Sample Category Title

Bitcoin Extends Rally To Over $10,000

Bitcoin extended the rally to trade above $10,000 for the first time in two weeks. The rally came as the regulatory noise that dominated the markets in recent times seemed to fizzle out.

The current rally started last week when the Commodities and Futures Trading Commission (CFTC) and Securities and Exchange Commission (SEC) appeared before a Senate committee. Asked about their recommendations about cryptocurrencies, they emphasized on regulatory issues instead of outright banning of the currencies.

This language was divergent from the one used by other regulators, particularly in South Korea and China. This week, however, the South Korean government toned down the criticism of cryptocurrencies. The minister of the office for government coordination, Hong Nam-Ki released a statement saying the government was not prepared to ban cryptocurrencies trading. Traders take this as a positive thing for the currencies.

In the past two weeks, bitcoin has gained by almost 50% and is currently trading at $10,200. The continued stability could bring more demand for the currencies. In fact, a report by CNBC showed that online brokers have started seeing more stability caused by more demand.

The BTC/USD is currently trading well above the 25-day and 15-day moving average. The pair’s average directional index is currently near 40, which is an indicator of a strong trend. At the same time, the pair appears to be forming a cup and handle pattern. Therefore, there is a likelihood that the pair could continue moving up, potentially to the $11,700 level.

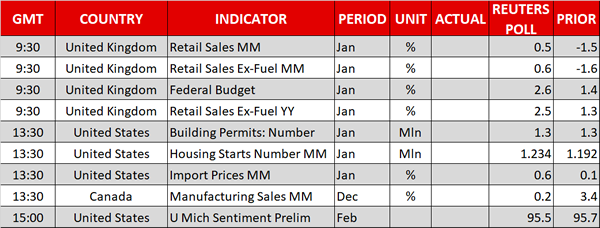

Data From UK, US Set To Drive Markets On Friday

A steady stream of economic data will make its way through the financial markets on Friday, with the United Kingdom and the United States set to release the most noteworthy reports. Meanwhile, traders will be gauging overall market sentiment as Wall Street continues to recover from one of its worst weeks since the financial crisis.

The first calendar event of the day is a report on German wholesale prices, which is set for release at 07:00 GMT. The monthly report is expected to show a 0.2% increase in the wholesale price index for January.

Two-and-a-half hours later, the UK's Office for National Statistics will present the latest retail sales numbers for January. Receipts at retail stores are forecast to jump 0.5% following a sharp decline during Christmas. In annualized terms, retail sales are expected to grow 2.6%.

Shifting gears, to North America, a report on US housing starts and building permits will make headlines at 13:30 GMT. Housing starts are forecast to climb 3.4% in January to a seasonally adjusted annual rate of 1.234 million units. Building permits – a bellwether of future construction intentions – are expected to climb 3.5% to 1.3 million.

Later in the session, the University of Michigan will release the preliminary consumer sentiment index for February. The monthly reading of 95.5 is expected to be only slightly lower than the January print.

Meanwhile, energy traders will be keeping close tabs on the weekly oil rig count data from Baker Hughes Inc.

The US dollar is wrapping up a disastrous week where it fell to fresh three-year lows against a basket of world currencies. The US dollar index (DXY) was last seen trading at 88.59, more than reversing last week's solid gain. The currency is down nearly 4% year-to-date, with more losses expected as central banks in Europe and Canada continue to roll back monetary easing.

EUR/USD

Dollar pains drove the euro firmly higher on Thursday, a trend that continued into a mostly subdued Asian session on Friday. The EUR/USD exchange rate edged up 0.1% to 1.2512, where it was testing new multi-year highs. The pair is eyeing a strong resistance test around 1.2540

GBP/USD

Cable was back in the driver's seat on Thursday, as prices returned to 1.4100 for the first time in over a week. The GBP/USD exchange rate was last up 0.1% at 1.4111, where it had reversed most of last week's slump. The pair is now approaching an important target above 1.4150 as the next cue for the bulls.

