Sample Category Title

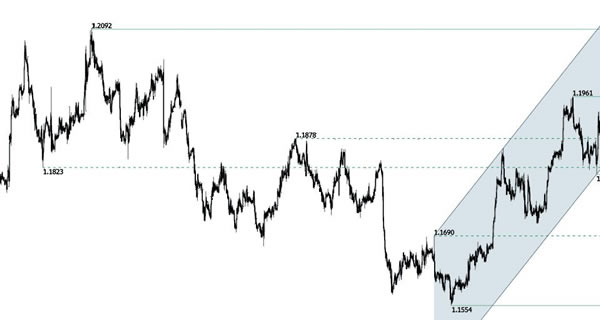

EUR/USD Pushing Higher

EUR/USD's bullish momentum continues. Hourly resistance is now given at 1.1961 (27/11/2017 high). Hourly support is given at a distance at 1.1809 (30/11/2017 low). Expected to show continued increase.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Euro Unchanged As Eurozone, German Mfg. Reports As Expected

The euro has shown some movement on Friday, but remains close to the 1.19 line. Currently, EUR/USD is trading at 1.1906, up 0.01% on the day. On the release front, the focus is on manufacturing data, with the release of PMIs in Europe and the US. The Eurozone Final Manufacturing PMI improved to 60.1, above the estimate of 60.0. German Final Manufacturing PMI climbed to 62.5, matching the forecast. Later in the day, the US releases ISM Manufacturing PMI, which is expected to dip to 58.4 points. We’ll also hear from FOMC members Robert Kaplan and Patrick Harker.

Manufacturing numbers in the eurozone and Germany continue to impress, as Manufacturing PMIs improved in October, with the eurozone indicator at 60.1 and the German indicator at 62.5 points. The German reading marked the highest since February 2011, while the eurozone release was the strongest since April 2000. The sparkling numbers underscore stronger global demand for European products, which have boosted the manufacturing and export sectors.

German retail sales remain problematic, and posted a sharp decline of 1.2% in October. This marked the third decline in four months. Germany’s economy is solid and the labor market is strong, so why isn’t the German consumer spending? Strong economic conditions have not translated into higher wages for a large segment of the labor force, and low unemployment numbers have masked the problem of underemployment, ,which of course means lower wages for workers who can’t find full-time work. The lack of inflation in Germany is apparent in the eurozone as well, as inflation levels remain below the ECB’s inflation target of around 2 percent.

All eyes are on Washington, as the Senate is set to vote on its version of tax reform. A vote was expected on Thursday night, but this has been delayed until Friday. Republican lawmakers are confident that they have the necessary votes to pass the bill, but with the vote expected along party lines, the results will be close. If the Senate does pass the bill, the stock markets and US dollar will likely respond with gains. The next step in the tax reform saga would be for the House and Senate to bridge the differences between the two bills and come up with a single version.

Technical Outlook: WTI OIL Price Bounces After Rising 20SMA Contained Correction

WTI Oil price moved higher on Friday and forming reversal pattern on daily chart. Thursday’s action ended in long-legged Doji and signaled stall of pullback from $59.02 peak, which was contained by rising 20SMA.

Fresh recovery needs firm break above $58.00 to confirm reversal and higher base at $56.80 zone.

Oil prices remained steady after OPEC and other major oil producers agreed to extend output cut program until the end of 2018, in widely expected decision.

Bullish close in November comes as extension of previous two months rally and signals further rally of oil prices.

However, WTI contract is on track for bearish weekly close which may delay bulls for extended consolidation under high at $59.02.

Bullish daily techs remain supportive for further retracement of $59.02/$56.75 pullback which may show hesitation on approach to $59.02 target.

Alternative scenario sees increased risk of extension of pullback from $59.02 on close below 20SMA (currently at $57.05).

