Sample Category Title

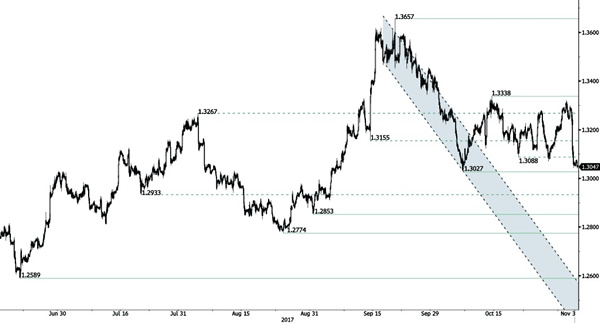

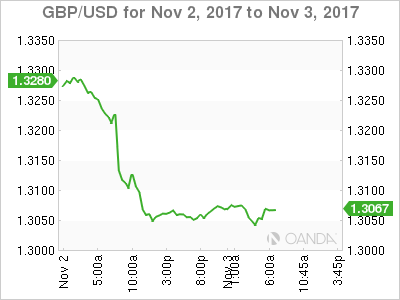

GBP/USD Strong Decline

GBP/USD is back towards resistance given at 1.3027 (06/10/2017 low). String resistance is given at 1.3338 (13/10/2017 high). Expected to show continued decline.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Slight Increase

EUR/USD is edging higher after setting a new hourly support at 1.1575 (27/10/2017 low). Hourly resistance is located at 1.1658 (30/10/2017 high). Expected to show some short-term consolidation.

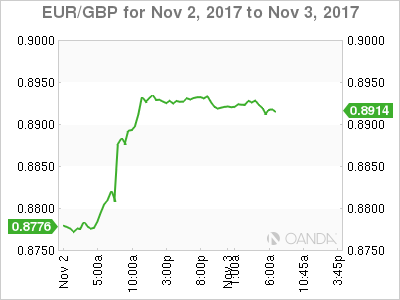

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Next Up, U.S Jobs Report

Friday November 3: Five things the markets are talking about

The October U.S jobs report is set for release at 08:30 am EDT and after the September headline print revealing the first monthly drop in seven-years – attributed to a hurricane effect – investor expectations for last month's reading are considered very high.

Market consensus is looking for a headline print of +310k and an unemployment rate unchanged at +4.2%.

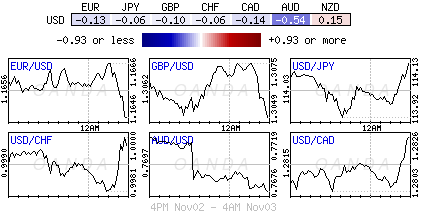

The 'mighty' dollar is holding steady across the board, a day after the greenback had slipped after Republicans in the U.S House of Representatives released proposals to overhaul the U.S tax code. Congressional passage of this legislation is far from certain, and reasons enough for the dollar to see 'red.'

President Trump's nomination yesterday of Jerome Powell to be the next Fed chair came as no surprise. To bond dealers, his successful nomination is considered more of the same – broadly extending the path that the Fed reinforced at this week's meeting – a hike in December and more to come in 2018.

Elsewhere, the U.S trade balance and Canadian unemployment numbers (08:30 am EDT) will also help to set this morning's trading tone.

1. Stocks mixed reaction

Asian equities were mixed overnight after Wall Street reacted uncertainly to emerging details of the U.S tax change proposals.

Note: Japanese markets were closed Friday for a holiday.

Down-under, Australian stocks stood out, hitting fresh 2017 highs on gains in commodity prices. Australia's S&P/ASX 200 Index rallied +0.5%, while South Korea's Kospi index rose by +0.4%.

In Hong Kong, stocks ended firmer overnight, as China slowdown worries were offset by the upbeat mood from strength on Wall Street. The Hang Seng index rose +0.3%, while the China Enterprises Index was unchanged.

Note: For the week, the Hang Seng was up +0.6%, but the HSCE lost -0.4%.