US OIL

After trading sideways for two days, US oil prices rebounded sharply in back-to-back sessions. The contract is trading at $61.50 and could be poised to continue higher should the weekly inventory data show a drop in active rig counts.

Dollar Sinks To 3-Year Low, UK Retail Sales Eyed

Here are the latest developments in global markets:

FOREX: The dollar index traded almost 0.3% lower on Friday, adding to the losses it posted yesterday and recording a new three-year low. The continued slide in the world’s reverse currency managed to push euro/dollar to 1.2555 overnight, marking a fresh high last seen in 2014 for the pair. Meanwhile, dollar/yen posted a new 15-month low.

STOCKS: US equity indices continued to recover yesterday, amplifying expectations that the recent turbulence may be gradually fading. The Nasdaq Composite led the way, climbing by 1.6%, while the S&P 500 and the Dow Jones both rose by 1.2%. It is worth noting that all three of these indices have closed higher every day so far this week, while the so-called 'fear index' (VIX) has also declined steadily, both factors enhancing the argument that the selloff may have run its course, for now at least. Futures tracking the Dow, S&P, and Nasdaq 100 are all in positive territory at the time of writing, albeit marginally so. This positive sentiment rolled into Japanese trading as well, with the Nikkei 225 and the Topix indices gaining 1.2% and 1.1% respectively. Markets in mainland China and Hong Kong are closed in celebration of the Lunar New Year. Over in Europe, futures tracking all of the major stock indices are safely in the green.

COMMODITIES: Oil prices traded a little higher on Friday, with WTI and Brent crude gaining 0.2% and 0.3% respectively. With little in the way of energy news, the liquid’s gains may be owed to the continued weakness in the US dollar, as well as the sustained recovery in risk sentiment, which is supporting energy stocks and by extent, oil prices themselves. Despite the recent rebound though, one must sound a note of caution, as the fundamentals of the oil market seem to be deteriorating rather quickly. US production is already at all-time highs and seems to be rising still, a factor that could keep a lid on any near-term gains in oil. Today, investors will look to the release of the Baker Hughes oil rig count for signs on whether US output continues to soar. In precious metals, dollar-denominated gold is nearly 0.4% higher today, last seen near the $1360/ounce mark. The $1366 resistance zone is worth keeping an eye on. If buyers manage to overcome it, that would mark a fresh high on the daily chart, and it could be a signal for further advances.

Major movers: The dollar’s slide continues; Kuroda secures another term as BoJ Governor

The US dollar continued to bleed on Thursday, extending its losses during the Asian trading session Friday, even though the yields on 10-year US Treasuries touched a fresh four-year high yesterday. The inability of the greenback to draw any support from the bond market lately is quite perplexing, and likely reflects the fact that yields may be rising for the 'wrong reasons'.

Namely, instead of the surge in yields being driven by expectations that a healthy US economy will lead the Fed to raise rates more aggressively, it may be largely owed to investors reducing their exposure to Treasuries amid concerns that widening US deficits will make the nation’s debt trajectory even more unsustainable. Indeed, today’s release of flow data from the Japanese Ministry of Finance adds credibility to this argument, as it confirmed that Japanese investors continued to sell off foreign bonds in the week ended February 9. The repatriation of these funds in light of the Japanese fiscal year ending soon may be one of the major factors behind the yen’s recent gains.

Speaking of the yen, it gained nearly 0.3% against the dollar today to briefly touch the 105.50 area, a fresh 15-month low for dollar/yen, even despite relatively dovish news coming out of Japan. Haruhiko Kuroda has been reappointed for another term as Bank of Japan (BoJ) Governor, while the government also nominated another two deputy Governors to join the BoJ, both of which are seen as policy doves. This suggests that the Bank is very likely to keep its ultra-loose policy framework in place for a while longer, which in isolation, is a negative development for the yen. Nonetheless, in an environment where Japanese funds are repatriating money, and where the currency may enjoy increased inflows due to its safe-haven status amid this equity turbulence, this may not matter all too much in the near-term.

