Sample Category Title

Crypto Market Completes Initial Rebound, Nearing Key Resistance

Market picture

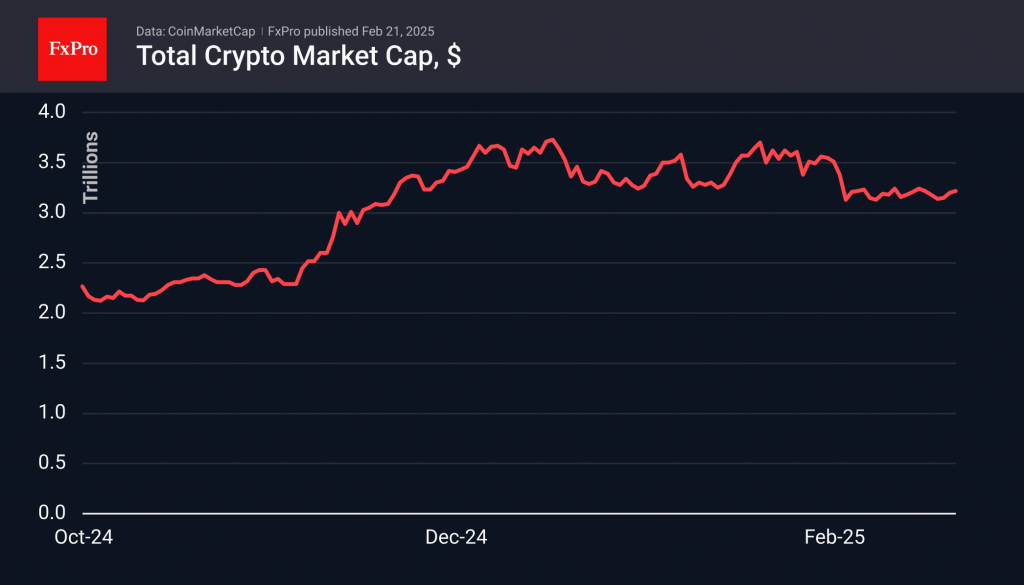

The cryptocurrency market has added 1.3% in the last 24 hours to $3.24, approaching the upper boundary of the consolidation range after the collapse in early February. Only the ability to rise above $3.3 trillion would signal an exit from consolidation and be a prologue for a return to the $3.50 area or a move to all-time highs near $3.70.

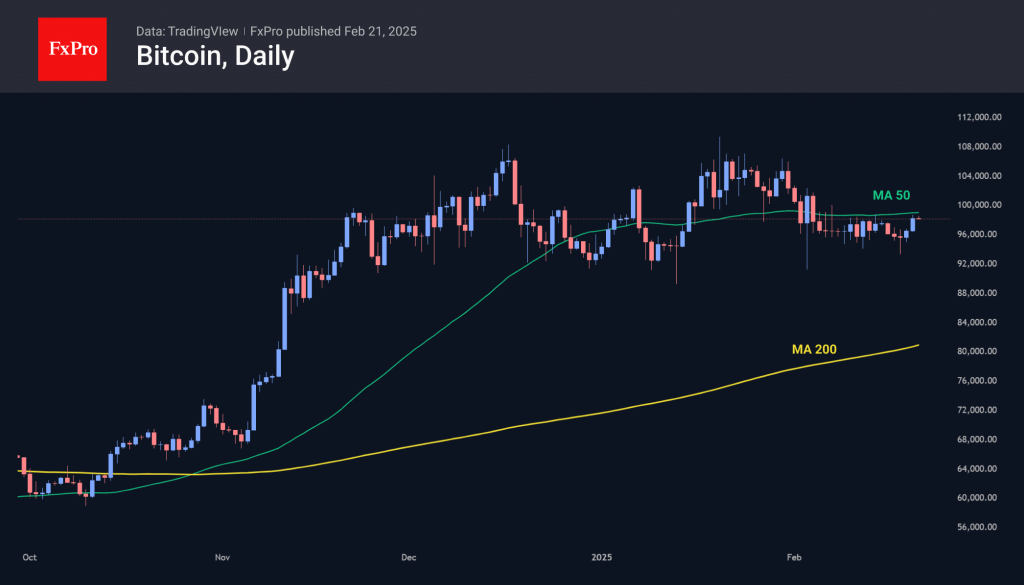

Bitcoin has risen to $98,000, once again trying to break above the 50-day moving average. As with the crypto market, Bitcoin has found enough buyers on dips and has done the easy part with a return to meaningful resistance levels. Only a confident move higher will mark the start of a new rally phase.

News Background

JPMorgan notes that the observed weakening of institutional demand for Bitcoin and Ethereum futures on the CME is a bearish signal for the near term. The lack of positive catalysts and fading price momentum are the reasons.

QCP Capital records demand for high delta call options on Bitcoin, indicating growing expectations of strong price growth in the future. Implied volatility has shifted in favour of calls across all maturities, indicating bullish market positioning.

