Sample Category Title

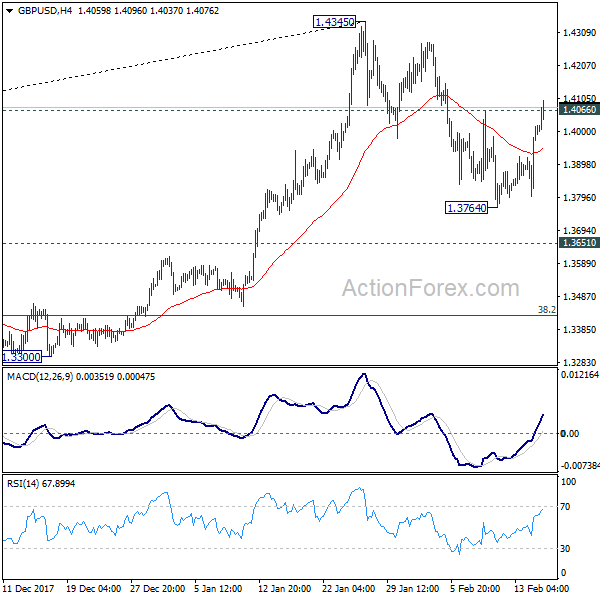

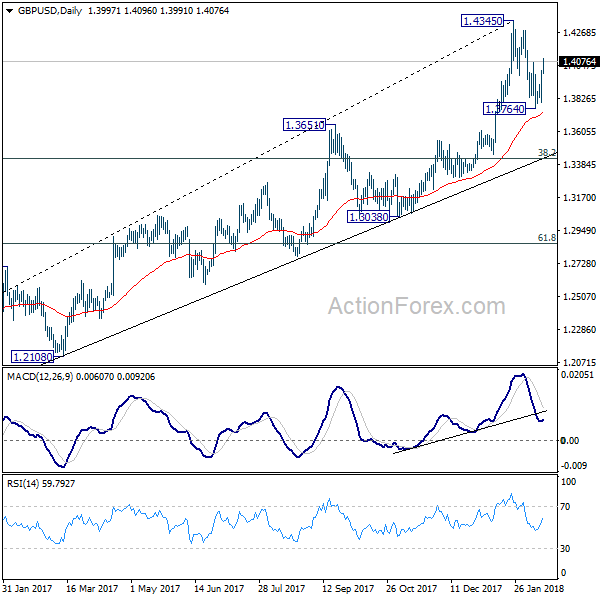

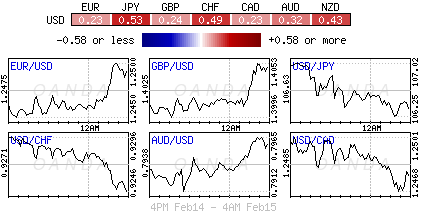

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3859; (P) 1.3938; (R1) 1.4075; More.....

GBP/USD's break of 1.4066 minor resistance suggests that pull back from 1.4345 has completed at 1.3765 already. Intraday bias is turned back to the upside for retesting 1.4345 first. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105).

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

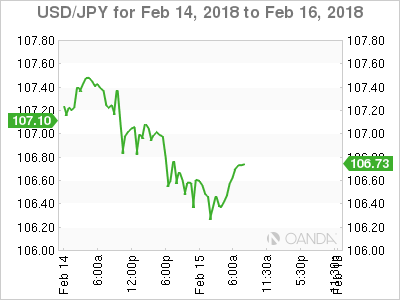

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.52; (P) 107.21; (R1) 107.69; More...