Res: 58.02, 58.28, 59.02, 60.00

Sup: 57.61, 57.28, 57.05, 56.75

European Indices Record Remarkable YTD Performance | Bitcoin Holds 9K Level | Irish Border Control Presents Challenge

May's Brexit At Risk Due to Irish Border

Us Tax Outcome awaited

OPEC's win push oil higher

Bitcoin stay above 9K for now

December is here and investors are going to look for the traditional Santa rally. The trading volume would start to fall as we move closer to the holiday season because traders and investors would start participating in the celebration of the festival season. This particular year we have seen some remarkable gains for the European indices and FTSE MIB takes the medal with a YTD gain of 16.29% and DAX is up 13.44%.

Thanks to the ECB's monetary policy which enabled good times for smaller companies. Hence, there is no surprise that European economic data consistently showing signs of strength. Smaller businesses make the backbone of the euro-zone economy and the earning season confirmed that small and medium-sized firms have once again picked up steam. Countries like Greece, which were facing hurdles in igniting the growth have also started to show more encouraging signs. The SMEs are optimistic about the future which is backed by their turnover.

The dollar bulls had a setback yesterday and the outcome of the US tax bill wasn't what they were hoping for. The US decided to delay the vote and hold Donald Trump from celebrating his victory by another day. The collapse of the voting process took place due to the failure of a compromise, something which we are used to. The points of disagreement included changes in the tax cut expiration. The dollar index could reverse its losses if the US tax reform bill finally sees the sunlight today.

When it comes to the Brexit negotiations, the Irish border issue remains very active without any solutions. Theresa May would have to utilise the weekend and think outside the box to find a solution for this. The solution must be in the form of dessert which the EU's Jean Claude could enjoy during his lunch meeting with May on Monday. The agenda for May is to make her decision on the control points in Northern Ireland, and if she decides to go with no border option, it would make matters tough for her given her relationship with the DUP party.

Bitcoin had another volatile session yesterday which makes many in the industry to question if it has the ability to act like a currency. For now, we are holding the level of 9K but it does look likely that bitcoin may break this level and that would create another headline. The daily moves are just mammoth and if Bitcoin is going to become a form of currency, first it needs to show stability. Institutions are supporting and adopting the blockchain technology without any doubt, however, the concept of cryptocurrency under the current circumstances is something which is making them nervous and not many are on board with this idea

Market Update – European Session: European Manufacturing PMI In Sync With ECB View On Region’s Robust Recovery

Notes/Observations

Euro Zone PMI Manufacturing complements ECB view of a robust and broad-based recovery (Beats: Euro Zone, France, UK, Swiss, Sweden, Norway, Poland; miss: Spain, Russia, Czech, Hungary; In-line: Germany, Italy)

US tax-reform vote was put off by the Senate until at least Friday perhaps due to sufficient votes could not be secured; Budget hawks still seem reluctant to vote

Asia:

Japan core CPI rises for the 10th straight month to 0.8%; result could add to recent speculation over an early tightening move by the BOJ as it heads a little closer to its 2% inflation target

Japan Oct Jobless rate matches lowest rate since Jun 1994 (2.8% v 2.8%e); Job-to-Applicant ratio at a fresh 43-year high (1.55 v 1.52e)

Japan Nov Final Manufacturing PMI: 53.6 v 53.8 prelim (highest final reading since March 2014)

China Nov Caixin Manufacturing PMI 50.8 v 50.9e (5-month low)

Europe:

SPD official Weil ( PM of Lower Saxony): coalition talks with Germany Chancellor Merkel's CDU/CSU could extend until at least Feb as a best case scenario

EU official: EU and UK reach agreement over Brexit divorce bill regards to on future commitments. London has committed to paying a set share of EU budgets after leaving EU. No discussion of numbers, but Britain agrees on formula for calculating British divorce bill

Greece Debt Agency (PDMA) said to plan 2 to 3 bond offerings in H1 2018

Americas:

Senate did not vote on the Republican tax bill on Thursday and debate to continue on Friday

US Senate Majority Leader McConnell: Next floor vote on tax reform will be at 11 AM on Friday, Dec 1st

Joint Committee on Taxation (JCT): Senate tax bill pays for less than half of its cost. Overall, the budgetary effects of changes in economic growth are projected to reduce the deficit by $407 billion during the budget window.