Trump linked Bitcoin’s highs to his policies. According to him, BTC has set new records because everyone knows he is committed to making the US the crypto capital of the world.

Stacks platform CEO Muneeb Ali said most second-tier bitcoin-based projects will disappear within three years. He said the market is evolving in a highly competitive environment, and enthusiasm around L2 solutions has waned markedly.

The CBOE has filed a Form 19b-4 proposal with the SEC asking it to approve staking in 21Shares’ Ethereum-based ETF. The NYSE previously filed a similar proposal for Grayscale’s Ethereum-ETF.

The SEC has softened its stance on regulating cryptocurrencies and DeFi. The regulator filed a motion to withdraw an appeal of a ruling limiting the application of securities laws to users of cryptocurrencies and DeFi services.

Ten companies have been approved to issue stablecoins in the European Economic Area (EEA) under MiCA rules. Tether, the USDT issuer, is absent from the list. Circle, the issuer of USDC, the main competitor of USDT, received the right to issue stablecoins in the EEA back in July.

Solana’s (SOL) annual inflation rate rose 30.5% after the implementation of a new fee allocation model on the platform (SIMD-0096), Blockworks notes. Recent scandals surrounding LIBRA, and previously TRUMP, MELANIA, BARRON and HAWK, have undermined Solana’s reputation and increased pressure on the altcoin market.

USD/JPY Recovers After Dropping Below 150 Yen per Dollar

As the USD/JPY chart shows:

→ Yesterday, the pair fell below the psychological level of 150 yen per dollar.

→ However, today it staged a strong recovery, rising back above this level.

The yen weakened following the release of Japan's inflation data. According to Forex Factory, the National Core CPI increased by 3.2% year-over-year (forecast: 3.1%, previous: 3.0%).

According to Reuters:

→ The 19-month high in CPI strengthens expectations of further interest rate hikes in Japan.

→ The yen is weakening as Bank of Japan Governor Kazuo Ueda stated that the central bank may step up government bond purchases if long-term interest rates rise.

Can USD/JPY Continue to Rise?

USD/JPY Technical Analysis

On 12th February, we noted that key highs and lows over the past three months formed an ascending channel, with the 154 yen per dollar level acting as a resistance barrier.

Indeed, since then, bulls have failed to sustain levels above 154 yen per dollar (as indicated by the arrow), leading to a decline below the lower boundary of the blue channel after a brief rebound on 18th February.

As a result, the former support at the lower boundary of the blue channel may now act as resistance around 151.3 yen per dollar, reinforcing the relevance of the descending channel (marked in red).

The trajectory of USD/JPY today could be significantly influenced by the release of the US Flash Manufacturing PMI and Flash Services PMI indices at 16:45 GMT+2.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

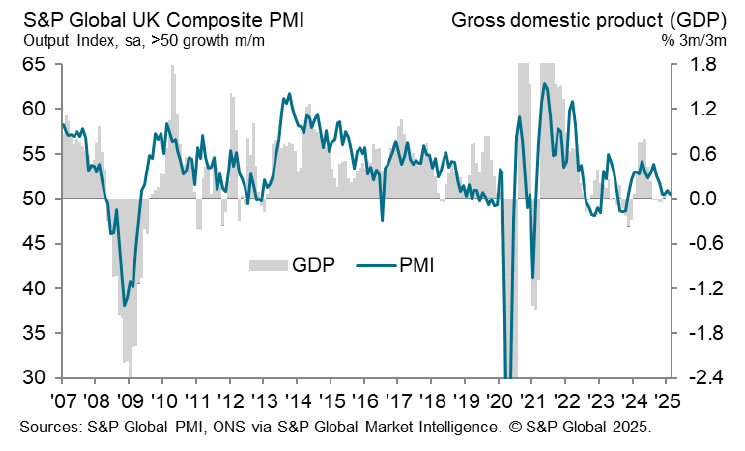

UK PMI composite dips to 50.5, stagflation dilemma for BoE

UK’s PMI Manufacturing dropped from 48.3 to 46.4 in February, a 14-month low. PMI Services edged up slightly to 51.1 from 50.8, while Composite PMI dipped to 50.5 from 50.6, indicating minimal overall growth.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted that business activity remained "largely stalled" for the fourth straight month, with job losses accelerating amid declining sales and rising costs. He cautioned that the combination of stagnant growth and mounting price pressures is creating a "stagflationary environment," presenting a "growing dilemma" for BoE.

A primary driver of inflationary pressure is the increase in firms raising prices to offset rising staff costs tied to the National Insurance hike and minimum wage increase announced in the autumn Budget. However, these same fiscal measures have also exacerbated job cuts, with employment falling at its fastest pace since the global financial crisis, excluding the pandemic period.