Intraday bias in USD/JPY remains on the downside at this point. Right now, we'd still look for strong support around 106.48 to bring rebound. But break of 107.89 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will stay bearish. Firm break of 106.48 will extend medium term fall from 118.65 to 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

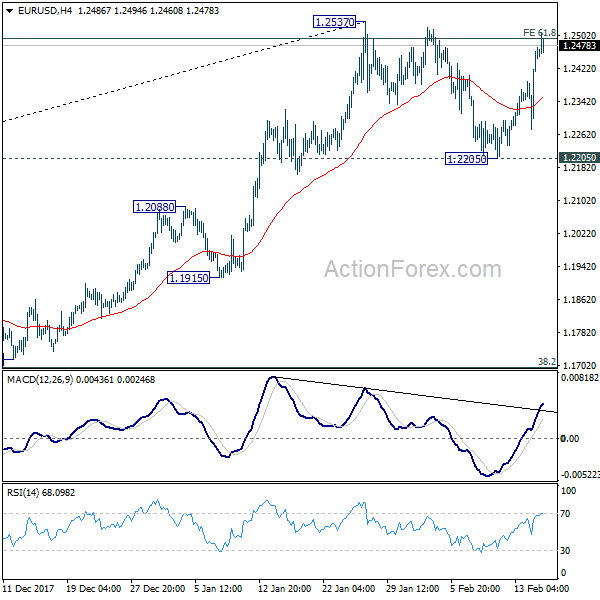

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2328; (P) 1.2397 (R1) 1.2518; More....

Intraday bias in EUR/USD remains on the upside for 1.2537 high. As noted before, pull back from there should be completed at 1.2205 already. Decisive break of 1.2537 will resume larger up trend and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. In any case, for now, as long as 1.2205 support holds, outlook will remain bullish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Remains the Weakest One after Mixed Economic Data

Dollar remains the weakest one and is under broad based selling pressure. Mixed economic data from the US provides little support to the greenback. Headline PPI rose 0.4% mom, 2.7% yoy in January, versus expectation of 0.4% mom, 2.5% yoy. Core PPI rose 0.4% mom, 2.2% yoy, versus expectation of 0.2% mom, 2.1% yoy. Empire state manufacturing index dropped to 13.1 in February, below expectation of 18.0. Philly Fed survey rose to 25.8, above expectation of 21.6. Initial jobless claims rose 7k to 230k in the week ended February 10. 1.2537 is a key level to watch in EUR/USD today.

EU to remove punishment clause from Brexit draft

It's reported that EU official have removed a so called "punishment clause" from a draft regarding Brexit transition arrangements. The clause is about having UK to abide by all existing rules and regulations of the EU during the transition. If such request is not respected, there would be specific sanctions. On the other hand, a number of Conservatives were angered as UK will not have any say on new results approved during the period. It's believed that the requirements would be replaced by less tough-sounding languages.

From Eurozone, trade surplus widened to EUR 23.8b in December.

Government to submit BoJ Governor nomination tomorrow

In Japan, it's reported that the government is finally going to submit the nominations for the next BoJ Governor and Deputies tomorrow. Haruhiko Kuroda remains the front runner to get a rare second term as BoJ Governor. BOJ Executive Director Masayoshi Amamiya, could succeed Hiroshi Nakaso as Deputy. That should give enough time for both House to approve the appointment, before Kuroda's term ends in April. The Deputies terms will end in mid-March.

From Japan machine orders dropped -11.9% mom in December. Industrial production was revised up to 2.9% mom in December

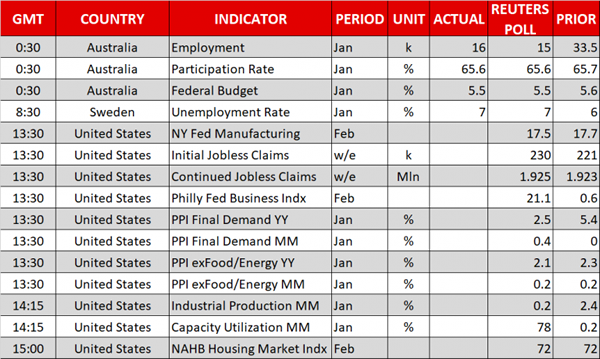

Elsewhere, Australia employment grew 16k in January, unemployment rate dropped 0.1% to 5.5%. Australia consumer inflation expectation rose 3.6% in February.

FX trading volume surged

According to a major FX settlement services provider CLS, activity in FX trading surged at the start of the year. CLS's average daily traded volume rose to USD 1.8T in January, 24% up from a year ago, and 15.6% up from December. In the four days from February 5 to 8, volume jumped a further 14% over January. The surge in volume is seen by some as the result of Dollar's down trend resumption.

