariffs on Chinese imports too after Chinese firms have shifted production there to dodge the very duties Trump put in place during his first term.

Overall

The worsening geopolitical and trade outlook boost appetite for safer pockets of the market. The US 10-year yield pushed below the 4.40% mark, gold advanced to a fresh record high while the US dollar rebounded from the lowest levels since December. The EURUSD returned below the 1.05, while Cable failed to clear offers near1.2650, that matches the 100-DMA and the major 38.2% Fibonacci retracement. In the actual geopolitical setup, gold is certainly a better hedge than the US dollar and Treasuries.

Speaking of geopolitics, US crude extends rebound after approaching the critical $70pb support last Friday on news that Trump government imposed new sanctions on oil brokers and ships that were linked to illicit Iranian crude. But the worsening global economic outlook on rising trade tensions will likely keep the upside limited.

Tier-Two Releases and Politics in Focus

In focus today

From the US, Conference Board's February consumer confidence survey is due for release. The Fed's Logan and Barkin will also be on the wires today.

Today, we receive the ECB's negotiated wages indicator for Q4 2024. We expect that negotiated wage growth declined to 5.0% in the fourth quarter based on country data and more timely wage indicators. It is important to be cautious when interpretating the negotiated wages indicator as it can be very volatile, which the past quarters have shown with wage growth at 5.4% y/y in Q3 up from 3.5% y/y in Q2 due to the timing of one-off inflation compensation payment.

In Hungary the central bank will announce its policy rate. We and markets expect an unchanged decision, keeping the policy rate at 6.5%.

Economic and market news

What happened overnight

In China, the 1y Medium Lending Facility rate was left unchanged at 2.0%. This is in line with our expectations, as we believe PBOC remain sidelined awaiting new signals from the Fed and on tariffs before deciding on the next move.

What happened yesterday

In the US, President Trump pressed the tariff "on" button again, stating that the planned tariffs on Canada and Mexico are "going forward on time, on schedule" - although he did not specifically mention the 4 March deadline. A US official also stated that the reciprocal levies which may hit all countries will take effect in April. The headlines saw the USD ticking higher against CAD and MXN.

In the euro area, the final inflation data for January confirmed the flash release with headline inflation at 2.5% y/y and core inflation at 2.7% y/y. Details revealed that mainly energy prices drove the uptick in inflation. At the same time, some one-off factors were also visible in prices adjusted in January, mainly due to previous inflation, and thus are not indicators of future price pressures.

All in all, the details of the final release confirm that underlying inflation continues a cooling trend, while the rise in headline inflation was mainly due to energy prices and some one-off effects on core services in January.

In Germany, the Ifo indicator was lower than expected in February, staying put at 85.2 (cons: 85.8) - in contrast to the uptick recorded in the PMIs. The subcomponents showed an increase in expectations and a decline in the assessment of the current economic situation. Hence, the German economy continues to be stuck in the mud.

Turning to politics, the German election winner Friedrich Merz opened the door to loosening Germany's "debt brake" - the rule capping the federal government's net borrowing at 0.35% of GDP - before the new parliament is established to allow for more defence spending. Merz has roughly a 30-day window to push this through before the new parliament is settled, where AfD and Die Linke's securing more than a third of the seats gives them the power to block any constitutional changes to the debt brake.

On the geopolitical stage, the UN General Assembly backed an EU-Ukraine resolution condemning Russia's invasion, with 93 countries in favour and 18, including the US and Russia, opposed. The US proposed a rival resolution avoiding mention of Russian aggression, reflecting Trump's policy shift toward engagement with Putin. According to the AP, Trump also stated that he is in "serious" talks with Putin about ending the war -though Putin said they have not discussed resolving the war in detail, while Moscow has not ruled out European participation in any peace talks. U.S. diplomats attempted to block the EU-Ukraine resolution, emphasizing a vague commitment to peace instead.

Also, French President Macron was at the White House yesterday, meeting with Trump. Per Fox News, Macron said that a potential ceasefire between Ukraine and Russia could be negotiated within the coming weeks.

