Sample Category Title

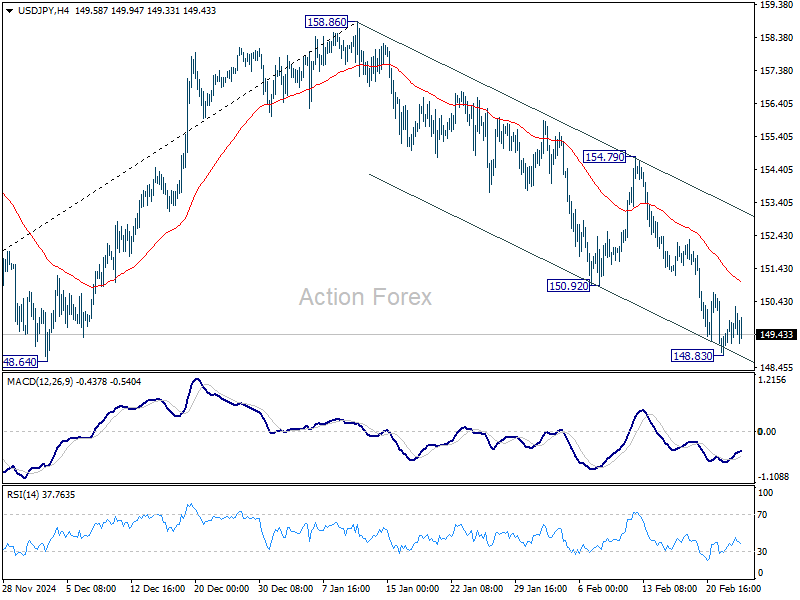

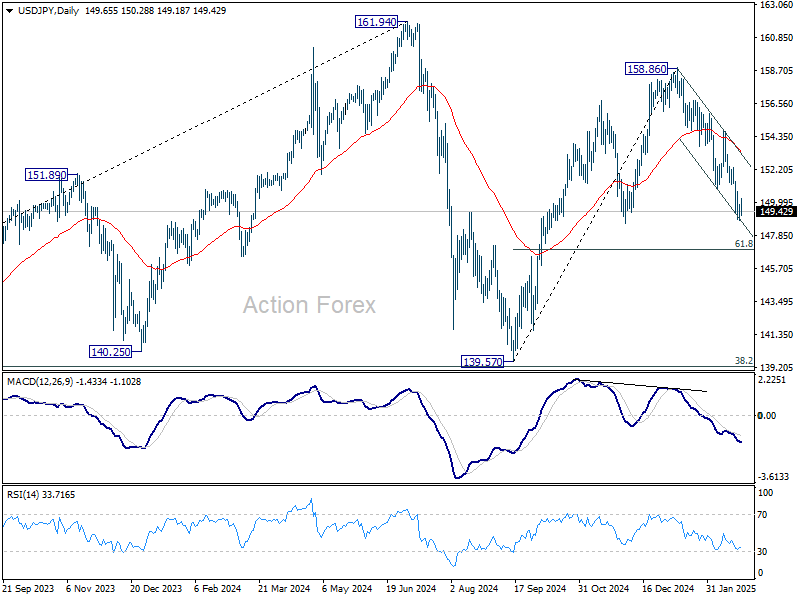

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.09; (P) 149.48; (R1) 150.12; More...

Intraday bias in USD/JPY stays neutral for consolidations above 148.83 temporary low. Further decline is expected as long as 154.79 resistance holds. Fall from 158.86 is seen as the third leg of the pattern from 161.94 high. Below 148.83 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