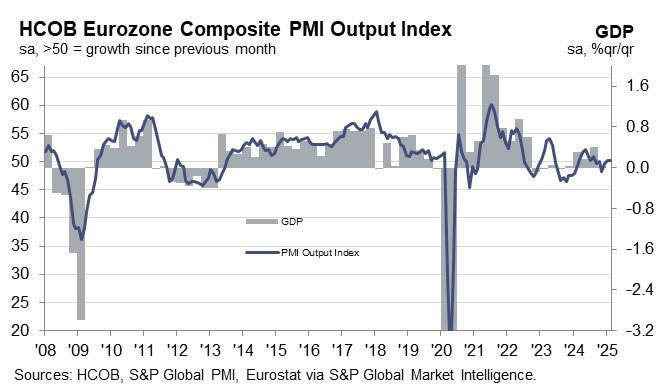

Eurozone PMI manufacturing rises to 47.3, but services falls to 50.7

Eurozone Manufacturing PMI improved from 46.6 to 47.3 in February, a nine-month high. However, Services PMI declined to 50.7 from 51.3, dragging Composite PMI flat at 50.2, indicating near stagnant overall growth.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted that services sector price pressures remain elevated, creating complications for the ECB ahead of its next meeting. Persistent wage growth and rising input costs in manufacturing, driven by energy prices, add to inflationary risks.

Regionally, France’s services sector led the slowdown, with business activity deteriorating at an accelerated pace since September. In contrast, Germany maintained modest growth, supported by expectations of greater political stability ahead of its federal elections.

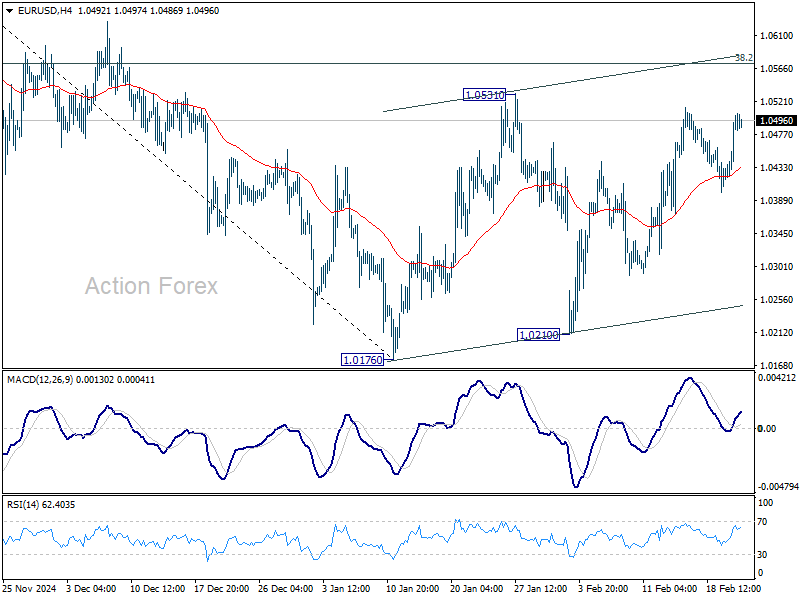

EUR/USD Poised to Renew Two-Month Highs as Buying Momentum Builds

The EUR/USD pair is hovering around 1.0503, extending its rally since midweek. The major currency pair has climbed to a two-month high, with market sentiment favouring further gains.

Key drivers behind EUR/USD’s rise

A decline in US Treasury bond yields has weighed on the US dollar, following a series of weaker-than-expected US economic reports and dovish remarks from Federal Reserve officials.

Austan Goolsbee, President of the Federal Reserve Bank of Chicago, stated that he does not expect the Core Personal Consumption Expenditures (PCE) index to be as concerning as the recent Consumer Price Index (CPI) data. As a key inflation measure for the Federal Reserve, the Core PCE significantly influences monetary policy expectations.

Meanwhile, St. Louis Fed President Alberto Musalem warned of stagflation risks and the potential challenges in setting future policy.

The latest US jobless claims data further raised concerns, showing an increase to 219,000 from the previous 213,000, exceeding the forecast of 214,000.

In the eurozone, the euro could see further upside if the German election outcome triggers additional short-covering in EUR/USD.