Equities: Despite the promising start, markets were unable to rebound Monday. Equities were mostly lower (MSCI World -0.5%) driven by the US while Europe were unchanged. The rotation into defensive stocks continued, with health care, real estate and banks in the lead, while investors took home profits in tech and industrials. Despite the thin news flow, VIX continued higher, just south of 20, so sentiment has evidently turned sour among US investors. Asian markets broadly lower this morning and US futures just north of zero.

FI: Another trading session with limited volatility. 10y Bunds traded in a narrow 4bp range, as they digested the German election result. The result was close to indications suggested thus leading to the limited market impact. Last night, discussion on a potential EUR200bn defence spending package led by Merz and supported by SPD was mentioned. This is likely to weigh on ASW spreads this morning.

FX: The USD and JPY was on the losing end on a relatively calm day in FX markets yesterday. The EUR ended the day higher as the market was relieved by the results of the German election, which did not bring about any big surprises.

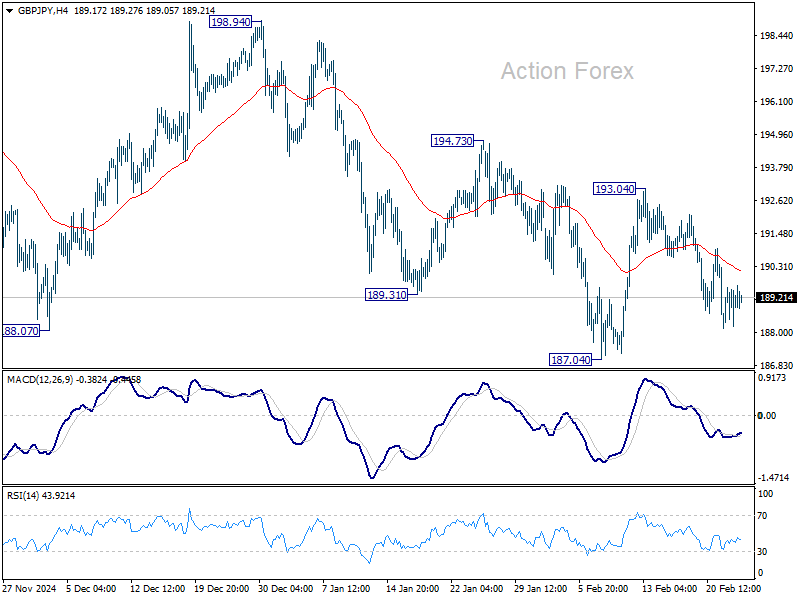

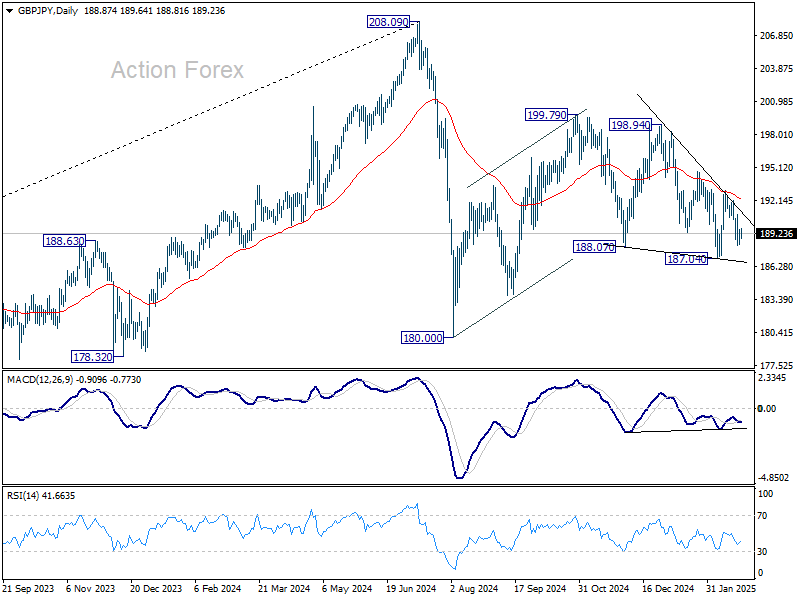

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.29; (P) 188.95; (R1) 189.66; More...