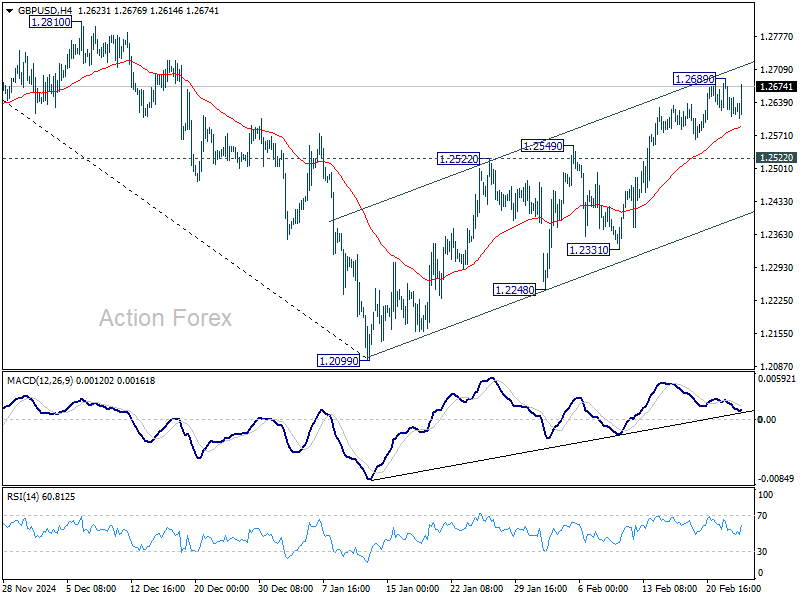

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2643; (R1) 1.2673; More...

Intraday bias in GBP/USD stays neutral at this point. Further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

Greenback Drops Ahead of Consumer Data, Risk Sentiment in Focus

Dollar weakened notably against European majors and Yen as markets transitioned into US session, despite subdued overall trading activity. The decline was largely driven by extended fall in US 10-year Treasury yield, which hit its lowest level since mid-December.

Beyond geopolitical and trade war concerns, market focus has turned toward whether slowing US consumption and softer economic data could force Fed to resume rate cuts sooner than expected, even as inflation remains elevated. Fed funds futures now price in a near 65% chance of a 25bps rate cut in June, a notable increase from 45% just a week ago.

The next catalyst for Dollar’s direction will be consumer confidence report, set for release shortly. However, Dollar’s next moves may not be straightforward, as risk aversion—if it intensifies—could provide some support due to safe-haven demand. US stocks, particularly the tech-heavy NASDAQ, could be vulnerable on the upcoming Nvidia earnings report later in the week.

For now, commodity currencies are under the most pressure, with Kiwi leading the declines. On the other hand, Swiss Franc is the strongest performer, followed closely by Sterling and Euro. Dollar and Yen are positioned in the middle.

Looking ahead to the Asian session, Australia’s monthly CPI reading will draw attention. Consensus suggests inflation might edge up from 2.5% to 2.6% in January, supporting RBA’s cautious stance even after it initiated its easing cycle earlier this month. Still, a downside surprise would provide RBA with added confidence to proceed with additional rate cuts if economic conditions worsen.

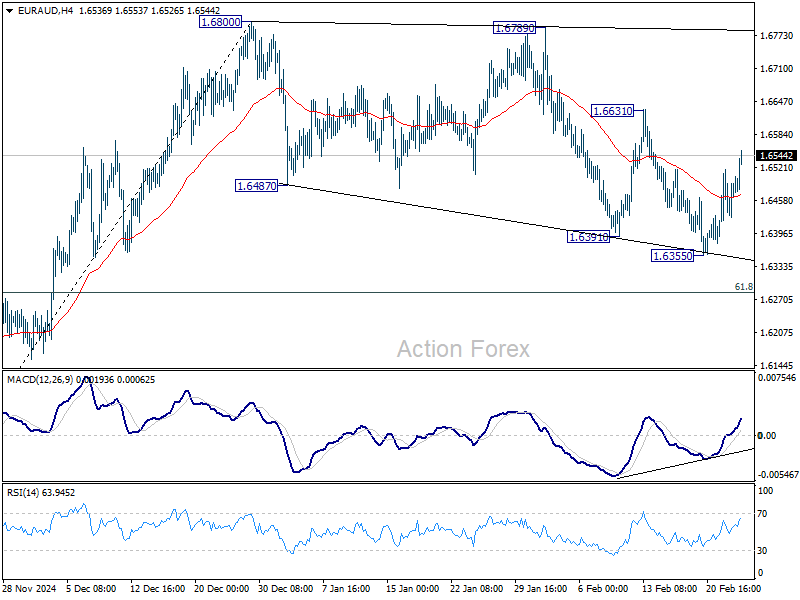

Technically, EUR/AUD's rebound is gaining some momentum today. Firm break of 1.6631 resistance will argue that the corrective pattern from 1.6800 has completed, and larger rise from 01.5963 is finally ready to resume through 1.6800.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.43%. CAC is up 0.04%. UK 10-year yield is down -0.0475 at 4.525. Germany 10-year yield is down -0.0012 at 2.479. Earlier in Asia, Nikkei fell -1.39%. Hong Kong HSI fell -1.32%. China Shanghai SSE fell -0.80%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield fell -0.0511 to 1.376.