Elsewhere, aussie/dollar is 0.4% higher, with the pair remaining largely unfazed by some comments from Reserve Bank of Australia Governor Philip Lowe overnight, who said that he would prefer a lower AUD to a higher one.

Day ahead: UK retail sales, US housing data and University of Michigan consumer sentiment survey among Friday’s releases

Dominating attention during morning European trading hours (at 0930 GMT) will be the release of UK retail sales for the month of January. Both headline and core retail sales – that exclude fuel for automotives – are projected to rebound on a monthly basis following December’s contraction. In 2017, UK retailers experienced their worst year since 2013 as inflation outstripping wage growth – translating into weaker purchasing power for households – weighed on consumer spending and consequently on retail sales. Should the readings move convincingly towards offsetting weakness from the past, then market participants are likely to interpret them as yet another factor supporting the case for a Bank of England rate hike being delivered sooner rather than later, potentially pushing sterling higher versus other currencies.

US housing data due at 1330 GMT are also of importance. Housing starts were affected by cold weather conditions in December, recording their sharpest monthly fall in around a year. January’s print is interesting to watch as the extreme weather effects are dropping out of the data. Building permits and import prices for January will be made public at the same time.

Another release attracting interest in the US is the University of Michigan’s preliminary survey on consumer sentiment for the month of February. Not much of a change in consumer sentiment is expected relative to January. The survey will be made public at 1500 GMT. Investors may also look at another aspect of this survey, inflation expectations, to either confirm or disprove the recent narrative that higher US inflation is around the corner.

Canadian manufacturing sales for the month of December due at 1330 GMT will be gathering loonie traders’ attention.

In politics, US Secretary of State Rex Tillerson will be meeting Turkish Foreign Minister Mevlüt Çavuşoğlu. The meeting could be interesting given the rising tensions between the two countries. Also of interest – amid Brexit negotiations – might be a meeting between UK PM Theresa May and German Chancellor Angela Merkel in Berlin.

Oil traders will be paying attention to the US Baker Hughes oil rig count due at 1800 GMT.

The earnings season remains in full swing, with Coca-Cola being among companies releasing quarterly results in the US.

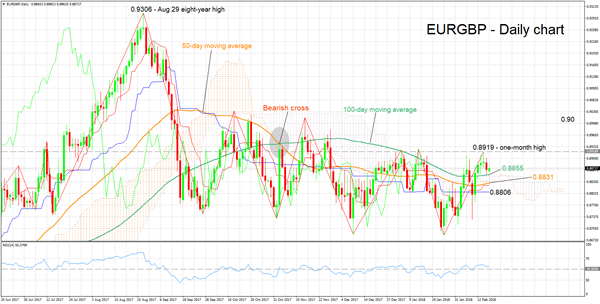

Technical Analysis: EURGBP looking increasingly neutral in short-term ahead of UK data

EURGBP retreated a bit after hitting a one-month high of 0.8919 on Wednesday. The Tenkan-sen line remains above the Kijun-sen line – a positive short-term signal – though both lines have flatlined, perhaps pointing to a lack of direction in the short-term. The RSI seems to have halted its advance as well, lending support to a mostly neutral short-term picture.

UK retail sales data due later have the capacity to move the pair in either direction. Stronger-than-anticipated readings are likely to push it lower. Support in this case could come around the current level of the 100-day moving average at 0.8855. The area around this level also encapsulates the Ichimoku cloud as well as the 50-day MA (0.8831), while not far below lie the Tenkan-sen (0.8825) and Kijun-sen (0.8806) lines; given the proximity of all these points, they could in essence be viewed as one broad range of support.