Intraday bias in GBP/JPY stays neutral at this point. Risk will be mildly on the downside as long as 193.04 resistance holds. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

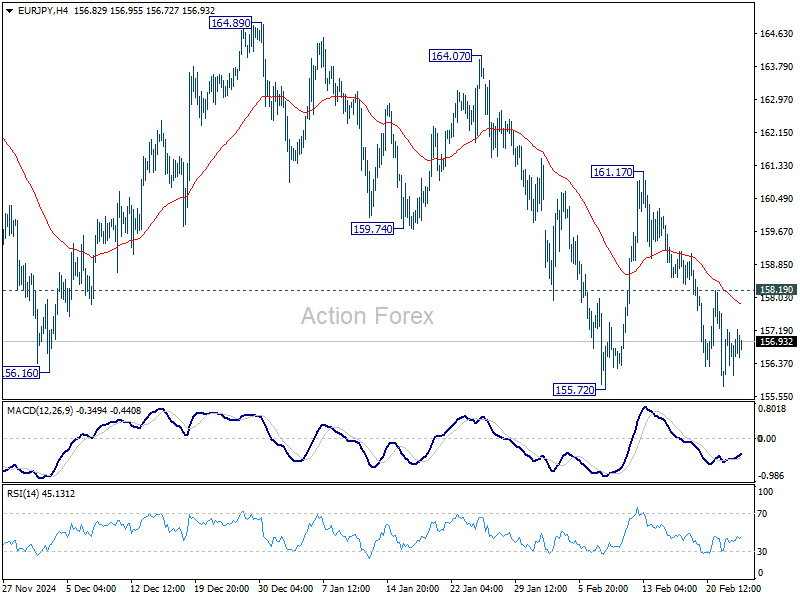

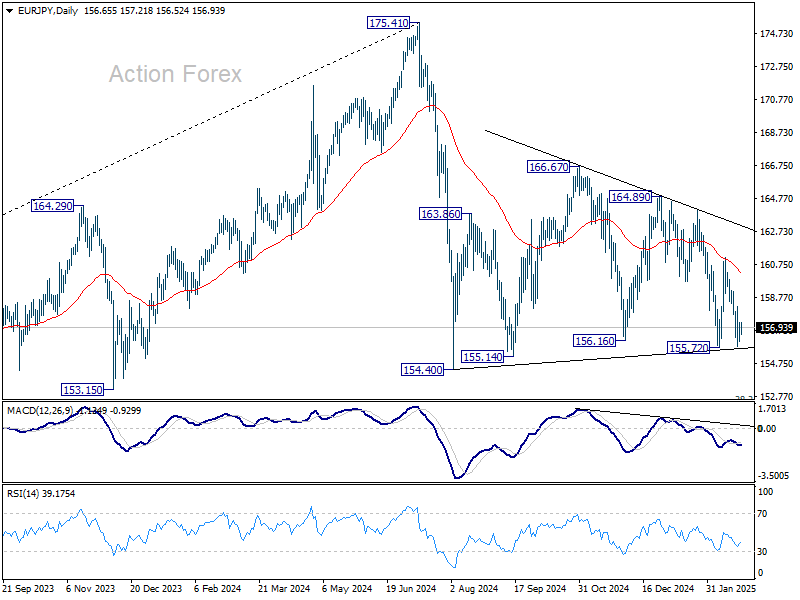

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.12; (P) 156.69; (R1) 157.29; More...

Intraday bias in EUR/JPY remains neutral for the moment. the downside, firm break of 155.72 will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm. However, break of 158.19 resistance will turn bias back to the upside and extend the corrective pattern from 154.40 with another rising leg.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