ECB’s Nagel expects more rate cuts Amid encouraging price trends

German ECB Governing Council member Joachim Nagel indicated that incoming data suggests the central bank is on track to achieve its inflation target this year, opening the door for further rate cuts.

Speaking today, Nagel stated, "This would allow us on the Governing Council to lower the key interest rates further," reinforcing expectations that ECB will continue its gradual easing cycle.

However, Nagel also cautioned against premature optimism, highlighting "persistently elevated core inflation and the undiminished strength of services inflation."

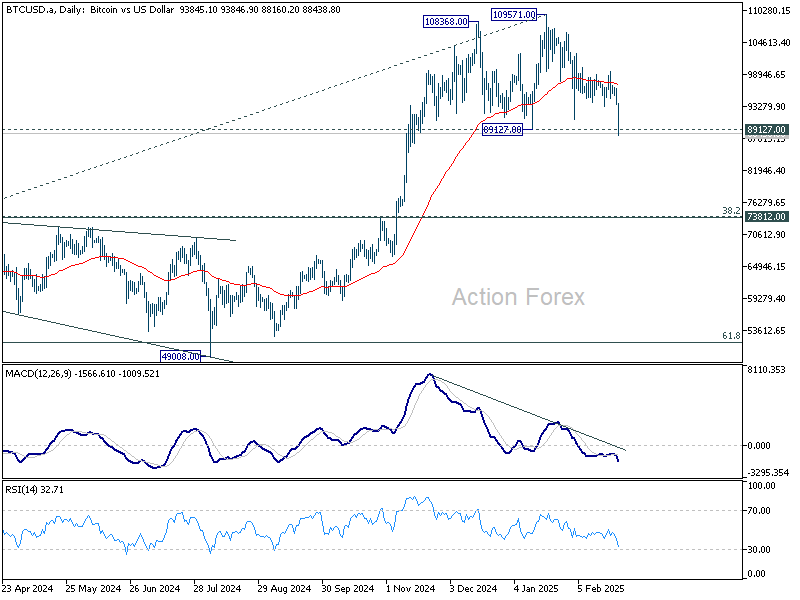

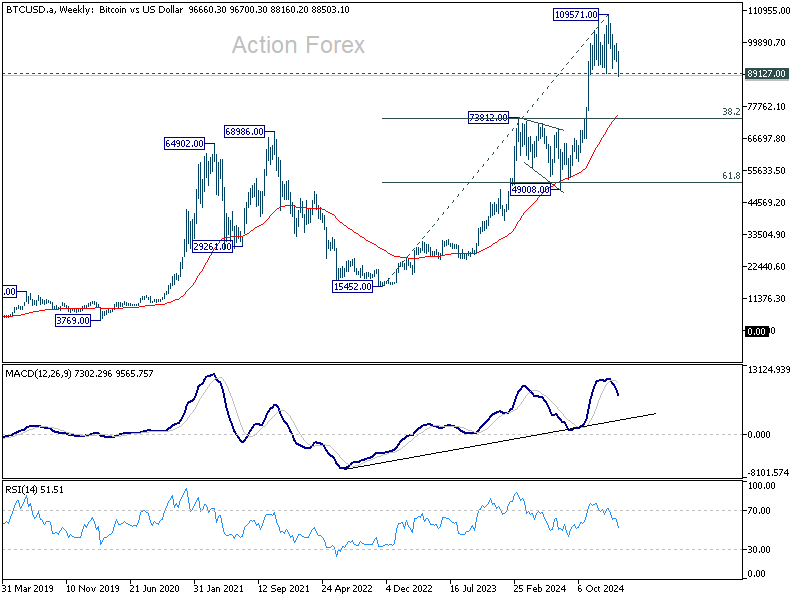

Bitcoin breaches 90K, double top breakdown could trigger deep correction

Bitcoin’s selloff intensified today, plunging below the 90k mark and hitting its lowest level since November. The immediate catalyst appears to be last week’s massive hack of USD 1.5B worth of Ether from cryptoexchange Bybit—an incident researchers have labeled the biggest crypto heist on record.

