Sample Category Title

Summary 12/4 – 12/8

Monday, Dec 4, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Dec 5, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Dec 6, 2017

[php_everywhere] [/php_everywhere]

Thursday, Dec 7, 2017

[php_everywhere] [/php_everywhere]

Friday, Dec 8, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Data Continue to Provide Reasons for Cheer

U.S. Review

'Tis the Season to be Jolly

- Consumer confidence surged to a 17-year high in November, according to the Conference Board, which is good news at the start of the holiday shopping season.

- The personal income and spending report for October showed healthy income growth as spending receded from September's storm-induced surge to a still-respectable pace. Consumers also increased their saving rate from a cycle low in October. The ISM manufacturing index showed factory conditions continue to strengthen.

Data Continue to Provide Reasons for Cheer

The consumer was in good spirits heading into the last quarter of the year, according to most of the new economic data this week.

Shoppers in the new housing market may be one exception, however, as October's new home sales report suggests that the market was very competitive and there is little relief ahead. The pace of new sales accelerated to the fastest of the current cycle, as product was snapped up even before construction. Some of the uptick may be traced to seasonal factors. The largest gains were in the Northeast and Midwest, which are smaller and susceptible to large seasonal swings. Still, not seasonally adjusted gains were also strong in all four regions. Attesting to the strong demand, homes where construction had not yet started accounted for the entire rise in new homes sold and almost all of the increase in forsale inventory on the market. At October's pace of new home sales, there were just 4.9-months of inventory, down from 5.2 in September. The inventory of completed homes was unchanged. Such fundamentals should keep developers in good spirits this winter.

The Conference Board provided the most recent evidence that consumer confidence remains high, with its headline index registering a 17-year high in October. Confidence stemmed from a combination of the strong labor market and financial gains improving consumers' assessment of the present situation, as well as rising expectations about the future. There has been a marked uptick in the expectations index in recent months. Apparently any partisan bickering has not deterred consumers' optimistic outlook for tax cuts. The rising stock market and home values are also likely boosting their outlooks. Consumers' buying plans for major appliances increased to 52 from 48.8, which should give retailers reasons for cheer this holiday shopping season.

October's report on personal income and spending suggested consumers should have the means to act on surging confidence. Disposable personal income increased another 0.5 percentage points in October, building on September's 0.4 percent increase. Inflation trimmed some of October's rise, but the 0.3 percent increase in real disposable income was a welcome lift from essentially flat growth since May. The consumption expenditures side of the report was more a come-down story from September's 0.9 percent hurricane-induced lift. Spending in October increased a more modest 0.3 percent or 0.1 percent in real terms. The saving rate increased a bit in October to 3.2 percent from a cyclelow of 3 percent.

All told, the personal income and spending story in October gave reason for cautious optimism for spending in the last quarter of the year. The fundamentals are aligned to support a strong showing for holiday sales, from the improving labor market and consumers' assessment of current financial conditions to their high expectations. October's solid bump in disposable income was a welcome change as income growth has been somewhat of a Scrooge in recent months. The spending picture looks bright going into the holiday sales season.

U.S. Outlook

International Trade • Tuesday

The trade deficit rose slightly in September to $43.5 billion. Exports for the month grew 1.1 percent while imports rose 1.2 percent. Exports were boosted, in part, by stronger industrial supplies while the stronger import growth was supported by an improvement in capital goods and industrial supplies. For the last three quarters net exports have marginally added to headline GDP growth. We expect that trend to reverse course in the fourth quarter as strong domestic demand lifts the growth rate of imports above than the more modest pace of export growth. We expect the trade deficit to widen further in October to $47.4 billion. For the fourth quarter as a whole, we expect net exports to subtract 0.2 percentage points from headline GDP growth. This trend is expected to continue into next year as the pace of domestic demand is expected to lead to a faster pace of imports than exports.

Previous: -$43.5 Billion Wells Fargo: -$47.4 Billion Consensus: -$47.0 Billion

ISM Non-Manufacturing Index • Tuesday

ISM's non-manufacturing index climbed higher in October to 60.1 from September's reading of 59.8. The index was lifted by better current activity and employment. Several respondents reported greater activity related to hurricane recovery efforts. The more forward-looking new orders component pointed toward continued solid growth, at 62.8, only slightly below the 63.0 reading in September.

Looking ahead to November's reading, we expect the index to pull back slightly to 59.7 as some of the hurricane effects begin to subside. We continue to expect the service sector to lead growth in employment as the year progresses. The continued strength in the service sector will also continue to be a key driver of economic activity going forward and supports our forecast for 2.1 percent GDP growth in the fourth quarter of this year.

Previous: 60.1 Wells Fargo: 59.7 Consensus: 59.0

Employment • Friday

Nonfarm employment bounced back in October following a disappointing reading in September related to post-hurricane effects. Nonfarm payrolls rose 261,000 in October following a gain of just 18,000 in September. The unemployment rate continued to fall, reaching a cycle low of 4.1 percent. A bit more disappointing was the flat average hourly earnings reading following a 0.5 percent rise in September. We expect nonfarm payrolls to rise by 220,000 in November, which should keep the unemployment rate steady at 4.1 percent. Overall, job growth should average 197,000 in the fourth quarter, and we expect the unemployment rate to end the year at the current 4.1 percent rate. We continue to expect the pace of job growth to gradually decelerate next year as slack in the labor market continues to diminish. By the end of 2018 we see the unemployment rate at 3.9 percent.

Previous: 261,000 Wells Fargo: 220,000 Consensus: 200,000

Global Review

Mixed Global Data; Brazil Back from the Brink

- In Germany, real retail sales fell 1.2 percent sequentially in October after a relatively strong print in September, up 0.5 percent.

- Better news came from the important Chinese economy with a slight improvement in the official manufacturing PMI index to 51.8 from 51.6 in October.

- Although the Brazilian economy grew less than what markets were expecting in Q3, up only 0.1 percent sequentially versus consensus expectations of 0.3 percent, growth in Q2 was revised up from an original 0.2 percent to a 0.7 percent improvement. For the year as a whole this will make a big difference.

Mixed Economic Signals Across the Global Economy

This week we saw some mixed signals from the global economy. In Germany, real retail sales fell 1.2 percent sequentially in October after a relatively strong print in September, up 0.5 percent. This was the weakest month-on-month performance since November 2016 when real retail sales declined 1.7 percent. The decline in October brought the year-over-year rate into negative territory, down 1.4 percent after printing a strong increase of 4.1 percent in September. However, the behavior of both the month-on-month as well as year-over-year rates is not atypical for this German series so it should not dim the prospects for a continuation of economic growth in the largest economy of the Eurozone.