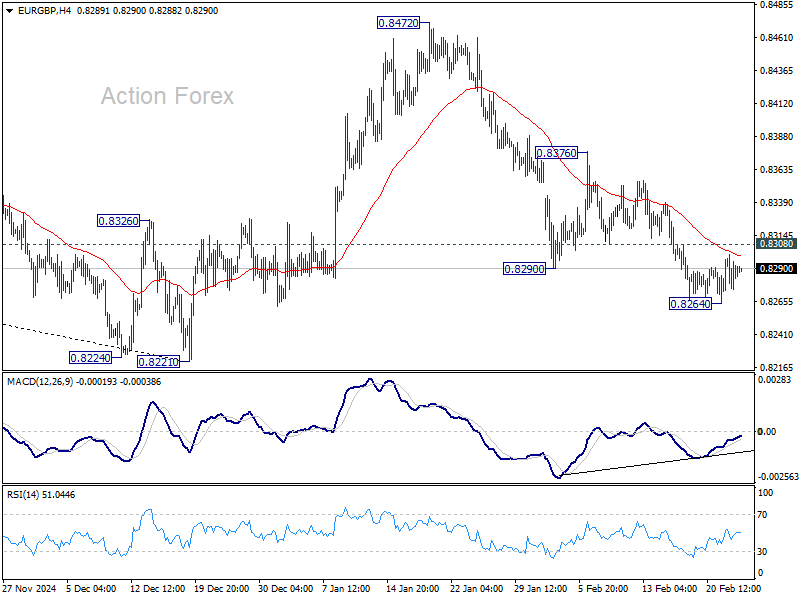

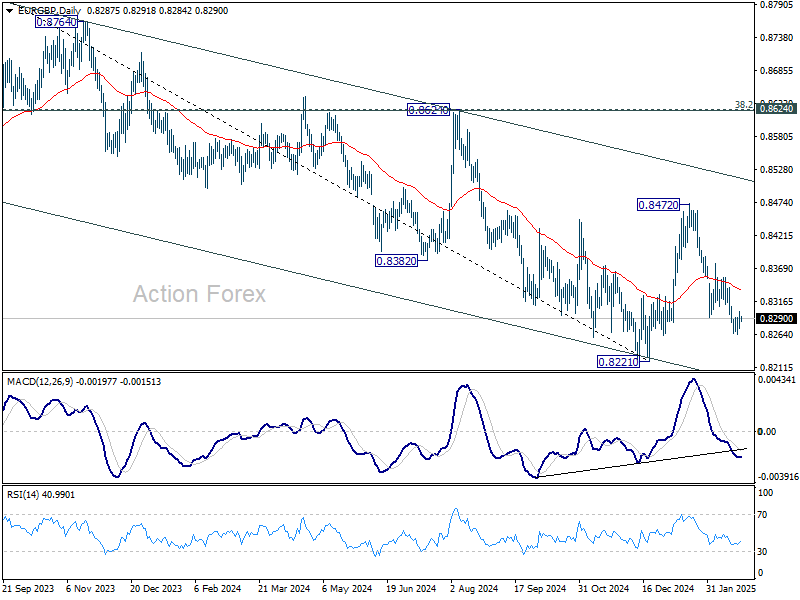

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8277; (P) 0.8290; (R1) 0.8303; More...

Intraday bias in EUR/GBP remains neutral first. Another fall is expected as long as 0.8308 minor resistance holds. Below 0.8264 will resume the whole decline from 0.8472 to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.