In China, the major indexes slid on Friday to end the week lower, led by Shanghai stocks posting their worst week in three-months, as weak growth in the service sector last month heightened investor worries about an economic slowdown. The blue-chip CSI300 index eased -0.1%, while the Shanghai Composite Index closed down -0.4%.

Note: For the week, CSI300 lost -0.7%, while SSEC dropped -1.3%.

In Europe, regional indices trade mostly higher across the board with the exception of the Spanish Ibex ahead of October's U.S jobs report..

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx600 +0.2% at 395.6, FTSE +0.3% at 7576, DAX +0.4% at 13493, CAC-40 flat at 5511, IBEX-35 -0.9% at 10359, FTSE MIB +0.1% at 23064, SMI +0.1% at 9291, S&P 500 Futures +0.1%

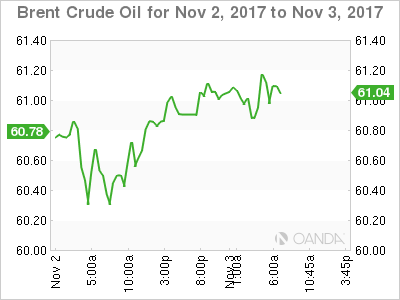

2. Oil edges up to near two-year highs as market tightens, gold unchanged

Oil prices remain better bid, trading atop of their two-year highs, as the outlook remains upbeat, as OPEC-led supply cuts have tightened the market and drained inventories.

Brent crude is up +13c, or +0.2% at +$60.62 per barrel. The contract is up by more than a third from its 2017-lows in June. U.S light crude (WTI) is up +24c, or +0.4% at +$54.54, almost +30% above its 2017-lows in June.

Investor confidence has been supported by an effort this year lead by OPEC and Russia to hold back about -1.8m bpd in oil production to tighten markets.

On Thursday, the Saudi Energy Minister Khalid al-Falih said supply and demand balances were tightening and oil inventories falling, while compliance with the OPEC-led pact to curb supplies had been “excellent”.

Note: Overall, oil markets have been slightly undersupplied this year, resulting in inventory drawdowns and the OPEC pact to withhold supplies runs to March 2018, but there is growing consensus to extend the deal to cover all of next year.

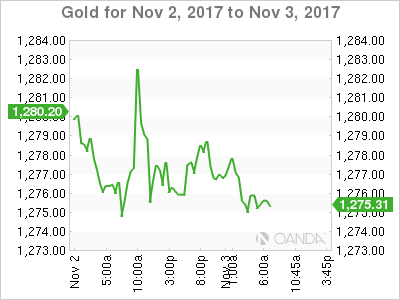

Ahead of the U.S open, gold prices are trading in a narrow range as the U.S dollar trades steady amid caution ahead of non-farm payrolls (NFP). Spot gold is mostly unchanged at +$1,275.82 per ounce, and is on track for its first weekly gain in three. Yesterday, the 'yellow' metal hit its highest in about two weeks at +$1,284.10 an ounce.

3. Sovereign yields fall

U.K bond yields haven fallen in the past 24-hours after yesterday's BoE's announcement of the first rate hike in ten-years (+25 bps to +0.50%). The 7 to 2 vote spilt, and the removal from the minutes of previous reference to monetary policy tightening by more than markets expect, meant that the move has been interpreted as a 'dovish' or 'token' hike.

U.K's 10-year gilt yield has declined -2 bps to +1.335%, the lowest in almost seven weeks.

In the U.S, the gap between 5- and 30-year Treasuries yields have shrank to the narrowest in almost a decade. The market has been happy to drive down longer-end yields after President Trump said he would nominate Jerome Powell to run the Federal Reserve from February.

Powell has shown a 'Yellen-esque' sensitivity towards emerging markets and a gradual U.S rate path – extending the path that that Fed members reinforced at this week's FOMC meeting – a hike in December and more to come in 2018.

The yield on U.S 10-year Treasuries has backed up +1 bps to +2.35%.

4. 'Big' dollar waiting for jobs headline

The FX market is holding steady after President Trump nominated Jerome Powell as the new Federal Reserve chair. Investors will take their cues from this morning's U.S non-farm payrolls (NFP). This morning's headline print is expected to keep the door ajar for a December Fed rate hike.