Although Bybit has announced that it fully restored the stolen Ether, market sentiment remains firmly negative, as traders grow wary of systemic risks and question the exchange’s ability to prevent future breaches.

Technically, Bitcoin now hovers at a critical juncture. The key 89,127 support level is under heavy pressure, and decisive break there would complete a double top pattern (108368, 108571). Such a development would strongly indicate that a larger-scale correction is underway.

In the bearish scenario, Bitcoin could be entering a correction of the entire rally from 15,452 (2022 low). The correction could target 73,812 cluster support (38.2% retracement of 15,452 to 109,571 at 73,617) before completion.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2594; (P) 1.2643; (R1) 1.2673; More...

Intraday bias in GBP/USD stays neutral at this point. Further rise will remain in favor as long as 1.2522 resistance turned support holds. Above 1.2689 will resume the rally from 1.2099 to 1.2810 resistance next. However, firm break below 1.2522 will argue that the rebound might have completed, and bring deeper fall to 1.2331 support.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

ECB’s Nagel expects more rate cuts Amid encouraging price trends

German ECB Governing Council member Joachim Nagel indicated that incoming data suggests the central bank is on track to achieve its inflation target this year, opening the door for further rate cuts.

Speaking today, Nagel stated, "This would allow us on the Governing Council to lower the key interest rates further," reinforcing expectations that ECB will continue its gradual easing cycle.

However, Nagel also cautioned against premature optimism, highlighting "persistently elevated core inflation and the undiminished strength of services inflation."