Technical analysis of EUR/USD

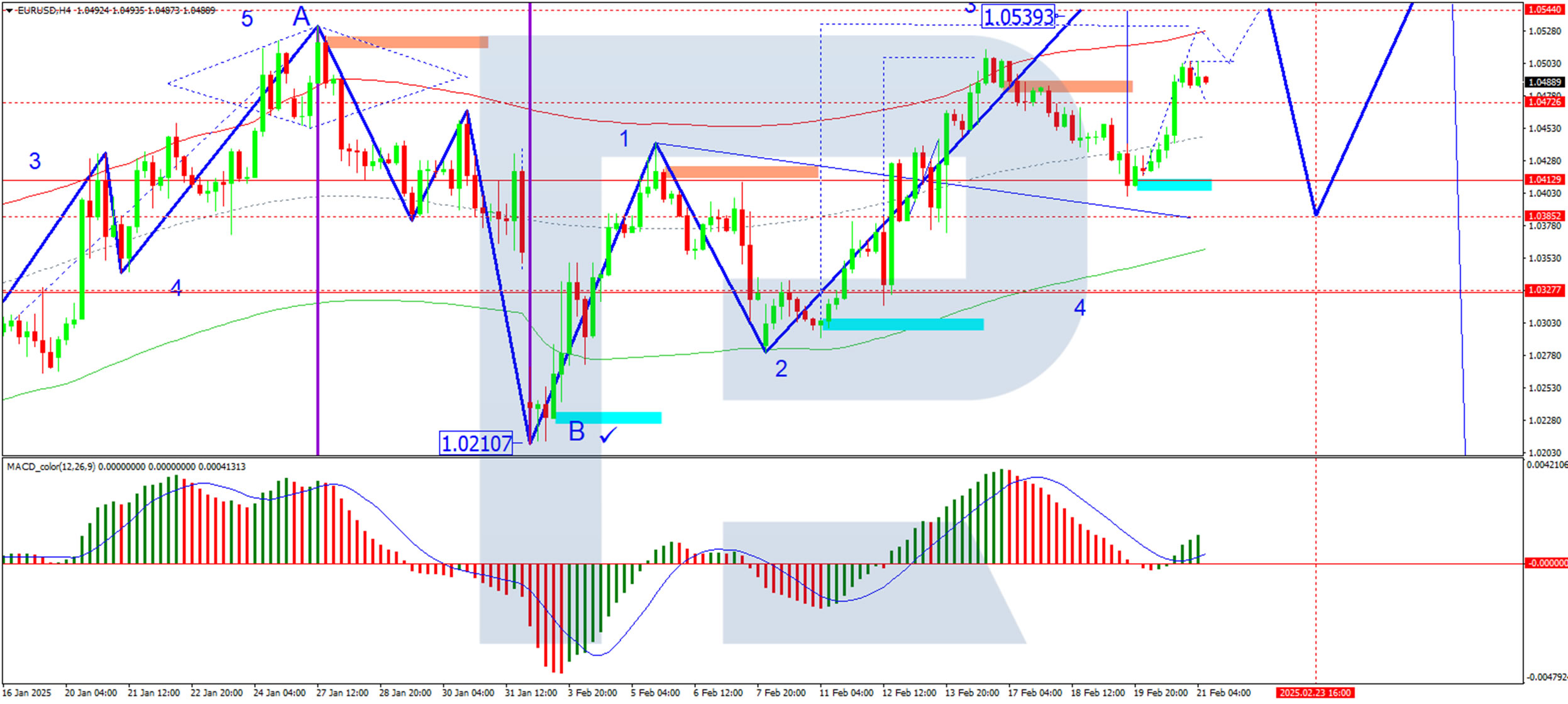

On the H4 chart, EUR/USD has completed a growth wave to 1.0470, forming a consolidation range around this level. The market has since broken higher, paving the way for further gains towards 1.0544. A correction towards 1.0385 may follow after reaching this level. The MACD indicator supports this scenario, with its signal line above zero and pointing upwards, indicating continued bullish momentum.

