Sample Category Title

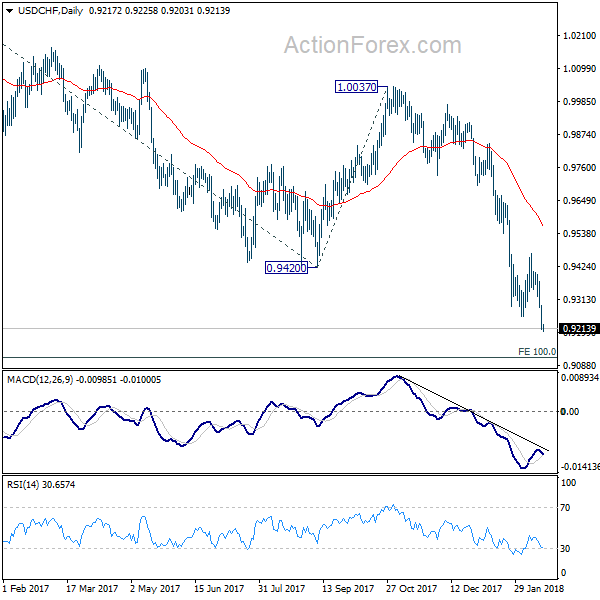

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9188; (P) 0.9240; (R1) 0.9271; More...

USD/CHF's decline is still in progress and intraday bias remains on the downside. Current down trend should target 0.9115 medium term projection level next. On the upside, break of 0.9469 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

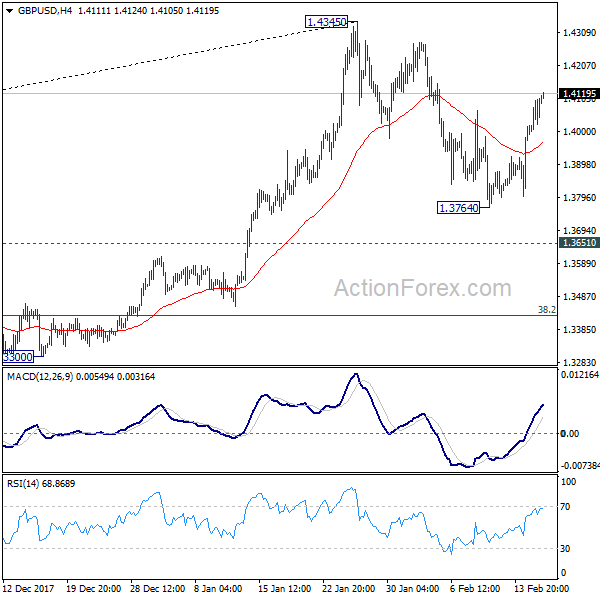

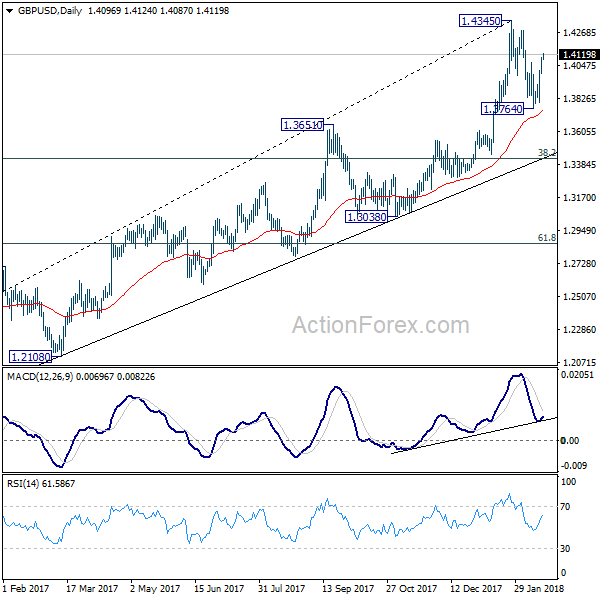

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4027; (P) 1.4065; (R1) 1.4139; More.....

Outlook in GBP/USD is unchanged. Pull back from 1.4345 should have completed at 1.3764 already. Intraday bias remains on the upside for retesting 1.4345 first. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105). On the downside, below 1.3764 will extend the correction to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

USD/JPY Remains In Major Downtrend

Key Highlights

- The US Dollar declined heavily this week and moved below the 108.20 support against the Japanese Yen.

