Sample Category Title

Weekly Focus: Low Volatility in Markets – and in the Global Economy

Market Movers ahead

- We are heading for a very quiet week with no big movers in the US or Europe. In the UK, Brexit negotiations will continue on Thursday.

- China is due to release inflation and FX reserves data. We look for PPI inflation to stay high for now at 6.9% before heading lower next year. We expect CPI inflation to stay subdued at 1.7%.

- Japanese wage numbers will be interesting to watch. Wage growth has so far stayed low despite the strongest labour market in more than 20 years.

- In Sweden, the most important release will be the Riksbank minutes and Prospera inflation expectations.

- We estimate Norwegian core inflation rose slightly to 1.1% in October from 1.0% in September.

Global macro and market themes

- Volatility has continued to fall as central bank predictability is considered high and the macroeconomic outlook looks increasingly stable. We argue it bodes well for continued focus on 'carry' and 'hunt for yield'.

- 'Hunt for yield', ECB QE and a solid budget surplus also mitigate the upside pressure on German long yields from the macro economy.

- The IMF warns 'financial products tied to equity volatility [bought] by investors such as pension funds are creating unknown risks that could result in severe shock to financial markets'.

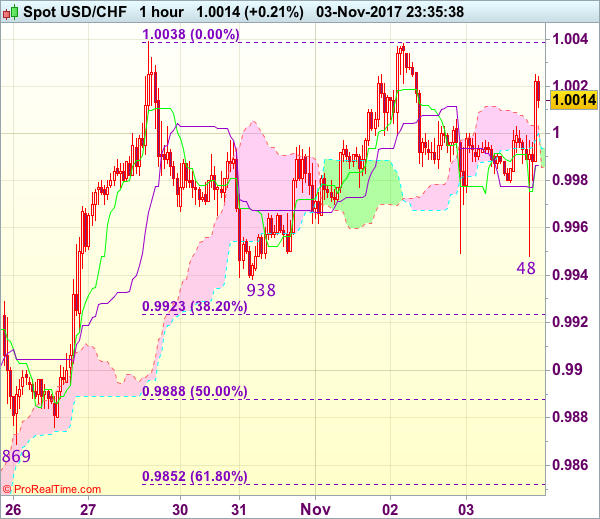

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9950

USD/CHF - 1.0008

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9987

Kijun-Sen level : 0.9987

Ichimoku cloud top : 1.0004

Ichimoku cloud bottom : 1.0000

Original strategy :

Bought at 0.9950, Target: 1.0050, Stop: 0.9930

Position : - Long at 0.9950

Target : - 1.0050

Stop : - 0.9930

New strategy :

Hold long entered at 0.9950, Target: 1.0050, Stop: 0.9930

Position : - Long at 0.9950

Target : - 1.0050

Stop : - 0.9930

Dollar’s retreat after faltering below indicated resistance at 1.0038 has retained our view that further consolidation below this level would be seen, however, still reckon downside would be limited to 0.9945-50 and bring another rise later. Above 1.0005-10 would bring retest of 1.0038 but break there is needed to confirm recent upmove from 0.9421 low has resumed and may extend further gain to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 resistance.

In view of this, we are holding on to our long position entered at 0.9950. Below said support at 0.9938 would abort and signal top is formed instead, risk correction to 0.9920-23 (38.2% Fibonacci retracement of 0.9737-1.0038) but 0.9885-90 (50% Fibonacci retracement) should limit downside and support at 0.9869 would remain intact.

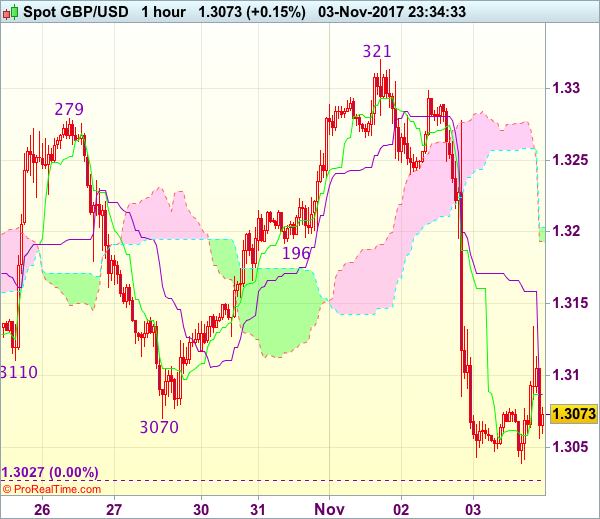

Trade Idea Wrap-up: GBP/USD – Sell at 1.3150

GBP/USD - 1.3072

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3087

Kijun-Sen level : 1.3087

Ichimoku cloud top : 1.3203

Ichimoku cloud bottom : 1.3193

Original strategy :