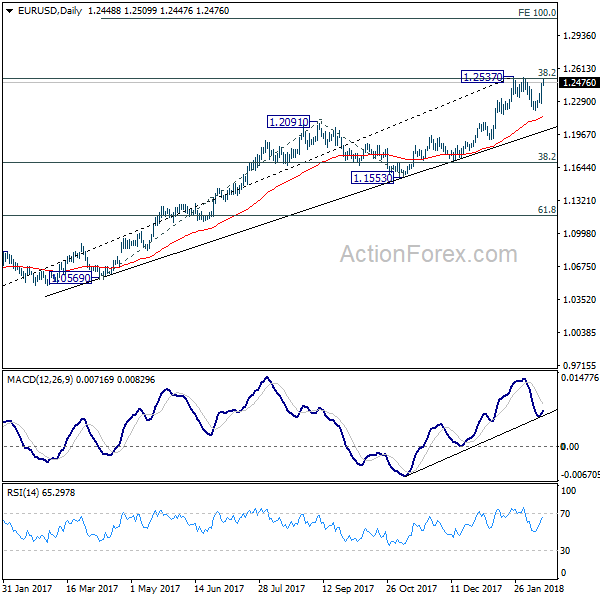

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2328; (P) 1.2397 (R1) 1.2518; More....

Intraday bias in EUR/USD remains on the upside for 1.2537 high. As noted before, pull back from there should be completed at 1.2205 already. Decisive break of 1.2537 will resume larger up trend and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. In any case, for now, as long as 1.2205 support holds, outlook will remain bullish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Dec | -11.90% | -2.30% | 5.70% | |

| 00:00 | AUD | Consumer Inflation Expectation Feb | 3.60% | 3.70% | ||

| 00:30 | AUD | Employment Change Jan | 16.0K | 15.2K | 34.7K | 33.5K |

| 00:30 | AUD | Unemployment Rate Jan | 5.50% | 5.50% | 5.50% | 5.60% |

| 04:30 | JPY | Industrial Production M/M Dec F | 2.90% | 2.70% | 2.70% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | 23.8B | 22.6B | 22.5B | 22.0B |

| 13:30 | USD | Empire State Manufacturing Feb | 13.1 | 18 | 17.7 | |

| 13:30 | USD | Initial Jobless Claims (10 FEB) | 230K | 227k | 221k | 223K |

| 13:30 | USD | PPI M/M Jan | 0.40% | 0.40% | -0.10% | |

| 13:30 | USD | PPI Y/Y Jan | 2.70% | 2.50% | 2.60% | |

| 13:30 | USD | PPI Core M/M Jan | 0.40% | 0.20% | -0.10% | |

| 13:30 | USD | PPI Core Y/Y Jan | 2.20% | 2.10% | 2.30% | |

| 13:30 | USD | Philadelphia Fed Business Outlook Feb | 25.8 | 21.6 | 22.2 | |

| 14:15 | USD | Industrial Production M/M Jan | 0.20% | 0.90% | ||

| 14:15 | USD | Capacity Utilization Jan | 78.00% | 77.90% | ||

| 15:00 | USD | NAHB Housing Market Index Feb | 72 | 72 | ||

| 15:30 | USD | Natural Gas Storage | -119B | |||

| 21:00 | USD | Net Long-term TIC Flows Dec | 50.3B | 57.5B |

Canadian Dollar Gains Ground After Dismal US Retail Sales

The Canadian dollar has paused on Thursday, after posting strong gains a day earlier. Currently, USD/CAD is trading at 1.2491, down 0.01% on the day. On the release front, Canada releases ADP Non-farm Employment Change. In the US, there are a host of indicators, highlighted by PPI and Core PPI reports for January. Both indicators are expected to record gains after declining in the December readings. The US will also release key manufacturing reports and unemployment claims. On Friday, the US releases key housing and consumer confidence numbers. Canada will publish Manufacturing Sales.