- There are two bearish trend lines forming with resistance at 107.40 and 108.10 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending Feb 10, 2018 rose from the last revised reading of 223K to 230K.

- The US Industrial Production in Jan 2018 declined 0.1% (MoM), whereas the market was looking for 0.2%.

USDJPY Technical Analysis

The US Dollar was under a lot of bearish pressure this week against the Japanese Yen. The USD/JPY pair broke a major support at 108.20 and moved into the bearish zone.

Looking at the 4-hours chart of USD/JPY, the pair clearly faced an increased selling pressure and declined by more than 200 pips. After the 108.20 support break, the pair traded below the 108.00 and 107.00 support levels.

The downside move was strong and the pair traded close to the 106.00 level. A low was formed at 106.02 from where a minor correction was initiated. On the upside, an initial resistance is around the 23.6% Fib retracement level of the last decline from the 108.77 high to 106.02 low.

There are also two bearish trend lines forming with resistance at 107.40 and 108.10 on the same chart. If the pair corrects substantially from the current levels, the broken supports at 107.50 and 108.00 are likely to act as resistances.

On the downside, a break below the recent low of 106.02 could push the pair below 105.80. The next major support is at 105.40, followed by 105.00.

UK Industrial Production

Recently in the US, the Industrial Production for Jan 2018 was released by the Board of Governors of the Federal Reserve. The market was looking for an increase of 0.2% in the Industrial Production compared with the previous month.

The actual result was well below the forecast, as there was a decline of 0.1% in the Industrial Production. This was also well below the last increase of 0.4%. The report added:

Manufacturing production was unchanged in January. Mining output fell 1.0 percent, with all of its major component industries recording declines, while the index for utilities moved up 0.6 percent. At 107.2 percent of its 2012 average, total industrial production was 3.7 percent higher in January than it was a year earlier.

Overall, the US Dollar remains in a bearish zone versus other major currencies such as the Euro, British Pound, Japanese Yen and Aussie Dollar. Today, the Building Permits and Housing Starts reports for Jan 2018 will be released, which may impact the greenback in the short term.

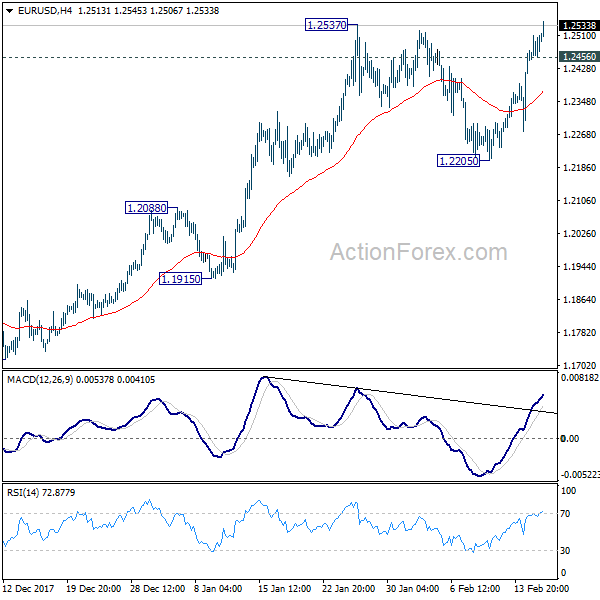

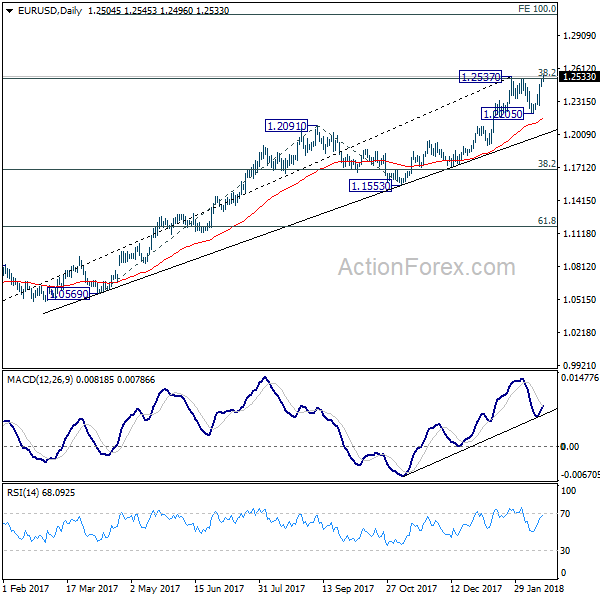

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2464; (P) 1.2487 (R1) 1.2529; More....

