Sample Category Title

Fed’s Musalem warns of inflation expectations unanchoring

St. Louis Fed President Alberto Musalem raised concerns overnight about inflation expectations becoming "unanchored", emphasizing that the risk is higher when the economy is running without slack and after a period of elevated inflation.

Musalem pointed out that market and survey data show a notable rise in near-term inflation expectations over the past three months, reinforcing worries that inflation might remain above the Fed’s 2% target for longer than anticipated.

He warned that if inflation remains stuck at elevated levels or expectations continue to rise, “a more restrictive path of monetary policy relative to the baseline path might be appropriate.”

Fed’s Bostic sees two rate cuts in 2025 but flags significant uncertainty

Atlanta Fed President Raphael Bostic noted his baseline expectation for two 25bps rate cuts later this year, but cautioned that “the uncertainty around that is pretty significant”, with multiple factors that could shift the outlook in either direction.

He acknowledged growing concerns from businesses regarding the potential impact of new tariffs, immigration policies, and regulatory changes on economic conditions.

He noted that there is both enthusiasm and “widespread apprehension” among business contacts regarding these policy shifts. Specifically, he warned that tariffs could push up costs, adding, “Many feel confident that if that happens, then they can pass along higher costs in their prices.”

Fine-Tuning (is) the Message

The RBA cut the cash rate 25bps to 4.1% this week as expected. But the tone in the forecasts and initial rhetoric was more hawkish than we expected, reflecting an apparent pivot to ‘fine-tuning’.

As was widely expected, the RBA cut the cash rate this week by 25bps to 4.1%. Inflation has declined faster than the RBA’s previous forecasts implied, with underlying inflation running at an annualised rate consistent with the 2–3% target over the second half of 2024. Getting inflation sustainably back down to target is the Board’s highest priority. Given these data and the likely near-term outcomes that they imply, it would be difficult to say that the goal is off-track. The post-meeting statement acknowledges the progress made on getting inflation to target, and that inflation might be declining a bit faster than earlier expected.

The post-meeting communication also highlighted that the RBA assesses policy to still be restrictive. Indeed, some refinements to the RBA’s models for estimating the neutral rate now suggest that, even after this week’s cut, monetary policy is more restrictive than the RBA thought three months ago.

So why was the RBA’s rhetoric so hawkish? The press statement highlighted that there was a risk of easing ‘too much too soon’, in which case disinflation would ‘stall’ and inflation would ‘settle above the midpoint of the target range’ – exactly what their forecasts show trimmed mean inflation doing. The Governor went out of her way to challenge the market’s view of the likely path of the cash rate, describing it as ‘far too confident’ and ‘unrealistic’.

Part of the reason for the hawkish move is ‘lingering tightness’ in the labour market. The prior easing in the labour market had ‘stalled’ over the second half of last year. While the Governor declined to provide an estimate of the NAIRU – the unemployment rate that is consistent with full employment – the structure in the forecasts suggests that the staff are still working on the assumption that it is around 4½%. The RBA’s framework (appropriately) goes beyond this single number and considers other variables such as underemployment and vacancies. But it seems to have remained quite unresponsive to the evidence of wages growth coming in lower than expected – including, at the margin, this week’s WPI data.

The hawkish tone is also an outworking of the 2023 RBA Review. Recall that the RBA Review recommended, and the latest Statement on the Conduct of Monetary Policy adopted, a framing of the inflation target that requires the RBA to set policy ‘such that inflation is expected to return to the midpoint of the target’, even though ‘all outcomes within the target range are consistent with the Reserve Bank Board’s price stability target’.

The key point here is that RBA’s revised forecasts now have trimmed mean inflation constant (dare we say ‘sustained’) at 2.7% out to mid-2027. Recall that trimmed mean inflation was already running at an annualised rate of 2.7% over the second half of 2024. So the RBA’s forecasts imply no further disinflation from here at all, if policy were to follow the market pricing at the time the forecasts were finalised, which was for about 90bps of cuts. (The RBA’s forecasts are put together assuming the cash rate follows the path implied by market pricing at the time the forecasts are finalised.)

It seems that, in the new world, 2.7% is not good enough: policy must be set to show 2.5% at the end of the forecast period. It also explains why in the post-meeting press conference, the Governor emphasised that people still needed to be patient to get inflation down – down by a whole 0.2ppts. (Yes, year-ended trimmed mean inflation is 3.2%, but that is all base effects from the first half of 2024. In the current environment, though, the forward pulse in inflation is better represented by calculations with less stale information in them.)

In an unusual move, Deputy Governor Hauser was quickly wheeled out in a Bloomberg interview to settle things down after the first round of communication generated some confusion (and pushback) among commentators and market participants. And he did strike a more placatory tone, highlighting the good news on inflation and the possibility that labour supply might be higher than assumed.

The key piece of new information revealed in that interview was that the Board reviewed a scenario of unchanged cash rates that had inflation undershooting the midpoint of the target, ‘not by a lot, but by a little bit’. Assume this means 2.3%. Contrast that with the published forecasts with (trimmed mean) inflation settling at 2.7%.

So, we see a 0.4ppt difference in inflation a couple of years from now, given a difference in the cash rate of just under 1ppt. This is around double the sensitivity of inflation to interest rates in the RBA’s flagship MARTIN model, and above the rules of thumb that most Australian policymakers have in their head about how the Australian economy works.