It's been a rough February for the Canadian dollar, but the currency jumped on the bandwagon on Wednesday, as the US dollar posted broad losses. The Canadian currency posted its best one-day performance in 2018, gaining 0.09% against the greenback. The US dollar sagged as investors focused on poor retail sales reports in January. Retail Sales was flat at 0.0%, short of the estimate of 0.5%. Core Retail Sales declined 0.3%, well off the forecast of +0.2%. On the inflation front, CPI jumped 0.5%, above the estimate of 0.3%. Last week's market sell-off, which sent the US dollar higher against other currencies, was triggered by fears of higher inflation. This strong CPI reading has raised concerns that investors could again lose their risk appetite and send the Canadian dollar lower.

Will the recent volatility in the markets affect interest rate policy in the US? Currently, the Fed has projected three hikes this year, but that could change to four or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion. The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, when he started his new position last week. Powell sought to send a reassuring message earlier this week, declaring that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed's hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

Dollar Dives on Confidence, No Support from Fundamentals

Thursday February 15: Five things the markets are talking about

U.S bond yields have backed after an unexpected rise in U.S consumer inflation to its fastest pace in a year - the core's +1.8% y/y print yesterday was higher than expected, but still below the Fed's +2% target - making it more likely the Fed will raise interest rates three or more times this year. But, higher U.S rates have not been able to make the U.S dollar more attractive.

The dollar remains under pressure, building on yesterday's slide in the Euro session, as the market seems to be losing confidence in the long-run state of the U.S economy.

The Dollar Index is down -0.5% and poised to log another three-year low if the decline persists as we head to U.S session open.

Without any new positive U.S demand or supply shocks that could change the landscape for the country's economy, it's easy to see the weak dollar story persisting.

For the dollar to rise with Treasury yields, which it has not been doing this year, there needs to be a return in relative confidence over the medium-term U.S.

Also yesterday, January retail sales fell unexpectedly in their biggest drop in 11- months, declining -0.3%, raising new concerns about the U.S economy as a weaker sale print will lead to lower expectations for Q1 GDP growth.

1. Stocks edge higher

The global stock rally is marching ahead as investors take in stride a jump in sovereign yields.

In Japan, the Nikkei posted a solid rise despite a stronger yen (¥106.31). The index ended up +1.5% overnight, after tumbling to a four-month low on Wednesday. The broader Topix advanced +1.0%.

Down-under, Australia's S&P/ASX 200 rebounded +1.2% as the stock index's energy component rallied +2.4% to reverse some of this month's decline.

In a shortened session ahead of the Lunar New Year holiday, Hong Kong's Hang Seng Index jumped +2%. Its rise of +5.4% this week has erased +50% of last week's decline, its biggest fall in a decade.

Note: China, South Korea, Taiwan, Vietnam markets were all closed.

In Europe, regional indices continue their ascent higher, tracking another positive session in Asia and on Wall Street yesterday. The French CAC is +1% higher following earnings from a host of Index components. The Swiss SMI is underperforming after Nestle reported mixed results.

U.S stocks are set to open in the 'black' (+0.8%).

Indices: Stoxx600 +0.9% at 378.0, FTSE +0.7% at 7264, DAX +0.9% at 12455, CAC-40 +1.6% at 5248, IBEX-35 +1.3% at 9808, FTSE MIB +1.1% at 22687, SMI +0.2% at 8924, S&P 500 Futures +0.8%