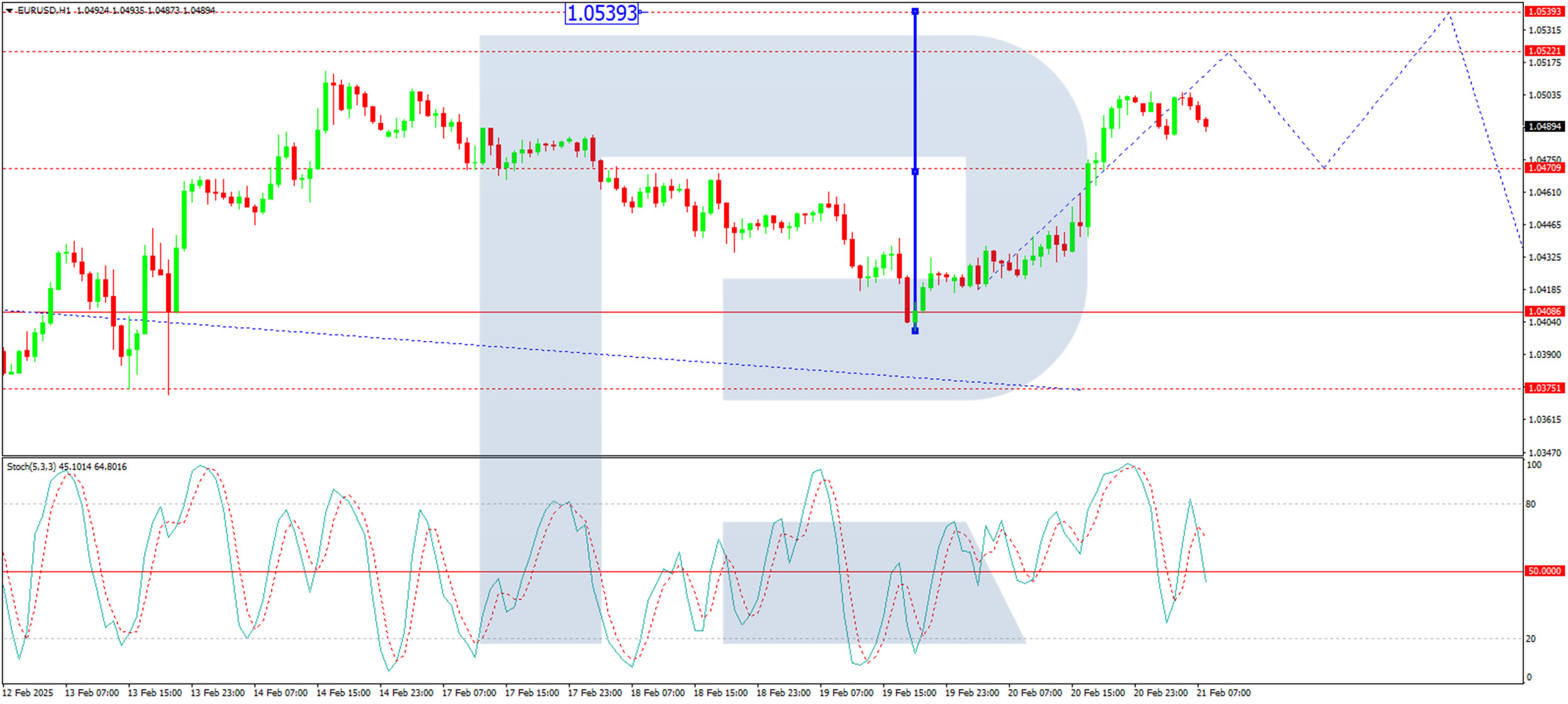

On the H1 chart, the pair executed a growth wave to 1.0470, followed by a narrow consolidation range around this level. The likelihood of an upward breakout towards 1.0520 remains high. After reaching this level, a correction to 1.0470 could occur before the growth wave resumes towards 1.0544. The Stochastic oscillator confirms this outlook, with its signal line above 80 and trending towards 20, suggesting a possible pullback before further gains.

Conclusion

EUR/USD remains in an uptrend, supported by weakening US Treasury yields and a cautious Fed outlook. If bullish momentum continues, the pair may extend gains towards 1.0544. However, a corrective move could follow before further upside. The outcome of the German election could also influence short-term price action, potentially driving additional volatility.

Monthly PMI Release May Spark Some Volatility Today

Markets

Bessent’s interview with Bloomberg offered a welcome distraction in yesterday’s generally dull trading session. The US Treasury Secretary touched on a range of topics, including on the US’ debt maturity profile. He ruled out terming out the debt for the time being, due to elevated inflation and the Fed being a competitive seller through QT. US yields eased a few basis points with the long end outperforming. German rates declined about 2 bps across the curve in technical trading. Bessent also tried to quell speculative market chatter about a potential gold revaluation of the US reserves. Such a one-off windfall would generate some $800bn out of thin air but is not what Bessent “had in mind” when he said he wants to monetize the US balance sheet. Gold prices eased from its intraday highs but still finished with a record. The US dollar fainted into late-European and US dealings even though risk sentiment was a bit shabby. EUR/USD surged towards 1.05. The trade-weighted index tested support at 106.35 (38.2% retracement on the Q4 rally). USD/JPY closed sub 150 for the first time since December only to reverse course this morning.

The monthly PMI release may spark some volatility today. The January edition for the first time since August of last year suggested the European economy eked out a bit of growth with the composite indicator venturing north of 50. Consensus expects this (painstakingly slow) bottoming out process to continue in February. The overarching PMI would rise from 50.2 to 50.5 on improvements in both manufacturing (47 from 46.6) and services (51.5 from 51.3). We hold a similar view. Barring (external) shocks, we think the European economy has seen the trough but lacks the drivers to get into higher gear for now. Unless the PMIs offer a positive surprise, it may be difficult for European rates to rally and EUR/USD to steam ahead beyond first resistance levels of 1.0533 and 1.0551. That’s particularly the case given event risk looming this weekend. German elections on Sunday could be a gamechanger, for the country and EU. The polls offer three scenario’s, assuming the far-right AfD (currently running at 20% in the polls) won’t be joining any coalition. The “Grand Coalition” of CDU/CSU and SPD (socialists) is the most market friendly one: it’s simply, straightforward and known territory. The “Kiwi Coalition” – CDU/CSU & the Greens – has never been tested on a federal level and ideological differences are larger than in a Grand Coalition. The least-favourable outcome is a three-way coalition (“Kenya”) with all of the above parties setting the stage for difficult and long negotiations. On one thing they all agree though: the debt brake must be adjusted or lifted to unlock a necessary fiscal impulse.