Better news came from the all-important Chinese economy with a slight improvement, to 51.8 from 51.6 in October, of the official manufacturing PMI index. The difference with the previous month is negligible, but the fact that consensus was expecting a slight decline was enough to improve the view regarding this important sector in China. The Caixin manufacturing PMI, which includes small and medium-sized manufacturing firms typically not included in the official PMI, was slightly lower in November, to 50.8 versus 51.0 in October but still above the 50 demarcation point.

The Brazilian Economy: Back from the Brink

In Brazil the data were better than expected. We have been at the top of the consensus expectations for the whole year on Brazilian GDP but are probably going to fall short when all is said and done. After the release of Q3 results markets will likely considerably re-price growth in GDP higher for this year and next. Although the Brazilian economy grew less than what markets were expecting in Q3, up only 0.1 percent sequentially versus consensus expectations of 0.3 percent, growth in Q2 was revised up from an original 0.2 percent to a 0.7 percent improvement which, for the year as a whole, will make a big difference. The economy has already grown 0.6 percent year to date and that is our current forecast for this year, which would mean that economic growth in Q4 will make for a stronger performance for the year as a whole.

The details were even more encouraging as economic growth was kept relatively low by a strong increase in real imports of goods and services, which increased 5.7 percent versus a year earlier and 6.6 percent sequentially, not annualized. Recall that imports enter the GDP calculation with a negative sign so imports are a subtraction from economic growth. At the same time, real exports of goods and services were very strong, up 7.6 percent versus a year earlier and 4.1 percent sequentially. Real personal consumption expenditures were up 2.2 percent year over year while they were up 1.2 percent sequentially and not annualized. Meanwhile, although real gross fixed investment was still negative on a year-earlier basis, down 0.5 percent, it surged 1.6 percent sequentially, which means that investment is on track to start contributing to GDP growth in Q4. All these data points show an economy that is, finally, back from the brink.

Global Outlook

Brazil Industrial Production • Tuesday

Brazilian industrial production has continued its steady grind higher, returning to positive year-over-year growth back in May and trending up over the past couple months. Industrial output was up 0.8 percent sequentially in Q3 and 0.4 percent year over year, with annual gains across all three sectors of mining, manufacturing and construction.

The Brazilian economy was decimated by the commodity price collapse, the slowdown in global growth that occurred over the 2015-2016 period plus a severe political crisis. As we highlighted in this week's international review, export growth was strong in Q3, likely aided by healthy growth in external demand among the world's economies, and fixed investment spending surged in the quarter. These trends bode well for continued momentum in Brazilian industrial production headed into the fourth quarter.

Previous: 0.2% Consensus: 0.1% (Month-over-Month)

Bank of Canada Meeting • Wednesday

The Bank of Canada (BoC) surprised some back in September when it chose to increase its overnight lending rate 25 basis points, bringing the policy rate to 1.0 percent. Real economic growth was especially robust in Canada in the first half of the year, averaging a more than 4 percent annualized rate.

Data released this morning showed Canadian real GDP decelerating from the breakneck pace seen through the first half of the year. Economic growth coming back down to earth should reassure monetary policymakers in Canada that a gradual path of monetary policy tightening is warranted. As the BoC's last policy statement from October highlighted, wage and other data indicate there is still some slack in the labor market, and household spending is likely more sensitive to interest rates than in the past due to high debt levels. We do not expect a rate hike at the December meeting and look for the BoC to roughly keep pace with the Fed next year.

Previous: 1.00% Wells Fargo: 1.00% Consensus: 1.00% (Overnight Lending Rate)

U.K. Industrial Production • Friday

The factory sector in the United Kingdom strengthened in the third quarter, with manufacturing output rising 0.4 percent or better in each month of the July-September period. Capital goods production in particular has been strong, up nearly 7 percent year over year through September, an encouraging sign given the concerns surrounding investment spending in the wake of Brexit.

The depreciation of the pound that has spurred above-target inflation in the United Kingdom this year has likely provided a boost to U.K. manufacturers looking to export their products abroad. The improving global growth environment, particularly across the English Channel in Europe, has also helped spur stronger factory sector output. Looking ahead, the depreciation effect on both inflation and manufacturing will likely begin to fade, which should produce a more balanced composition of economic growth as slower inflation improves purchasing power for consumers.

Previous: 0.7% Consensus: 0.0% (Month-over-Month)

Point of View

Interest Rate Watch

Yield Curve and Recessions

With all the commentary on the yield curve and recessions recently, we shall review some points we made in our empirical study released several months ago – Is the Yield Curve Enough to Predict Recessions?

Inverted Yield Curve Not a Leader

An inverted yield curve did not lead every recession—top graph. The yield curve inversion is neither a necessary nor sufficient condition for a recession. Moreover, the yield curve is neither causa remota nor causa proxima. For example, the long lead times for the recession of 1990, 2001 and 2007 intimate that the yield curve had little to do with any factor(s) that promoted the recession as causa proxima. In addition, the variable lead times throughout the table would imply that there is no reliable remote link that leads directly to a recession. The inverted yield curve appears as one factor, and just one factor, within a host of other factors that alters the economic/financial landscape. On a fundamental level, the yield curve reflects the underlying shift in both policy and private sector attitudes about the willingness to take on risk over time.

Recession–Lags are Long and Variable

As evidenced in the table at the right, the lag times between the appearance of the inverted yield curve and the recession are long and variable. Moreover, the lengths of an economic expansion also vary quite a bit so the length of time for an expansion or the lead time for the yield curve, or any set of indicators to signal recession, is likely to be highly variable simply given the complexity of the modern economy.

Our Probit model predicts the probability of a U.S. recession during the next six months. The model utilizes the LEI, S&P 500 index and Chicago-PMI employment index as predictors. Using the most recent data (October 2017), our model suggests a low chance of a U.S. recession during the next six months (0.20 percent probability, bottom chart). Therefore no recession clouds are looming over the next six months.

Credit Market Insights

Confident on Credit

Consumer confidence, as measured by the Conference Board, reached its highest level in 17 years in November. While the headline figure is encouraging, parsing through the individual questions can shed light on more specific confidence measures.

