Sample Category Title

Market Update – Asian Session: Risk Appetite Returns With Bond Yields Lower

Headlines/Economic Data

Japan

Nikkei 225 opened +0.9%;

Automakers track Monday’s gains in US auto sector; Toyota +1.6%

Steelmakers track recent gains in shares of US Steel; JFE +1%

Mega Banks and Topix Securities Brokers index gain (rebound from prior session’s losses)

Toshiba +4% (closed -5.8% on Monday), Softbank +1.3%, Fast Retailing +0.8%

(JP) Japan Finance Min Aso: Tax changes need to consider work reform and an aging society; one time depreciation is a big encouraging investment

(JP) Japan Defense Min Onodera unable to rule out more North Korea ‘provocations’ - Japanese Press

Korea

Kospi opened +0.2%

LG Display +4% (South Korea to decide on planned investment in China), Hynix +1.5% (Micron +3.2%); Hanwha Life -3% (stake sale)

(KR) South Korea Nov (20 days) Exports Y/Y: 9.7% v 6.9% prior; Imports Y/Y: 14.0% v 3.1% prior

Won reversed yesterday’s losses as risk appetite returns

(KR) Local South Korea think tank: Expect the won to remain strong in 2018

(US) Pres Trump: US to designate North Korea as a state sponsor of terrorism

034220.KR South Korea said to hold meeting related to planned investment in China - South Korean Press; +5.7%

China/Hong Kong

Shanghai Composite opened -0.3%, Hang Seng +0.4%

Hang Seng Information Technology Index +3.5% (Tencent +3.9%, market cap moves above Facebook’s)

Hang Seng Financials Index +1%; Insurers gain amid rise in China 10-year bond yield

Hang Seng Consumer Goods Index +0.8% (L’Occitane +2.5% after reporting final Q3 earnings); Property Index -0.5%

(CN) China Energy Investment Group and China National Coal Group will keep their 2018 coal contract prices at CNY535/t, flat y/y - financial press

(CN) China NDRC Vice Chairman Lian Weiliang says coal prices are currently relatively high and should be guided downward – Chinese Press

USD/CNY (CN) PBoC sets yuan reference rate at 6.6356 v 6.6271 prior

(CN) PBoC OMO: Injects CNY180B v CNY100B injected in 7,14 and 63-day reverse repos prior; Net injects CNY10B v CNY20B prior

Australia/New Zealand

ASX 200 opened +0.2%;

Graincorp -5% (FY17 profits below ests; CEO sees challenging year ahead)

AUD trades at 5-month low: Morgan Stanley (MS) said to forecast the Aussie to trade at $0.65 (timing uncertain)

The pass-through to inflation could be delayed by many factoring including retail competition, consumption growth likely to be lower in Q3 versus Q2, says the Reserve Bank of Australia (RBA) Nov Meeting Minutes.

(AU) Australia banking regulator, APRA, Chairman Byres: Have concerns over housing and lending standards

(AU) Australia PM Turnbull: considering tax cuts for low and middle income earner, in addition to lowering the corporate rate to 25% from 30% - speaking to Business Council of Australia

RBA Gov Lowe to speak during European morning

Australia Q3 Construction work done to be released on Wednesday’s session

ATM.NZ Reports FY18 first 4-months EBITDA NZ$78.4M; Rev NZ$262.2M – AGM; +4.3%

Other Asia

(TW) Taiwan Gov sells NT$25B in 30-yr bonds, avg yield 1.667% v 1.7%e; bid-to-cover 1.54x

North America

US equity indices ended Monday broadly higher: Dow +0.3%, S&P 500 +0.1%, Nasdaq +0.1%, Russell 2000 +0.7%; Financials and Industrials outperformed