If the RBA has revised up its estimate of the sensitivity of inflation to interest rates in recent times, this has not been widely signalled. But, even with this greater sensitivity, what we are seeing is an RBA trying to finesse a scenario where inflation lands at exactly 2.5% instead of 2.7%. This is the epitome of fine-tuning – something monetary policymakers are supposed to avoid.

Given the RBA’s communications difficulties this week, it is not clear that this recommendation of the RBA Review represents an improvement on past practice.

Bitcoin (BTC/USD) Holds Above $95k But Faces Significant Resistance Ahead

- Bitcoin (BTC/USD) is holding above $95k but facing significant resistance.

- While spot Bitcoin ETFs have attracted substantial investments, there have been recent net outflows, and on-chain data suggests a cooling down in speculative appetite.

- Strategy’s potential Bitcoin purchase, following a $2 billion fundraising, could be a catalyst for a future bull run.

Bitcoin has regained momentum after finding support at the key $95k level this week before rising to trade at 98357 at the time of writing. The recent consolidation suggests that Bitcoin could be ready for its next big rally, with a move higher looking appealing once more.

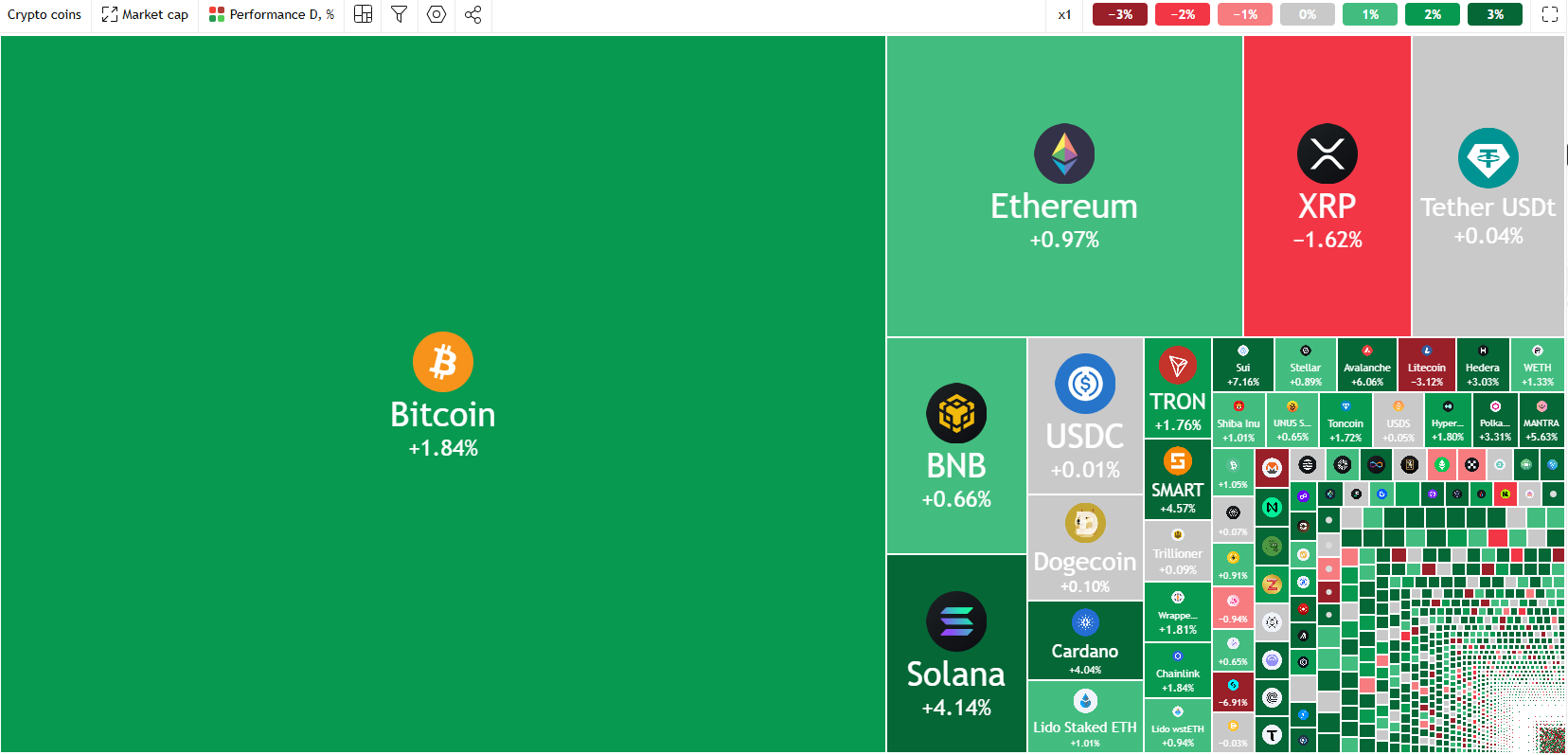

Crypto Heatmap, February 20, 2025

Source: TradingView (click to enlarge)