For example, the percent of consumers who plan to buy an automobile within six months continues to trend upward. Such sentiment is not unfounded, especially when the fed funds rate is just 1.25 percent and consumers are looking to lock in low rates before future rate hikes. In fact, consumers are increasingly turning to credit markets for auto purchases, and financers appear willing to provide credit, even as the average auto loan stretched to 67 months in Q2.

Likewise, the percent of consumers who plan to buy a home within six months climbed to 6.9 percent in November, the highest measure since the Great Recession. However, unlike the period leading up to the Great Recession, loan delinquencies continue to trend downward. In Q3 only 1.4 percent of mortgage loans were categorized as delinquent – the lowest rate for all household debt categories.

While lofty consumer confidence measures are often attributed to animal spirits and viewed as non-analogous to the underlying hard data, credit conditions in the consumer space appear to be healthy. We will keep a close eye on the net charge-off rates on consumer products as the Federal Reserve continues guiding rates higher.

Topic of the Week

Understanding the Tax Bill's Dynamic Score

Yesterday the Joint Committee on Taxation (JCT), Congress's official revenue-scorekeeper, released its "dynamic" score of the Senate GOP tax plan. In short, a dynamic score differs from a "static" score in that it attempts to account for changes to aggregate economic variables such as GDP and interest rates when estimating the revenue impact of a tax bill. The score from JCT showed the Senate plan increasing the deficit by roughly $1 trillion over the next 10 years amid GDP growth that is about 0.08 percentage points faster per year, on average (top chart).

A host of factors can influence the output of a dynamic score, but one of the most important factors that explain different outcomes is a phenomenon known as "crowding out." Crowding out occurs when an increase in the federal budget deficit leads more national savings to be used to buy Treasury securities rather than to fund private investment. The Congressional Budget Office, a cousin to the Joint Committee on Taxation, estimates that when the deficit goes up by one dollar, private savings rise by 43 cents and foreign capital inflows rise by 24 cents (as higher interest rates increase the incentive to save and attract foreign capital flows), leaving a net decline of 33 cents in savings available for private investment.

Some independent think tanks have also produced dynamic scores, with somewhat similar results. The Tax Policy Center and the Penn Wharton Budget Model produced estimates suggesting that the House-passed bill would lift growth by less than 0.1 percentage point per year. The Tax Foundation, a leading conservative think tank whose model assumes a much smaller crowding out effect, estimated the House bill would lift growth by about 0.3 percentage points per year over the long-run.

As we wrote in a piece earlier this year, with real potential GDP growth roughly 2 percent at present, the hurdles to sustained economic growth of 3 percent or more are high, even with optimistic assumptions about the possible growth effects from tax reform (bottom chart).

The Weekly Bottom Line: Tax Cuts Just Around The Corner

U.S. Highlights

- The prospect of corporate tax cuts led both the Dow Jones Industrial Average and the S&P 500 to record highs this week, with financial stocks outperforming substantially.

- Economic data was supportive, with third quarter real GDP being revised up to 3.3% annualized, as business investment came in stronger than initially thought.

- Incoming Fed Chairman Jerome Powell stated that "conditions are supportive" of a December rate hike, and we expect the Fed to proceed with one, followed by two more in 2018.

Canadian Highlights

- The Canadian economy created a whopping 80k jobs in November, pushing the unemployment rate down to 5.9% - the lowest level in nearly a decade.

- Economic growth came in largely as expected in the third quarter at 1.7% annualized. While this is a marked deceleration from the prior quarter, it signals a return to a more sustainable pace of growth.

- OPEC and its allies agreed to extend production cuts until the end of 2018 - a timeframe the group expects will allow the global oil market to balance.

U.S. - Tax Cuts Just Around The Corner

The prospect of corporate tax cuts made for another strong week in equity markets. Investors flocked to financial shares, leading both the Dow Jones Industrial Average and the S&P 500 to record highs. Financials have posted stellar earnings growth this year and are among the corporations that stand to benefit the most from the proposed tax cuts. Consumer discretionary stocks were also in high demand, following record-breaking estimates of Black Friday and Cyber Monday sales. Treasuries, on the other hand, sold off this week, sending the benchmark ten-year yield above 2.4% on Thursday, the highest level in over a month. These positive developments led the greenback higher initially, but the gains were pared by the end of the week.

Economic data released this week also supported investor sentiment, with third quarter real GDP revised up to an impressive 3.3% as business investment accelerated (even more than previously estimated), with firms ramping up expenditures on equipment notably (Chart 1). This marks the strongest two consecutive quarters of growth for the American economy in three years. Momentum in business investment is expected to continue, with shale oil production likely to be a key contributor. Producers have ramped up activity this year in response to a rising price of WTI crude oil. OPEC's commitment to extend supply cuts through 2018, announced this week, should maintain this momentum. As a result, the upside for the price of crude oil will be limited; we expect the price of WTI crude to sit in the US$50-55 range as the market balances out.

Consumers are also likely to maintain their pivotal role in the economic expansion alongside businesses. Consumer spending slowed in October, after a bump in the prior month as a result of hurricane-damaged vehicle replacement. With continued job growth and accelerating wages, consumer spending should bounce back in the months ahead. On the inflation front, core PCE price growth held steady at 1.4% (year-on-year) in October, with an uptick in the following month looking increasingly likely as industry contacts reported strengthening price pressures in November's Beige Book (Chart 2). Producers across a range of industries including manufacturing and transportation reported passing on increases in input costs to selling prices, ensuring that inflation will turn higher in the near future. Several FOMC voting members also expressed their agreement with this view in speeches this week.

Incoming Fed Chairman Jerome Powell stated that "conditions are supportive" of a December rate hike at his confirmation hearing on Tuesday. Mirroring this view were Yellen and Kaplan in their speeches this week, in contrast to Kashkari who would like to see firmer evidence of inflationary pressures building before proceeding with a hike. At this point, markets are fully pricing in a December hike and we expect the Fed to proceed with one, followed by two more in 2018. Making this scenario increasingly likely is progress on the tax reform front which will require faster monetary policy normalization in order to temper the potential inflationary pressures.

Canada - Employment Stealing the Spotlight

It was a busy morning on the Canadian data front, with third quarter GDP and November employment figures released. The Canadian dollar shot up by more than a cent following the data releases, recouping most of the week's losses. Meanwhile the S&P/TSX remained down on the week on softer oil prices ahead of the OPEC meeting.