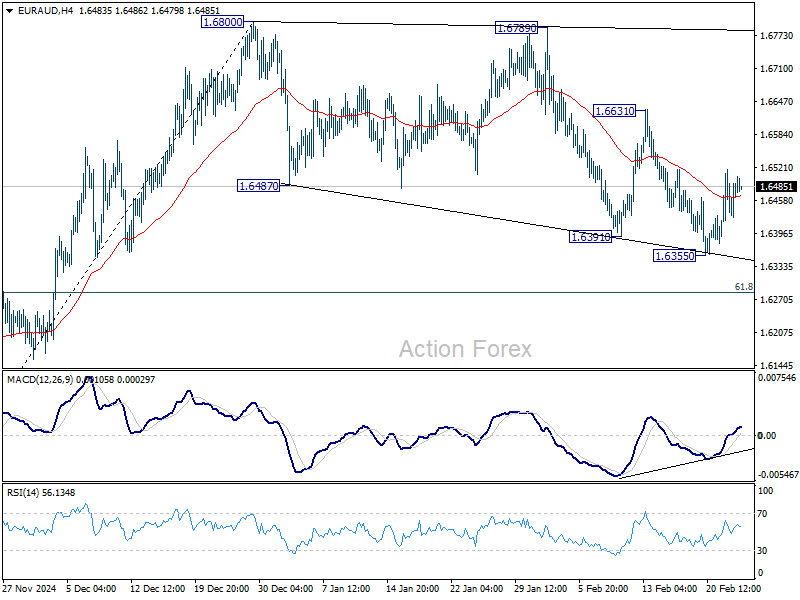

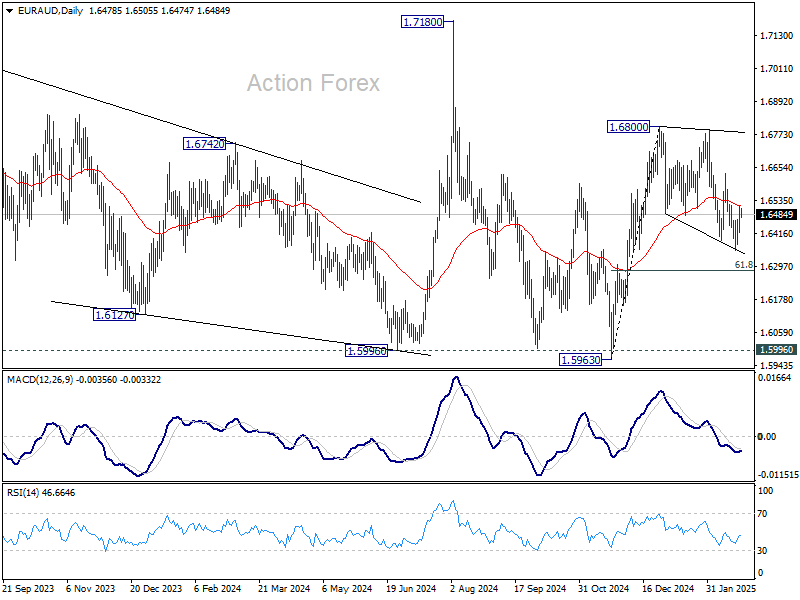

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6437; (P) 1.6479; (R1) 1.6528; More...

Intraday bias in EUR/AUD remains neutral at this point. Below 1.6355 will extend the corrective pattern from 1.6800 to 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, firm break of 1.6631 resistance will suggest that the correction has likely completed, and rise from 1.5963 is finally ready to resume.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

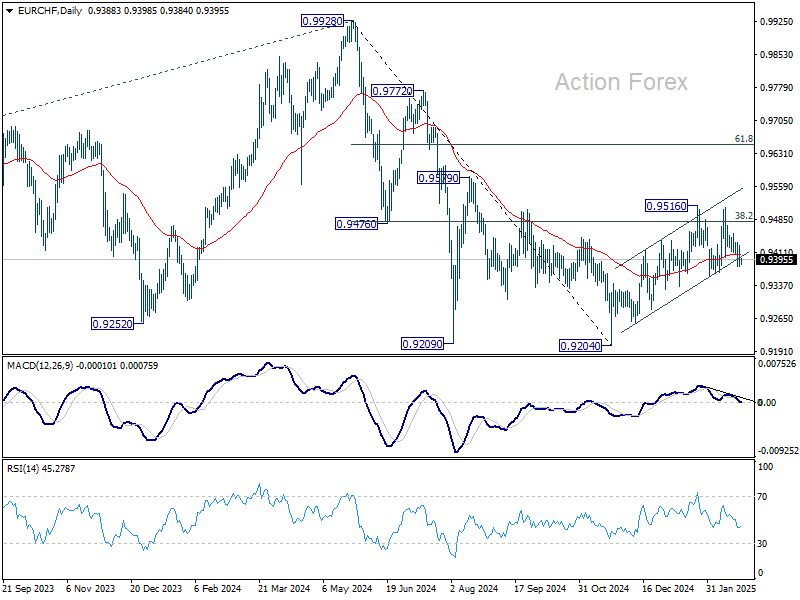

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9372; (P) 0.9400; (R1) 0.9419; More....

