Sample Category Title

USD/JPY Heading Lower

USD/JPY's selling demand is pushing lower and the pair has broken hourly support given at 110.84 (27/11/2017 low). Hourly resistance can be found at 113.75 (12/12/2017 high). The technical structure suggests further short-term downside moves.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Bullish Breakout

GBP/USD is trading on an uptrend bias. The technical is highly positive at the moment. Hourly support is given at a distance at 1.3458 (11/01/2018 low) while strong resistance at 1.3764 (15/01/2018 high) is being monitored.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. The pair has set up a long-term support given at 1.1841 (07/10/2017 low). A reversal is currently happening. Strong resistance is given at 1.5018 (24/06/2016 high).

EUR/USD Short-Term Bearish Consolidation

EUR/USD is pushing lower. The pair is bouncing back lower. Hourly resistance is given at 1.2297 (15/01/2018 high). Stronger support is given a distance at 1.1916 (09/01/2018 low).

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

NZDUSD Retreats After Sharp Bullish Rally

NZDUSD has reversed aggressively back to the upside, after the rebound on the 0.6815 support level, posting an almost 4-month high of 0.7313 during Monday’s trading session. This top is above the 61.8% Fibonacci retracement of the down-leg from July’s more than a 2-year high of 0.7555 to November’s 18-month low of 0.6780.

From the technical point of view, in the daily chart, momentum indicators are holding in the overbought areas with the RSI just above the 70 level, but it seems to be ready for a downward slope after the sharp buying interest. On the other hand, the MACD oscillator is strengthening its bullish momentum and there are no signals for a retracement. Also, the 40-day simple moving average created a bullish crossover with the 20-day SMA in the previous sessions, signaling for further gains.

Upside moves are likely to find resistance at 0.7370, this is the top of August 10. Rising above this area would help shift the focus to the upside towards the 0.7430 resistance level.

In the short-term, the bullish phase remains but if the price slips below the 61.8% Fibonacci mark, it could hit 0.7210. Moreover, a break below the aforementioned obstacle could open the door for a bearish run towards the 50.0% Fibonacci level of 0.7167.

As a side note, in the medium-term timeframe, NZDUSD recorded five green weeks in a row and successfully surpassed the 50 and 100-week SMAs.

Technical Outlook: GBPUSD Eases After UK CPI Data, Overbought Conditions Weigh

Cable dipped on Tuesday after strong three-day rally showed initial signs of stall ahead of important Fibo barrier at 1.3837 (61.8% of post-Brexit vote 1.5016/1.1930 fall).

Fresh easing was triggered by UK CPI data which ticked lower in December, pulling from previous month's six-year high at 3.1%.

December inflation came in line with expectation (3.0%) and should not cause stronger negative impact which was expected on release below 3%.

However, overextended studies on daily chart point to corrective action, following recent steep ascend.

Daily RSI is emerging from o/b territory, slow stochastic is strongly overbought and turned sideways, while momentum is turning south.

Today's close in red will be next bearish signal, with corrective easing to be ideally contained by rising 10SMA (currently at 1.3605), before broader bulls continue.

Res: 1.3776, 1.3800, 1.3816, 1.3837

Sup: 1.3740, 1.3724, 1.3700, 1.3638

DAX Jumps, Investors Eye Eurozone CPI

The DAX has posted gains in the Tuesday session. Currently, the index is trading at 13,306.50, up .80%. On the release front, there are no major German or eurozone releases. German inflation numbers were a mixed bag. Final CPI improved to 0.6%, matching the forecast. WPI declined 0.3%, missing the estimate of +0.3%. On Wednesday, the eurozone releases Final CPI.

The DAX jumped out of the gates after New Years’ with strong gains, but has since steadied. Will the rally resume? There are signs that favor additional gains for the German stock markets. First, the ECB minutes from the December meeting were hawkish, leading to speculation that the ECB could wind up its asset purchase program in September. In the minutes, policymakers said that risks to the current outlook were to the upside, which could necessitate a gradual shift in guidance in the next few months. As for the eurozone, the minutes stated that the economy was displaying “continued robust and increasingly self-sustaining economic expansion”. Policymakers have echoed the sentiment that tighter policy could be on the way. On Monday, ECB Governing Council member Ardo Hansson said if the economy and inflation develop as expected, the ECB could wind up the asset purchase program in one shot after September.

The second factor is major progress in coalition negotiations in Germany, raising hopes that the political stalemate may soon be over. There was a report on Friday that Angela Merkel’s conservative bloc and the Social Democrats have agreed on a coalition draft. This ends months of political uncertainty, which has eroded Merkel’s standing and also sidelined Germany on key issues such as Brexit and political reform in the eurozone. Still, the talks are only in the preliminary stage, and further negotiations will take at least several weeks before it is clear that the talks have been successful.

