Sample Category Title

October Jobs Rebound, Wages Disappoint

Job gains put the labor market back on track. Last month we emphasized taking the long view on the labor market, which worked well. Meanwhile, wages were flat but should drift upward again in the coming months.

October Jobs Rebound 261,000: Solid Q4 Economic Growth

Nonfarm payrolls jumped 261,000 in October, with the three-month average at 162,000 jobs. Job gains are consistent with 2.5-3.0 percent economic growth in the fourth quarter, with steady consumer spending, better business investment and a likely FOMC December rate hike.

A rebound in jobs appeared for leisure & hospitality and professional & business services. Meanwhile, there were continued solid gains in education & health (top graph). Government jobs, both federal and state & local, have averaged 12,000 over the past three months. In the goods sector, manufacturing employment posted a strong gain (24,000) and is in line with its average over the past three months, while hiring in construction was up 11,000 jobs for a second straight month.

Wage Growth Stalls in October

After the strongest monthly gain of the expansion, average hourly earnings growth stalled in October. The weak read stemmed in part from the rebound in leisure & hospitality employment, which pays the lowest average wages among major industries. Wages also edged down or slowed across a range of industries, including construction and education & health services. Compared to last October, average hourly earnings are up only 2.4 percent versus a 2.7 percent year-ago pace this time in 2016.

Despite the setback last month, we still expect to see average hourly earnings strengthen in the coming months. In contrast to October, the survey week for November contains the 15th of the month, which tends to produce somewhat stronger monthly gains. The year-over-year reading should also get a boost with a relatively easy base comparison considering monthly earnings growth was flat last November. Beyond the monthly dynamics, wage pressures should continue to build with labor becoming increasingly scarce as indicated by a further drop in unemployment and under-employment.

Unemployment Measures Continue to Tighten

The headline unemployment rate continued to fall, reaching a cycle low of 4.1 percent. The last time the rate was this low was December 2000. Likewise, the U-6 measure of unemployment, which includes marginally attached workers and part time workers who want full time work, fell to 7.9 percent. This is a more comprehensive look of slack in the labor market and is now tied with the previous cycle's low reached in December 2006.

The mean duration of unemployment remains at 26 weeks, which is higher than any level since 1982 and indicates structural issues persist, however. Finally, the labor force participation rate dipped in October to 62.7 percent and remains far below the average level of participation since 1990.

U.S. Labour Markets Recover the Hurricane-Related Weakness

Highlights:

- Payroll employment jumped to 261k from 18K in September as the downward impact from Hurricanes Irma and Harvey reversed.

- The October unemployment rate unexpectedly dropped to 4.1% from September's 4.2% though this did not prevent the annual increase in wages moderating to 2.4% from 2.8% the previous month.

Our Take:

The robust 261k rise in October payroll employment was in part bolstered by the unwinding of the hurricane-related impact in September that limited that month's payroll gain to only 18k (originally reported as down 33k). The average increase between the two months of 140k better reflects the underlying trend over this period. This modified increase does represent a slight easing from the 160k average increase over the previous six months though this is likely more indicative of labour markets approaching capacity, and reduced availability of workers, rather than indicating any weakening in demand. This tightness in labour markets was clearly conveyed by the unemployment unexpectedly dropping to 4.1% from and already low 4.2% in September. This October rate is significantly below the Fed's assumed long–run equilibrium range of 4.5% to 4.8%. However, indications of labour markets operating at, if not beyond, capacity are not putting any material upward impact on wages with the annual increase in October wages moderating to 2.4% from 2.8% in September and the 2.6% that prevailed the previous two months.

Today's employment report makes clear that the weakness in September employment was clearly a temporary weather-related phenomenon. Controlling for this factor, the underlying employment gains likely remain sufficient to keep the above-potential GDP growth evident in the second and third quarters continuing into the fourth quarter. Such is expected to keep the Fed gradually tightening policy. Our forecast assumes that the Fed will raise fed funds another 25 basis points at the next FOMC meeting in December followed by similar-sized hikes every quarter through 2018. The tightening is also consistent with inflation rising through the forecast though not threatening to move beyond the central bank's 2% objective.

Canada’s Trade Deficit Held Steady at -$3.2 Billion in September

Highlights:

- Canada's nominal merchandise trade deficit held steady at an elevated $3.2 billion in September.