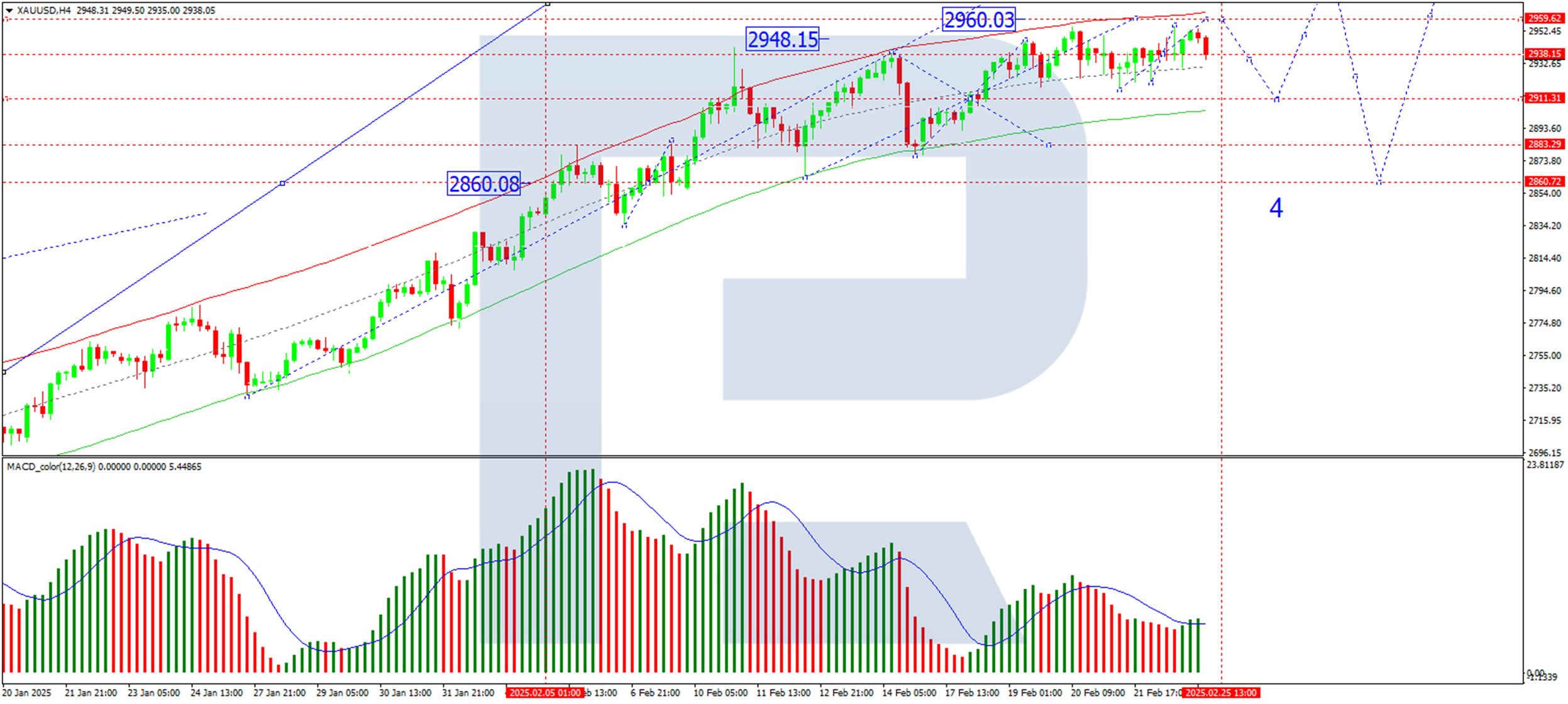

Gold Prices Rise Again as Demand for Safe-Haven Assets Increases

Gold stabilised around 2,940 USD per troy ounce on Tuesday, remaining close to record highs. The metal continues to benefit from strong demand for safe-haven assets amid growing concerns over US President Donald Trump’s tariff policies.

Key factors driving Gold prices

On Monday, Trump confirmed that tariffs on Canadian and Mexican imports will proceed as planned. This triggered fresh market concerns over inflation risks, which could influence the Federal Reserve’s future monetary policy.

In addition to geopolitical tensions, Gold is receiving support from the SPDR Gold Trust, the world’s largest gold-backed exchange-traded fund. The fund reported increased assets to 904.38, marking the highest level since August 2023.

Investors focus now shifts to Friday’s Personal Consumption Expenditures (PCE) report, the Fed’s preferred inflation gauge. The data is expected to show the slowest price growth since June 2024. However, persistent inflationary pressures may keep the Fed cautious about cutting interest rates too soon.