Market Update – European Session: UK CPI Moves Off 5-Year Highs

Notes/Observations

UK Dec CPI moves off five year highs (as expected)

German SPD party showing divide on alliance with Merkel; congress needs to decide whether to enter official coalition negotiations or not at its conference on Sunday, Jan 21st

China rating agency Dagong cuts US sovereign rating by a notch to BBB+ citing concerns about political stability in DC and potential impacts from tax cuts on the federal government's debt-repayment abilities.

Asia:

Japan Fin Min Aso: No comment on FX levels, do not see a big deal with dollar at ~¥110.80; reiterates view that Big currency fluctuations would be problematic

China Chinese Academy of Social Sciences researcher Zhang Ming: Ratio of US Treasuries in China FX reserves is not likely to fall

Europe:

BOE's Tenreyro: Ample time before next Bank of England rate move needed; Expected to vote for "a couple more" quarter-point rises in the next three years if the economy performs in line with the BOE's expectations

ECB's Hansson (Estonia): Appropriate to end asset purchases after September if growth and inflation continue to evolve in-line with the central bank's expectations; euro's appreciation posed no danger to the inflation outlook.

PM May planning speech to outline Brexit policy in February

Americas:

GOP leaders said to be weighing stopgap bill to avert Govt. shutdown to Feb 16th

Economic Data:

(DE) Germany Dec Final CPI M/M: 0.6% v 0.6%e; Y/Y: 1.7% v 1.7%e

(DE) Germany Dec Final CPI EU Harmonized M/M: 0.8% v 0.8%e; Y/Y: 1.6% v 1.6%e

(DE) Germany Dec Wholesale Price Index M/M: -0.3% v +0.5% prior; Y/Y: 1.8% v 3.3% prior

(FI) Finland Nov GDP Indicator WDA Y/Y: 3.5% v 3.2% prior

(FR) France Nov YTD Budget Balance: -€84.7B v -€77.1B prior

(CZ) Czech Dec PPI Industrial M/M: 0.3% v 0.1%e; Y/Y: 0.7% v 0.5%e

(IT) Italy Dec Final CPI M/M: 0.4% v 0.4% prelim; Y/Y: 0.9% v 0.9% prelim; CPI Index (ex-tobacco): 101.1 v 100.8 prior

(IT) Italy Dec Final CPI EU Harmonized M/M: 0.3% v 0.3% prelim; Y/Y: 1.0% v 1.0% prelim

(UK) Dec CPI M/M:0.4 % v 0.4%e; Y/Y: 3.0% v 3.0%e; CPI Core Y/Y: 2.5% v 2.6%e; CPIH Y/Y: 2.7% v 2.8%e

(UK) Dec RPI M/M: 0.8% v 0.6%e; Y/Y: 4.1% v 3.9%e, RPI-X (ex-mortgage interest payment) Y/Y: 4.2% v 3.9%e, Retail Price Index: 278.1 v 277.6e

(UK) Dec PPI Input M/M: 0.1% v 0.4%e; Y/Y: 4.9% v 5.3%e

(UK) Dec PPI Output M/M: 0.4% v 0.2%e; Y/Y: 3.3% v 2.9%e

(UK) Dec PPI Output Core M/M: 0.3% v 0.2%e; Y/Y: 2.5% v 2.3%e

(UK) Dec ONS House Price Index Y/Y: 5.1% v 4.2%e

(ZA) South Africa Nov Total Mining Production M/M: % v 3.4% prior; Y/Y: % v 5.1%e

Fixed Income Issuance:

(SE) Sweden opened its book to sell EUR-denominated Apr 2023 notes; guidance seen -26bps to mid-swaps

(BE) Belgium Debt Agency (BDA) opened its book to sell EUR-denominated Jun 2028 OLO bond; Guidance seen -15bps to mid-swaps

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2030, 2040, 2044 and 2048 bonds

(ID) Indonesia sold total IDR25.5T vs. IDR17T target in 2018, 2019, 2028, 2033 and 2038 bonds

(ES) Spain Debt Agency (Tesoro) sold total €4.17B vs. €3.5-4.5B indicated range in 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.4% at 399.6 , FTSE +0.2 at 7782, DAX +0.8% at 13302, CAC-40 +0.4% at 5531 , IBEX-35 +0.6% at 10530, FTSE MIB +0.6% at 23690 , SMI +0.2% at 9560, S&P 500 Futures +0.5%]

Market Focal Points/Key Themes: European Indices trade higher across the board, with the Dax outperforming following weakness yesterday, after higher closes in Asia and stronger indicated opens in the US. Retail names including Hugo Boss, Dunelm, Lindt and JD Sports reported prelim results, while CGG outperforms in France after strong Revenue growth with shares advancing over 15%. Elsewhere Fiat shares decline slightly after CEO Marchionne says he has no intention to break up the group. Looking ahead to the US morning, Citigroup are set to report alongside United Health among others.