- Energy exports rose 4.6% but that was offset by a fourth consecutive monthly drop in non-energy shipments.

- Import growth has also softened but - unlike exports - not enough to retrace earlier strength.

- We continue to expect GDP growth in Canada slowed in Q3 from the outsized pace of growth over the past year but still look for slightly 'above-potential'

Our Take:

Non-energy export volumes declined for a fourth consecutive month with the cumulative drop more than reversing what had been an encouraging increase over the prior three months. Energy shipments provided some offset, rising 4.6% in volume terms. Part of the recent non-energy export weakness has been related to production disruptions in the auto and chemical sectors over the summer. We continue to expect modest growth in exports going forward as global trade flows improve and demand from the U.S. industrial sector strengthens. Nonetheless, it is clearly difficult to argue that there has been much of an acceleration in external demand year to-date in 2017 with annual export growth not tracking significantly different than the 1.0% increase last year.

On the other hand, domestic demand still looks relatively solid. Goods import volumes inched 0.9% lower in Q3 (at an annualized rate) but that retraced little of an 11.2% surge in Q2. Another quarterly increase in equipment imports - notwithstanding softer readings in August and September - mean business investment probably rose again in Q3. Separately released labour market data for October this morning suggests that Canadian businesses are continuing to hire. Clearly growth in the economy has slowed from the outsized - and unsustainable - 3.7% rate mid-2016 to mid-2017. We, nonetheless, still expect overall GDP increased 1.7% in Q3 and look for growth to be sustained at a slightly 'above-potential' 2% rate going forward.

Plenty of Positives as Canada’s Labour Market Continued to Improve in October

Highlights:

- Employment rose 35k in October, the 11th consecutive monthly increase and the best gain since June.

- Despite solid hiring, the unemployment rate edged up to 6.3% as more people looked for work.

- Wage growth picked up to 2.4% year-over-year from as low as 0.5% in April. October's rise was helped by minimum wage hikes in six provinces, all of which were larger than last year's increases.

- Most of October's job growth reflected a broadly-based increase in goods sector employment, led by the construction industry. The services sector, which has accounted for most of Canada's job growth over the last year, was closer to flat.

Our Take:

Canada's streak of job growth continued unabated in October with employment rising 35k, well in advance of market expectations. And there were plenty of positive takeaways beyond the headline figure. Job gains were concentrated in private sector, full-time work and wage growth (helped by minimum wage hikes in several provinces) continued to trend higher from the lows recorded earlier this year. Youth labour market conditions, which Bank of Canada Governor Poloz put in the spotlight last week, also improved with employment for 15-24 year-olds rising 18k and labour force participation increasing. Other, less positive developments - the unemployment rate ticked higher and average hours worked edged lower - don't take much away from an overall solid labour market report. The unemployment rate is still down 0.7 ppts from a year ago and hours worked are close to their 10-year average.

Today's employment numbers reinforce some of the themes from the Bank of Canada's latest economic outlook. The acceleration in job growth relative to last quarter points to GDP growth returning to an above-trend pace in Q4. Stronger wage growth is also consistent with their expectation that tighter labour market conditions will feed through to wages, albeit with some lag. Finally, an increase in labour force participation might indicate there is a bit more room to run on the employment side than a zero output gap would suggest. All told, we think the BoC will be pleased with today's report but not surprised enough to raise rates again this year after a cautious tone was expressed last week.

Dollar Dips as US Jobs Report Disappoints

Sellers wasted no time in attacking the Dollar on Friday, following news that the United States added another 261,000 jobs to its economy in October.

While the headline Non-Farm Payroll (NFP) data continues to highlight the underlying strength of the U.S. jobs market, it is still below the market expectation of 312,000. Digging deeper into the report, the key culprit behind the Dollar selloff was most likely average monthly earnings, which remained flat in October. With tepid wage growth fueling concerns that inflation could remain depressed for extended periods, the markets may start debating how often the Fed raises rates in 2018. On the bright side, the unemployment rate dropped to a 17-year low at 4.1%, after the hurricane disruptions.