The employment report stole the spotlight this week, with a stunning 80k job added in November. This pushed the unemployment rate down to 5.9%, which is the lowest level seen in nearly ten years and a full percentage point below the level at the start of the year. Wage growth accelerated to 2.7% during the month, which is a stark improvement relative to the 0.6% pace in April. All told, there is little doubt that the Canadian economy is operating at full capacity.

On the other hand, economic growth in the third-quarter came in largely in line with expectations, at 1.7% (annualized). This is a marked slowdown from the stellar 4.3% pace recorded in the prior quarter, reflecting a sharp pullback in exports that was only partly offset by continued strength in consumption and an uptick in government investment. On the whole, the deceleration in the third quarter was expected and is consistent with a return to a more sustainable pace.

These reports will not go unnoticed by the Bank of Canada when deciding on interest rates. Strength in the domestic economy, characterized by solid job and wage gains, appears supportive of higher rates, with a rate hike likely in the coming months.

In other news, during the much-anticipated OPEC meeting yesterday, the group plus its non-OPEC allies extended production cuts through the end of 2018, as expected. Expectations for such an extension had been a key driver behind the recent uptick in prices to a 2½ -year high and the group did not disappoint. Yesterday's agreement also included a collective cap for Libya and Nigeria set above their current combined production levels.

Overall the oil market remains abundantly supplied, with inventories sitting well above their 5-year average. That said, inventories have been falling and with the extension of the production cuts, OPEC expects the remainder to be eliminated by the end of next year. Of course, US shale production - which is sitting near a record high - remains the wild card. With prices on the rise, hedging activity has surged, up nearly 150% in the third quarter. This should enable production to continue to rise in 2018 even if prices give back some of their recent gains. In Canada, production is set to grow over the next year as well, as a couple of new projects ramp up.

Overall, prices have likely been bid up too high given market fundamentals, suggesting that some downside could be in store going forward. Ultimately, we expect the WTI benchmark to sit in the US$50-55 per barrel range over the coming year as the market moves back into a more balanced position.

U.S.: Upcoming Key Economic Releases

U.S. Employment - November

Release Date: December 8, 2017

Previous Result: 261k, unemployment Rate 4.1%

TD Forecast: 175k, unemployment Rate 4.2%

Consensus: 198k, unemployment Rate 4.1%

We expect nonfarm payrolls to advance by 175k in November. Data on persons not at work due to bad weather suggest that hurricane impacts should have faded by this month, allowing payrolls to print closer to their current trend in the 150-200k range. Upward revisions to the prior two months are also likely. Meanwhile, labor market indicators (regional Fed surveys and consumer confidence) remained supportive of solid job growth.

We expect the unemployment rate to tick higher to 4.2% from 4.1%, given the outsized decline in labour force participation that has the potential to correct. We also look for a relatively modest 0.2% m/m increase in average hourly earnings, as calendar effects are less favourable this month. Still, that should leave earnings tracking higher on a y/y basis at 2.6% vs 2.4%.

Canada: Upcoming Key Economic Releases

Canadian International Trade - November

Release Date: December 5, 2017

Previous Result: -$3.2bn

TD Forecast: -$2.6bn

Consensus: N/A

TD looks for the merchandise trade deficit to narrow to $2.6bn in October on a rebound in exports, which should be partially offset by rising imports. Exports should see a broad increase due to higher factory prices, which are largely a symptom of CAD weakness, though we will need to wait another month to see a full rebound in vehicle exports. Labour disruptions in auto production were not resolved until mid-month and advance US imports were flat on the month. Exports of energy products are likely to see a nominal gain while a sharp increase in residential construction south of the border should support exports of building materials. Imports should see a more modest increase which will help to narrow the deficit by $600m.

Trump, US Jobs and Brexit to Guide Markets

Fundamentals and geopolitics to share spotlight on US jobs week

The USD was on a rollercoaster in the last week of November as the optimism surrounding the Senate tax reform bill was quickly eclipsed by the news that former National Security Adviser to the White House was prepared to testify that the Trump team directed him to contact Russian operatives. The US dollar is now mixed on a weekly basis against major currencies with an eye on more developments on the political front and the release of employment data in the US.

The Bank of Canada (BoC) will release its benchmark rate statement on Wednesday, December 6 at 10:00 am EST. The central bank is anticipated to keep rates unchanged at 1.00 percent after already hiking twice in 2017. Canadian jobs data defied estimates and gained 79,500 jobs in November raising the probability of the next Canadian interest rate hike coming sooner rather than later, but the data will not influence the decision on Wednesday.

The U.S. Bureau of Labor Statistics will release the non farm payrolls (NFP) report on Friday, December 8 at 8:30 am EST. The US economy is forecasted to have added 200,000 positions in November. Once again the emphasis will be on average hourly wages for signs on inflationary pressure. While the market has already priced in a rate hike of 25 basis points in the next Fed meeting doubts remain on what the central bank will do in 2018. Weak inflation is the biggest argument the doves within the FOMC have used to debate waiting before raising rates again. Wages are forecasted to have gained 0.3 percent in the last month after a flat reading in October.

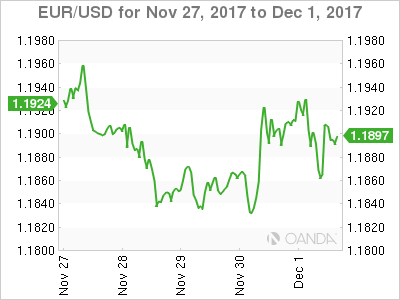

The EUR/USD lost 0.31 percent in the last five trading days. the single currency is trading at 1.1895 on Friday after geopolitical risk factors have put downward pressure on the dollar. The EUR was on a falling trend at the beginning of the week as the US tax reform in the US Senate was gathering momentum. The revelations that Michael Flynn would testify in the special counsel investigations on Russian collusion in the US presidential elections rocked the dollar and the stock market. The named thrown around in connection to Flynn and the Trump team is Jared Kushner.

The possible reversal of fortune on the Senate bill that is now facing more scrutiny as the crowdsourced efforts asking for more transparency could end up derailing the much awaited tax reforms. The tax reform bill is close to a vote and could pass as long as Republicans maintain a united front.

Trump took to twitter to also deny that Secretary of State Rex Tillerson has not been fired despite having differences, although he did tweet that he (Trump) calls the shots.