Sell at 1.3150, Target: 1.3030, Stop: 1.3185

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3150, Target: 1.3030, Stop: 1.3185

Position : -

Target : -

Stop : -

Yesterday’s selloff together with the breach of support at 1.3070 signals early erratic rise from 1.3027 has ended and bearishness remains for further fall, however, break of said support at 1.3027 is needed to signal early downtrend has resumed for weakness to psychological support at 1.3000, then towards 1.2970-75 which is likely to hold from here due to near term oversold condition.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.3150 should limit upside and bring another decline later. Above 1.3200 would defer and prolong choppy trading, risk rebound to 1.3235-40 first.

US Dollar Gains Despite Disappointing Jobs Report as Broader Picture Supports December Hike

The US dollar posted gains during today's European session, despite a disappointing October employment report, which did little in dissuading the market to expect a rate hike at the next Fed meeting.

In this week's major economic release, the US labor market rebounded less strongly than expected from the hurricane-induced slowdown of September. The economy created a net 261 thousand jobs during October, missing analyst forecasts of 310 thousand. There was a positive revision of the previous month's figures to +18 thousand from a contraction of 33 thousand. The other bit of positive news concerned the unemployment rate, which dipped further to 4.1% from the previous month's 4.2% – the lowest rate since 2001. However, average hourly earnings disappointed by coming in flat against expectations of a 0.2% month-on-month expansion. The yearly growth rate in hourly wages thus fell sharply – down to 2.4% from the previous month's slightly inflated 2.9%. The participation rate also disappointed as it fell to 62.7% from 63.1%. Overall the data certainly did not impress but nor did it create worries that there was a significant slowdown underway.

Other data supported the case for strong US economic growth. The huge services sector was doing very well in October according to the Institute for Supply Management (ISM), as the non-manufacturing PMI climbed to 62.2 – the highest since May. The expectation was for the index to ease back to 61 from September's 61.3 print. September factory orders also came in positive as they gained 1.4% month-on-month versus analyst expectations of a 1.3% gain. Finally, the trade deficit for September widened slightly to 43.5 billion dollars from 42.8 billion in August, but that was the result of the growth in imports outpacing slightly the growth in exports, which can be a positive indication for both the domestic and the global economy.

Euro/dollar initially rallied just after the release of the employment numbers, touching a high of 1.1689, but subsequently weakened to 1.1606 as the session progressed and traders assessed the impact of the data together with the other news. Dollar/yen also staged a strong rally, rising to 114.35 and getting ready to test the highs of the last 7 months around 114.45-50. The dollar's resurgence despite the weak employment data also stopped an attempt by sterling to rebound from yesterday's big losses. Pound/dollar dropped to 1.3066 after unsuccessfully trying to take on the 1.31 level earlier in the day.

There was also some good news concerning the pound as the UK services' PMI climbed to 55.6 in October from 53.6 the previous month. The PMIs released this week for the various sectors of the UK economy are pointing to decent growth of around 0.5% during the fourth quarter according to Markit, which would calm worries about a Brexit-induced economic slowdown.

The one currency that managed to recover strongly from recent losses against the US dollar was its northern neighbor, the Canadian dollar. USD/CAD dropped by more than 100 pips following the simultaneous release of positive Canadian employment figures at the same time as the US employment report was hitting the wires. It was a volatile day for the loonie as USD/CAD fell to as low as 1.2714 from around 1.2830 before the numbers were released. The greenback subsequently recovered to 1.2767. The Canadian economy created 35.3 thousand jobs in October while economists were expecting around 15 thousand new jobs. On the other hand, the unemployment rate rose slightly to 6.3% from 6.2%, but traders seemed to place more emphasis on the number of jobs created.

Following three very busy days for the US dollar that included the Fed meeting, the announcement of the nominee for the post of new Fed chair and the all-important nonfarm payrolls, market participants will now be focusing on the tax cut package that Trump and the Republicans are working on. The other week will likely involve digestion of recent events, as the calendar for the major economies will be relatively more light.