Taking a look at the technical picture, the Dollar Index is under pressure on the daily charts. Prices have descended towards 94.50, with bears currently eyeing 94.00. Sustained weakness below this level puts the current bullish setup at threat, with the next level of interest at 93.50. In an alternative scenario, the Dollar index needs to break above 95.00, for further upside.

Jerome Powell is in the building

Financial markets offered a fairly muted response on Thursday, after President Donald Trump nominated Jerome Powell as the next Fed Chair. Trump's decision is in line with market expectations, and Powell is expected to keep the 'status quo', so the flat reaction short-term is understandable. Although markets expect Powell to take the baton from Yellen by following the current monetary policy course, it should be kept in mind that he is seen as a cautious dove. While it is probably too early to make any assumptions, a dovish Fed head could weigh on the prospects of higher US interest rates in 2018.

Sterling pummeled and thrashed

Sterling was pummeled, pounded and thrashed by sellers on Thursday, after the Bank of England moved forward with a 'dovish rate hike'. This was the first time in over a decade that UK interest rates were increased, and the heavy tone of caution radiating from the meeting raised concerns over the future path of rates in 2018. With Brexit uncertainty and concerns over slowing economic growth weighing heavily on the currency, further downside is on the cards.

The Pound attempted to recover on Friday morning, following reports of Britain's service sector growing at its fastest rate in six months. UK Services PMI jumped 55.6 in October, up from 53.6 in September, which seemed to offer some confidence to bulls. The upside seems limited, especially when considering how Thursday's dovish hike has eroded buying sentiment towards the currency.

From a technical standpoint, Sterling is under pressure on the daily charts. Sustained weakness below 1.3050 may open a path towards 1.3000 and 1.2970, respectively.

A trading week to remember…..

Investors are likely to remember the first trading week of November as one where the Bank of England raised UK interest rates for the first time in over a decade. Reports of Trump unveiling his full tax plan, and the nomination of a new Federal Reserve Chair, has added some spice to proceedings. This, coupled with October's mixed U.S. jobs report, is likely to give investors lots to ponder over the weekend.

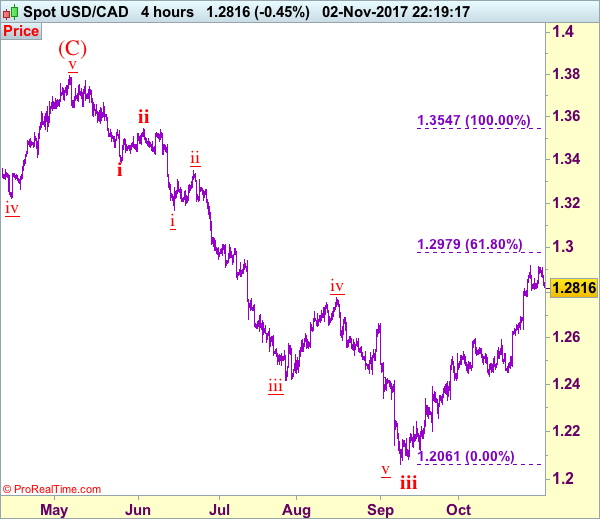

Trade Idea: USD/CAD – Exit long entered at 1.2755

USD/CAD - 1.2740

Trend: Near term up

Original strategy :

Bought at 1.2755, Target: 1.2955, Stop: 1.2695

Position: - Long at 1.2735

Target: - 1.2955

Stop: - 1.2695

New strategy :

Exit long entered at 1.2705

Position: - Long at 1.2755

Target: -

Stop:-

Current selloff after meeting renewed selling interest at 1.2836 suggests a temporary top has been formed at 1.2917 last week and downside risk remains for this retreat to bring retracement of recent rise, hence weakness to 1.2700-05 cannot be ruled out, however, downside would be limited to support at 1.2636 and bring rebound later. Only a drop below 1.2636 would signal recent rise has ended at 1.2917, bring further fall to 1.2600 and later towards 1.2550-60.

In view of this, would be prudent to exit long entered at 1.2755 and stand aside for now.above 1.2800 would bring test of said resistance at 1.2836 but a sustained breach above there is needed to revive bullishness and signal the pullback from 1.2917 has ended instead,bring further gain to 1.285-80, then later towards said resistance at 1.2917. Having said that, as we are still treating this rebound from 1.2061 as wave iv, reckon 1.2975-80 (61.8% Fibonacci retracement of wave iii) would limit upside and 1.3000 should hold, bring selloff later in wave v. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Canada: Job Growth Perks Up in October on Full Time Hiring

Canada recorded an eleventh straight month of job gains as 35.3k net new positions were added in October. The unemployment rate ticked up a touch to 6.3% after holding at 6.2% for two months, as more people entered the labour force.