Congressional Budget Office (CBO): Government could run out of cash in late March, early April unless debt limit raised

Fed's Mester (hawk, non-voter): tax plan unlikely to have major impact on growth; inflation expectations remain reasonably well anchored

Energy:

OPEC delegate: OPEC and non-OPEC agree to extend output cuts agreement to end of 2018

OPEC+ Communique: To review duration of oil cuts based on fundamentals at next OPEC meeting in June; Libya, Nigeria had informed OPEC they won't produce above 2017 levels in 2018

Economic Data:

(PE) Peru Nov CPI M/M: -0.2% v 0.0%e; Y/Y: 1.5% v 1.7%e

(IE) Ireland Nov Manufacturing PMI: 58.1 v 54.4 prior (54th month of expansion and highest since Dec 1999)

(RU) Russia Nov Manufacturing PMI: 51.5 v 51.8e (16th month of expansion)

(FI) Finland Q3 GDP Q/Q: 0.4% v 0.8% prior; Y/Y: 3.0% v 3.6% prior

(TR) Turkey Nov Manufacturing PMI: 52.9 v 52.8 prior (9th month of expansion)

(SE) Sweden Nov Manufacturing PMI: 63.3 v 60.2e

(CZ) Czech Q3 Preliminary GDP (2nd reading) Q/Q: 0.5% v 0.5%e; Y/Y: 5.0% v 5.0%e

(NO) Norway Nov Manufacturing PMI: 57.1 v 55.0e

(PL) Poland Nov Manufacturing PMI: 54.2 v 54.0e (37th month of expansion)

(HU) Hungary Nov Manufacturing PMI: 58.6 v 59.5e (24th month of expansion)

(ES) Spain Nov Manufacturing PMI: 56.1 v 56.5e (49th month of expansion and highest since Feb 2007)

(CZ) Czech Nov Manufacturing PMI: 58.7 v 59.0e (16th month of expansion and highest since Apr 2011)

(CH) Swiss Nov Manufacturing PMI: 65.1 v 62.5e (23 month without a contraction)

(IT) Italy Nov Manufacturing PMI: 58.3 v 58.3e (15th month of expansion and highest since Feb 2011)

(FR) France Nov Final Manufacturing PMI: 57.7 v 57.5e (confirmed its 14th month of expansion and highest since Nov 2010)

(DE) Germany Nov Final Manufacturing PMI: 62.5 v 62.5e (confirmed its 36th month of expansion and highest since Feb 2011)

(EU) Euro Zone Nov Final Manufacturing PMI: 60.1 v 60.0e (confirmed 52nd month of expansion and highest since Apr 2000)

(GR) Greece Nov Manufacturing PMI: 52.2 v 52.1 prior (6th month of expansion)

(ZA) South Africa Nov Manufacturing PMI: 48.6 v 47.8 prior (6th straight contraction)

(NL) Netherlands Nov Manufacturing PMI: 62.4 v 60.4 prior (highest since series began in 1960)

(NO) Norway Nov Unemployment Rate: 2.3% v 2.4%e

(IT) Italy Q3 Final GDP Q/Q: 0.4% v 0.5%e; Y/Y: 1.7% v 1.8%e

(UK) Nov Manufacturing PMI: # v 56.5e (16th month of expansion and highest since Aug 2013)

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.6% at 384.4, FTSE -0.2% at 7315, DAX -1.0% at 12898, CAC-40 -0.9% at 5325, IBEX-35 -0.4% at 10175, FTSE MIB -0.9% at 22158, SMI -0.3% at 9293, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices trade sharply lower across the board with near 1% declines in Germany and France being attributed to a stronger Euro as well as uncertainty spillover in the US over the delay in Senate tax reform vote. Shares of Indivior trades sharply higher after the FDA approved its Buprenorphine injection, whilst on the earnings front Games Workshop trades higher following strong Revenue growth. UK mailing giant Royal Mail trades over 3.5% lower after an analyst downgrade; RBS trades lower after announces the closure of further branches as it continues its digital push. Looking ahead notable earners include Big Lots, Genesco and American Woodwork.