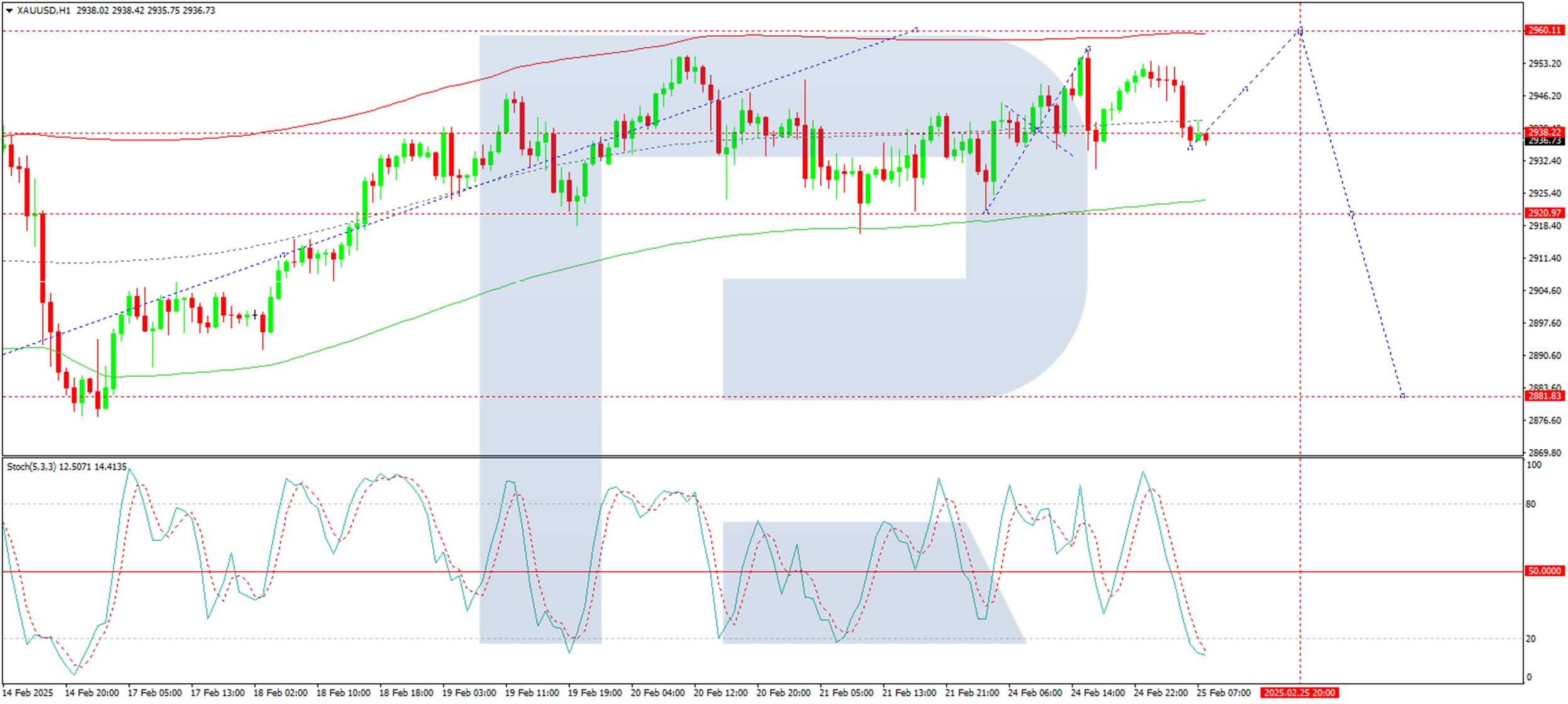

Technical analysis of XAU/USD

On the H4 chart, XAU/USD is consolidating around 2,938. A potential downward move towards 2,911 (a test from above) is likely before a renewed growth wave targets 2,960 as a local high. Once this level is reached, a corrective decline towards 2,860 could begin. The MACD indicator confirms this outlook, with its signal line above the zero level and pointing decisively upwards.

On the H1 chart, Gold recently formed a growth wave to 2,956 before correcting back to 2,938. A consolidation range is expected to develop around this level. If the price breaks downwards, a move towards 2,920 could occur before another upward impulse targets 2,960. The Stochastic oscillator supports this scenario, with its signal line below 20, indicating an imminent rise towards 80.

Conclusion

Gold remains in a strong uptrend, supported by safe-haven demand, geopolitical uncertainties, and increased holdings in gold-backed ETFs. Technical indicators suggest a potential short-term dip before another move higher towards 2,960. However, investors should watch upcoming inflation data, which could influence the Fed’s rate outlook and Gold’s trajectory.

Bitcoin – Violation of Key Supports Risks Deeper Correction

Bitcoin was sharply down in early Tuesday trading (losing over 6% in Asian / early European session) as soured sentiment sparked strong selling.

Fresh fall broke through key 90K support zone (floor of larger 90K/110K range) and generating strong bearish signal, with close below this zone to validate signal and open way for deeper correction, as bears also cracked pivotal Fibo support at 87801 (38.2% retracement of 52563/109582 rally.

Break of the range floor would also complete a double top pattern on daily chart and add to growing negative signals.

Technical pictures turn bearish (momentum indicator broke into negative territory / south-heading daily Tenkan/|Kijun-sen are diverging after creating a bear cross) and contributing to bearish outlook.

However, oversold conditions and today’s significant drop suggest that bears may take a breather for consolidation.

Broken 90K level turned into resistance which should ideally cap and maintain bearish stance for deeper drop and potential attack at 81200/81000 zone 200DMA / 50% retracement).

Res: 89038; 90000; 91759; 93292

Sup: 86784; 85132; 81235; 81059

Japanese Yen Steady as Producer Price Inflation Unchanged

The Japanese yen continues to have a quiet week. In the European session, USD/JPY is trading at 149.68, down 0.01% on the day.