EUR/USD's rally continues today and breach of 1.2537 resistance suggests that larger up trend is resuming. Intraday bias stays on the upside. Sustained trading above 1.2537 will confirm and page the way to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2456 minor support will indicate rejection from 1.2537 and turn bias back to the downside for 1.2205 support.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Suffering Renewed Selloff, Yen Firm after Kuroda Nomination

Dollar suffers renewed selloff in Asian session with EUR/USD finally taking out 1.2537 near term resistance. The development could trigger more broad based weakness in the greenback before the weekly close. Elsewhere in the currency markets, Yen remains the strongest one for the week after Haruhiko Kuroda's nomination as BoJ Governor again is finally confirmed. Euro is trading as the second strongest for the week and that helps keep EUR/JPY resilient above 132 handle. Dollar and Canadian Dollar are the two weakest ones. Aussie closely follow as the third weakest after RBA Governor Philip Lowe reiterated the neutral stance.

RBA Lowe: No strong case for near term hike

RBA Governor Philip Lowe told the parliament today that the timing of any change in interest rate will "depend upon the extent and pace of progress that we make in reducing the unemployment rate and having inflation return to target." And, "as things currently stand, we expect that progress to be steady, but to be only gradual." Therefore, "the reserve bank board does not see a strong case for a near-term adjustment of monetary policy."

Regarding the job market, Lowe said that "we don't expect a repeat of these very strong outcomes in 2018, but we do expect employment growth to be fast enough to see a further gradual reduction in the unemployment rate." And, "the unemployment rate, though, is likely to remain above conventional estimates of full employment in Australia for some time."

For inflation, Low expected "wage growth to pick up as the labor market strengthens further." But, "the pick-up, though, is likely to be gradual." He added that "this increase in wage growth and the more general reduction in spare capacity in the economy are expected to contribute to inflation picking up as well. But to continue the theme, this pick-up, too, is expected to be only gradual."

NZ manufacturing expands at faster pace

Business NZ manufacturing PMI rose to 55.6 in January, up from 51.2, indicating faster expansion. BNZ Senior Economist Craig Ebert noted that "while the NZ PMI has led the world for the last five years, the global PMI has now pretty much caught up. This suggests the international investment cycle is clicking into place and promises to self-sustain the global economic expansion. This should be good for manufacturing industries, New Zealand included."

Kuroda nomination finally confirmed

In Japan, it's finally confirmed that Haruhiko Kuroda is nominated by the government to server a rare second term as BoJ Governor. BoJ executive director Masayoshi Amamiya and Waseda University professor Masazumi Wakatabe are nominated as the to deputies. Hiroshi Nakaso and Kikuo Iwata will be replaced as deputies when their terms expire in mid-March. With the ruling coalition holding a majority, the nominations will be easily approved by both houses.

Looking ahead

UK retail sales is the only feature in European session. Canada will release manufacturing sales and international securities transactions. US will release import price, housing starts and building permits, as well as U of Michigan sentiments.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2464; (P) 1.2487 (R1) 1.2529; More....

EUR/USD's rally continues today and breach of 1.2537 resistance suggests that larger up trend is resuming. Intraday bias stays on the upside. Sustained trading above 1.2537 will confirm and page the way to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2456 minor support will indicate rejection from 1.2537 and turn bias back to the downside for 1.2205 support.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Jan | 55.6 | 51.2 | ||

| 09:30 | GBP | Retail Sales M/M Jan | 0.60% | -1.50% | ||

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0.30% | 3.40% | ||

| 13:30 | CAD | International Securities Transactions (CAD) Dec | 19.56B | |||

| 13:30 | USD | Import Price Index M/M Jan | 0.60% | 0.10% | ||

| 13:30 | USD | Housing Starts Jan | 1.23M | 1.19M | ||

| 13:30 | USD | Building Permits Jan | 1.31M | 1.30M | ||

| 15:00 | USD | U. of Mich. Sentiment Feb P | 95.5 | 95.7 |

GBPUSD – Bullish, Eyes Further Strength

GBPUSD - The pair was seen following through higher on the back of its Wednesday rally during Thursday trading session. Support lies at the 1.4000 level where a break will turn attention to the 1.3950 level. Further down, support lies at the 1.3900 level. Below here will set the stage for more weakness towards the 1.3850 level. Conversely, resistance stands at the 1.4100 levels with a turn above here allowing more strength to build up towards the 1.4150 level. Further out, resistance resides at the 1.4200 level followed by the 1.4250 level. On the whole, GBPUSD looks to move further higher.