Equities

Consumer discretionary [ Games Workshop [GAW.UK] +7% (Trading update), Royal Mail [RMG.UK] -3.9% (Analyst downgrade)]

Financials: [Barclays [BARC.UK] -2% (Reduces stake in BAGL),

Healthcare: [Basilea [BSLN.CH] +1.2% (Extends licence agreement with Pfizer), Indivior [INDV.UK] +10% (US FDA approved first once-monthly Buprenorphine injection)]

Speakers

Sweden Central Bank (Riksbank) Dep Gov Floden reiterated inflation is near target but too early to make policy less expansionary

EU official: Hope to reach staff-level agreement on Greece bailout review on Monday, Dec 4th. Next Greek tranche payment could be disbursed by mid-Feb if all goes well

Thailand Central Bank: Inflation to return to within the 1.0-4.0% target range in Q1 (previously saw it occurring in Q2) if oil prices remain at high levels

Currencies

USD maintained a soft tone heading into the end of the trading week as the tax-reform vote was put off by the Senate until at least Friday perhaps due to sufficient votes could not be secured

EUR/USD was firmer throughout the session as various Euro Zone PMI Manufacturing data complemented ECB view of a robust and broad-based recovery. France and Germany levels were at 7-year highs while the Euro Zone data hit its highest since 2000.

Fixed Income

Bund futures trade 163.09 up 40 ticks, as European stocks slide and major European PMIs' come in line, while reaching record or multi-year highs. Continued downward pressure sees 162.10 followed by 161.50. A reversal targets 163.40 then 163.75.

Gilt futures trade at 124.74 up 39 ticks, rebound after the mid-week decline. Continued upside eyeing 125.15 then 125.65. Downside targets include 124.01 then 123.75.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.886T from €1.858T. Use of the marginal lending facility fell to €65M from €286M prior.

Corporate issuance saw 3 issuers raise $2.3B in the primary market. For the week ending Nov 29th Lipper fund flows reported IG fund net inflows of $2.4B.

Looking Ahead

06:00 (BR) Brazil Q3 GDP Q/Q: 0.3%e v 0.2% prior; Y/Y: 1.3%e v 0.3% prior, GDP 4-quarters accumulated: -0.3%e v -1.4% prior

06:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month Bills (£1.0B, £1.0B and £1.5B respectively)

06:30 (IN) India Weekly Forex Reserves - 06:45 (US) Daily Libor Fixing

07:00 (CA) Canada Oct MLI Leading Indicator M/M: No est v 0.1% prior

07:00 (CL) Chile Oct Retail Sales Y/Y: 3.7%e v 3.5% prior

07:00 (ZA) South Africa Nov Naamsa Vehicle Sales Y/Y: No est v 4.6% prior

07:00 (DE) Germany Fin Min official Spahn at event

(US) Nov Wards Domestic Vehicle Sales; Total Vehicle Sales

08:00 (BR) Brazil Nov PMI Manufacturing: No est v 51.2 prior

08:00 (CZ) Czech Nov Budget Balance (CZK): No est v 26.5B prior

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:30 (CA) Canada Sept GDP M/M: +0.1%e v -0.1% prior; Y/Y: 3.3%e v 3.5% prior; Quarterly GDP Annualized: 1.6%e v 4.5% prior

08:30 (CA) Canada Nov Net Change in Employment: +10.0Ke v +35.3K prior; Unemployment Rate: 6.2%e v 6.3% prior,

09:05 (US) Fed's Bullard (non-voter, Dove) in Aransas

09:30 (CA) Canada Nov Manufacturing PMI: No est v 54.3 prior

09:30 (US) Fed's Kaplan (moderate, voter) in Tx

09:45 (US) Nov Final Markit Manufacturing PMI: 54.0e v 53.8 prelim

10:00 (US) Oct Construction Spending M/M: 0.5%e v 0.3% prior

10:00 (US) Nov ISM Manufacturing: 58.3e v 58.7 prior; Prices Paid: 67.0e v 68.5 prior