Weaker-than-projected data on the other hand, are expected to be met with price advancing. In this scenario, the area around Wednesday’s high of 0.8919 (including the 0.89 handle which may be of psychological significance) might act as a barrier to the upside. In case of an upside break, the 0.90 handle would be eyed next. The range around this point includes a number of peaks from the recent past.

Technical Outlook: GBPUSD Extends Recovery For The Fifth Day, UK Retail Sales/May/Merkel Meeting In Focus

Sterling maintains firm tone in early Friday's trading and extends steep recovery leg from 1.3764 (09 Feb correction low) into fifth straight day, posting new nearly recovery high at 1.4144 (the highest in nearly two weeks).

Strong bullish acceleration in past two days resulted in probe through pivotal barrier at 1.4123 (Fibo 61.8% of 1.4344/1.3764 pullback) today, with close above here to generate fresh bullish signal for further advance.

Next barrier lies at 1.4207 (Fibo 76.4%), followed by 1.4277 (01/02 Feb double top / lower platform) and key resistance at 1.4344 (25 Jan peak) the highest since 24 June 2016 Brexit vote.

Session low at 1.4088 marks initial support, followed by broken 20SMA at 1.4037, which is expected to keep the downside protected.

Technical studies are in full bullish setup and underpinning with focus turning on release of UK retail sales and meeting between UK PM Theresa May and German Chancellor Angela Merkel.

Retail sales are forecasted for significant rise in Jan (m/m 0.5% f/c vs -1.5% in Dec / Core m/m 0.6% f/c vs -1.6% in Dec, while annualized figures are forecasted to rise over 1% in Jan).

Release at/above forecasted levels would further inflate pound and accelerate recovery.

Market participants will be also closely watching the outcome of the meeting of UK/Germany leaders who will try to overcome the difficulties in negotiations of divorce between the UK and European Union.

Res: 1.4156, 1.4200, 1.4277, 1.4344

Sup: 1.4088, 1.4021, 1.4000, 1.3960

USDCAD Looking Neutral In Short Term, Bearish In Medium Term

USDCAD attempted several times to cross above the 50% Fibonacci of the downleg from 1.2919 to 1.2248 but its efforts were fruitless as it finally reversed direction to test resistance at the 38.2% Fibonacci. The technical indicators now support that the short-term bias is neutral, while in the medium-term the outlook is seen bearish.

The 20-day simple moving average (SMA) has flattened, suggesting that the pair might consolidate for a while. However, if prices manage to fell below this line, a trend reversal to the downside in the near term could be close at hand. The RSI also shows that some consolidation might emerge since the index is currently attached to its neutral threshold of 50. Yet we cannot exclude any upside movements as the red Tenkan-sen line has recently crossed above the blue Kijun-sen line and is positively sloped.

Should the market head up, the 38.2% Fibonacci at 1.2503 could provide nearby resistance before the 50% Fibonacci of 1.2590 of the downleg from 1.2919 to 1.2248 come into view. The latter is seen as a stronger barrier as the area has been approached several times in the past and, while the pair would need to break the 50-day SMA as well. Therefore, a substantial close above this level would resume the recent upswing, opening the way towards the 61.8% Fibonacci of 1.2673. A leg above the 200-day SMA of 1.2729 could also increase bullish sentiment in the long-term.

To the downside, immediate support could come from the 20-day SMA at 1.2446 ahead of the 23.6% Fibonacci of 1.2404. Further below, the focus would shift to the 1.2300 key-level and the previous low of 1.2248.

Regarding the medium-term picture, the outlook is bearish as long as the market keeps trading below the 50-day SMA and the bearish crossover between the 50- and the 200-day SMA remains intact.