US Bond Auction TIPS The Dollar

US Bond Auction TIPS the dollar

A dismal US 30year TIPS auction is weighing on dollar demand as the sagging bid to cover ratio of 2.31 is signalling dwindling investor appetite as inflationary headwinds build. The dollar is lower because no one wants to own US bonds despite the higher yield, knowing the inflationary headwinds will push yields higher and bond prices lower

The market remains nonplussed by the breakdown of FX /Interest rate correlations and while the debate still rages concerning Wednesday dollar sell-off. I think its time to throw textbook economics out the window as well as the so-called interest rate pivot point. G-10 yield differentials are so tiny that traders could care less about differentials as they become increasingly focused on the future outlook of the expanding US deficits and in particular the budget deficit

Another hot inflation reading as PPI showed a substantial gain but provided no bounce to the buck. When real money is taking the dollar to the woodshed and reluctant to own greenbacks in anyway shape or form, it matters little what the Feds are doing or yields for that matter. And by all indications, we could be in the early stages of protracted dollar sell-off.

Equity Markets

Equity investors are in a happy spot as US stock markets carved out their fifth consecutive day of gains. Despite a midday swoon, markets roared back as investors view the uptick in inflation as non-threatening and remain in buy on dip mode as last weeks equity meltdown looks more and more like an illogical outlier than ever.

Oil Markets

After the decent bounce on the back weaker dollar and Khalid al-Falih suggesting no imminent demise of OPEC and non-member compliance. Not unexpected the markets are becoming a bit more position sensitive heading into the weekend. The weaker US dollar has been a significant component driving market sentiment, and with the dollar entering oversold territory at weeks end, we could see short dollar position pared which could negatively impact interday oil prices.

Frankly giving the evolving vital narratives surrounding OPEC compliance vs Shale output I expect the WTI whipsaw to be as active next week as it was this week. But given the overly bearish outlook for the greenback, we may have printed a short-term floor and dips will remain supported.

Gold Markets

There was very little follow through on the much hotter than expected US PPI print which convinced investors to book some profits after gold rallied hard the previous session. A while the weaker USD is underpinning gold prices, the short dollar speculators a bit overextend suggesting the market could pare back US short dollar risk which may temper topside expectations for Gold prices today. Medium-term bullish conviction remains intact given the higher US inflation profile and weaker USD narrative.

Crypto Markets

Bitcoin buyers were back en masse chasing the dream as the fear of missing ( FOMO)out propelled BTC above 10,000. It appears the recent wave or regulatory worries have been tempered as the massive South Korean market could roar back to life as rumours are circulating that Seoul is looking at licencing several exchanges adding a level of credibility and shoring up severely dented investor confidence.

Currency Markets

The Japanese Yen

Talking about FOMO, is there anyone who is not short USDJPY? Of course, “the crowded trade theory” did cross my mind overnight, for second or two, as USDJPY powered back to 106.80 overnight on the Wakatabe headline, before pressing the sell button again. Dovish or not the market cares little about centeral bank policy these days while looking for any and all opportunities to hammer the dollar mercilessly. With very little chance of intervention at these levels, the JPY bulls should continue to have their way near-term.But short-term speculators are a bit stretched so now is not the time to get greedy.Let’s see what fortunes next week brings.

The Euro

It looks like the grind higher is back in fashion, and the upticks have been relentless over the past 24 hours. But unlike the recent test of 1.25 positioning is much lighter so we could punch higher as traders continue moan over not buying the dips to the low 1.22’s

The Malaysian Ringgit

Powerful bullish signals are falling on deaf ears as investors are far and few between due to Chinese Lunar New Year and quite frankly it’s not worth paying the holiday liquidity premiums to put on risk. Very little offshore interest today so expect the market to remain quiet.