EUR/CHF is still bounded in range of 0.9359/9516 and intraday bias remains neutral. On the downside, firm break of 0.9359 will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

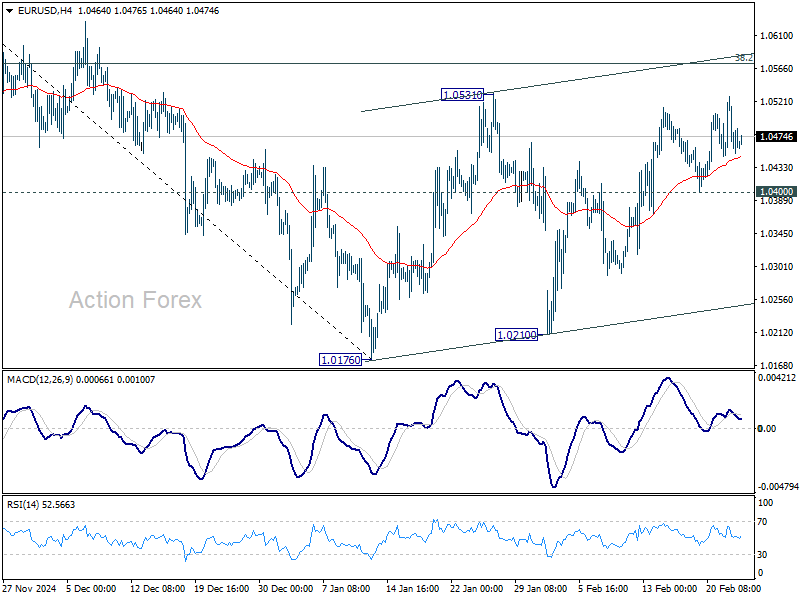

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0438; (P) 1.0483; (R1) 1.0513; More...

Intraday bias in EUR/USD remains neutral. Outlook is unchanged that price actions from 1.0176 are forming a corrective pattern only. Strong resistance is expected from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