After Market Movers: Intuit (INTU) Reports Q1 $0.11 adj v $0.05e, Rev $886M v $855Me; -2.4% afterhours Palo Alto Networks (PANW) Reports Q1 $0.74 v $0.68e, Rev $505.5M v $489Me; Promotes Bonanno as CFO; +7.3% afterhours; Urban Outfitters (URBN) Reports Q3 $0.41 v $0.33e, Rev $893M v $857Me; +3.1% afterhours

M&A: US DoJ seeking to block merger between Time Warner Inc and AT&T; Nestle said to show bidding interest in Hain Celestial (press report); CVS may reportedly come to definitive agreement to acquire Aetna by end of Nov (press report)

Debt Issuance: Weight Watchers International priced $300M in high yield 2025 senior notes (offering downsized from $500M)

Little news seen regarding US tax reform.

(US) Janet Yellen to resign from Fed Board of Governors, effective upon the swearing in of her successor as Chair

BABA Muddy Waters in a report calls Alibaba's Singles Day numbers "obviously fake"

Europe

(DE) German Chancellor Merkel: new elections would be better than a minority govt; goal is still to form a stable govt - TV interview

(DE) CDU Parliamentary Leader Kauder: we seem to be on the course for new elections in Germany

(EU) Reportedly ECB expected to make small, incremental changes next year in discussing QE exit - press

(UK) UK panel reportedly considering move to £40B (€45B) Brexit offer - UK press

(UK) Unnamed source in PM May's office says nothing is agreed upon in the Brexit until everything is agreed - financial press

(UK) EU Chief Brexit Negotiator Barnier reportedly informs EU27 that more clarity is needed on the Brexit bill; believes bill cannot be tied to trade agreement

(UK) BOE's Dep Gov Ramsden: UK economy in a weaker growth period for some time to come; domestic CPI is below the rate consistent with 2% goal

Levels as of 00:00ET

Nikkei +1.0%, Hang Seng +1.22%; Shanghai Composite +0.4%; ASX200 +0.4%, Kospi +0.1%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.0%; FTSE100 0.0%

EUR 1.1745-1.1730; JPY 112.70-112.51; AUD 0.7558-0.7532;NZD 0.6819-0.6789

Dec Gold +0.4% at $1,280/oz; Dec Crude Oil +0.1% at $56.45/brl; Dec Copper +0.1% at $3.09/lb

Officials Concerned Over Wage Growth Timing: RBA Minutes

For the 24 hours to 23:00 GMT, the AUD declined 0.09% against the USD and closed at 0.7549.

LME Copper prices rose 0.4% or $23.5/MT to $6752.0/MT. Aluminium prices declined 0.5% or $9.5/MT to $2067.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7539, with the AUD trading 0.13% lower against the USD from yesterday’s close, following the release of downbeat minutes of the Reserve Bank of Australia’s (RBA) November meeting.

According to the minutes, policymakers cautioned that there remains “considerable uncertainty” about how quickly wages might grow and how this could impact inflation. Further, the board members noted that growth in inflation would be influenced by pressure on margins from strong retail competition and the outlook for wage growth.

The pair is expected to find support at 0.7523, and a fall through could take it to the next support level of 0.7506. The pair is expected to find its first resistance at 0.7565, and a rise through could take it to the next resistance level of 0.7590.

Looking ahead, a speech by the RBA Governor, Philip Lowe, due in a few hours, will attract significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.1734, pressured by heightened political uncertainty in the Euro-zone's largest economy.

Yesterday, German Chancellor, Angela Merkel stated that she would prefer new elections if she fails to form a majority coalition.

In economic news, Germany's producer price index (PPI) climbed 2.7% on a yearly basis in October, at par with market expectations and compared to a rise of 3.1% in the prior month.

Macroeconomic data released in the US indicated that the leading indicator rebounded 1.2% in October, exceeding market expectations for a gain of 0.8%. In the prior month, leading indicator had recorded a drop of 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.1738, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1708, and a fall through could take it to the next support level of 1.1677. The pair is expected to find its first resistance at 1.1789, and a rise through could take it to the next resistance level of 1.1839.