Movers

Consumer Discretionary [ Hugo Boss [BOSS.DE] +2.4% (Prelim Earnings), JD Sports [JD.UK] +7.4% (Trading update), Lindt [LISP.CH] -1.7% (Earnings), Premier Foods [PFD.UK] +3.2% (Trading update), Marimekko [MM01.FI] +6% (Prelim earnings), Greggs [GRG.UK] +3.2% (Trading update)]

Industrials [ Fiat Chrysler [FCA.IT] -1.4% (Has no intention to break up group)]

Energy [CGG [CGG.UK] +18% (Prelim earnings)]

Materials [Rio Tinto [RIO.UK] -1% (production update)]

Speakers

EU's Tusk reiterated that UK needed to offer more clarity on future ties

Germany Berlin SPD said to reject coalition talks with Merkel bloc citing results of the exploratory talks (had Saxony-Anhalt state SPD reject it over the weekend)

Russia Fin Min Siluanov: Russia would be priority buyers of new Eurobonds. To do everything to provide RUB currency (Ruble) with stability and reiterated could spend its reserves if sanctions are expanded

Bank of Korea (BOK) Dec Minutes: Several members suggest keeping CPI target at 2% (**Note: BOK current 2% inflation target is for the 2016-18 period. BOK to set a new target this year for 2019)

China sovereign rating agency Dagong cuts US sovereign rating to BBB+ from A-; Outlook Negative

Currencies

USD weakness tried to find a reprieve in the session. Dealers noted that the greenback's global supremacy to be challenged by the yuan as the pricing medium for energy and other key industrial commodities. Yuan currency strength leaves dealers pondering over China's line in the sand. The USD also faced headwinds as US GOP leaders faced its most difficult shutdown deadline yet

EUR/USD retraced from recent highs just under the 1.23 area. German SPD party showing divide on alliance with Merkel. Germany Berlin SPD said to reject coalition talks with Merkel bloc citing results of the exploratory talks (had Saxony-Anhalt state SPD reject it over the weekend). The recnt EUR's rise seemed to be accepted by the ECB. Hansson's comments that "Euro appreciation no threat to inflation outlook" came just as the market had pushed the currency to the highest level since the ECB began its QE

GBP/USD consolidated in the session after testing above 1.38 on Monday following reports late last week that Netherlands and Spain were open to a deal for Britain to remain as close as possible to the trading bloc crushed short positions. Focus was on UK inflation data as the Dec CPI moved off five year highs as expected to 3.0%. Pair roughly steady at 1.3770 ahead of the NY morning.

Fixed Income

Bund Futures trades up 29 ticks at 160.69 as the bund rally tries to extend. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 123.96 up 23 ticks as UK inflation comes in mildly cool. Support continues to stand at 123.55 then 122.83, with upside resistance at 124.25 then 124.96.

Tuesday's liquidity report showed Monday's excess liquidity rose to €1.874T from €1.871T prior. Use of the marginal lending facility fell to €286M from €98M prior.

Corporate issuance was light with the US markets closed for holiday.

Looking Ahead

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO)

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

06:00 (TR) Turkey to sell Zero Coupon 2019 Bonds

06:00 (IE) Ireland Dec CPI M/M: No est v -0.2% prior; Y/Y: No est v 0.5% prior

06:00 (IE) Ireland Dec CPI EU Harmonized M/M: No est v -0.1% prior; Y/Y: No est v 0.5% prior

06:00 (PT) Portugal Dec PPI M/M: No est v 0.5% prior; Y/Y: No est v 3.2% prior

06:00 (IL) Israel Q3 Final GDP Annualized Q/Q: No est v 0.9% prelim; Y/Y: 3.5%e v 3.5% prelim

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction

07:00 (IS) Iceland Dec Unemployment Rate: No est v 2.1% prior

08:00 (PL) Poland Dec CPI Core M/M: 0.1%e v 0.1% prior; Y/Y: 0.8%e v 0.9% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Jan Empire Manufacturing: 19.0e v 18.0 prior

09:00 (EU) Weekly ECB Forex Reserves

09:00 (NZ) Fonterra Global Dairy Trade Auction

11:30 (US) Treasury to sell 4-Week Bills

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

12:00 (CH) SNB's Jordan in Zurich

GBP/USD Holds Ground After Hitting 1.38, USD Picks Up

UK inflation figure to go unnoticed as investors focus on negotiations

After printing a new multi-month high on Monday, the pound sterling has stabilised gains at around $1.3785. Since the beginning of the year, the pound sterling and the single currency have been moving side by side, suggesting that the market was more focused on the Trump situation rather than the divorce between the EU and the UK. In our opinion, Brexit risks are currently underestimated and investors seemed to have forgotten that the EU has the upper hand and is currently taking a tougher stance on transition talks.