Full-time jobs dominated gains in the month, adding 88.7k jobs. However, about 53.4k part-time jobs were shed in the month, the second consecutive month of part-time job losses. The private sector added 39k jobs in October, while there was little change in public sector employment. Self-employment was little changed in the month.

Jobs in good-producing industries led the gain, adding 33.9k positions, driven largely by construction (+18.4k), and a notable uptick in manufacturing (+7.8k). The services side of the economy remained subdued for the second consecutive month (+1.4k), as healthy gains in sectors such as other services (+21.4k) and information culture and recreation (+15.3k) were largely offset by a large decline in trade (-35.9k). Statistics Canada notes that "Other Services" includes services related to civic and professional organizations, and personal and laundry services.

Regionally, Quebec recorded strongest job gain (+18k), adding net 33k full-time jobs while part-time jobs fell back 15k. Job gains elsewhere were less robust, with net increases recorded everywhere except Ontario and British Columbia; both provinces saw employment little changed in October.

Growth in both hourly wages and hours worked accelerated in October. The headline hourly wage rate accelerated further, to 2.4% on a year-on-year basis, while hours worked rose 2.7% y/y, albeit from a weak base, with the month-on-month increase much more modest.

Key Implications

Overall, October was a strong report, with robust full-time job gains, a slight uptick in the participation rate, and acceleration in hourly wage growth and growth in hours worked. This morning's data extends the streak of job gains to 11-months.

Hourly wage growth is likely to raise some eyebrows at the Bank of Canada, holding above 2% for the second consecutive month and even accelerating a touch. With Governor Poloz emphasizing labour market developments as a key indicator of capacity pressures in last week's interest rate announcement, the persistent move back up to over 2.0% growth in wages will be viewed as confirmation that economic slack has largely diminished.

Broader measures of labour market slack have improved so far this year. For example, the unemployment rate measure including discouraged searchers, and involuntary part-timers (R8) has trended down sufficiently such that it's only a touch elevated relative to the pre-crisis trough. Moreover, there has been some progress on the share of discouraged workers who are not part of the labour force but want to work. On the other hand, youth employment participation rates remain stubbornly below pre-crisis levels, and it remains unclear if this trend can be fully attributed to students focusing on studies.

The Canadian labour market remains consistent with a view that the Canadian economy is operating at or very near to capacity. As such, we reiterate what we said last week after the Bank of Canada decision. The economy is in something of a sweet spot, as economic slack is gradually giving way to rising capacity pressures and growth evolving back towards its longer-term trend. But, inflation remains relatively subdued with some evidence that wage growth is persistently ticking upward, and housing and trade risks help skew risks toward the downside. Altogether, this removes any immediate urgency to raise interest rates from current levels, but more signs of rising capacity pressures will eventually lead to another rate hike as early as January 2018.

A Hot Canadian and U.S Jobs Market

- US Labor Oct non-farm payrolls +261k; consensus +315k

- US Oct Unemployment Rate +4.1%; Consensus +4.2%

- US Oct Average Hourly Earnings -0.04%, or -$0.01 to $26.53; Over Year +2.4%

- US Oct Private Sector Payrolls +252k and Government Payrolls +9k

- US Oct Labor-Force Participation Rate 62.7%

- US Sep Payrolls Revised to +18K; Aug Revised to +208K

U.S. employers hired at a strong pace last month, and revisions showed the labor market weathered hurricane damage better than previously estimated.

Disappointing was wages, it failed to break out, rising +2.4% from a year earlier, a slowdown from last month.

Strong revisions

Payroll growth was significantly stronger than previously estimated in recent months. Upward revisions showed +90k more jobs were added to payrolls in August and September than previously reported.

September hiring was revised to a gain of +18k from an initial estimate of down -33k. When combined with August and September's job growth, data show the economy added jobs over the last three months at a pace of +162k a month.