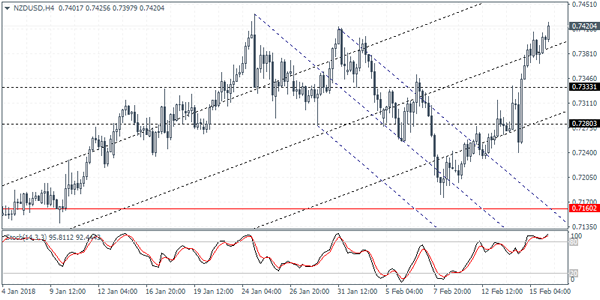

NZDUSD Intraday Analysis

NZDUSD (0.7420): The New Zealand dollar is seen testing the highs around 0.7420 level, marking the highs established from two weeks ago. The reversal in the price action suggests upside momentum with the U.S. dollar continuing to remain weak. Watch for a retest of support near the 0.7333 region which served as resistance. To the upside, NZDUSD could be targeting 0.7480 level where the next main resistance level will be tested.

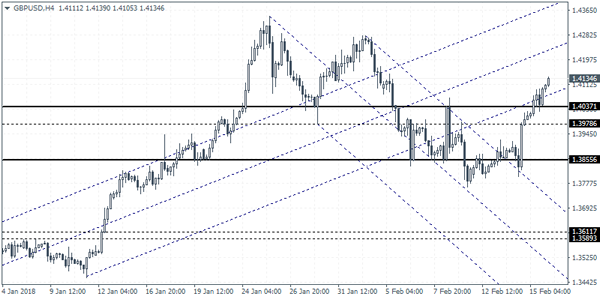

GBPUSD Intraday Analysis

GBPUSD (1.4134): The British pound managed to push higher with price breaking out from the upside. The breakout from the resistance level at 1.4037 could indicate further upside gains in the currency pair. Watch for a short term correction towards 1.4037 for support to be established. This could potentially see further gains targeting the previous highs around 1.4279. To the downside, the declines will be limited to the support level but a break down below this level could keep GBPUSD range bound in the short term.

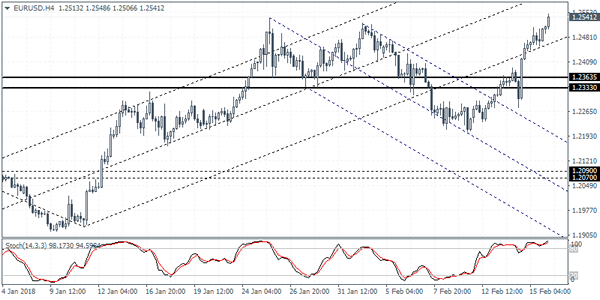

EURUSD Intraday Analysis

EURUSD (1.2541): The EURUSD maintained the gains yesterday as price rallied to a fresh 3 year higher earlier today. The gains in the euro came as the U.S. dollar failed to hold on the gains giving a lift to the common currency. With the strong gains, any downside correction could be limited to the 1.2365 level which previously served as resistance. A retest of support at this level could signal a potential rebound with the upside bias intact.

USD Stays Soft As Market Price In A March Rate Hike

The USD was seen trading weaker across the board on Thursday. The biggest gains came from the Japanese yen which surged 0.82% on the day.

Economic data from the U.S. was mixed. Producer price index data from the U.S. showed a 0.4% increase matching estimates and rising to an annual pace of 2.7%. Industrial production figures showed a 0.1% decline in January with previous month's data being revised lower as well.

The capacity utilization rate slipped to 77.5%. The regional manufacturing index data showed that the Philly Fed manufacturing index rose to 25.8 beating estimates while the NY Fed manufacturing index eased from 17.7 in the previous month to 13.1 in February.

Looking ahead, the retail sales data from the UK is expected to show a 0.5% increase after falling 1.5% the month before. The data comes amid UK households facing faster inflation and slower wage growth. Data from the U.S. today will see the housing starts and building permits data coming out.

Currencies: Red Alert For USD

Sunrise Market Commentary

- Rates: Some consolidation ahead of the weekend?