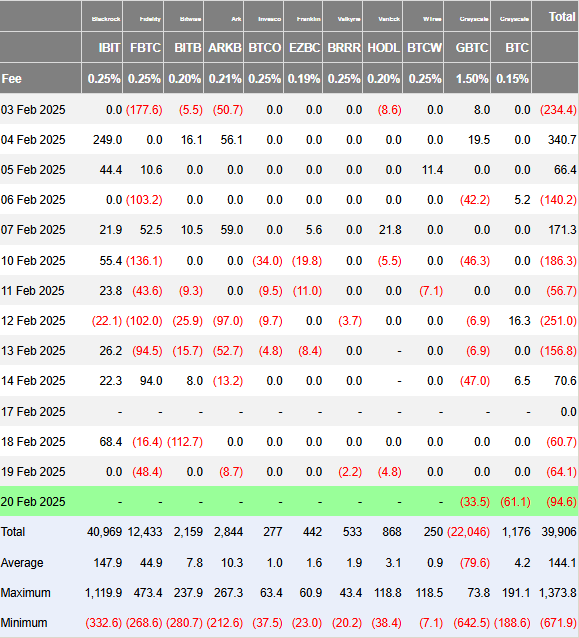

ETF Flows

Even though Bitcoin’s price fell from its all-time high on January 20, data from CoinShares shows that spot ETFs tied to Bitcoin have still attracted a huge $5.6 billion in new investments.

However, over the last few days we have seen a consistent amount of net outflows with figures of 60.7, 64.1 and 94.6 million USD in net outflows since Tuesday.

Source: Farside Investors

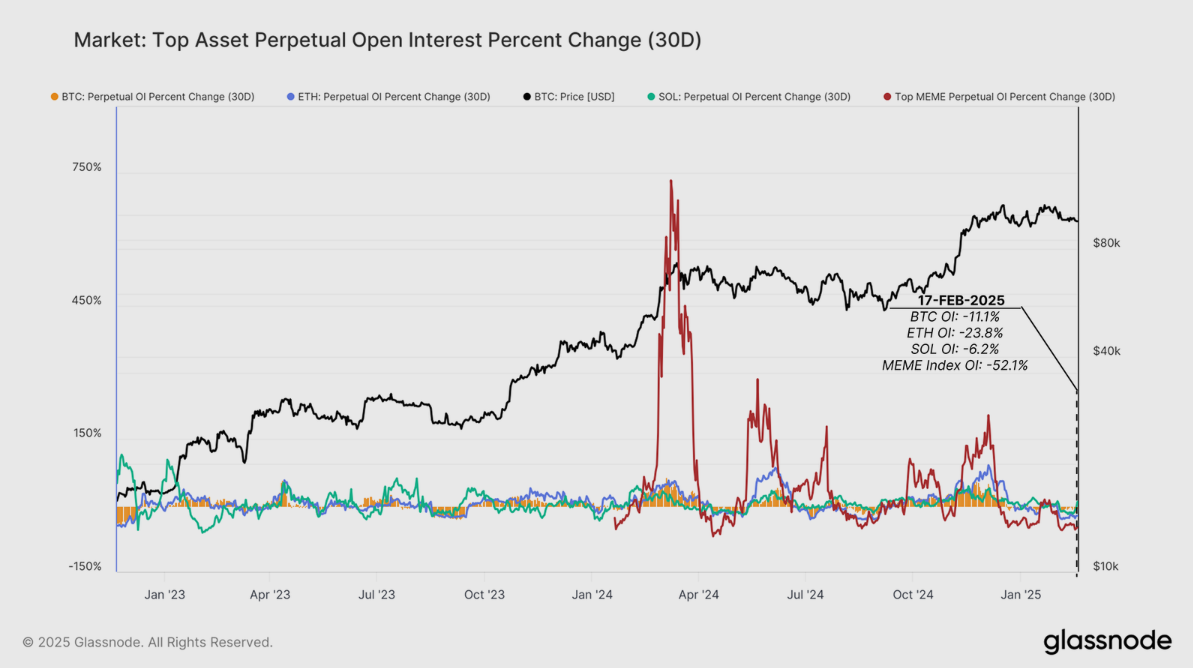

The Week on Chain – Glassnode Data Reveals Downside Risks

Money flowing into the market is slowing down, and trading in derivatives is dropping. The way short-term investors are buying now looks similar to May 2021, which was a tough time for the market.

Overall, in recent weeks markets are seeing the momentum of capital inflows has declined for all digital assets. This signals a meaningful cooling down in speculative appetite and alludes to a potential for capital rotation out of riskier assets on the road ahead.

This is in line with the overall market sentiment at the moment.Although US stock markets continue to hold near highs, the rise of Gold is a clear sign that markets remain nervous as haven demand continues to propel the precious metal to fresh highs.

Momentum in spot markets is slowing down, and less money is going into perpetual futures. This drop in demand has caused a big decline in open interest across major assets, showing less speculative trading and lower profits from cash-and-carry strategies.

The drop in open interest shows that traders are cutting back on risky leveraged bets, likely because the market feels weaker and less certain. The biggest decline is in Memecoins, which usually attract short-term traders but quickly lose popularity when confidence fades.

Source: Glassnode

Microstrategy or ‘Strategy’ Gearing Up for Fresh Buys?

MicroStrategy or as we should get used to calling them, Strategy didn’t buy any Bitcoin last week, keeping its total at 478,740 BTC for the second time.

However, MicroStrategy has hinted at a new Bitcoin purchase with its recent fundraising effort. On February 20, the company announced it had successfully priced a $2 billion offering of 0% convertible notes due in 2030. The deal, set to close on February 21, also gives buyers the option to purchase an extra $300 million in notes.

Will such a purchase prove to be the catalyst for another bull run?