Despite being a strong print, it did not beat market expectations. The dollar is trying to gain some traction across the board (€1.1663, £1.3030 and ¥113.34), with the one exception CAD (C$1.2742).

Canadian Job Market on Fire

- Canada Oct net jobs +35,300 from Sep vs. forecast at +15,000

- Canada Oct full-time jobs +88,700; part-time -53,400

- Canada Oct jobless rate +6.3%; Sep +6.2%

- Canada Oct avg. hourly wages +2.4% y/y

Canada added jobs (+ 35.3k) in October at a stronger-than-expected pace amid a slowing economic backdrop, with full-time employment surging and wage gains accelerating for a second straight month.

The unemployment rate rose from a post crisis low of +6.2% to +6.3%, but that was due to more young people searching for work.

October's advance marked the 11th straight month of job gains, which is the longest streak in over a decade. All of the net new jobs added were in the private sector and of the full-time variety, which tend to offer higher pay and steady benefits compared with part-time work.

The 'loonie' has strengthened across the board +0.64% to C$1.2729 outright and +0.74% EUR/CAD to €1.4832.

U.S. Economy Bounces Back from Hurricane Disruptions

Non-farm payrolls rebounded 261k positions in October, after hurricane-related disruptions held back job growth to a meagre 18k in September (that figure was revised up from an earlier-reported 33k loss). Still, the unemployment rate ticked even lower to 4.1%.

Given the disruptions from the hurricanes, the details of the payrolls report must be taken with a grain of salt. Employment in food services and drinking places increased sharply (+89k) over the month, mostly offsetting a decline in September that reflected the impact of the hurricanes. Business services (+50k) and education and health sector (+41k) hiring continue to be solid. On the goods side, employment also accelerated to 33k new jobs, on healthy hiring in manufacturing (+24k).

On the household side, the decline in unemployment rate is less positive given it was driven by a sizeable drop in the labor force (-765k). The participation rate declined to 62.7%, and has shown little movement over the past 12 months. The employment to population ratio also fell to 60.2%, but is still 0.5%-points higher than a year ago.

Average hourly earnings were unchanged in October, taking the year-on-year pace to a modest 2.4%.

Key Implications

Given September's hurricane-related payroll disappointment, the bar was set high for October, and on the surface September fell short. However, revisions over the past two months totaled 90k jobs, should vanquish any disappointment.

Today's sold rebound combined with the strong economic momentum in the third quarter, certainly argues for a rate hike by the FOMC in December. However, we still have yet to see a notable pick-up in core inflation and now wage growth has disappointed. We expect that Yellen will still be comfortable taking rates another 25 bps higher in what will likely be her second last meeting as Chair

Canada’s Trade Deficit Unchanged in September

Canada's trade deficit was unchanged at $3.2 billion in September as both imports and exports were down 0.3%. In real terms, export and import volumes both edged down 0.2%.

The decline in exports was driven largely by motor vehicles and parts, with a strike that began mid-month contributing to a 16% drop in exports of passenger cars and light trucks. Most other industries recorded gains during the month, led by energy exports which were up 7.2% during the month.

The drop in imports was fairly widespread, however an 18.5% surge in energy product imports and a 7% increase in metal ores and non-metallic minerals provided some offset.

Canada's trade surplus with the U.S. narrowed to $2.2B in September (preciously $2.7B), as exports were down 1.2% and imports rose 0.4%. Canada's trade deficit with the rest of the world narrowed to $5.3 billion (previously $5.8B), with exports up 2.4% and imports down by 1.4%.

Key Implications

September marks the fourth consecutive month in which export volumes declined. For the quarter as a whole, they were down 3.8%. With imports falling by a slight 0.2% over the same period, net trade will weigh on overall growth in Q3 - which is now tracking under 2% - and provides a weak hand off for the fourth quarter.

Going forward, conditions should remain supportive for exports to resume growth, with a solid U.S. economy likely to keep demand for Canadian-made goods healthy and a Canadian dollar that has fallen back to around 78 US cents. However, the strike at an auto assembly plant that lasted into mid-October will limit output and thus exports during the month.

With the Bank of Canada's next move heavily data dependent, the soft export performance does not support a move higher. However, several data reports will be released between now and the Bank's next meeting in December. At this point, we don't expect the Bank to hike until early next year.