The yen has shown recent strength against the US dollar and gained 2% last week. On Monday, the yen strengthened to 148.84 per dollar, its strongest level this year.

The Bank of Japan meets on March 18-19 and once again the markets will be in suspense ahead of the decision. The BoJ is expected to hold rates but there is a slight possibility of a rate hike. Inflation has been moving higher and yields on 10-year Japanese government bonds have been climbing and hit 1.455% last week, the highest level since Nov. 2009.

Last week, Japan’s core CPI hit rose to 3.2% in January, the highest level in 19 months. On Tuesday, the services producers price index jumped to 3.1%, up from 2.9% in December and in line with expectations. This will be followed by BoJ Core CPI on Wednesday and Tokyo Core CPI on Friday.

Will BOJ continue raising interest rates?

The BoJ has been an outlier amongst central banks as it has embarked on a tightening cycle. Every rate hike has had a strong impact on the financial markets but it’s important to remember that rates remain very low in Japan, at just 0.50%. The BoJ is expected to continue raising rates but the hikes will be gradual and the cash rate will remain much lower than in other central banks.

The BoJ is in no rush to raise rates and the threat of US tariffs has stoked concerns about higher inflation and lower global growth. The central bank will be carefully monitoring US trade policy and if the US imposes further tariffs, the BoJ is more likely to put plans to hike rates on ice.

USD/JPY Technical

- USD/JPY tested support at 149.48 earlier. Below, there is support at 149.09

- 150.12 and 150.51 are the next resistance lines

Bitcoin breaches 90K, double top breakdown could trigger deep correction

Bitcoin’s selloff intensified today, plunging below the 90k mark and hitting its lowest level since November. The immediate catalyst appears to be last week’s massive hack of USD 1.5B worth of Ether from cryptoexchange Bybit—an incident researchers have labeled the biggest crypto heist on record.

Although Bybit has announced that it fully restored the stolen Ether, market sentiment remains firmly negative, as traders grow wary of systemic risks and question the exchange’s ability to prevent future breaches.

Technically, Bitcoin now hovers at a critical juncture. The key 89,127 support level is under heavy pressure, and decisive break there would complete a double top pattern (108368, 108571). Such a development would strongly indicate that a larger-scale correction is underway.

In the bearish scenario, Bitcoin could be entering a correction of the entire rally from 15,452 (2022 low). The correction could target 73,812 cluster support (38.2% retracement of 15,452 to 109,571 at 73,617) before completion.

BTC/USD Analysis: Why Bitcoin’s Price Dropped Below $90K

The BTC/USD chart shows Bitcoin dipping below $89K today—the first time since November 2024, when the leading cryptocurrency surged on news of Donald Trump’s presidential victory.

We previously posted:

→ 28 January: Bitcoin Holds Above $100K—For Now

→ 11 February: How Trump Affects Bitcoin’s Price

In those analyses, we highlighted the extreme trading volumes during Trump’s inauguration and the heightened crypto market volatility. These conditions may have allowed major players to take profits after the 2024 rally. The subsequent price action has confirmed this bearish outlook.

Technical Analysis of BTC/USD

Since the surge in market activity during Trump’s inauguration (marked by a red arrow), Bitcoin has:

→ Formed a descending channel

→ Failed to break the psychological $100K level (black line)

→ Dropped below key support around $91K

A rebound attempt from the lower boundary of the long-term blue channel (blue arrow) was unsuccessful. In this environment, negative news could have aided bears in pushing Bitcoin towards the lower boundary of the channel.

Bitcoin’s Price Crash on 25 February

Bitcoin’s decline may have been driven by:

→ Market concerns over the ByBit hack, where around $1.5 billion in ETH was stolen

→ South Korean government sanctions on crypto exchange Upbit

→ A drop in US tech stocks ahead of Nvidia’s earnings report and PCE Price Index data, signaling investor caution toward risk assets

This bearish momentum has resulted in an almost 8% drop in under 24 hours, with over $1 billion in long positions liquidated across crypto exchanges. The RSI indicator is now near multi-month lows.

Bitcoin Price Outlook

BitMEX co-founder Arthur Hayes predicted on X that Bitcoin could fall to $70K if major hedge funds exit US Bitcoin ETFs.