Technical Analysis BTC/USD

Bitcoin (BTC/USD) from a technical standpoint on the daily timeframe sees price eyeing a breakout following a period of consolidation.

The consolidation between 94000 and 100000 has lasted for the last two weeks with Tuesday seeing price dip to a low of 93340 before reclaiming the 95000 handle.

Thursday daily candle did close back above the 100-day MA resting at 97899 but there are significant hurdles ahead. The 50-day MA rests at 99059, just shy of the psychological 100000 level.

Bitcoin (BTC/USD) Daily Chart, February 20, 2024

Source: TradingView.com (click to enlarge)

Dropping down to a two-hour chart and there may be scope for a short term pullback. Significant support rests below current price as we have the 50,100 and 200-day MA converging between the 96000-97000 handles.

This makes this a key area of confluence which could serve as a base for a move toward the 100000 psychological level and beyond.

Immeidate support rests at 97000 before the key 95000 handle comes back into focus.

Resistance rests at 99059 and 100000 before markets will turn their attention toward the 102157 resistance handle.

Bitcoin (BTC/USD) Two-Hour (H2) Chart, February 20, 2024

Source: TradingView.com (click to enlarge)

Support

- 97000

- 95000

- 93200

Resistance

- 99059

- 100000

- 102157

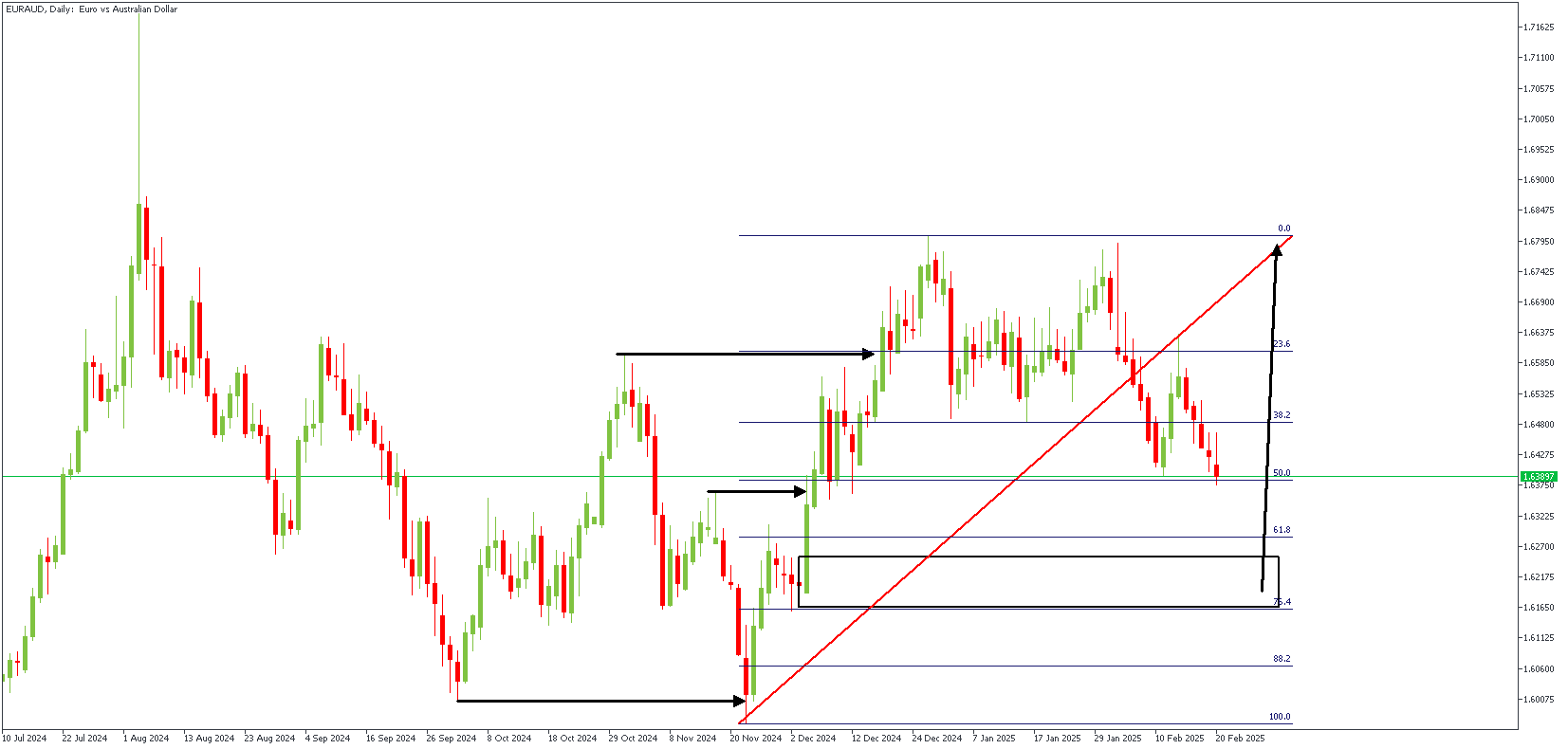

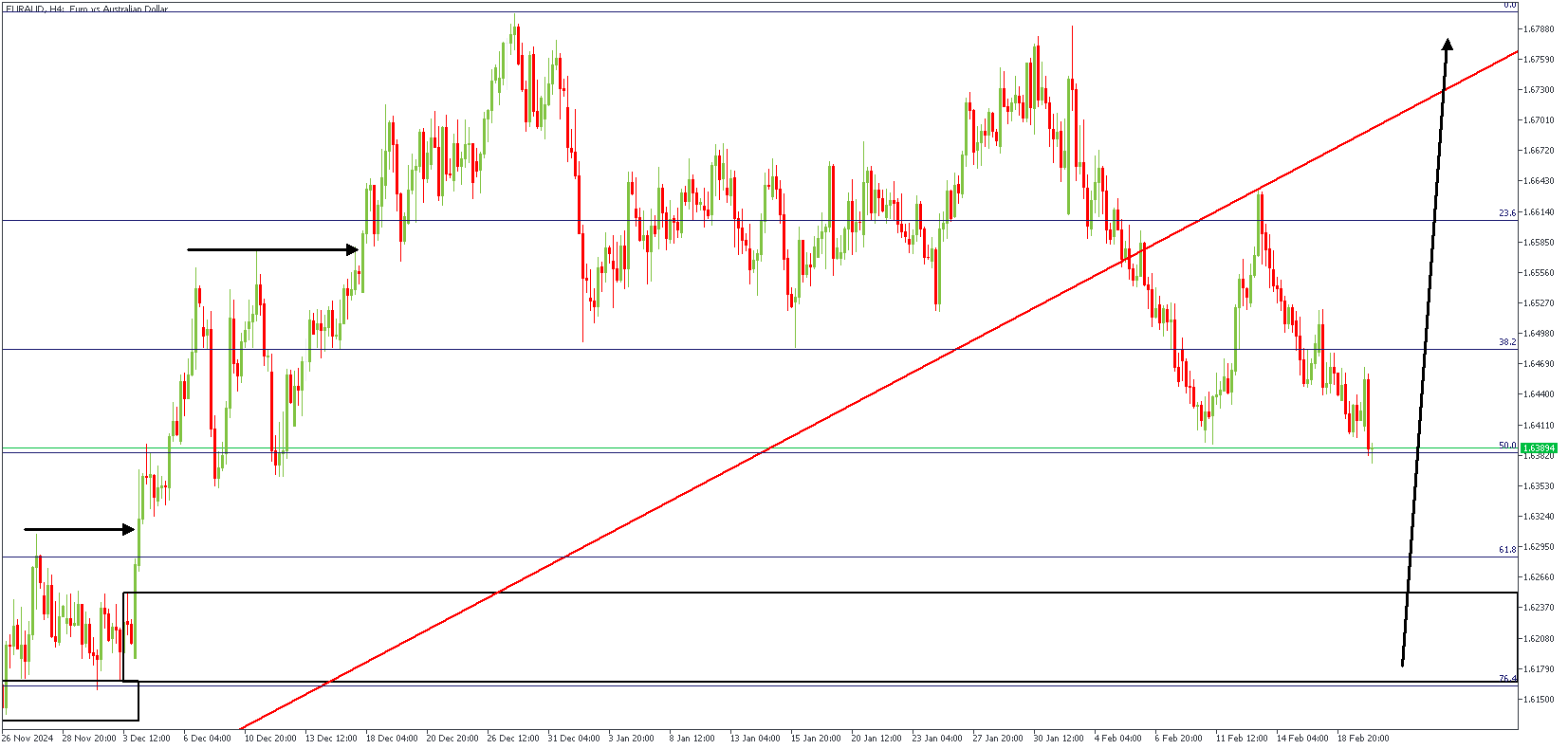

EURAUD Technical Analysis

Global trade concerns continue to influence currency movements. The Australian Dollar and other risk-sensitive currencies have risen recently as the US Dollar weakened. However, fresh worries about new US tariffs have again put pressure on these currencies.

Earlier in February, US President Donald Trump temporarily boosted markets by postponing a 25% tariff on Canadian and Mexican goods. But that optimism quickly disappeared as new tariff threats surfaced. The US has now imposed a 10% tariff on Chinese imports, raising fears that China might retaliate.

Since China is Australia’s biggest trading partner, any trade war escalation could hurt Australian exports—especially commodities like iron ore and coal. China has even hinted that it may challenge the US tariffs at the World Trade Organization (WTO), creating more uncertainty for countries like Australia that rely heavily on exports.

EURAUD – D1 Timeframe

On the daily timeframe chart of EURAUD, the price movement created an SBR pattern (Sweep break Retest), with a demand zone sitting on top of the 76% Fibonacci retracement level, right behind the FVG area. The fact that liquidity would have been swept before the price tapped into the demand zone further confirms its validity.

EURAUD – H4 Timeframe

On the EURAUD 4-hour timeframe chart, we see the price approaching the area of demand, with the induced low already within reach of the momentum. Following this, I expect the market to give off a bullish reaction from the demand area.