Gold Takes Breather After Strong Gains

Gold prices is trading sideways in the Thursday session, after surging higher on Wednesday. Currently, the spot price for an ounce of gold is $1351.30, up 0.05% on the day. On the release front, PPI gained 0.4%, matching the forecast. Core PPI also gained 0.4%, beating the estimate of 0.2%. Both indicators rebounded after declines in the previous month. Unemployment Claims climbed to 230 thousand, just above the estimate of 229 thousand. Manufacturing data was mixed. The Empire State Manufacturing Index continues to slow down, and dropped to 13.1, missing the estimate of 17.7 points. The Philly Fed Manufacturing Index rose to 25.8, easily beating the estimate of 21.5 points. On Friday, the US releases key housing and consumer confidence numbers.

The US dollar has sagged against the major currencies, and gold has jumped on the bandwagon. On Thursday, gold jumped 1.6% on disappointing retail sales reports. Concerns of high inflation was a catalyst for the market sell-off last week, and fears of a resumption in the downward spiral are weighing on the dollar. If investors react negatively and ditch the markets yet again, safe-haven assets like gold will likely be the big winners. Gold prices were down in the first half of February, but gold has recovered these losses, after posting strong gains of 2.7% this week. US fundamentals remain solid, as the US economy is showing strong expansion, the labor market remains at capacity, and inflation levels are moving higher. This has led some analysts to attribute the recent sag in the US dollar to technical factors rather than fundamental reasons.

The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, as he started his new position last week. Powell sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed’s hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time. Currently, the Fed is planning three hikes this year, but that could change to four or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion.

Pound Higher As Sentiment Remains Negative On Greenback

The British pound continues to head higher this week. In Thursday’s North American trade, GBP/USD is trading at 1.4067, up 0.48% on the day. On the release front, there are no British events on the schedule. In the US, PPI gained 0.4%, matching the forecast. Core PPI also gained 0.4%, beating the estimate of 0.2%. Both indicators rebounded after declines in the previous month. Unemployment Claims climbed to 230 thousand, just above the estimate of 229 thousand. On Friday, the US releases key housing and consumer confidence numbers. The UK will release Retail Sales.

The pound has posted winning sessions every day this week, and has continued the upward trend on Thursday. GBP/USD has gained 1.7% this week, and punched above the 1.41 line earlier on Thursday. The pound posted strong gains on Wednesday, as US consumer spending reports were weaker than expected. Still, US fundamentals remain solid, as the US economy is showing strong expansion, the labor market remains at capacity, and inflation levels are moving higher. This has led some analysts to attribute the recent sag in the US dollar to technical factors rather than fundamental reasons.

With US inflation indicators pointing higher in January, the Fed will be reevaluating its projection for rate hikes in 2018. Currently, the Fed is planning three hikes this year, but that could change to four, or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion. The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, as he started his new position last week. Powell sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed’s hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

Italian Elections: Europe’s and the Common Currency’s Next Big Test?

Italy will be heading to the polls to elect a new national government on March 4. This is widely viewed as the common currency's - more widely the eurozone's and Europe's - next major risk event. The result of the elections is far from known, with a number of possible outcomes being at play and populist-perceived forces enjoying popularity. The euro is expected to come under intense selling pressure should for example the Five Start Movement find itself ruling the country; an outcome that doesn't look that likely at the moment. However, the sell-off from such an outcome is likely to be short-term in nature, or at least this is the argument brought forward, as despite the initial uncertainty, at the end of the day there might not be much of a change in the eurozone's third largest economy.

At the beginning of last year, the political landscape in the eurozone was rife with events posing downside risks to the euro, one of those being the French presidential elections. However, to the surprise of many, the bloc in large part moved against the "trend" that seemed to be evolving following the Brexit referendum and the US presidential election. This was seen as euro-supportive and led to a strong rally that eventually saw the common currency finishing last year 14.1% higher versus the greenback.

The themes of populism, immigration and social inequality that have dominated attention and led to heated debates in major elections from the recent past - among them, those mentioned previously - are making a comeback in the upcoming Italian elections. Employment opportunities are one of the hottest topics, with Italy's unemployment rate standing at around 11%. This is one of the highest in the eurozone. The youth unemployment rate though is what is truly painting a dire picture for the country, exceeding 30%. The lack of opportunities is also contributing to "brain drain" issues, with talented youth leaving the country to make a living elsewhere, casting clouds on the outlook for growth; a similar situation is at play in Greece.