10:00 (MX) Mexico Central Bank Economist Survey

10:00 (MX) Mexico Oct Total Remittances: $2.4Be v $2.3B prior

10:00 (CO) Colombia Oct Exports: $3.1Be v $3.3B prior

10:15 (US) Fed's Harker (voter, hawk) on economic growth

10:30 (MX) Mexico Nov Manufacturing PMI: No est v 49.2 prior

11:00 (EU) Potential sovereign ratings after EU close (Cyprus Sovereign Debt to be rated by DBRS; Ireland Sovereign Debt to be rated by S&P and Sweden Sovereign Debt to be rated by Moody's)

12:00 (IT) Italy Nov New Car Registrations Y/Y: No est v 7.1% prior

12:00 (BR) Brazil Nov Trade Balance: $4.5Be v $5.2B prior; Total Exports: $18.1Be v $18.9B prior; Total Imports: $13.6Be v $13.7B prior

13:00 (MX) Mexico Nov IMEF Manufacturing Index: 52.2e v 52.4 prior; Non-Manufacturing Index: 51.7e v 51.9 prior

13:00 (US) Weekly Baker Hughes Rig Count data

(AR) Argentina Nov Government Tax Revenue (ARS): No est v 219.7B prior

(BR) Brazil Nov CNI Consumer Confidence: No est v 101.2 prior

(IT) Italy Nov Budget Balance: No est v -€5.0B prior

(RU) Russia Nov Sovereign Wealth Funds: Reserve Fund: No est v $16.9B prior; Wellbeing Fund: No est v $69.4B prior

USD Edges Lower Amid Rising Uncertainty Over US Tax Bill

USD's turmoil benefits EUR

After a promising start into the week, the greenback is back in the doldrums as investors scale down their long USD positions. After rising as much as 0.75% during the week, the dollar index reversed gains and returned at around 92.80 on Friday morning. A couple of month ago, everything was looking good for the greenback as Trump's tax reform finally started to move forward, the Fed started to reduce its giant balance sheet and signalled a rate hike in December, while economic indicators came in roughly in line with market expectations.

However, it looks like investors are still disappointed regarding developments with the US tax reform and the last batch of economic indicators. The economic agenda was quite busy this week. The first revision of the third quarter GDP was revised higher to 3.3% (q/q annualized). The downward revision in personal consumption (2.3% vs 2.2%) killed off the enthusiasm. Still on the positive side, the last inflation figures were also in line. The Fed's favourite measure of inflation, the core personal consumption expenditure, remained steady at 1.4%y/y in October, while the headline gauge edged lower to 1.6%y/y from 1.7% in the previous month.

On the political side, the US tax reform is facing difficulties in the Senate. Even with a small majority in the upper chamber, Trump is struggling to get the required numbers of vote to pass the bill. Investors manifested their disappointment by trimming their long USD positions.

Looking at the positioning of speculators, data reported by the CFTC showed that non-commercial short USD positions have increased slightly over the last few weeks. More specifically, speculators remains bullish EUR/USD. We also believe that there is plenty of room for further euro appreciation, especially against the dollar. Positive economic developments together will a “tightening” of monetary policy conditions were encourage investors to reallocate their capital on the other side of the Atlantic.

Bitcoin stabilizes below 10k

Now that the Bitcoin has reached 10k dollar. Speculation regarding its futures are reaching a climax. Some sees it at 1 million dollar like John Mcafee who in a tweet declared that he was increasing its forecast on the digital currency. Some other like Jamie Dimon said “Bitcoin was a fraud”, forgetting that JP Morgan was involved in the Libor scandal.

Others are also very suspicious like the 2014 Nobel Prize, Jean Tirole, who is concerned about the possible financial bubble that Bitcoin represents. Unfortunately we did not hear him yet about the massive debt from G10 countries. He then added that he is afraid that money is being privatised. We should recall that the Fed is a private bank that control the issuance of any dollar. Is there any reason to be afraid of the Fed in this case?