The first full week of December will be a quiet one for European releases, with the EU-UK Brexit negotiations taking the top spot. In the US the calendar will be focused on jobs data with the release of the ADP, unemployment claims and the heavyweight indicator, the U.S. non farm payrolls (NFP) to be released on Friday, December 8. Employment data is expected to remain strong and lead the way to the Fed meeting where it is expected they will announce their third interest rate hike of the year on December 13.

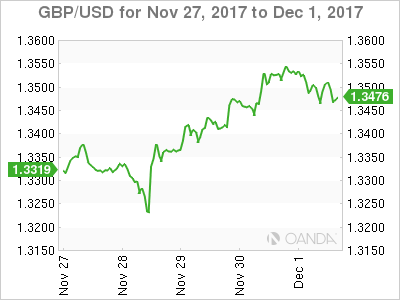

The GBP/USD gained 0.99 percent this week. The Pound is trading at 1.3470 on the back of a softer Brexit optimism. The upwards weekly move has not been one directional. The GBP is weaker on Friday as the European Union went on the record and stated that if Ireland cannot accept the UK's offer for its border then trade negotiations with the single market will not move to the next stage. The deadline for a border proposal is Monday and faced with the solidarity of the EU, Ireland holds the fate of the UK in its hands. The Irish border became a show stopping issue after the disastrous snap election results forced British Prime Minister Theresa May to partner with the Northern Irish Democratic Unionist Party (DUP). The DUP demand Northern Ireland be treated the same as the rest of Britain, not left behind in half EU, half UK.

The EU's backing of Ireland in the border issue puts more pressure on May and her government with the worst case scenario being the end of her rule. Cable touched daily lows at around 1.3640 despite strong manufacturing PMI data in November as Brexit negotiations are eclipsing fundamental data.

Gains on Purchasing Manager Indices in construction (Monday, December 4 at 4:30 am EST) and services (Tuesday, December 4 at 4:30 am EST) alongside an expected slowdown in manufacturing production prices in the United Kingdom are on the agenda for the week of December 4 to 8.

Oil surged on Friday as the decision by the Organization of the Petroleum Exporting Countries (OPEC) and Russia to extend its production cut agreement by 9 months combined with geopolitical risks being elevated in the US after the news broke that Michael Flynn pleaded guilty to lying to the FBI. West Texas Intermediate is trading at $58.12 and is almost back to the price levels where it opened on Monday.

The fact that the OPEC announcement was expected and already priced-in exacerbated market reactions to rumours about the duration and doubts that Russia will sign on for the full 9 months. Despite a positive move on the day of the announcement, a strong dollar led by tax reform optimism on Thursday put the price of energy at weekly lows.

Despite the united front shown in Vienna between the OPEC and other major producers, most notably Russia, there are various calls within the bloc to look for an exit strategy. Russia is keen to get back to full production, but for now will seek stability than profits. Nigeria and Libya who were exempt from the original production cut have now been limited to not exceed the levels from this year as compliance within the group will be a challenge.

US shale producers continue to ramp up production and free from weather disruptions will put pressure on crude prices that have been boosted by the effort put forth by the OPEC. The technology advances that made oil extraction cheaper created a sudden drop in prices as the OPEC sought to price them out of the market in a strategy that backfire by exchanging market share for profits.

Diplomatic stability within the producers organization will prove to be difficult as Saudi Arabia has taken a more aggressive role in domestic and regional politics which could pit it against number two and three producers Iraq and Iran.

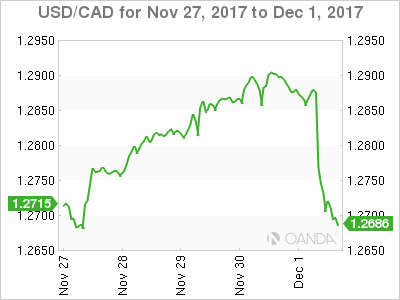

The USD/CAD lost 1.55 percent on Friday. The currency pair is trading at 1.2695 after the Canadian jobs number defied expectations with a 79,500 positions added in November. Monthly gross domestic product (GDP) came in higher at 0.2 percent but in fact confirmed the slowdown of the economy as the third quarter saw an expansion of 1.7 percent and a downward revision to the second quarter data to 4.3 percent. The Canadian economy grew a bit less than expected by the Bank of Canada (BoC) who had forecasted a 1.8 percent gain but beat the economist forecast of 1.6 percent. The number did validate the effective cool down of growth in Canada which puts the central bank on a more wait and see approach despite the solid gains seen in employment.

The loonie was on the back foot for most of the past week with the USD gaining 1.53 percent in the last 4 days on the market optimism that the Trump Administration could score a victory. Expectations of a rate hike by the U.S. Federal Reserve in December are high, and already priced into the pair, but the Bank of Canada (BoC) is seen more dovish by the minute. A new Reuters survey of 30 economists shows that there is little expectation of a rate move by the Canadian central bank in December, and a third see April at the earliest.

Factors such as the precarious state of the NAFTA renegotiations and evidence of the economy slowing down have cooled the BoC's desire to reduce further stimulus worried about the effect of higher interest rates on borrowers that hold record high levels of debt. The two data releases on Friday could confirm the headwinds facing the loonie, or in case they over perform expectations give the currency a boost against the US dollar.

Market events to watch this week:

Monday, December 4

- 4:30am GBP Construction PMI

- 7:30pm AUD Current Account

- 7:30pm AUD Retail Sales m/m

- 10:30pm AUD Cash Rate

- 10:30pm AUD RBA Rate Statement

Tuesday, December 5

- 4:30am GBP Services PMI

- 8:30am CAD Trade Balance

- 10:00am USD ISM Non-Manufacturing PMI

- 7:30pm AUD GDP q/q

Wednesday, December 6

- 8:15am USD ADP Non-Farm Employment Change

- 10:00am CAD BOC Rate Statement

- 10:00am CAD Overnight Rate

- 10:30am USD Crude Oil Inventories

- 7:30pm AUD Trade Balance

Thursday, December 7

- 8:30am USD Unemployment Claims

- 11:00am EUR ECB President Draghi Speaks

Friday, December 8

- 4:30am GBP Manufacturing Production m/m

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 8:30am USD Unemployment Rate

*All times EDT

ISM Manufacturing: Solid Gains, Solid Growth Ahead

Overall, the ISM purchasing managers index came in at 58.2 with solid gains once again in production, employment and orders. Input prices continue to show upward pressure and restraint on profits.