GBP/USD (£1.3067) continues its soft tone following yesterday's dovish rate hike by the BoE, but off its intraday lows after this morning's U.K services PMI print (see below) came in better than expected.

In yesterday's BoE statement, dealers noted that BoE dropped the wording that “interest rates may need to rise more than markets expected” and that Governor Carney had now linked the future path of rates to the outcome of the Brexit talks.

5. U.K services sector grows at fastest rate in six months

Data this morning showed that Business activity in the U.K's service sector grew last month at the fastest pace in six-months and significantly faster than anticipated.

IHS Markit Ltd. said its purchasing managers index for the services industry -which accounts for some +80% of the U.K economy – rose to 55.6 in October, up from 53.6 in September, and above market expectations that forecasted a -0.2 point drop. The growth in activity was supported by improved order books and resilient client demand, the survey indicated.

Today's data goes some way's to justify yesterday's first BoE rate hike in a decade.

However, the pace of job creation slowed to a seven-month low, and sentiment about future growth prospects remained subdued amid Brexit uncertainty and concerns about business investment.

Positive UK Services PMI Fails To Inspire Sterling Bulls

Sterling bulls were hesitant to enter the scene on Friday morning, despite reports Britain’s service sector is growing at its fastest rate in six months.

Although UK Services PMI jumped 55.6 in October, up from 53.6 in September, the fairly muted reaction suggests that investors may be redirecting energy and attention elsewhere. Thursday’s dovish rate hike, has not only encouraged sellers to pummel Sterling, but has also heavily bruised buying sentiment towards the currency. With the bias towards the Pound currently tilted to the downside, any appreciation could be viewed as a technical bounce and an opportunity for bears to begin fresh rounds of selling. Taking a look at the technical picture, Sterling is under intense selling pressure on the daily charts. Sustained weakness below 1.3050 may open a path towards 1.3000 and 1.2970, respectively.

Crude Oil On A Solid Footing, NFPs In Focus

USD flat-lined amid Fed Chair nomination, tax plan in focus

The nomination of Jerome Powell as next Federal Reserve Chairman came as no surprise. The US dollar barely reacted to the news. The US Dollar Index treaded water within its weekly range, between 94.4 and 95. Donald Trump definitely made the choice of stability and continuity by choosing the New York republican Fed President. The USD edged slightly lower after the announcement as investors discounted completely the risk that a more hawkish candidate will replace Yellen. Similarly, US yields lost some ground yesterday, especially on the long-end of the curve. The 10-year eased to 2.35%, while the 30-year returned to 2.83%.

Today is NFP Friday and we’ll likely get some action following last month’s disappointing reading. NonFarm payrolls are expected to come in at 313k in October after contracting 33k in September. As usual, investors will pay a close attention to wage growth with average hourly earnings anticipated to rise 2.7%y/y versus 2.9% in September. The release of the September job report will be our best and last shot to get some volatility this week. Unfortunately, the market is more focus on developments on Trump’s Tax plan, as it will have a larger impact on inflation and growth, should it be approved. In addition, investors realized that a stronger job market do not ensure, at all, sustained inflation pressures.

Commodity Currencies lagging oil

Oil prices are looking to break resistance at $55.03 making 2017 new highs. Decline oil stocks and solid growth in demand has overcome weather and geopolitical issues. Brent is now trading above $60brl and futures backwardation has invited deeper buying in the long end of the curve. OPEC has sighted their success in supply restrain pointing to falling inventories. It seem that WTI at $55 is likely to maintain.

However, commodity liked currencies have not following oil prices higher. CAD and NOK have diverged significantly from oil prices in recent weeks. It is not uncommon for decoupling but the divergence rarely is for an extended period. The rationale is the convergence of higher oil at the same time US rates have risen, which reduced the sensitivity to external influenced. With US yields stabilizing we would watch for CAD and NOK to catch up to higher oil.