Analyst’s Expectations:

- Direction: Bullish

- Target- 1.67425

- Invalidation- 1.60984

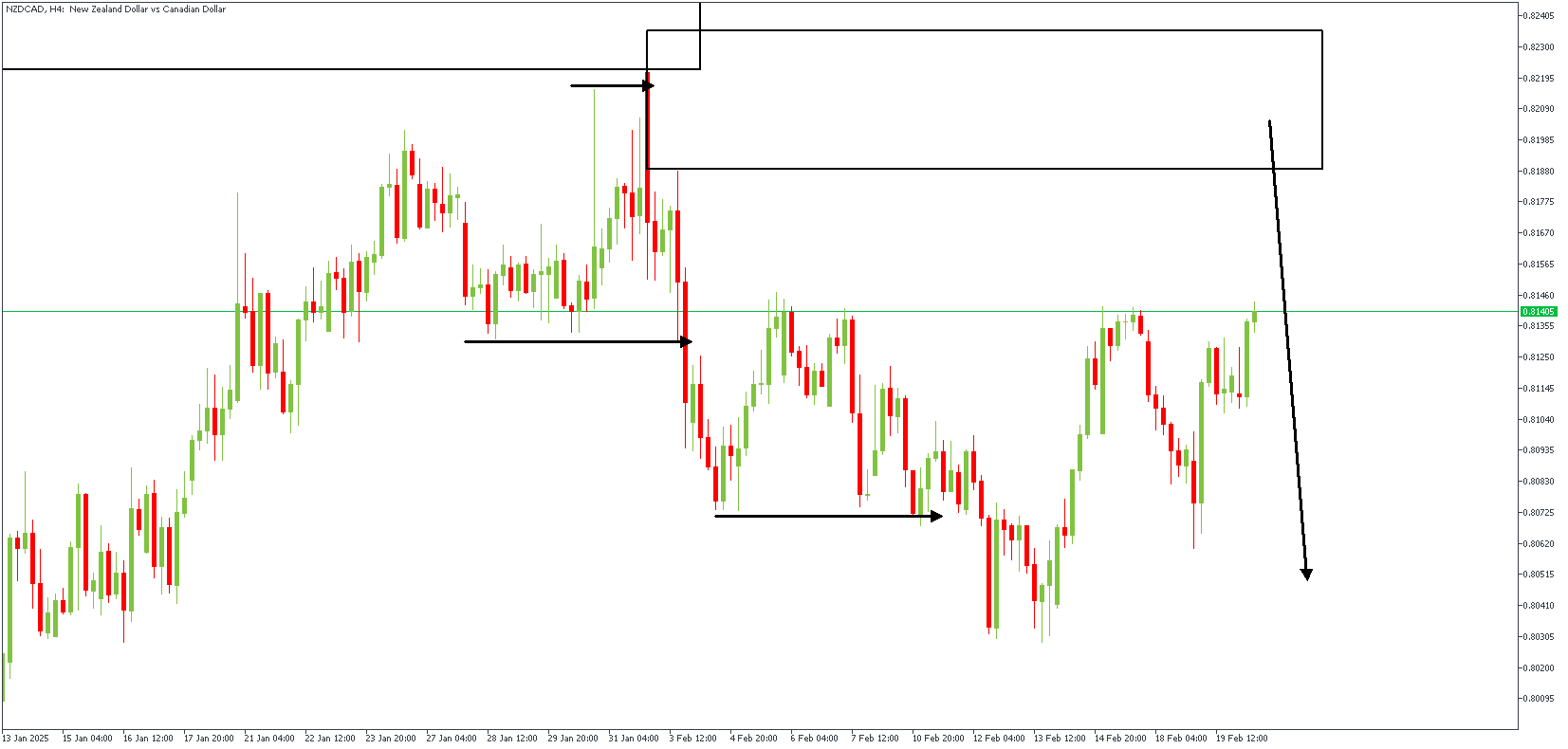

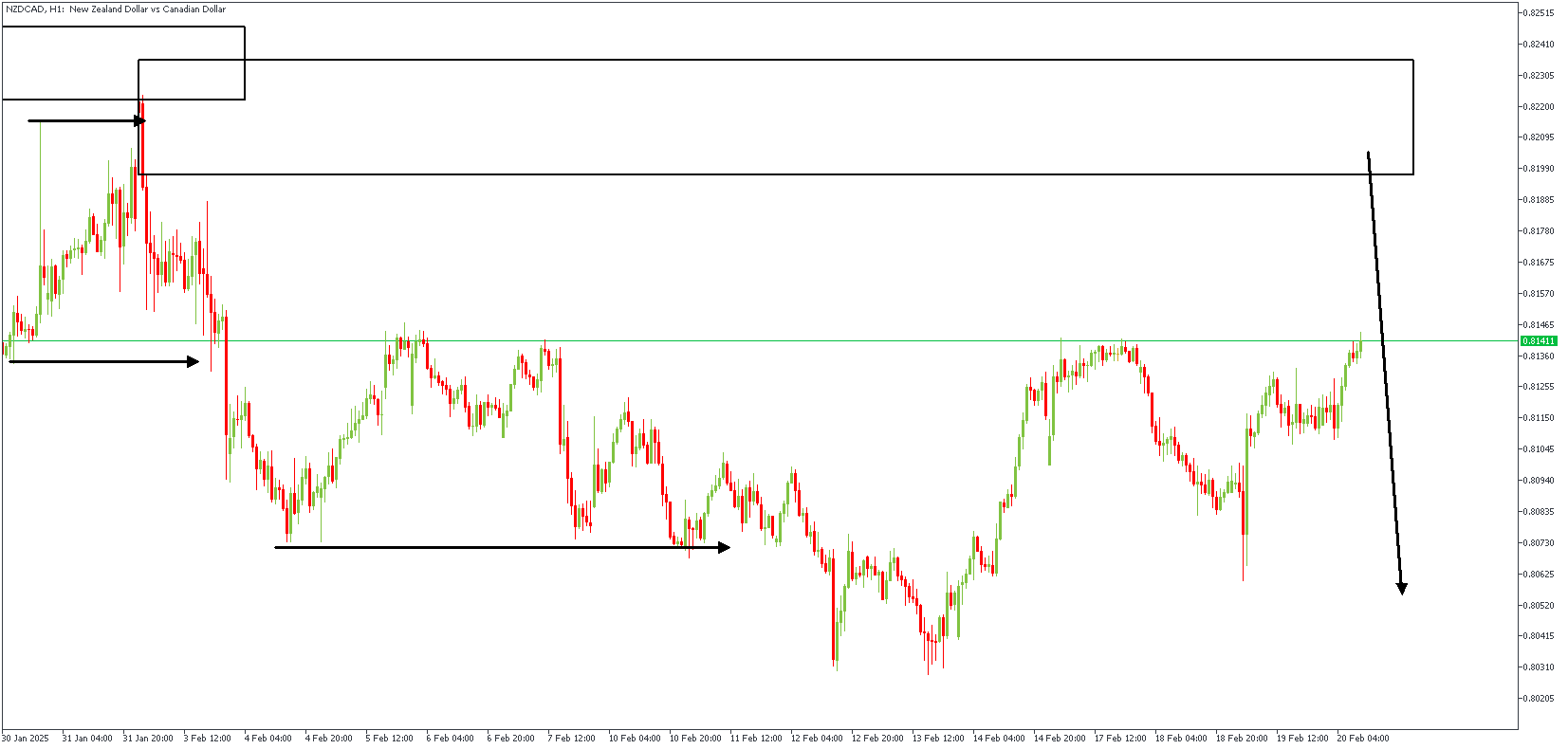

NZDCAD Technical Analysis

The New Zealand Dollar rose on Wednesday, trading at 0.5721 despite a significant interest rate cut by the Reserve Bank of New Zealand (RBNZ). As expected, the RBNZ lowered rates by 0.50% to 3.75%, the lowest since November 2022. The bank has cut rates by 1.75% since August, but the NZD’s strength was surprising since rate cuts usually weaken a currency. The RBNZ said inflation remains within its 1%-3% target but warned that slow economic growth at home and globally is a concern. It also mentioned trade restrictions as a potential risk, though it didn’t address US tariff threats directly. Governor Adrian Orr expects rates to drop to 3% by year-end, slightly lower than previous projections. Instead of significant cuts, the RBNZ plans to gradually lower rates in the coming months.

NZDCAD – H4 Timeframe

The daily timeframe chart of NZDCAD shows an initial rejection of the daily timeframe supply zone; the momentum from the rejection was so impulsive that it broke the previous structure and created an SBR pattern. The retest of the highlighted supply area is expected to trigger the next wave of bearish impulse.