Despite Modest Retreat in Headline, Production Remains Strong

The ISM manufacturing index slowed ever so slightly in November to 58.2 from 58.7 (top graph). The composite index is coming off a cycle high of 60.8 in September and with a six-month average of 58.4, the index continues to signal firmness in the manufacturing sector. For the year ahead, we expect quarterly GDP gains of 2 percent or greater.

Subcomponent details are encouraging. The production index, for example, has been above 60 since June and came in at 63.9 in today's report for November; that's the highest reading since March 2011. Fourteen industries reported gains in production including paper, furniture, plastics & rubber and machinery.

As for employment, that index came in at 59.7, above its six-month average of 58.7 with 11 of 18 industries reporting employment growth. This is a plus for the employment numbers to be reported next Friday. Industries reporting gains in employment include textile mills, machinery, computer products and paper. We anticipate that job gains in the first half of 2018 will be in line with the 2017 pace and thereby support continued consumer income and spending gains.

New Orders—Signal of Growth Ahead

New orders came in at 64.0 in November, above the 63.4 for October and the 62.7 six-month average. This is a good signal of continued growth ahead (middle graph). Fourteen of 18 industries showed growth in orders, including electrical equipment, appliances, paper, furniture, plastics and machinery. The gains in new orders are solid and broadly based. Foreign sources of demand contributed to the overall strength in orders as new export orders came in at 56.0 in November, which was in-line with the six-month average. Eight industries reported growth in new export orders. The "backlog of orders" subcomponent came in at 55.0 in November. Rising backlogs are another forward indication that manufacturing production will continue ahead.

Input Cost Pressures Continue to Increase

Rising commodity prices have led to some cost pressures in the nation's factory sector and this is reflected in the 65.5 reading on prices paid (bottom graph). Fifteen of the 18 industries surveyed indicated paying higher prices for their inputs including plastics, textile mills, machinery, food & beverage and paper, curbing profit growth in these industries.

Commodities up in price included aluminum (13 straight months), corrugated boxes (14 straight months), caustic soda (5 months) and hot rolled steel (12 months). The rise in the ISM prices index does intimate upward pressure on core finished goods in the producer price index.

Canadian Growth Slows, but Not as Much as Expected

A spate of indicators released this morning show continued strength in Canadian domestic demand, improved business activity and a dip in the unemployment rate to a 9-year low.

Slower Growth Sustained by Domestic Demand

Real GDP growth in Canada came in at an annualized pace of 1.7 percent in the third quarter. In each of the first two quarters of the year, Canada boasted the fastest growth of any G7 economy, so this is clearly a slowing in the growth rate. That said, the consensus had anticipated an even bigger slowdown, so today's report is a bit better than expected.

Business spending declined in seven out of eight quarters in 2015 and 2016 before bouncing back in the first couple of quarters this year. Business investment picked up, growing at a 3.5 percent annualized pace and lifting headline growth by 0.7 percentage points.

Inventories: What Goes Up…

Inventories increased for the fifth time in the past five quarters. In fact, stockpiles have been growing in double digits on a percentage basis in each quarter this year. As a result, inventories added another 1.1 percentage points to the overall growth rate.

We are concerned that a reversion to the trend-pace of inventory investment will eventually result in a drag on GDP. A mere slowing in the pace of inventory investment translates into a drag on growth in GDP accounting. For example, since the start of 2010, the average pace of inventory investment has been 6.7 percent. If inventories grew at that pace in Q4, it would result in a drag on GDP growth of more than 2.5 percentage points. We do not yet have much data to form an outlook on fourth quarter inventories, but it is something that merits watching closely.

More Help from the Consumer, but Trade Rains on the Parade

Consumer spending continued to expand just as it has in every period since the second quarter of 2009. We have been cautioning in recent quarters that household debt levels in Canada are getting worryingly high. If Canadian households begin to hold back on outlays in an effort to bring down debt levels, it would clearly be a headwind to the uninterrupted run of consumer spending growth. For now, the 4.0 percent annualized pace of spending was sufficient to lift third quarter growth by 2.3 percentage points.

So if all these measures of domestic demand were positive, where was the weakness? In a word: trade. A steep decline in exports and little change in imports resulted in a 3.4 percentage point drag from net exports.

In separate reports also released this morning, we learned that Canadian jobs increased 79.5K and the unemployment rate fell to 5.9 percent, a nine year low, and the Markit Canada Manufacturing PMI climbed to 54.4.

The Canadian dollar strengthened on this morning's news, but we still expect the Bank of Canada to remain on hold at its meeting on Wednesday of next week.

Week Ahead – RBA and BoC Meet; Aussie GDP and US Jobs Report Eyed

The first week of December will get off to a packed start with a number of key indicators and central bank meetings set to keep traders busy. Among the highlights are Australian GDP figures for the third quarter, European industrial output figures and US nonfarm payrolls. Also in focus are central bank meetings in Australia and Canada.

RBA to hold rates as Aussie GDP rebounds

The Australian dollar will be under the spotlight next week as a flurry of economic data is due out of Australia as well as a policy meeting by the Reserve Bank of Australia. Monday's business inventories numbers and Tuesday's current account figures for the third quarter will be a good indication to Wednesday's GDP report. Australia's economy is expected to have expanded by 0.7% in the third quarter. This is slightly below the prior quarter's 0.8% rate but it takes the annual pace up to 3.0% from 1.8% as last year's shock contraction in third quarter GDP drops out of the calculation.

A stronger reading may provide the aussie with a bit of a boost but is unlikely to change the bearish outlook for the currency given the subdued inflation picture in the country. The RBA should give its latest thoughts on the growth and inflation outlook on Tuesday when it announces its latest policy decision. No change in rates is expected from the RBA but its statement will be scrutinized for any shift in its language. Also important will be the October retail sales and trade balance on Tuesday and Thursday respectively.

Apart from the Australian data, the aussie will also have to contend with Chinese releases next week (the aussie is regarded as a liquid proxy for China's economy due to Australia's export dependency with China). Friday will see the release of the monthly trade data for November, which should indicate how exports and imports performed during the month. They will be followed by November producer and consumer prices on Saturday.

Sticking to Asia, Japan will publish its second estimate of GDP growth in the third quarter on Friday. An upward revision to the preliminary estimate of 1.4% is likely after data this week showed business capital expenditure accelerated to 4.2% in the third quarter from 1.5%.