Chine Gold consumption increases while output declines

Price of gold remains above $1270. Since the start of the year, we recall that gold has gained almost 6% underlining global uncertainties. It is important to assess gold’s potential by looking at China as a significant part of the market takes place in China. The Chinese consumption has increased in the first 3 quarters of this year of 15.49% y/y. This increase has happened against the backdrop of the stock market recovery. Indeed Chinese stocks took a big hit in 2015.

In China, the gold output has strongly declined, facing a 3.76% decline since the start of the year. On top of that Chinese regulations are also stricter, in particular regarding the waste from gold mining. Chinese authorities have considered that the environmental impact of producing gold has overcome the proceeds from the sale.

In our view, we also believe that levels of production cannot be sustainable over the long haul. The reserves are falling and then the production should keep on declining. We consider that it is likely that the gold price should head higher within the next few month to reflect those data.

Euro Steady Ahead Of US Nonfarm Payrolls, Wage Growth

The euro continues has ticked lower in the Friday session. Currently, EUR/USD is trading at 1.1644, down 0.09% on the day. On the release front, there are no eurozone indicators on the schedule. Employment data will be in the spotlight on Friday, as the US releases Average Hourly Earnings, Nonfarm Payrolls and the unemployment rate. The markets are expecting NFP to rebound to 311 thousand, but Average Hourly Earnings is forecast to slow to 0.2 percent. No change is expected in the unemployment rate, with an estimate of a sizzling 4.2 percent. As well, the US releases ISM Non-Manufacturing PMI, which is expected to drop to 58.5 points.

A strong manufacturing sector has been an important factor in the stronger eurozone economy, and September Manufacturing PMIs continue to point to expansion early in the fourth quarter. The German Manufacturing PMI held at 60.6, its highest level since April 2011. Eurozone Manufacturing PMI isn’t far behind at 58.6, and accelerated for a third straight month. The German employment market remains robust, as unemployment rolls have declined for three straight months. Unemployment rolls have now dropped in all but two readings since June 2015.

There were no surprises from the Federal Reserve on Wednesday. The Fed’s rate statement was little more than a run-up to the December rate decision, as the Fed maintained interest rates at a range of 1.00 percent to 1.25 percent. The Fed indicated that a rate increase is very likely at the December meeting, and was careful not to change any of the wording in its statement regarding future rate hikes. The rate statement noted that hurricanes which hit the US had caused a decline in payrolls in September, but the Fed did not expect the hurricanes to “materially alter the course of the national economy over the medium term.” The markets are expecting a strong rebound in nonfarm payrolls – the forecast for US nonfarm payrolls is a robust 311 thousand, after a decline of 33 thousand in September. Still, wage growth, which was remained soft despite the strong economy, is expected to slow to 0.2 percent, as inflation remains the Achilles heel of a robust US economy.

Market Update – European Session: UK Services Data Beats Expectations, Focus On US Jobs Report

Notes/Observations

US Non-farm payroll expected to rebound from the hurricane-affected Sept report

Negative economic impact of Brexit is the main challenge for BOE

Overnight

Asia:

China Oct Caixin Serv PMI: 51.2 v 50.6 prior

Australia Sept Retail Sales data mixed M/M: 0.0% v 0.4%e; Q3 Ex Inflation Q/Q: 0.1% v 0.0%e

Europe:

ECB’s Weidmann (Germany) reiterated that ECB board members were in agreement that accommodative monetary policy remains necessary. He noted that it was far too early to discuss successor for Draghi (**Note: term ends in Nov 2019)

Spain state prosecutor asks judge to issue arrest warrant for former Catalan President Puigdemont (**Note: Puigdemont: Arrests are an attack on democracy; demands end to political repression)

Americas:

President Trump appointed Jerome Powell to the Fed Chair position (as expected)

GOP leadership tax plan summary document: To set tax brackets at zero, 12%, 25%, 35% and 39.6%. Would keep mortgage interest tax deduction for existing loans and newly purchased homes up to $500K [reduced from $1M] and allow state and local property taxes deduction up to $10K

President Trump: House Republican tax bill important step towards tax relief; will work tirelessly to deliver historic tax cuts and reforms