With no major macroeconomic releases in the Euro-zone today, investors would focus on the US existing home sales data for October, slated to release later in the day. Additionally, a speech by the Federal Reserve Chair, Janet Yellen due overnight, would keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.33% against the USD and closed at 1.3238, propelled by speculations that the UK government is ready to offer around £40.0 billion to the European Union as part of its ‘divorce bill'.

In the Asian session, at GMT0400, the pair is trading at 1.3248, with the GBP trading 0.08% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3200, and a fall through could take it to the next support level of 1.3153. The pair is expected to find its first resistance at 1.3287, and a rise through could take it to the next resistance level of 1.3327.

Going ahead, traders would closely monitor UK's public sector net borrowing data for October, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading Marginally Higher This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.49% against the JPY and closed at 112.56.

In the Asian session, at GMT0400, the pair is trading at 112.53, with the USD trading marginally lower against the JPY from yesterday’s close.

Earlier in the session, Japan’s all industry activity index slid 0.5% on a monthly basis in September, higher than market expectations for a drop of 0.4%. In the prior month, the index had recorded a revised rise of 0.2%.

The pair is expected to find support at 112.08, and a fall through could take it to the next support level of 111.63. The pair is expected to find its first resistance at 112.85, and a rise through could take it to the next resistance level of 113.17.

With no further macroeconomic releases in Japan today, Yen investors would look forward to global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher, Ahead Of Swiss Trade Balance Data

For the 24 hours to 23:00 GMT, the USD rose 0.53% against the CHF and closed at 0.9934.

In economic news, Switzerland’s total sight deposits inched up to a level of CHF577.6 billion during the week ended 17 November, from CHF577.5 billion recorded in the previous week.

In the Asian session, at GMT0400, the pair is trading at 0.9928, with the USD trading 0.06% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9892, and a fall through could take it to the next support level of 0.9857. The pair is expected to find its first resistance at 0.9950, and a rise through could take it to the next resistance level of 0.9973.

Ahead in the day, traders would eye the release of Switzerland’s trade balance figures for October.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Slightly Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.14% against the CAD and closed at 1.2811.

In the Asian session, at GMT0400, the pair is trading at 1.2806, with the USD trading a tad lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2767, and a fall through could take it to the next support level of 1.2727. The pair is expected to find its first resistance at 1.2834, and a rise through could take it to the next resistance level of 1.2861.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

RBA Worried About Wage Growth Despite Strong Job Market

The RBA minutes for the November minutes delivered a dovish tone as policymakers expressed concerns over the wage growth outlook. This is consistent with the central bank's worry over household spending as indicated in the meeting statement (released earlier this month). We believe this has added further pressure to Aussie's recent weakness, sending AUDUSD to the lowest level in 5 months. The central bank kept its powder, leaving the cash rate unchanged at 1.5%, in November. We expect the monetary policy would stay unchanged at least until 1H18 and could extend to 2H18.

Policymakers remained upbeat over the employment market, describing the conditions as 'surprisingly strong over 2017'. The acknowledged that the broadly-based employment growth had been 'running well above growth in the working-age population' and had been driven by full-time employment over the past months. However, they showed particular concerns over the wage growth outlook, and its impacts on inflation. Policymakers acknowledged that wage growth had been 'weaker than expected' and had been 'particularly low in the mining-related parts of the economy'. They noted that 'the outlook for inflation would be influenced by the persistence of heightened competitive pressures, the outlook for wage growth and the speed with which wage costs might flow through to higher prices'. Yet, 'there was considerable uncertainty around when and how quickly wage pressures might emerge and about how much these would add to inflationary pressure'. All in all, the members retained the view that inflation should increase, but 'only gradually'.