Bank of Canada to stand pat

A December rate hike by the Bank of Canada was looking like a strong possibility not that long ago but those expectations have receded on dovish remarks by BoC officials and softer economic data in recent weeks. The Bank is widely anticipated to keep its overnight rate unchanged at 1% for the second straight meeting on Wednesday. However, it may provide some forward guidance about the timing of the next rate hike in its statement, which may not be that long away given this week's November employment and third quarter GDP numbers that surprised on the upside. A hawkish statement could help the Canadian dollar move further away from one-month lows versus its US counterpart.

Industrial output and Brexit in focus in Europe

The Eurozone economy has been going from strength to strength in 2017 and data due next week is expected to further confirm this view. The third estimate of Eurozone growth in the third quarter is expected to remain unrevised at 0.6% on Thursday. The final readings of the services and composite PMIs are also forecast to show no revision on Tuesday. Other business surveys out of the euro area will include the sentix index on Monday, with a slight fall expected, as well as producer prices and retail sales figures on Monday and Tuesday respectively.

Germany and France will publish industrial production and trade figures for October. German industrial output is expected to see a 1.1% month-on-month rebound on Thursday after a sharp drop in the prior month. French output is forecast to see a small dip during the month in Friday's numbers.

Across the channel, the UK will also release industrial output and trade figures. As a slowdown in consumer spending drags on the dominant services sector, the manufacturing sector is starting to become a bright spot in the British economy as rising global demand and a weaker sterling finally start to lift UK exports. Both industrial and manufacturing output are expected to rise by just 0.1% m/m in October, but the annual rates should quicken to the fastest since late 2016. Also to watch next week are the construction and services PMIs out on Monday and Tuesday, respectively.

A bigger potential mover for the pound though will likely be the outcome of the meeting between British Prime Minister Theresa May and European Commission President Jean-Claude Juncker and EU chief Brexit negotiator Michel Barnier in Brussels on Monday. After this week's headlines that the UK and the EU are very close to an agreement on the Brexit divorce settlement, any setbacks in the negotiations over the next seven days could knock sterling sharply below its current two-month highs versus the US dollar.

US hourly earnings eyed in NFP report

Friday's nonfarm payrolls report will be the main focus in next week's US calendar. But before then, there will be plenty of other data to occupy investors. October factory orders will start the week on Monday, followed by the goods trade balance on Tuesday. The ISM non-manufacturing PMI for November will also be watched on Tuesday, which hit a 12-year high in October. The preliminary reading of the University of Michigan's consumer confidence index on Friday will be important too but all eyes will be on the November jobs report.

The US economy added 261k jobs in October as the labour market bounced back from the disruption caused by the hurricanes in September. Jobs growth is forecast to ease to around 188k in November, though that's still a strong figure considering the economy is close to full employment. The unemployment rate will likely remain steady at a 17-year low of 4.1%.

With recent US data already pointing to continued solid growth in the US and a December rate hike fully priced in by the markets, the NFP report is unlikely to be a game changer unless there was to be a big surprise in wage growth. Average hourly earnings are expected to rise by 0.3% m/m in November, up from 0% in October and pushing the annual rate to 2.9%, which would be the highest in nearly a year. Faster wage growth ahead of the December FOMC meeting when Fed policymakers publish their quarterly projections on the rate path could lead to a more hawkish dot plot chart.

US: Manufacturing Activity Softens a Touch in November But Remains Healthy

The Institute for Supply Management (ISM) index of manufacturing fell 0.5 points to 58.2 in November, largely in line with market expectations for a 58.3 reading. Nevertheless, the index remains well in expansionary territory - a fifteenth consecutive month of growth.

The report details were mixed, with declines in the components previously affected by hurricanes offsetting gains in more forward looking indicators. For instance, both supplier deliveries (-4.9 points to 56.5) and inventories (-1 to 47) declined from hurricane-elevated levels. In contrast, production advanced 2.9 to 63.9 and new orders rose 0.6 to 64.

Prices paid index continued to fall back from September's hurricane-boosted high of 71.5, giving back 3 points to 65.5 in November.

The spread between new orders and inventories - a good leading indicator of activity - widened in November to 17 (+1.6 points), suggesting that the manufacturing is likely to hold onto the recent gains in the coming months.

Fourteen of the eighteen manufacturing industries reported expansion in November, with paper products, machinery, and transportation equipment registering the strongest advances. Two industries recorded a contraction in activity (wood products, petroleum and coal products), while two others were unchanged in November.

Key Implications

As is sometimes the case with the ISM manufacturing index, the details of the report painted a more positive picture of the manufacturing sector than the headline index would suggest. The surge in the supplier deliveries following this summer's hurricanes was still unwinding in November. This weighed on the headline index, more than offsetting the positive contributions from a rise in production and new orders. Comments from business executives further reinforce the notion of a booming U.S. manufacturing sector, with record sales being reported in some sectors and limited signs of the typical seasonal slowdowns taking hold at year-end. While some of this is likely linked to hurricane rebuilding efforts, it's also a reflection of persistently strong domestic and global demand.

With the prospect of corporate tax reform in some form ever closer to being realized, there is a chance that, in addition to redistribution to shareholders, some of the extra cash may find its way into capital goods produced by U.S. manufacturers. Should this be the case, the 2017 boom in manufacturing is likely to carry into the New Year and continue to support the U.S. economy on its path to full capacity.

Dollar Holds Positive Bias, Despite Mixed Context

- European equities fell off a cliff this morning despite strong EMU data. Major indices lost up to more than 1%, but reversed a big part of the losses as sentiment improved in the US. European indices decline less than 0.5%. US equities open with limited losses. The Nasdaq (-0.5%) underperforms again.

- Global manufacturing expanded at the fastest pace in years last month and the second-best in two decades in the euro zone, driven by robust demand and bolstering the case for central banks to shift to tighter monetary policy. The EMU manufacturing PMI was upwardly revised to 60.1.

- The IHS Markit/CIPS UK Manufacturing PMI jumped to 58.2 from an upwardly revised 56.6 in October, hitting its highest level since August 2013. The report suggests that the manufacturing sector will support the UK economy even as consumer spending is eroded by a decline in consumers' disposable income.

- US Senate Republicans will grapple today with the possibility of adding a tax increase to sweeping legislation meant to cut taxes on businesses and individuals, aiming to win support from fiscal conservatives worried about the bill's impact on the federal deficit.