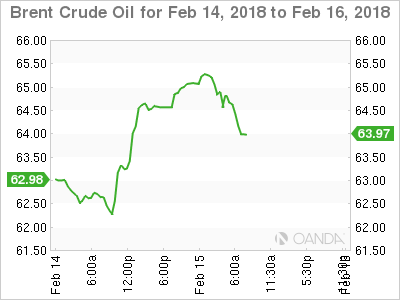

2. Oil rises on Saudi commitment to withhold output, gold higher

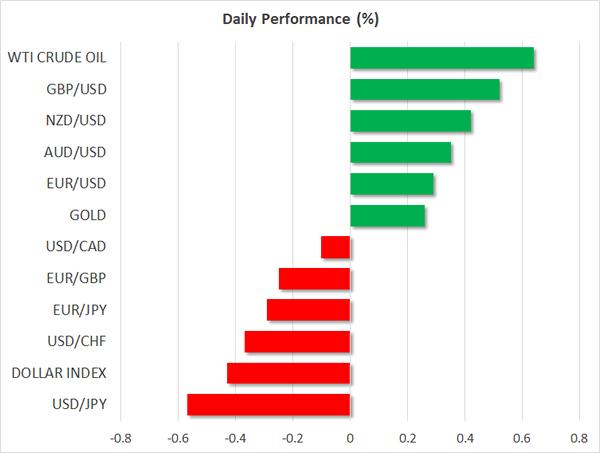

Oil prices have rallied +1% overnight to extend their gains from yesterday's session, lifted by a weak dollar and Saudi comments that it would rather see an undersupplied market than end a deal with OPEC.

Brent crude futures are at +$64.99 a barrel, up +63c, or +1%, extending Wednesday's +2.6% climb. U.S West Texas Intermediate (WTI) crude futures are up +83c, or +1.4%, from Wednesday's close at +$61.43 a barrel, adding to its +2.4% gain.

Oil markets have got a push from comments by Saudi Arabia, voicing support for output cuts backed by OPEC and other producers including Russia since 2017 in an effort to tighten the market and prop up prices.

OPEC Secretary General Barkindo said that preliminary data for January points to high compliance of cuts by producers.

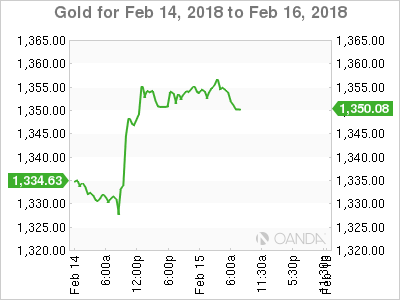

Ahead of the U.S open, gold prices have edged a tad higher as the dollar weakens and investors' bank on the precious metal as a hedge against inflation. Spot gold is up +0.3% at +$1,354.34 an ounce and is heading for a fourth consecutive session of gains.

3. Sovereign yields rise

The yield on U.S 10-year Treasuries is nudging closer to +3%, continuing its steady advance from last year's low of +2.01% in September.

Following this weeks U.S inflation data, and the potential implications that it has for the pace of Fed rate increases this year, the market will be closely scrutinize speeches later today by ECB policy makers to see whether the recent market turmoil will convince them to ease off plans to taper their bond purchases.

Note: Fed-fund futures show a +21% chance of at least four interest-rate increases by year-end, compared with +17% earlier this week.

In Germany, the 10-year Bund yield has gained +1 bps to +0.77%, the highest in more than two years on the biggest gain in a week.

4. Dollar dives again

The USD remains on the defensive despite higher U.S yields -the currency is usually highly correlated to short-term rates. Market seems to be reacting to concerns over weak U.S policies and/or diverging central bank policies as both the BoJ and ECB could begin tightening monetary policy.

The EUR/USD (€1.2467) probed the upper end this week's and year range as the pair re-tested the €1.25 handle. Sterling (£1.4042) is a tad higher initially aided by reports that the E.U Commission was looking to ease the Brexit transition conditions. However, the E.U later refuted the reports. The pound is also finding support not only from the dollar's weakness, but also a perceived higher probability that the current U.K government will serve its full five-year term.

USD/JPY (¥106.69) continues to trade atop of its 15-month lows as the pair probed below ¥106.20 overnight. Japan's Finance Minister Aso comments that the yen's strength is not abrupt enough to require intervention supported the yen's rally.

In cryptocurrencies, bitcoin (BTC) is moving back toward $10,000, up +6% on the day at +$9,840 - the price had slumped some -70% in the past six weeks.

5. Crisis in the Northern Ireland

U.K PM Theresa May is facing a political crisis in Northern Ireland as the DUP, who are part of the government's coalition, have stated there was "no prospect" of a power sharing deal and suggested a return to direct rule.