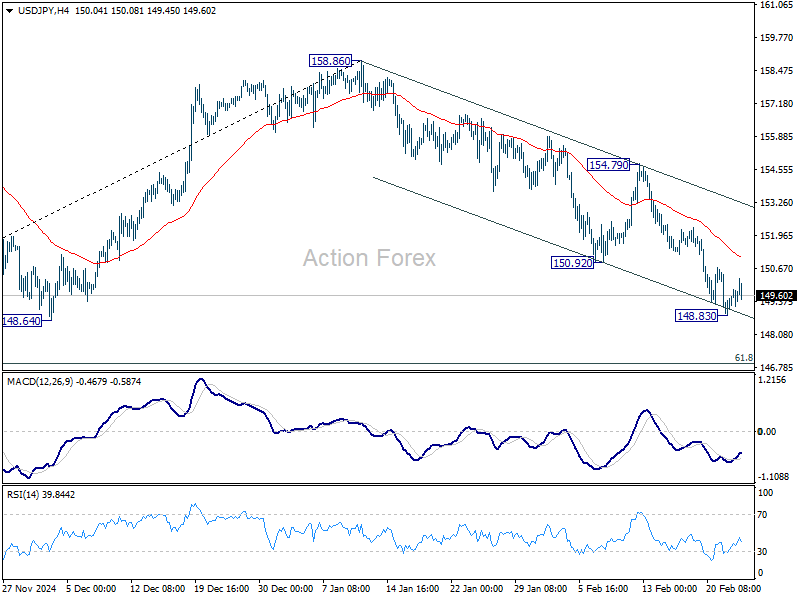

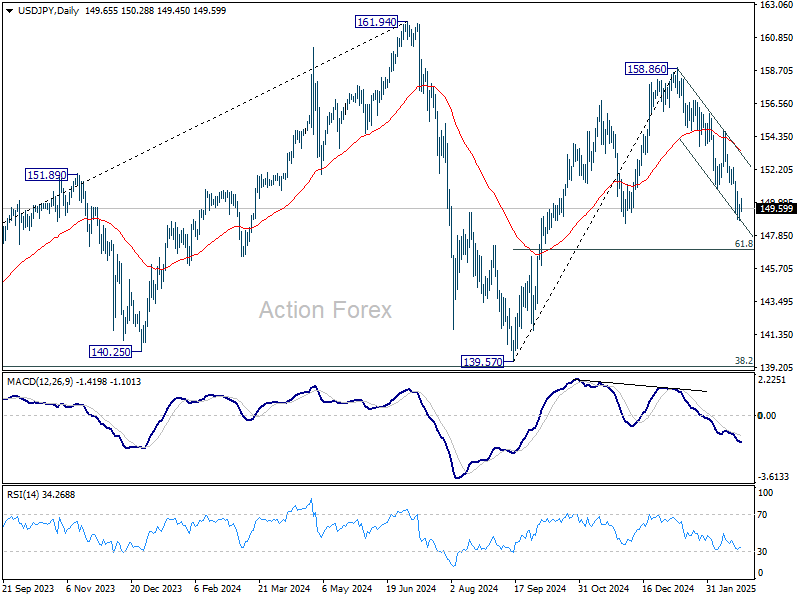

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.09; (P) 149.48; (R1) 150.12; More...

A temporary low is formed at 148.83 with current recovery and intraday bias in USD/JPY is turned neutral first. Further decline is expected as long as 154.79 resistance holds. Fall from 158.86 is seen as the third leg of the pattern from 161.94 high. Below 148.83 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

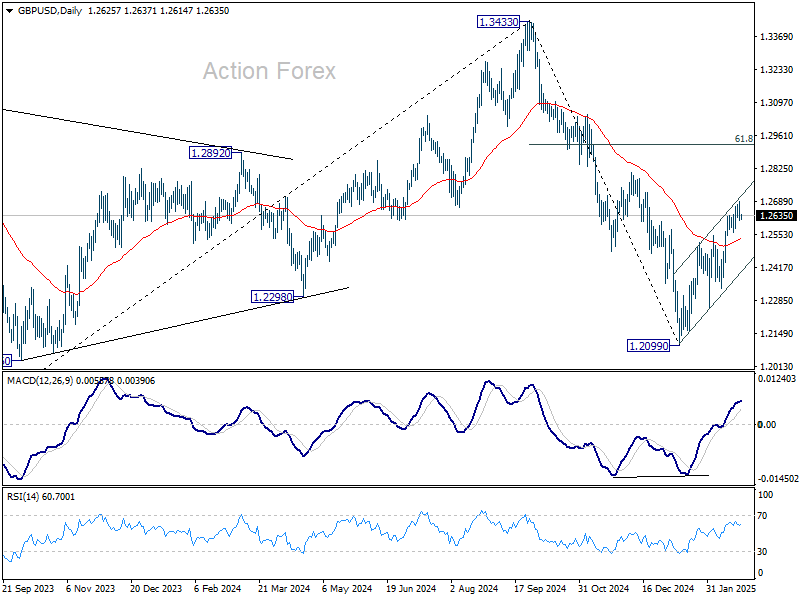

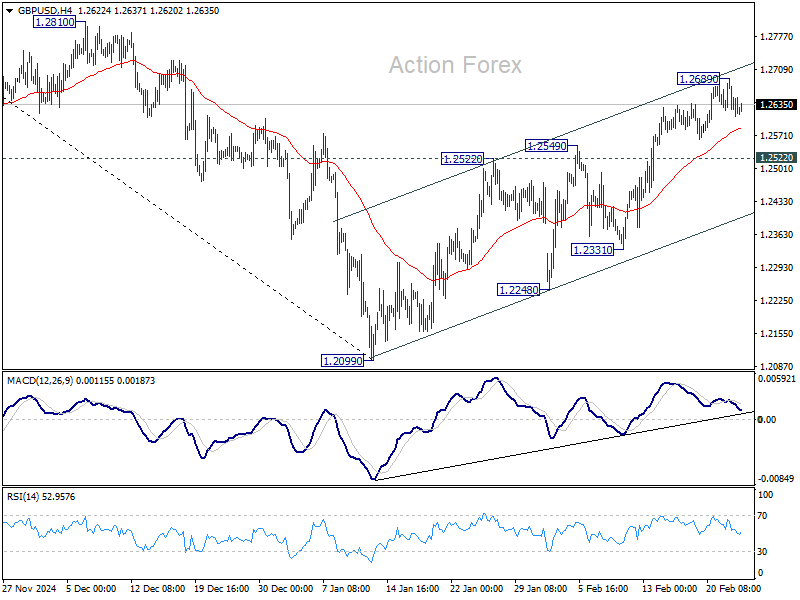

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2643; (R1) 1.2673; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.2689 temporary top. Further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.