- Hiring in Canada unexpectedly accelerated in November. The unemployment rate dropped to 5.9%; the lowest level since February 2008. Employment increased by 79,500 last month, well above economists' forecasts for a gain of 10,000 jobs. Average hourly wages also continued to accelerate, rising 2.7 percent from last year. The Canadian dollar jumped sharply higher after the report. USD/CAD trades in the mid 1.27 area.

- US manufacturing expanded at a robust pace in November (58.2 from 58.7 vs 58.3 expected) amid a burst of production and rising orders that signal durable gains in the industry, figures from the Institute for Supply Management showed.

Rates

Bund tests 163.43 resistance in risk off sentiment

Global core bonds gain ground today with the Bund outperforming the US Note future. The US Senate's tax reform drive lost momentum last night after a congressional watchdog determined the bill would send the budget deficit skyrocketing. A vote will now take place today instead of yesterday. The delay caused some risk aversion on stock markets and supported core bonds via safe haven flows in the first hours of European dealings. The bond rally petered out around noon though and the US Note future even started losing ground. Technically, the Bund tested the upper bound of its sideways trading range (160.24-163.43) but a break didn't occur. The European eco calendar didn't influence trading with only a slight upward revision to the November manufacturing PMI.

At the time of writing, German yields decline by 0.9 bps (2-yr) to 2.6 bps (10-yr). The US yield curve flattens with yield changes varying between +0.8 bps (2-yr) and -3.6 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrowed up to 3 bps (Belgium) with Greece (+3 bps) and Portugal (+5 bps) underperforming.

Currencies

Dollar holds positive bias, despite mixed context

The dollar traded with a positive bias today even as incentives from other markers were diffuse. Risk sentiment was outright negative in Europe this morning, but the dollar held up well. The US currency is gaining further ground this afternoon as US investors turn again more optimistic. EUR/USD trades in the 1.1870 area. USD/JPY trades at 112.65, near the intraday top.

Yesterday evening and overnight, the dollar showed quite a diffuse picture. USD/JPY was supported by a rise in US equities and higher US yields yesterday evening. At the same time, EUR/USD also rallied even as the interest rate differentials widened in favour of the dollar. Technical factors and end-of month repositioning might have been at work. The moves slowed this morning in Asia. USD/JPY stabilized in the mid 112 area. EUR/USD hovered in the 1.1925 area.

Risk sentiment deteriorated quite substantially soon after the open of the European equity markets. Uncertainty on the fate of the Tax Bill in the US Senate maybe played a role. However, (European) equities recently already showed tentative signs that the uptrend might become a bit exhausted. The (EMU) eco data were not to blame. The final EMU manufacturing PMI was even revised slightly higher to 60.1, a multi-year peak. However, the report couldn't stop the bleeding at that time. Core bond yields lost about 3-4 bps (10-y) but the interest rate differential between the euro and the dollar was little changed. The risk-off trade eased again as US traders entered the fray. US equities opened with only modest losses, the Nasdaq underperforming.

Of late, a decline in core yields and/or a risk-off context often weighed on the dollar, but this was not the case today. USD/JPY held up remarkably well. The pair hardly ceded any ground this morning and even set a minor top for the week this afternoon (currently around 112.65). The dollar also regained slightly ground against the euro. EUR/USD trades in the 1.1870 area. Markets (FX) closely monitor the headlines from the tax debate in the US Senate. The ISM manufacturing in the US is also interesting. However, the reaction to the UK/EMU data this morning suggests that the focus of (currency) traders is elsewhere. In globo, the dollar performed rather well today, given the price action on other markets. A harbinger of better times to come?

Sterling awaits clarity on Brexit process

Sterling trading showed no clear trend today. Over the previous days, markets saw the Brexit-glass half-full on tentative signs that the UK and the EMU were making progress on the conditions that the EU wants to be fulfilled to start negotiations on the future relation between the two parties. However, the issue of the Irish border proves to be a hard nut to crack. Markets had hoped that big progress would be announced after a meeting between EU president Donald Tusk and UK PM May scheduled for Monday 04 December. However, this scenario is becoming less likely. Sterling lost slightly ground against the euro and the dollar. EUR/GBP hovered mostly in the lower half of the 0.88 big figure (currently 0.8810). Cable is drifting back below the 1.35 barrier, but part of this decline is due to the USD rebound this afternoon. This morning, the UK November manufacturing PMI printed at a very strong 58.2 (from 56.6, 56.5 was expected), but the report had no lasting impact on sterling trading.

Canadian Job Growth Enters the Stratosphere, with Wages Starting to Follow

Highlights:

- Employment rose 80k in October, the 12th consecutive monthly increase and the best gain in more than five years.

- The unemployment rate plummeted to 5.9%, one of only a handful of sub-6% readings in the last 40 years. The decline was all employment driven—labour force participation was unchanged in November.

- Wages have accelerated sharply in recent months, with a bit of help from higher minimum wages in several provinces. Wage growth picked up to 2.7% year-over-year from as low as 0.5% in April.

- Job growth was widespread but led by Ontario, Quebec and British Columbia. Unemployment rates declined substantially in the former two provinces and Quebec's rate is now the lowest on record.

Our Take:

Where do we start? Canada's longest hiring streak in a decade continued with a whopping 80 thousand jobs added in November. Average employment growth of 32.5 thousand per month over the last year is the fastest pace since 2007. The unemployment rate fell 0.4 ppts in November, the largest monthly decline since 2005. And that was without a dip in the labour force. The rate, now at 5.9%, was only lower for a single month prior to the last recession—a time when the economy was operating beyond its longer run capacity limits. The only fly in the ointment was a sizeable drop in average hours worked that retraced much of the increase seen in recent months. The Bank of Canada has flagged below-trend hours worked as a sign of labour market slack, but other indicators are clearly pointing to very tight conditions.

For all the impressive numbers just listed, perhaps our favourite in today's report is wage growth. Average hourly wages for permanent employees were up 2.7% from a year ago in November, the best pace in a year and a half. Much of that increase has come in the last few months as wage growth accelerated sharply—finally a bit of evidence that tight labour market conditions are feeding through to wages. If that trend holds up it will be hard for the Bank of Canada to remain on the sidelines much longer. Our forecast assumes the bank will raise rates again in April when they have more information on Nafta renegotiation and how households are handling this year's rate hikes. If anything, today's blockbuster employment report raises the risk of an earlier move.