Italian election polls are showing no individual party or party coalitions securing a winning majority, and this is attributed to the country's new electoral system, a system that was dubbed as "complicated" even by Partito Democratico (PD - Democratic Party), the very party that introduced it.

The anti-establishment Movimento 5 Stelle (M5S - Five Star Movement) is the strongest single party heading into the election, polling at around 28%. However, this is well below the 40% threshold that is required to secure a governing majority in both chambers, the parliament and the Senate. The new electoral law favors coalitions, and this comes to the detriment of M5S, whose officials have repeatedly stated that they do not intend to enter into a deal with another party as it is believed that any concessions to forge a coalition would alienate their supporters; though one might argue that in politics, statements and actions don't always align. Other parties though have formed coalitions, with the latest polls showing them close to the 40% threshold.

Closest to that is the centre-right coalition, polling at 37%. This is made up of Berlusconi-led Forza Italia (FI - Forward Italy), Lega Nord (LN - Northern League) and Fratelli d'Italia (FdI - Brothers of Italy). It should be mentioned that if these forces take power, former prime minister Silvio Berlusconi cannot again assume the post of PM due to a 2013 tax fraud conviction - the party would have to decide who will take the reins in case of that outcome.

An amazing paradox is in existence: Berlusconi - his party included - is pro-Europe and pro-euro, while LN is anti-euro and is considered a populist party; to enhance reader understanding, LN could perhaps be viewed as Italy's equivalent of Marine Le Pen's Front National (National Front). Berlusconi's influence and him taking a "euro-friendly" stance on important issues that have to do with the eurozone and more widely the EU, is rendering a government involving LN as not something that markets - the euro - should view as much of a threat. In essence, Berlusconi is seen as acting as a buffer to the rise of populism. Lastly, it is worth mentioning that some analysts are saying that right-wing votes tend to be underestimated in polls due to a so-called "shy-factor". Past Italian elections give credit to this view, which if proved right, then the centre-right might secure the desired majority.

Regarding the centre-left coalition, that is overwhelmingly led by the ruling PD and is polling at 27%. On its own, the PD is the second biggest party after M5S (23% versus close to 28%), though it's been losing support as we're getting closer and closer to election day. The PD has traditionally been a pro-European party.

A hung parliament and a probable grand coalition is the most likely outcome and the one preferred by markets. The potential scenarios though are numerous and delving into them might pointlessly detract from the essence - there could also be repeated failed attempts to form a government, resulting in fresh elections. It would be fruitful and interesting though to go through the one outcome (despite it not being the most probable) that undoubtedly has the higher odds of leading to the greatest market turbulence and one can extrapolate beyond that and more or less figure out the market reaction in case of an alternative scenario.

A government led by M5S would qualify as the outcome spurring the most extreme market movements, likely resulting in considerable euro weakness versus other currencies. Is that justified though? The argument being pushed forward is that such a reaction would provide opportunities to buy the dip for those investors realizing that such a behavior - shorting the euro - would merely constitute a market overreaction. The reasoning being that M5S has altered its rhetoric on many of the things it was originally against, moving towards a more moderate stance. Perhaps more importantly, the party no longer wants to hold a referendum on Italy's membership in the single currency.

At the end of the day, the Italian elections could deliver more of the same. The real risk for Italy and the euro might not be March 4th, but a widespread crisis later on should those in power keep on kicking the can down the road, in the meantime allowing problems to grow up to the point they could not be longer be managed. Growth is picking up in Italy but is still far from inspiring (not far above 1.5% on an annual basis in Q4), Italian public debt is high, bureaucracy is stifling entrepreneurship and investment, and non-performing loans continue to haunt Italian banks despite efforts to improve the situation.

Another event that could incentivize market participants to short the euro and deserves mention is Germany's Social Democratic Party (SPD) disapproving entering into a coalition to form a government with Chancellor Merkel's conservative bloc. The SPD's voting process begins on February 20 and the results could be known around the time the Italian elections take place. The odds are in favor of a ratification of the deal that was struck with Merkel's conservatives.