NZDCAD – H1 Timeframe

One of the most striking details on the 4-hour timeframe chart of NZDCAD is the FVG (Fair Value Gap), as seen right below the highlighted supply zone. The presence of an inducement lends further credence to the bearish sentiment since the said supply overlaps the 76% Fibonacci retracement level.

Analyst’s Expectations:

- Direction: Bearish

- Target- 0.80569

- Invalidation- 0.82474

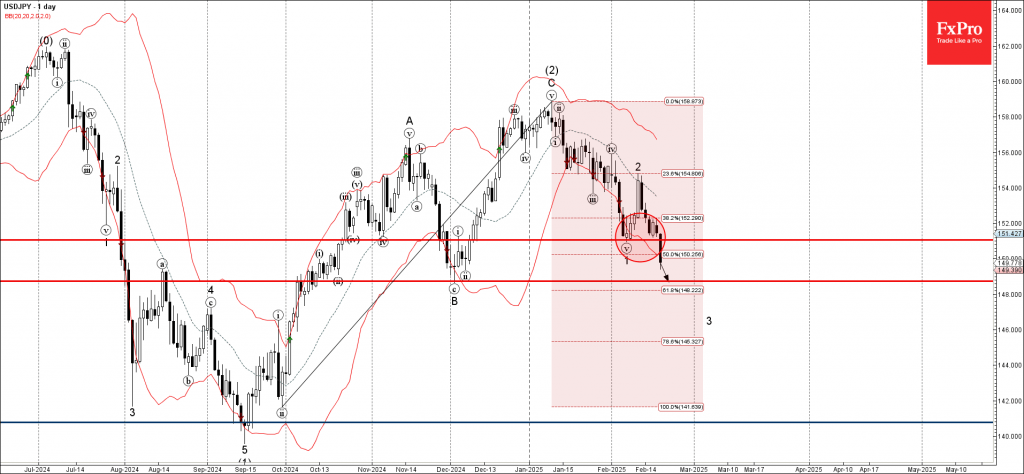

USDJPY Wave Analysis

- USDJPY broke support zone

- Likely to fall to support level 148.70

USDJPY currency pair recently broke the support zone between the support level 151.00 (which formed the daily Morning Star at the start of February) and the 50% Fibonacci correction of the previous upward impulse from September.

The breakout of this support zone accelerated the active short-term impulse wave 3 – which belongs to wave (3) from January.

USDJPY currency pair can be expected to fall to the next support level 148.70 (the former monthly low from December).