This crisis threatens to throw the Good Friday agreement into jeopardy and would be a significant blow to P.M May's authority as she attempts to agree to a crucial Brexit deal over the Irish border.

USDJPY Bearish in Control Below 106.84

The U.S dollar has fallen to its lowest trading level against the Japanese yen since November 2016, following much better than expected monthly U.S CPI inflation figures. The USDJPY currently trades around the 106.50 level, after the pair found support during the European trading session around the 106.17 technical level. Moving into today's U.S session, traders will be focused on the release of January PPI Inflation and Industrial Production numbers from the American economy.

The USDJPY pair is heavily intraday bearish while price-action trades below the 106.84 level, key intraday support is now found at the 106.17 and 105.50 levels.

Should the USDJPY pair start to trade above the key 106.84 level, buyers may push price-action back towards 107.29 and 107.91 levels.

GBPUSD Buyers Targeting 1.4100 Level

The British pound has continued to press higher against the greenback during the European trading session, with price-action surging towards the 1.4078 technical level. The GBPUSD pair is currently trading around the 1.4050 area, as traders start to book intraday profits from overextended technical levels. Moving into the U.S trading session, the next upside barrier for buyers is the 1.4110 level, whilst key daily technical support is situated around the 1.4000 region.

The GBPUSD pair retains an intraday bullish bias whilst price-action clearly trades above the 1.4000 level, further upside towards the 1.4110 and 1.4199 levels appears possible.

Should GBPUSD price-action move below the 1.4000 level for an extended period, sellers will likely test towards the 1.3939 and 1.3892 levels.

Dollar Holds Weak Amid Debt Concerns, European Stocks Extend Gains

Here are the latest developments in global markets:

FOREX: Stronger-than-expected consumer prices on Wednesday failed to support the dollar, pushing it even lower on Thursday despite markets increasing their expectations on the number of rate hikes delivered by the Fed. Investors seem to be cautious as they worry that the US national debt could surge significantly on the face of massive tax cuts and the government's two-year spending plan approved last week. Worse-than-expected US retail sales also dampened sentiment on consumption. Dollar/yen was last trading at 106.46, near today's fresh 15-month low of 106.16 (-0.50%), while the dollar index stood weak at 88.72 (-0.44%). Euro/dollar managed to gain ground, rising slowly to a two-week high of 1.2509 (+0.26%), although political news out of Germany signaled yesterday that the relationship between Merkel's Conservatives and their likely coalition partners, the SPD, might not be as harmonious as in the past. Uncertainties around the upcoming Italian elections were also weighing on the pair. Pound/dollar was getting love as well, crawling up to a 1 ½-week peak of 1.4076 (+0.46%). Dollar/loonie was flat at 1.2484.

STOCKS: European equities were broadly in the green, with the pan-European Stoxx 600 trading higher by 1.0% at 0940 GMT, recording a one-week high of 378.37, and the blue-chip Euro Stoxx 50 being up by 1.3%. The UK's FTSE 100, German Dax and CAC 40 were up by 0.6%, 1.1%, and 1.7% respectively, with the latter leading the gains among major blue-chip European indices. Airbus (up 10.4%) was the best performing stock within the CAC 40, as well as the Stoxx 600. The airspace firm was boosted after delivering an earnings beat. Food and drink company Nestlé declined notably (down 2.3%), leading the losses in the Swiss SMI (up 0.4%), which underperformed relative to other blue-chip indices in the continent. Nestlé's fall was spurred after it reported that last year's organic growth was the weakest since it began recording the measure more than two decades ago. Old Mutual (up 4.8%) led gains in the FTSE 100. A large part of the bank and insurance firm's revenues are made up in South Africa. Political developments in the country – leading to the resignation of President Jacob Zuma – have considerably boosted the rand, this being a positive for Old Mutual. Miner Anglo American (up 2.8% – also a FTSE constituent) was on the rise for similar reasons.

COMMODITIES: Oil prices remained higher on the day, despite giving up part of earlier gains. WTI and Brent crude were up by 0.6% and 0.2% respectively, trading at $60.97 and $64.47 per barrel. Gold traded higher by 0.25%, at $1,353.99 an ounce. The falling greenback is seen as supportive for these dollar-denominated commodities.