This suggests further downside within the red descending channel. However, Bitcoin is near the lower boundary of this channel, meaning it could act as short-term support.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Early Initiatives by the US Government Risk Outsized Negative Effects on Growth

Markets

US stock markets traded heavy for a second session straight. They eventually closed at the session lows after hitting an air pocket in the final ten minutes of trading. The S&P 500 and Nasdaq respectively lost 0.5% and 1.2%. From a technical point of view, both indices are moving at a rapid pace from the top- to the downside of sideways trading ranges in place since December. First support kicks in at 5773 (vs 5983 close yesterday) and 18832 (vs 19286) respectively. Following higher US CPI readings and the market reaction to them mid-February, we warned about different asymmetric risks in the US vs Europe. The bar for upward surprises in the US was high following the hawkish Fed repricing and initial Trump election euphoria, leaving scope for outsized reactions on negative scares. It’s the opposite around in Europe where peak growth pessimism and a too dovish ECB reaction function are the base scenario, suggesting room for outsized moves in case of some good news. Over the past two sessions, we’ve seen some of that materializing in the US. US February PMI’s and Michigan consumer confidence shifted the needle from a good growth, high(er) inflation scenario to a weak(er) growth, high(er) inflation tale. Early initiatives by the US government like for example the DOGE efforts risk having outsized negative effects on growth as they increase consumer uncertainty and stall capex and hiring plans by companies. This negatively effects risk sentiment with US Treasuries rallying as the onus shifts to the stagnation-part of stagflation. Today’s February consumer confidence by the Conference Board could be testament to this short term momentum shift in trading. US treasury yields lost 2.5 bps to 3.7 bps yesterday with the belly of the curve outperforming the wings. Both the US 2-yr yield and the 10-yr yield are at risk of losing YTD support at respectively 4.15% and 4.38%. It’s worth noting that yesterday’s $69bn 2-yr Note auction produced some record demand metrics, stopping a full bp through the WI yield. The US dollar shows more and more signs of fatigue with EUR/USD yesterday testing first resistance at 1.0533 (YTD top). Lack of some EUR-strength is probably the only thing preventing a short term break higher right now. In this respect, we follow up on German spending plans (see News & Views), coalition talks, EU spending efforts (March 6 emergency summit) and recent hawkish ECB rhetoric hinting at a potential April pause in the cutting cycle. In this respect, we pay close attention to the central bank’s quarterly wage indicator. Recall them rising by a record 5.4% annual pace in Q3 with ECB president Lagarde pinning her hopes on a significant slowdown this year. Speeches by central bank governors and the US Treasury’s $70bn 5-yr Note auction are wildcards for trading.

News & Views

Germany’s chancellor-to-be Merz is said to have opened up talks with the Social Democrats (SPD) to fast-track as much as €200bn in special defense spending through the lame duck parliament, Bloomberg reported citing people familiar with the discussions. They are exploring ways to get around the country’s constitutional debt restrictions to free up resources to upscale the military. One approach would be similar to June 2022. Back then the ruling SPD-led coalition teamed up with the CDU/CSU opposition to approve a €100bn special fund, a move that required a constitutional change. The roles have turned this time around as did the size of a potential new package. Other options would be to expand the existing €100bn fund or to adapt the debt brake. Either way, they all require a two-third majority that is easier to be found in the current, outgoing legislature than in the next (March 24) due to a blocking minority on the far left and far right have after Sunday’s elections.

The central bank of South Korea (BoK) cut the policy rate by 25 bps to 2.75% this morning. Governor Rhee said market views of two to three more rate cuts this year were in line with the BoK’s view, clearly hinting at more easing to come. Based on the views disclosed, these follow-up rate cuts should not come at every next meeting, though. Such guidance came after the central bank downgraded its growth forecast again to a below-average 1.5% for this year, citing US protectionist policies as one of the factors. South Korea is heavily trade-reliant while private consumption and construction is souring as well, along with consumer confidence that got seriously dented by the political chaos in December of last year. Rhee urged the government to step in with more spending (to the tune of KRW 15-20tn) to help prop up growth since monetary policy cannot do all of the heavy lifting alone. The South Korean currency reacted stoic near its YtD lows around USD/KRW 1431.