News & Views

The Japanese Statistics Bureau this morning reported inflation (ex. fresh food) rising further in January by 0.4% M/M and 3.2% (from 3.0%), slightly higher than expected. Core inflation ex. food and energy also rose from 2.4% to 2.5% while overall headline inflation accelerated to 0.5% M/M and 4.0% Y/Y (from 3.6%). The data add evidence to the upward price spiral that the BoJ is looking for even if it’s especially food prices that are rising (1.8% M/M and 7.8% Y/Y). Services inflation slowed to 1.4% Y/Y from 1.6%. For the BoJ to be sure that inflation is driven by higher wages, the services component preferably gets more weight as a driver for inflation. Even so, today’s report still supports the case for further BOJ policy tightening. In another release this morning, the composite PMI improved further in February from 51.1 to 51.6, the strongest pace in five months. The details of the report were a bit mixed. The modest improvement driven by sustained growth in services activity (53.1), while manufacturing output declined at a softer rate 48.6 from 47.3). New business increased for the seventh time in eight months, but the rise was assessed as modest. Orders for manufacturing continued to decrease but the decline was mild and more than offset by services. Confidence on activity growth over the next 12 months softened in February, to the lowest point since January 2021 on labour shortages, persistent inflation, and economic malaise in the domestic economy. Employment levels in the Japanese private sector rose at their slowest rate in just over a year. Additionally, the rate of input price inflation across the private sector was little changed from January’s historically sharp pace. Aside from the data, comments from BOJ governor Ueda this morning did catch the eye. On a question in Parliament, the governor indicated that the Bank is still ready to purchase government bonds if long term yields are rising too sharply. The 10-y yield (1.43%) recently rose to the highest level since 2009. While this in part may be driven by higher market inflation expectations, the BoJ signals that it still keeps a close eye on markets to develop orderly. The rise in LT yields slowed after the release (10-y currently minus 1.5 bp).

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0446; (P) 1.0475; (R1) 1.0532; More...

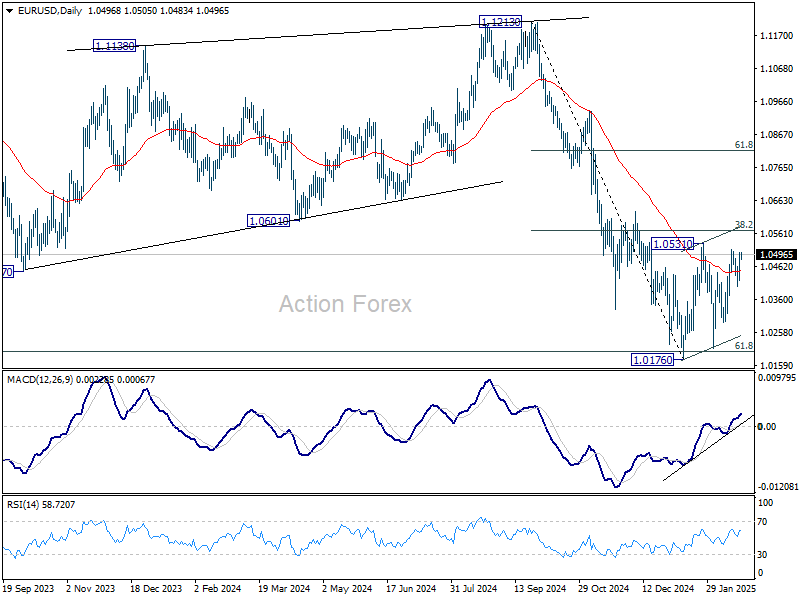

EUR/USD is still bounded in consolidation from 1.0176 and intraday bias stays neutral. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