Today’s eco calendar probably won’t impact trading, suggesting sentiment-driven and technical action. Underlying core bond sentiment remains negative and the comeback of stock/commodity markets adds to that picture. However, with the Bund and the US Note future entering oversold conditions, we’d argue in favour of some consolidation. - Currencies: Red alert for USD

Dollar weakness prevails this morning. USD/JPY dropped below key support (106.52). EUR/USD tests the 1.2537 cycle top. The trade-weighted dollar (DXY) tests the cycle low (88.43) which coincides with the 62% retracement level of the dollar’s 2014-2016 rally. Red alert for USD!

The Sunrise Headlines

- US stock markets closed with strong gains yesterday (+1.5%), marking a fifth straight positive day. Most Asian stock markets are closed for Lunar NY. Japan copies WS’s gains despite more yen strength.

- Japanese PM Abe nominated Kuroda to lead the BoJ for another 5y term, with the Cabinet forwarding the nomination to parliament. Central bank insider Amamiya and professor Wakatabe were tapped to be deputy governors.

- The US Senate failed to break its impasse over immigration after a week of debate as a flurry of unsuccessful votes left the chamber no closer to resolving the fate of hundreds of thousands of young, undocumented immigrants. (WSJ)

- Two thirds of supporters of Germany's SPD back forming a coalition government with Merkel's conservatives, an opinion poll showed, while 78% of supporters of the conservatives back the coalition.

- The RBA expects to make only gradual progress in reducing unemployment and having inflation return to its 2-3% target band, signalling interest rates will stay at record lows for a while yet.

- The UK is ready to lay out its post-Brexit plan for the financial sector, favoring an ambitious "mutual recognition" model, the FT reported.

- Today’s eco calendar contains UK retail sales, US building permits & housing starts and university of Michigan consumer confidence. ECB Coeuré is scheduled to speak.

Currencies: Red Alert For USD

Red alert for USD

The dollar remained under some downward pressure in Asia yesterday morning, but stabilized in Europe. Mixed US eco data had no impact. New US equity strength put the greenback again slightly in the defensive. EUR/USD closed the session at 1.2506. USD/JPY remains the biggest victim of dollar weakness with USD/JPY closing below the 62% retracement level of the mid 2016 to end 2016 rally (106.52). A confirmed break suggests complete retracement towards 99.02.

Positive risk sentiment and the dollar decline remain at play overnight. Several Asian markets are closed for the Lunar NY. Japanese stocks gain 1% despite a further decline of USD/JPY. The pair trades below 106 even if Japanese PM Abe confirmed Kuroda’s extension at the head of the BoJ. One of the newly appointed deputy governors is a proponent of QE and argued in favour of increasing asset purchases. Japanese FM Aso said that they are carefully watching FX moves and will act if needed. All yen-negative signals which the market currently ignores. Dollar weakness also translates in EUR/USD testing the 1.2537 cycle top this morning. The trade-weighted dollar (DXY) tests the cycle low (88.43) which coincides with the 62% retracement level of the dollar’s 2014-2016 rally. Red alert for USD!

The US eco calendar contains housing data and Michigan consumer confidence, but that won’t change the fortunes of the dollar. ECB Coeuré speaks. He wants to end APP in September 2018. Will he refer to current euro strength? The repositioning on equity markets and technical considerations are more important. Positive risk sentiment correlates with a further decline of the dollar. USD/JPY lost important support, while EUR/USD and DXY test key hurdles. A sustained break would signal more trouble for the dollar. We don’t see a fundamental reason for EUR/USD to already break this level, but this is not a good enough reason to row against the tide. The dollar is a falling knife.

EUR/GBP traded with a small negative bias yesterday, closing at 0.8858. UK retail sales are expected to rebound 0.6% M/M and 2.4% Y/Y after a sharp setback in January. We doubt that even better than expected data will be a big help for sterling. EUR/GBP holds the 0.8690/0.9033 range. We hold our view that the 0.8690 support won’t be easy to break without big progress on Brexit. UK PM May and German Chancellor Merkel hold Brexit talks in Berlin.

EUR/USD tests ST range top