In our view, even though the Bitcoin technology is not perfect, very low transaction speed and high transactions fees, the digital currency has a strong advantage. I am not talking about the ability to store and transfer value but about the strong acceptance rate that makes it a strong investment over the future. Anyone can create a blockchain but there is almost no chance that it becomes mainstream as the Bitcoin.

GBPJPY Surges Out Of Range, Bullish Bias Above 152

GBPJPY maintains a bullish intra-day bias after breaching the key 152 level yesterday. The pair has breached the upper end of the two-month consolidative range after a strong rally.

Strong support held at the 147 level and GBPJPY bounced off the bottom of the range to rise with strong momentum all the way back to the top of the range and consequently breaking above it.

Looking at the 4-hour chart, momentum appears to have faded and the market has become overextended following the strong surge. The RSI has entered overbought levels above 70. This suggests GBPJPY may consolidate in the near term or even see a pullback.

To the downside, strong support is now being provided at 152. If it fails to hold, then prices would fall back into the medium-term range. As long as GBPJPY can sustain trading above 152 then the consolidative phase has ended and this could be the start of a new bullish phase.

Risks are clearly tilted to the upside with scope to extend towards the 160 handle. On the 4-hour chart, it appears that there could be an imminent bullish crossover of the 50 and 200-period moving averages. On the daily chart, the moving averages are bullishly aligned.

EUR/JPY Elliott Wave Analysis

EUR/JPY - 133.92

Although the single currency did fall earlier this month to as low as 131.17 (our short position entered at 133.50 met target at 131.50 with 200 points profit), as euro found renewed buying interest there and has staged a strong rebound, suggesting the correction from 134.50 has ended at 131.17 and retest of this level would be seen, however, break there is needed to confirm medium term upmove has resumed and extend gain to 135.00, and then 135.50-60. Having said that, loss of upward momentum should prevent sharp move beyond 136.00-10 and reckon 136.95-00 would hold, price should falter well below 138.45-50 (1.618 times extension of 109.49-124.10 measuring from 114.85), bring correction later.

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, indicated upside targets at 126.00 and 130.00 had been met and further gain to 135.00 would follow.

On the downside, whilst initial pullback to 133.50-60 cannot be ruled out, reckon 132.90-00 would limit downside and bring another rise later to aforesaid upside targets. Only below support at 131.72 would abort and signal the rebound from 131.17 has ended instead, bring another test of this level. Once this support is penetrated, this would suggest a temporary top is formed, bring retracement of recent rise to previous support at 130.62, then towards 130.00 later.

Recommendation: Short entered at 133.50 met target at 131.50 with 200 points profit and would turn long at 133.00 for 135.00 with stop below 132.00.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

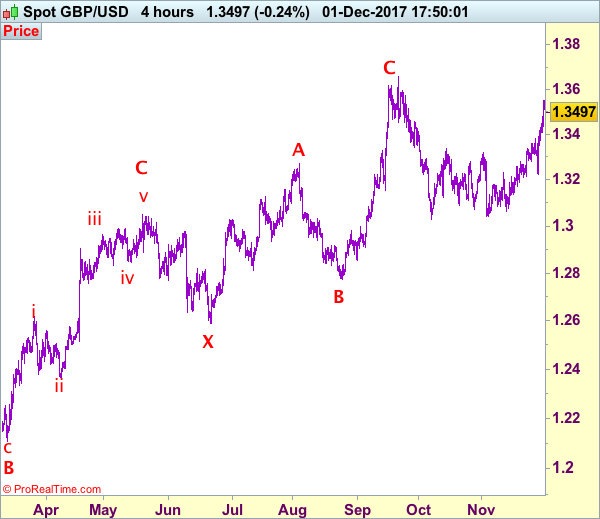

Trade Idea: GBP/USD – Target met and buy at 1.3410

GBP/USD – 1.3490

Original strategy :