Trade Idea Wrap-up: EUR/USD – Sell here

EUR/USD - 1.1620

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1647

Kijun-Sen level : 1.1647

Ichimoku cloud top : 1.1643

Ichimoku cloud bottom : 1.1639

Original strategy :

Sell at 1.1705, Target: 1.1605, Stop: 1.1740

Position : -

Target : -

Stop : -

New strategy :

Sell at market level, Target: 1.1520, Stop: 1.1655

Position : -

Target : -

Stop : -

As the single currency ran into renewed selling interest at 1.1691 and has retreated sharply, suggesting an intra-day top is formed there and consolidation with downside bias is seen for weakness to last week’s low at 1.1574, however, break there is needed to confirm recent decline has resumed and extend weakness to 1.1520-25, then 1.1500 but near term oversold condition should prevent sharp fall below latter level.

In view of this, we are looking to sell euro here for such decline. Above 1.1650-55 would risk another bounce to 1.1691, however, only break there would abort and suggest further choppy trading above 1.1574 and bring a stronger rebound to 1.1700-05 but upside should be limited to previous support at 1.1725 (now resistance).

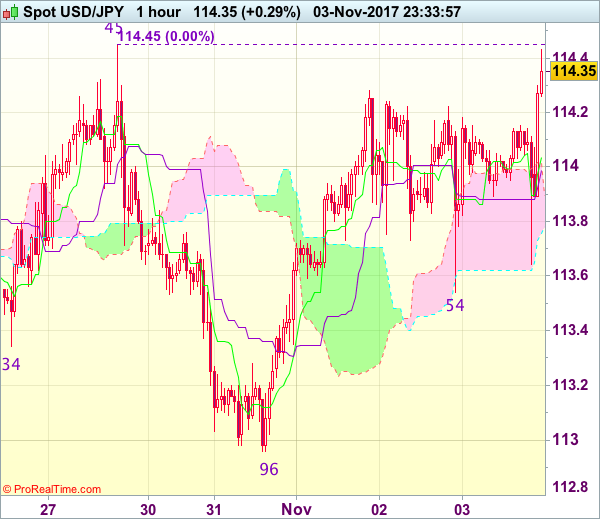

Trade Idea Wrap-up: USD/JPY – Buy at 113.80

USD/JPY - 114.34

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 114.04

Kijun-Sen level : 114.02

Ichimoku cloud top : 113.99

Ichimoku cloud bottom : 113.76

Original strategy :

Buy at 113.40, Target: 114.30, Stop: 113.05

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.80, Target: 114.80, Stop: 113.45

Position : -

Target : -

Stop : -

Although the greenback rebounded after finding support at 113.54 and gain to resistance at 114.45-50 cannot be ruled out, break of this tough level is needed to retain bullishness and confirm early upmove has resumed for headway to 114.75-80 and later towards 115.00 but overbought condition should limit upside. If said resistance continues to hold, then further consolidation would take place and another retreat to 113.40-45 cannot be ruled out but 113.15-20 should hold, bring another rise.

In view of this, we are looking to buy dollar on pullback as 113.80 should limit downside and bring another rise later. Below support at 113.54 would abort and prolong consolidation, risk weakness to 113.20-25, however, reckon support at 112.96 would remain intact, bring another rise next week.

US: Non-Manufacturing Sector Momentum Remains Upbeat in October

After surging an impressive 4.5 points in the month prior, the Institute for Supply Management's (ISM) non-manufacturing index improved further in October, rising 0.3 points to 60.1 - the highest reading since 2005. Today's print surprised on the upside with market consensus expecting a decline to 58.5.

Among the main subcomponents, business activity (+0.9 to 62.2) and employment (+0.7 to 57.5) recorded small improvements and extended their streak of monthly gains to three months. Meanwhile, the supplier deliveries index remained unchanged at 58 indicating slower deliveries for a second consecutive month, with industry comments pointing to hurricane-related supply shortages and transportation delays.

New orders pulled back slightly (-0.2) but remained elevated at 62.8, whereas new export orders improved markedly (+4 to 60).

The prices paid sub-index fell 3.6 points, ending four months of gains, leaving the index at 62.7 in October - still one of the best prints since 2012.

Comments from survey contacts continue to point to a positive outlook for fourth-quarter business conditions, with sixteen industries reporting growth in October. Educational Services; and Arts, Entertainment & Recreation were the two industries that recorded a contraction in activity.