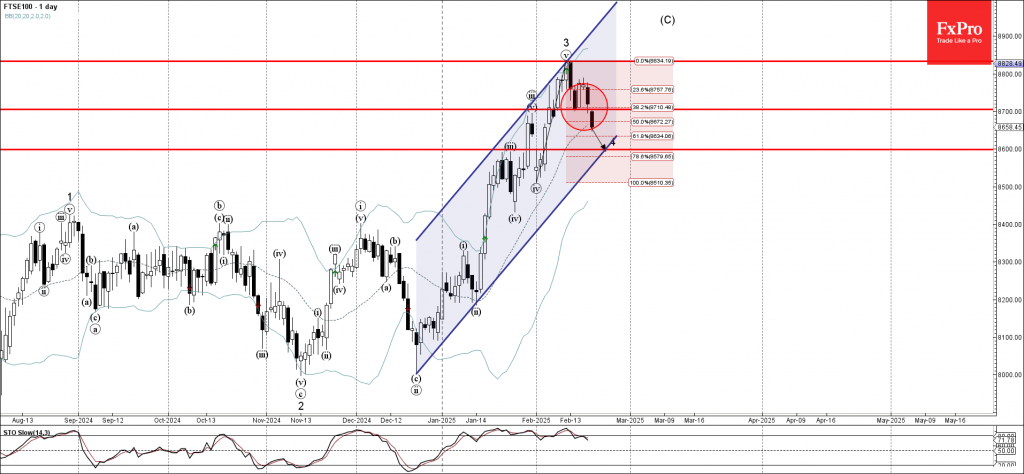

FTSE 100 Wave Analysis

- FTSE 100 broke support zone

- Likely to fall to support level 8600.00

FTSE 100 Index previously broke the support zone between the support level 8700.00 (which created daily Bullish Engulfing earlier this month) and the 38.2% Fibonacci correction of the upward impulse from January.

The breakout of this support zone accelerated the active short-term ABC correction 4, which belongs to the upward impulse sequence (C) from last year.

FTSE 100 Index can be expected to fall to the next support level 8600.00 (target price for the completion of the active correction 4 intersecting with the support trendline of the daily up channel from December).

Sunset Market Commentary

Markets

US Treasury Secretary Bessent said in an interview with Bloomberg Television that the Treasury team under the previous president had shortened the duration in Treasury sales. While he’s not shortening any further, the US Treasury is also a long way off in terming out the debt. He noted that elevated inflation and competition by the Fed (via quantitative tightening) currently hamper such a move. Fed governor Waller last year suggested that Fed could stop its balance sheet runoff once US reserves drop to 10%-12% of US GDP. That’s approximately $2800-3000bn compared to current reserves of $3220bn. The US Note future ticked marginally higher after the comments in today’s only noticeable market move. The US yield curve bull flattens slightly with yields losing 0.8 bps (2-yr) to 2.3 bps (10-yr). The US eco calendar contained near consensus but still very low weekly jobless claims (219k from 214k) and the expected setback in Philly Fed Business Outlook. The indicator reached its second best level since 1983 in January (44.3) before retreating to a still solid 18.10 in February (vs 14.3 expected). New orders fell back from 42.9 to 21.9, but that’s still the second best outcome since November 2021. Shipments equally remain strong at 26.3 (from 41). Both prices paid and received pointed at accelerating inflationary pressures. Companies turned less optimistic on the six months outlook since September though. Markets ignored the numbers. Daily changes on the European curves are neglectable with EUR/USD marginally stronger near 1.0450. European stock markets recover some of yesterday’s corrective losses (+0.30%). ECB Makhlouf warned after yesterday’s hawkish comments by ECB Schnabel that the disinflation process faces dangers. ECB Simkus was more neutral, aligning himself with the three additional 25 bps rate cuts the market discounts over the course of 2025. Everybody agrees that a 25 bps move at the March policy meeting is a done deal, but the outlook becomes more uncertain afterwards. The EMU money market is currently split on the possibility of a pause in April. The next couple of days/weeks remains full of event risk with global PMI surveys, a speech by ECB chief economist Lane and first talks between the US and China tomorrow, German parliamentary elections on Sunday and everything related to the Russian conflict in Ukraine and slow but steadily approaching tariff deadlines.

News & Views

The National Bank of Belgium’s consumer confidence indicator rose sharply in February. The 7-point surge from -11 to -4 was together with December 2022 the largest one-month improvement since May 2021. From a level point of view it is the highest since September of last year. Belgian households were much less concerned over the labour market: the unemployment series hit its lowest since early 2022. The NBB noted that “More stringent government regulations may be the reason for this.” The widespread pessimism surrounding expectations for the Belgian economic situation abated as well but this is not yet fully being reflected in household’s view on their personal situation. They downgraded their expectations concerning their own financial situation while slightly increasing saving intentions.

The European Central Bank (ECB) incurred a record loss of almost €8bn in 2024. It’s the second straight loss after booking a €1.27bn shortfall in 2023. They are a direct result of the central bank’s aggressive tightening campaign against the post-Covid inflation surge. That pushed up interest expenditures well beyond the income generated by the (extremely) low-yielding bonds purchased over the previous years. While the ECB may still incur losses in coming years, they should be lower than in the past two due to the central bank’s bond portfolio shrinking and after a series of rate cuts. The combined €9.21bn shortfall will be carried forward to be offset against future profits. The central bank stressed that it can still “operate effectively and fulfill its primary mandate of maintaining price stability regardless of any losses.”