Bought at 1.3260, met target at 1.3450

Position: - Long at 1.3260

Target: - 1.3450

Stop: -

New strategy :

Buy at 1.3410, Target: 1.3600, Stop: 1.3350

Position: -

Target: -

Stop:-

Cable rallied in line with our bullish expectation, our long position entered at 1.3260 met upside target at 1.3450 (with 190 points profit), this anticipated rise adds credence to our view that entire correction from 1.3658 has ended at 1.3027 earlier and upside bias remains for the rise from 1.3027 to extend gain to 1.3550, then 1.3595-00, however, reckon said recent high at 1.3658 (Sept high) would hold from here due to near term overbought condition, bring retreat later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

As we have taken profit on our long position entered at 1.3260, would be prudent to buy sterling again on pullback as 1.3400-10 should limit downside and bring another rise later. Below previous resistance at 1.3383 would defer and risk correction to 1.3335-40, break there would confirm top is formed instead, bring further fall to 1.3290-00 first.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

OPEC’s Decision To Extend Production Cuts And The Volatility Of Bitcoin

Investors who were banking on OPEC to enforce some 'extraordinary measures” to rebalance markets were left empty-handed on Thursday, after the cartel simply agreed on extending oil output cuts until the end of 2018.

Although short-term oil bulls were offered a slight boost following OPEC's decision to extend production cuts by nine months, the overall muted market reaction verifies how this was already mostly priced in. There is even a suspicion that reports of both Nigeria and Libya agreeing to cap their production in 2018, were the main reasons why oil prices held steady following the meeting. While OPEC and Co. continue to cut production in an effort to boost prices, U.S. shale output has increased - with production rising 3% in September to 9.48 million barrels a day. It is becoming clear that oil prices will continue to remain exposed to downside risks, thanks to rising production of U.S. Shale scuppering OPEC's efforts to rebalance markets.

Taking a look at the technical picture, WTI Crude still fulfills the prerequisites of a bullish trend on the daily charts as there have been consistently higher highs and higher lows. A breakout above $58.00 may encourage a further incline higher towards $59.00. Alternatively, sustained weakness under $56.75 could trigger a decline back towards $56.00.

Dollar jittery as U.S. tax vote stalls

The Dollar weakened against a basket of major currencies on Thursday, after U.S. Senate Republicans delayed voting on their tax bill as a setback forced them to make tweaks a few hours before a planned final vote.

With the Greenback becoming extremely sensitive to any progress on U.S. tax reforms, there could be some action today depending on the outcome of the U.S. Senate's vote on tax reform legislation. From a technical standpoint, the Dollar Index remains depressed on the daily charts. Bears remain in control below the 93.50 lower high with the next level of interest at 92.55.

Commodity spotlight – Gold

Gold was under pressure during Thursday's trading session, with prices dipping towards $1270 as the risk-on sentiment and positive U.S. economic data reduced appetite for safe-haven assets.

Although the yellow metal has edged slightly higher today on the back of a weakening Dollar, bears remain in power below the $1280 resistance level. From a technical standpoint, sustained weakness below $1280 could trigger a further decline back towards $1267. Alternatively, a break above $1280, is likely to open a path back towards $1289.

Are Bitcoin bulls tired?

It has certainly been another explosively volatile trading week for Bitcoin which sprinted to a record high above $11400 on Wednesday.

I found it mind-boggling how the cryptocurrency entered a bear market by sharply depreciating towards $9000 after hitting record highs then back to a bull market in less than 24 hours – but with Bitcoin, we are seeing that anything is possible. With everyone's favorite cryptocurrency having no intrinsic value and being inherently unstable, there are growing concerns over this just being another massive speculative bubble. While Bitcoin has on repeated occasions bounced back stronger amid criticism and negativity, the current price action suggests that bulls may be tired.

Taking a peek at the technical picture, the $10000 psychological level seems quite significant. A yearly close above this level could signal further upside; alternatively sustained weakness under $10000 may spark jitters resulting in a decline back towards $9000.