December inflation figures are due for release this morning. No major surprise is expected: the headline measure should eased to 3%y/y from 3.1% in November. The core measure, which excludes the most volatile components, is anticipated to come in at 2.6%y/y, down from 2.7%. Despite the improving inflation outlook, there is little chance that the BoE would step in any time soon as only two to three hikes are expected over the next 36 months. Therefore, we remain cautious regarding further GBP appreciation.

Is an US bond market crash a realistic scenario?

Since the recent US government bonds yield hike of last week (2-year government bond rates reaching above 2%, a 10 years high) and the market excitement that followed, coupled with possible Japanese and European central bank policy tightening, we could wonder whether we might be expecting an imminent US bond market crash in the next couple of days ! All ingredients would be there: a sudden US government bond rate hike increase, equity markets keep going up (hypothesis: the propensity of investors to take further risk for higher returns pushes bondholders to invest into equity markets), the timing of policy tightening can potentially become unpredictable.

From our perspective, Friday January 12th 2018 moves in the bond market were strongly influenced by December US core CPI growth (above expectations at 1.80%), coupled with strong monthly retail sales data (0.4%, on line with consensus) that signify faster-than-expected Fed policy tightening. Looking at the US 10-year and 2-year yields, we remain confident that as long as the yields range around the 3% and 2.50% respectively, the US bond market remains stable. We think that the US bond market conditions should rather be interpreted as positive and indicates that the US economy grows at an active pace. In any case, further rate hikes will expose the US government to higher interest rates, bearing in mind that the US government carries a national debt worth of USD 20 trillion that would remain expensive in the longer term.

USDCHF Tumbles Following Pullback Of 0.9840, Prints 4-Month Low

USDCHF has been underperforming in the past four days, breaking back below the strong psychological level of 0.9700 and challenged a fresh four-month low near the 0.9600 handle. When looking at the bigger picture the pair lacks a clear trend and has been consolidating within the 1.0340 and the 0.9420 barriers.

In the daily timeframe, prices had a pullback of the mid-level of the Bollinger band and the 40-simple moving average and based on the technical indicators, momentum remains to the downside. The MACD oscillator is falling and is strengthening its bearish movement below the trigger and zero lines, however, the RSI indicator is sloping slightly north but is holding in negative territory.

If price action remains below the lower band of the Bollinger band, further losses should see the September low of 0.9560 acting as a major support. A drop below the aforementioned level would reinforce the bearish structure in the short-term and the way towards the next key support of 0.9420.

In the event of an upside reversal, a break above 0.9700 would shift the short-term outlook to a more neutral one as it could push the pair to the 0.9840 resistance level.

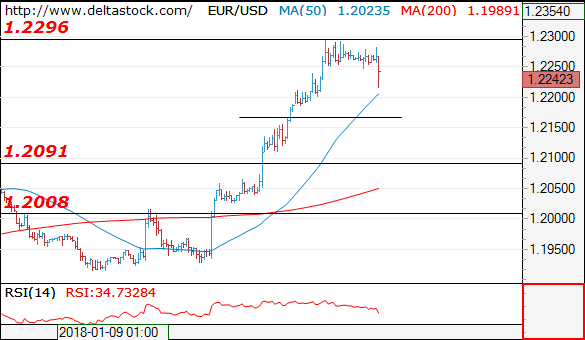

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2242

The violation of 1.2250 support signals a corrective pullback, towards 1.2165 and 1.2090 later on. Crucial on the upside is 1.2280.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2300 | 1.2500 | 1.2165 | 1.2090 |

| 1.2400 | 1.2500 | 1.2090 | 1.1910 |

USD/JPY

Current level - 110.72

The downtrend is still intact and current rebound after 110.30 should be considered corrective, preceding another dip to 109.50. Key resistance lies at 111.00 and crucial on the upside is 111.70.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.00 | 111.70 | 110.00 | 109.50 |

| 111.70 | 113.75 | 109.50 | 109.50 |

GBP/USD

Current level - 1.3781

I favor a break through the intraday support at 1.3765 to initiate a slide towards 1.3700 and 1.3660 static support. Crucial on the upside is 1.3818 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3800 | 1.3800 | 1.3765 | 1.3611 |

| 1.3800 | 1.4000 | 1.3700 | 1.3460 |