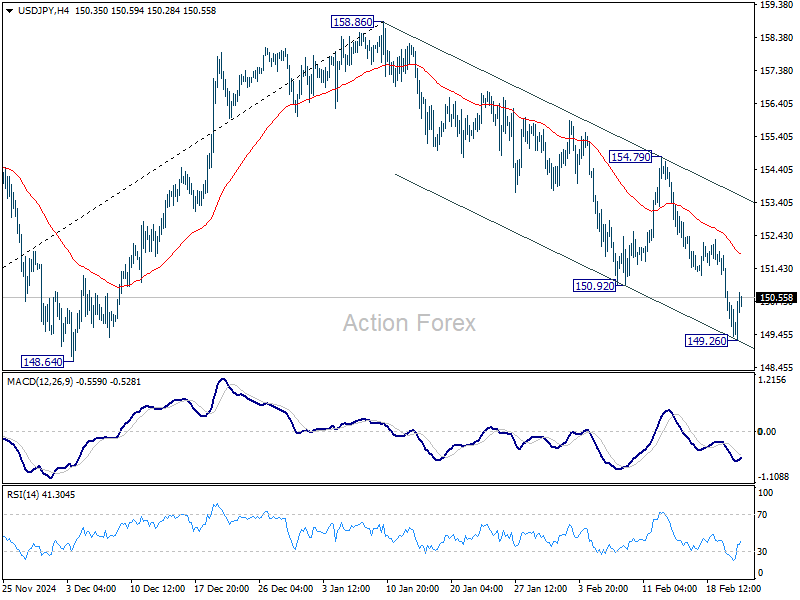

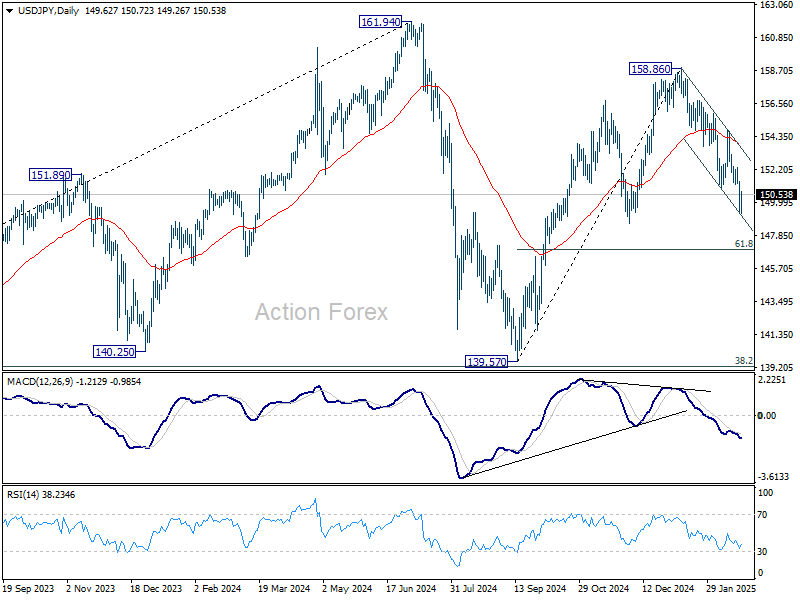

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.85; (P) 150.17; (R1) 150.93; More...

Intraday bias in USD/JPY is turned neutral first with current recovery. Some consolidations might be seen, but outlook will stay bearish as long as 154.79 resistance holds. Fall from 158.86 is currently seen as the third leg of the pattern from 161.94 high. Break of 149.26 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