Key Implications

Contrary to its manufacturing equivalent which retreated in October, the ISM non-manufacturing index held on to recent gains. Improvements in business activity and employment sub-indices are indeed very encouraging, but perhaps more significant is the support from the supplier deliveries sub-index which remained unchanged after spiking nearly 8 points last month. Given the latter, improved delivery times as per a return to normalcy could lead to some near-term giveback in the headline.

Still, the underlying trend remains an encouraging one, with broad underlying strength among the main sub-components reinforcing the notion that the services sector continues to expand at a solid clip. Rebuilding efforts should provide added support to this trend through the end of the year, boding well for another above-trend GDP print in the fourth quarter.

Dollar Going Nowhere on Mixed Payrolls

- European equities trade narrowly mixed with Madrid underperforming due to increasing political tensions. Also US equities trade sideways, near yesterday's closing levels.

- US job creation rebounded in October, but wage growth came in below economists' estimates. Employment rose by a net 261,000 last month, marking the biggest monthly job gains since July 2016. The unemployment rate unexpectedly dropped to 4.1%, but average earnings disappointed as they stabilized instead of increasing 0.2% M/M.

- Growth in the US services sector continued its upward march in October, providing evidence that the world's most important economy remains on course in H2 of 2017, despite the damage caused by the hurricanes. The non-manufacturing ISM came in at a very high 60.1 in October, confounding expectations for a decline to 58.5.

- The UK's vast services sector posted its best rise in activity since April this year, propelled by "resilient client demand" and "improved order books", according to a closely watched poll released on Friday. The headline index rose 2 points to 55.6.

- Ben Broadbent, deputy governor of the BoE sought to reinforce the central bank's message that it had not gone soft on future rate rises on Friday, saying "we will need a couple more interest rate rises".

Rates

US payrolls cannot give bonds a distinct direction.

US October payrolls were a mixed bag, giving investors a too diffuse picture to place new big bets. US Treasuries spiked modestly higher for a short period of time, as lower average earnings were considered as the key lesson out of the report. However, the report was even handed and soon US Treasuries were again at pre-payrolls levels. Later, the Non-manufacturing ISM business confidence surprised, as the headline index even rose to 60.1 instead of falling to 58.5. US Treasuries now tried to go lower, but also the downside was blocked. German Bunds moved sideways today, but with a slightly positive bias. It tried a few times to take out first resistance (162.78/83) and the test isn't over. Anyway the key resistance stands at 163.43.

At the time of writing, the German yield curve has bull flattened softly with yields down between 0.4 bp and 1.4 bps. The US yield curve is narrowly mixed with yields varying between +0.9 bp (2-yr) and -0.3 bp (30-yr). On intra-EMU bond markets, 10-yr yield spreads versus Germany are virtually unchanged with Greece underperforming (+6 bps) on profit taking, following a sharp narrowing in the previous two days (-39 bps).

The headline US payrolls gain of 261K in October fell short of the 313K expected, but an upward revision of 90K in the past two months compensated for the miss. The unemployment rate fell unexpectedly to 4.1%, while a stabilization at 4.2% was expected. However, the unemployment rate beat was (more than) compensated by lower than expected average hourly earnings. These were flat (instead of up 0.2% M/M) following a 0.5% M/M increase in September. The sensitivity of markets for wage growth (inflation) is great as it will play a big role in future Fed policy.

Currencies

Dollar going nowhere on mixed payrolls

Today, the focus was on the US payrolls. However, the report was a mixed bag and failed to give clear guidance for USD trading. A strong US non-manufacturing ISM was slightly supportive for the US currency. EUR/USD trades in the 1.1630 area. USD/JPY again tries to regain the 114 barrier. In a broader perspective, the dollar holds to the tight ranges od previous days.

Overnight, Asian equities showed modest gains. Tech stocks were supported by strong earnings from Apple published after the WS close. USD/JPY was little changed in the 114 area in light trading conditions (Japanese markets were closed). EUR/USD held a tight range in the 1.1650/70 area.

There were no data with market moving potential in Europe. Sentiment on risk was cautiously positive and the dollar gained marginally ground as investors looked forward to the US payrolls report. Interest rate differentials hardly changed. If anything there was a marginal widening in favour the dollar.