RBA in the minutes also discussed the upcoming CPI reweighting which has caused a little downward revision on the inflation forecasts. The central bank stressed that this should not change RBA's assessment of 'how inflationary pressures were likely to evolve'. Comparing actual inflation and RBA's forecasts, the central bank noted that 'underlying inflation … been slightly higher than forecast, but the increase in headline inflation had been smaller than forecast'.

On the housing market, the central bank acknowledged that credit growth had 'edged lower in recent months, as lending to owner-occupiers had eased and lending to investors had stabilized at a slower pace'. The minutes suggested that 'the recent sharp declines in interest-only loan approvals suggested that banks had comfortably met the requirement set by the Australian Prudential Regulation Authority (APRA) for interest-only housing loans to comprise less than 30% of new housing lending'

The monetary policy stance was the same as previous months. As noted in the minutes, the Board 'judged that holding the stance of monetary policy unchanged would be consistent with sustainable growth in the economy and achieving the inflation target over time'. While the language was the same 'neutral' stance as previous meetings, the central bank's explicit concerns over wage growth and inflation outlook signal it would unlikely consider raising interest rates for the coming year.

Elliott Wave View: EURAUD Short Term

EURAUD Short-Term Elliott Wave view suggests that the decline to 1.5057 ended Intermediate wave (X). The rally from there appears to be unfolding as a 5 waves impulse Elliott Wave structure, suggesting that as long as the pullbacks stay above 1.5057, it could see further upside. Up from 1.5057, Minute wave ((i)) ended at 1.5234, Minute wave ((ii)) ended at 1.5075, Minute wave ((iii)) ended at 1.5606, Minute wave ((iv)) ended at 1.5481, and Minute wave ((v)) ended at 1.5657.

The 5 waves rally from 1.5057 low ended Minor wave A of a zigzag Elliott Wave structure. Minor wave B is currently in progress as a double three Elliott Wave structure. Minute wave ((w)) ended of B at 1.545 and Minute wave ((x)) of B ended at 1.5626. Near term, expect another leg lower in Minute wave ((y)) of B towards 1.529 – 1.542 area before pair resumes the rally higher or at least bounce in 3 waves. Instead of going lower, if pair resumes higher from here and break above Minor wave A at 1.5657, then Minor wave B is already complete at 1.5451. We don't like selling the pair and expect buyers to appear in 3, 7, or 11 swing dips as far as pivot at 1.5057 low stays intact.

EURAUD 1 Hour Elliott Wave Analysis

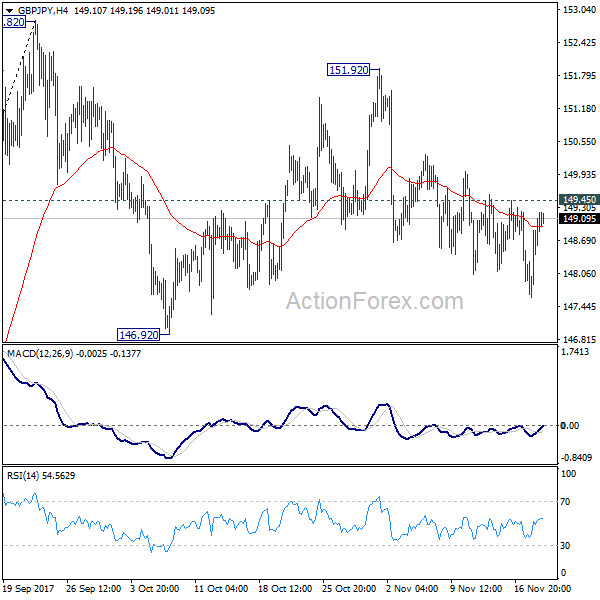

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.02; (P) 148.62; (R1) 149.62; More...

No change in GBP/JPY's outlook. Price actions from 152.82 are viewed as a corrective pattern, with fall from 151.92 as the third leg. Deeper decline could be seen through 146.92 support. But we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, break of 149.45 minor resistance will turn bias back to the upside for 151.92/152.82 resistance zone.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.