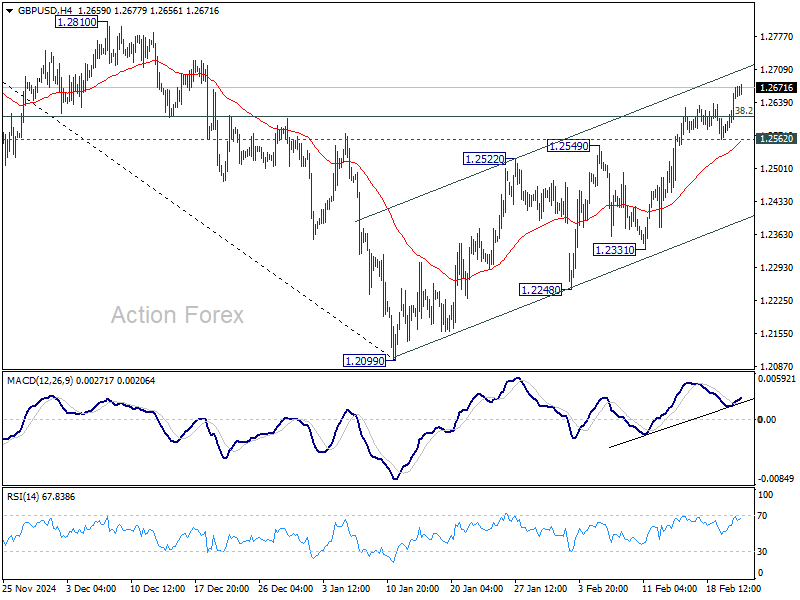

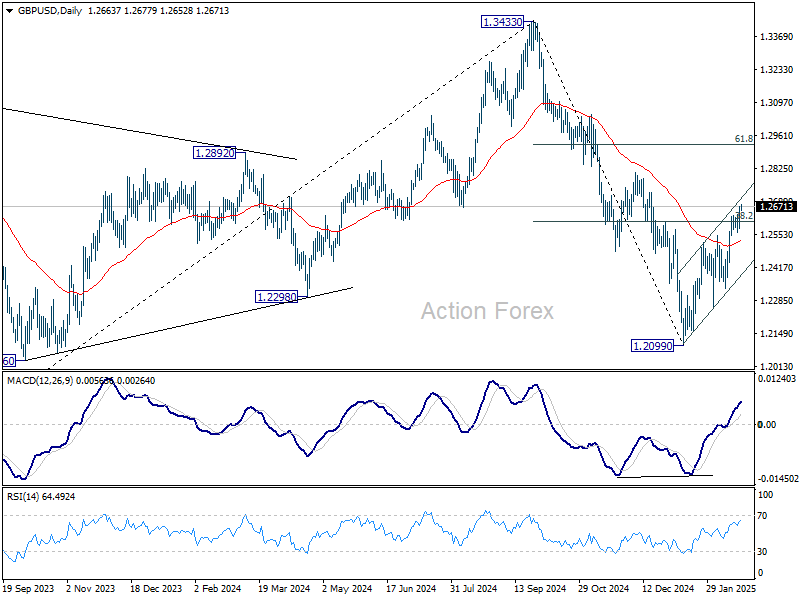

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2552; (P) 1.2597; (R1) 1.2631; More...

GBP/USD's rally from 1.2099 extended higher and intraday bias is now on the upside for 1.2810 resistance. Firm break there should target 61.8% retracement of 1.3433 to 1.2099 at 1.2923 next. On the downside, below 1.2562 minor support will turn intraday bias neutral again first. But another rise will remain in favor as long as 1.2331 support holds, in case of retreat.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

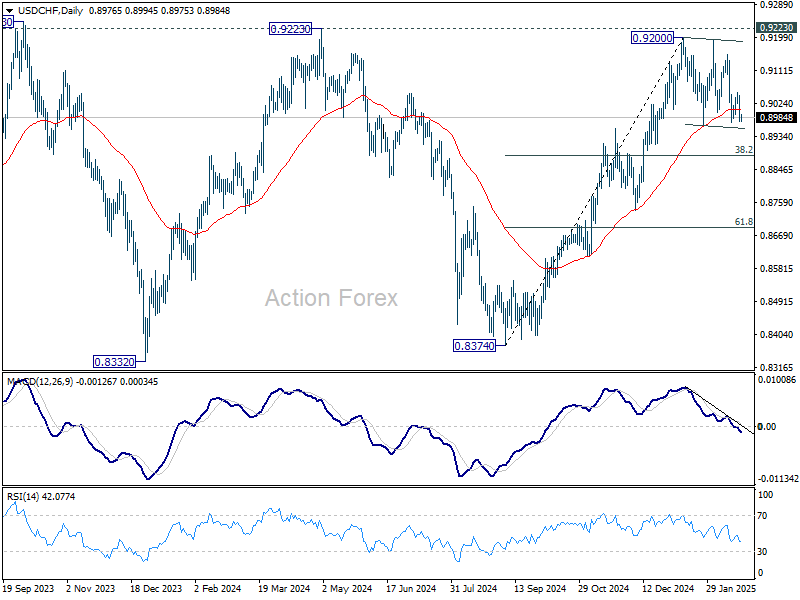

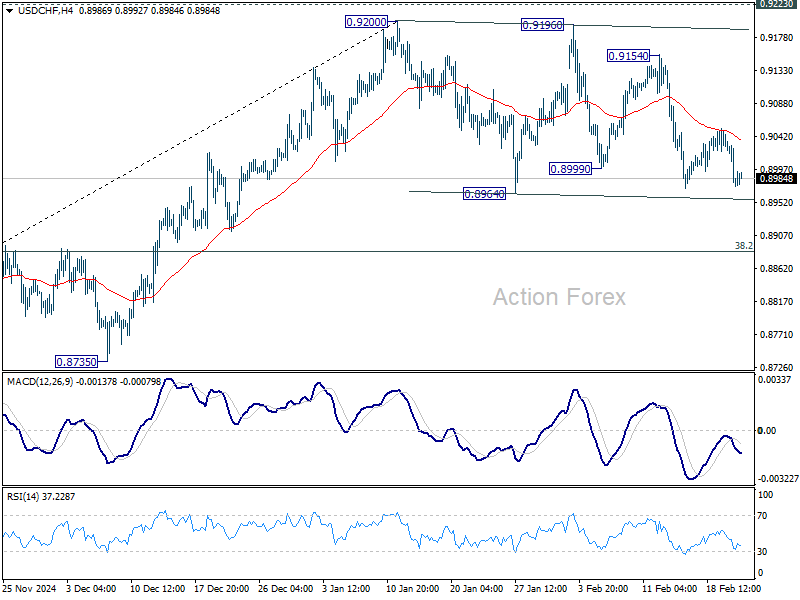

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8953; (P) 0.9003; (R1) 0.9031; More…

USD/CHF is still bounded in consolidation from 0.9200 and intraday bias remains neutral. While deeper pull back might be seen, outlook will stay mildly bullish as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, firm break of 0.9223 key resistance will carry larger bullish implication. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.