The US payrolls were a mixed bag. September job growth (261 000) was below consensus, but including upward revision of the previous two months, the figure was broadly as expected. The unemployment rate declined to the very low level of 4.1%. On the other hand, wage growth disappointed again at 0.0% M/M and 2.4% Y/Y. US interest rates and the dollar dropped temporary upon the disappointing wage data, but the USD and rates decline was reversed soon. Mid-morning in the US, the ISM non-manufacturing unexpectedly rose to a very strong 60.1 from 59.8 (58.5 was expected). The dollar gained a few more ticks. EUR/USD trades currently in the 1.1630 area. USD/JPY is changing hands in the 114.15 area. So, the dollar trades with a marginal gain in a daily perspective, but holds within this week's extremely tight sideways range.

Sterling rebounds slightly on strong services PMI

Yesterday, sterling was hammered as the BoE signaled that two additional rate hikes would be sufficient for inflation to return close to the 2% target at the end of the 2019/20 policy horizon.

Today, the UK services PMI unexpectedly improved from 53.6 to 55.6 (53.3 was expected). The UK composite PMI also improved substantially from 54.1 to 55.8, indicating that UK growth might be decent at the start of the fourth quarter, despite ongoing uncertainty on Brexit. EUR/GBP traded in a narrow range near 0.8925 in the run-up the PMI publication. Initially, the sterling gains were very limited. Investors assumed that even a better-than-expected performance in the key services sector was not enough to change the BoE assessment anytime soon. During the US trading session, sterling gradually captured a better bid. EUR/GBP trades currently in the 0.89 area. Cable spiked temporary higher upon the publication of the US payrolls, but this USD move was soon reversed. The pair trades in the 1.31 area (from 1.3059 at the open this morning).

Elliott Wave Analysis: USDCHF Taking Price To New Highs

USDCHF is on a strong rise after breaking through some important levels on a daily chart last week, so we see market turning bullish, currently making a five wave rise. Specifically we see price trading within corrective wave 4), that can cause a strong push higher soon into wave 5.

USDCHF, 4H

Below we see the daily chart of USDCHF, where we see a completed higher degree wave B. The broken trendline can suggest a completed correction and a change in trend, brom bearish to bullish. So more gains may follow in days and weeks to come.

USDCHF, Daily

Greenbak Loses Positions after Labor Market Data Release

Volatility increased for the EUR/USD following the publication of surprising macro statistics on the labor market in the US. The unemployment rate decreased to 4.1% in October which is 0.1% less than expected, and the number of non-farm payrolls for October increased by 261,000 against the 312,000 forecasted. September's figure was also revised down from 33,000 to 18,000. The instability in the figures is blamed on the impact of hurricanes Irma and Harvey on economic activity.

Another important factor that will influence the mood of traders is confirmation that Jerome Powell will become the next head of the Fed. He is known for his hawkish views and good relations with the other FOMC members which has reduced fears around the appointment of the next Fed chairman.

The AUD/USD weakened at the beginning of the trading session and bears were stimulated by the disappointing data on retail sales, which have not changed in September despite the forecasted increase of 0.4%. Currently investors are fixing positions due to the fall of the greenback and ahead of the weekend.

The USD/CAD demonstrated a powerful descending impulse after the publication of the labor market statistics in the US and Canada. The USD fall was able to offset the rise in the unemployment rate in Canada by 0.1% to 6.3%. At the same time, employment has grown by 55,600 in October against 15,300 forecasted which is positive for the Canadian dollar.

EUR/USD

The EUR/USD keeps moving within the limits of the local rising channel. In case of maintaining the current positive impulse, the immediate targets will be located at 1.1730 and 1.1825. The closest support levels in case of decline will be in the 1.1600-1.1620 range and breaking through it, may become the trigger for a massive selloff with t potential drops to 1.1550 and 1.1500.

AUD/USD

The AUD/USD is correcting upwards after it was not able to continue falling. Negative dynamics may resume after touching the SMA100 and resistance at 0.7700. In this situation, the first target will be at 0.7635. On the other hand, gaining a foothold above 0.7700 is likely to become the basis for continued price increases up to 0.7740 and 0.7800.

USD/CAD

After a long price consolidation above the 1.2800 level, the quotes were able to break through it and within the current impulse, the USD/CAD may fall to 1.2665 and 1.2550. Potential correction is possible up to 1.2800 and SMA100 on the 15-minute chart. The RSI on the 15-minute chart is in the oversold zone, indicating a possible rebound in the near future.