Day ahead: US initial jobless claims, PPIs & industrial production gather attention

US data will remain in the spotlight during Thursday's European afternoon, bringing new challenges to the greenback which has been under severe pressure this week.

At 1330 GMT a bunch of data will be available out of the US for review including initial jobless claims, producer prices, the New York Fed manufacturing index and the Philadelphia Fed's business index.

The number of people applying for unemployment benefits is expected to inch up to 230,000 in the week ending February 9 compared to 221,000 seen in the preceding week. However, the measure continues to hold below 300,000 since March 2015, flagging that the US labor market keeps operating under healthy conditions.

Th New York Fed's Empire State manufacturing index and the Philadelphia's Fed manufacturing index which measure business conditions in the aforementioned states are expected to stand slightly weaker in February but still remain at robust levels.

Producer prices, which might add further evidence on inflation, are projected to slow down on yearly terms in January, with the headline index anticipated to edge down by 0.1 percentage points to 2.5% y/y and the core equivalent which excludes volatile items expected to ease to 2.1% y/y. On a monthly basis though, both measures are said to post a strong rebound, rising by 0.4% and 0.2% respectively, following a pullback in December.

Later on, the readings on US industrial production will be published at 1415 GMT. Forecasts are for industrial output to rise at a slower pace in January, driving the monthly growth rate down from 0.9% to 0.2%.

Results from a housing survey conducted by the National Association of Home Builders (NAHB) will come to light a few minutes later (at 1500 GMT), probably showing no change in the outlook of US home sales in February.

Meanwhile, Canada will see the release of the ADP nonfarm employment report at 1330 GMT.

Regarding public speeches, Sabine Lautenschlager, an ECB board member, is scheduled to give a speech at Dutch Banking Day 2018 at 1200 GMT. Norway's central bank governor, Oystein Olsen, will be giving a keynote speech at 1700 GMT. Lastly, Bank of Canada Deputy Governor Lawrence Schembri will be talking at 1830 GMT.

In equities, companies releasing quarterly results will be attracting attention.

Zuma Conclusion Lifts Rand To Near 3-Year High

After months of ongoing speculation, the overnight climax with Jacob Zuma resigning from his position as President of South Africa has lifted the Rand to its highest level since March 2015.

The Rand has now advanced by nearly 2.4% against the Dollar this week, and has strengthened against all of the G10 currencies throughout the same period,at time of writing. While ongoing Dollar weakness across the currency markets has supported gains in the Rand, the fact that it has managed to also advance against the G10 currencies suggests that the confirmation of Zuma vacating his position has benefited overall investor sentiment towards South Africa.

The Zuma presidency was masked by multiple layers of political risk;confirmation of Zuma stepping aside should help the Rand continue to climb to levels not seen since the days of the Federal Reserve preparing the financial markets for the normalization of US interest rate policies.

It is quite possible that the Dollar will weaken to below 11 against the Rand for the first time since December 2014 over the coming weeks.

Euro and Yen benefit as slide in Dollar resumes

Moving away from the changing political situation in South Africa, the other major financial story ofthe week has been the resumption of Dollar selling across the currency markets. Investors selling the Dollar have contributed heavily towards the Japanese Yen advancing by 2% this week, with the USDJPY reaching its lowest level since 2016.

In reference towards why traders are becoming encouraged to resume selling the Dollar, it is likely linked to more clarification being provided following the EU GDP release this week, that showedthe distance between economic recovery in the United States and other developed economies has continued to narrow.

The United States is basically not on a pedestal of its own anymore when it comes to conversations of stronger economic growth and increased interest rates. This provides an opportunity for traders to price in yield into currencies elsewhere.

Confirmation that the European Union economy grew at its fastest pace in a decade last year at 2.5%, is ironically its best performance since the global financial crisis began to unfold in 2007. It also makes it inevitable that the European Central Bank (ECB) will at some point need to prepare investors for an eventual increase in EU interest rates