White House National Security Adviser McMaster: Trump will reiterate North Korea is threat to entire world on Asia trip (**Note: Trump embarks on a 10-dayt Far East trip on Fri)

Venezuela President Maduro stated that would restructure all foreign debt after Fri, Nov 3rd

Economic Data

(IN) India Oct PMI Services: 51.7 v 50.7 prior (2nd month of expansion), PMI Composite PMI: 51.3 v 51.1 prior

(IE) Ireland Oct Services PMI: 57.5 v 58.7 prior (62nd month of expansion but lowest since Nov 2016), Composite PMI: No est v 57.6 prior

(RU) Russia Oct PMI Services: 53.9 v 55.0e (21st month of expansion), PMI Composite: 53.2 v 54.8 prior

(TR) Turkey Oct CPI M/M: 2.1% v 1.7%e; Y/Y: 11.9% v 11.5%e; CPI Core Index Y/Y: 11.8% v 11.2%e

(ZA) South Africa Oct PMI (whole economy): 49.6 v 48.5 prior

(SE) Sweden Oct PMI Services: 61.4 v 63.8 prior

(ES) Spain Oct Net Unemployment M/M: +56.8K v +27.9K prior

(NG) Nigeria Oct PMI: 55.8 v 54.9 prior

(NO) Norway Oct Unemployment Rate: 2.4% v 2.5%e

(UK) Oct Services PMI: 55.6 v 53.3e (15th month of expansion), Composite PMI: 55.8 v 53.8e

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2024, 2027, 2034 and 2051 bonds

(ZA) South Africa sold ZAR vs. ZAR800M indicated in I/L 2029, 2033 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 395.6, FTSE +0.3% at 7576, DAX +0.4% at 13493, CAC-40 flat at 5511, IBEX-35 -0.9% at 10359, FTSE MIB +0.1% at 23064, SMI +0.1% at 9291, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade mostly higher across the board with the exception of the Spanish Ibex, as Indices trade in a sideways fashion ahead of October's US Non Farm Payrolls.

A number of components from the French CAC reported, with Air France down sharply after initially touching a multi year high following results, while SocGen trades lower after missing estimates. Altice trades lower after trimming its outlook and Lonmin trades over 15% lower after its production update and the delay of their FY results.

Elsewhere renewable energy stock are under pressure after proposed US tax changes that could cut tax credit by over a third.

Looking ahead notable earners include Duke Energy and CBRE.

Equities

Consumer discretionary [Air France [AF.FR] -8.2% (Earnings), L'Oreal [OR.FR] -0.6% (Earnings)]

Materials: [Lonmin [LMI.UK] -20% (Trading update, to delay FY results)]

Financials: [ SocGen [GLE.FR] -3.3% (Earnings), Axa [CS.FR] -1.6% (Earnings)]

Telecom: [ Altice [ATC.NL] -10.0% (Earnings)]

Energy: [Vestas Wind [VWS.DK] -9.5% (Proposed US tax changes)]

Speakers

ECB's Nowotny (Austria): ECB took right decision at last week policy meeting. Reiterated economy was improving substantially but not there yet. Inflation moving in the right direction and believed it could be higher than current expectations in 2018. Reiterated too early to discuss an end date for QE and that the ECB would not run into any scarcity issues on bond buying

BOE Dep Gov Broadbent: Spare capacity has been diminishing (in-line with recent QIR). Nov rate hike was a moderate one and might need a couple more rate hikes (**Note: BOE currently forecasting 2 hikes by 2020). Brexit was clearly having some impact on economy; affecting investment and spending

ECB's Angeloni (SSM board member): To rigorously review bank's plans to reduce bad loans

Greece PM Tsipras: Greek bailout review will close soon

Norway Central Bank (Norges) Dep Gov Nicolaisen: Low rate globally limits monetary policy maneuvers

Russia govt spokesperson: President Putin could meet Trump on sideline of APEC Summit meeting in Vietnam

Currencies

FX market was holding steady after Trump chose Jerome Powell as the new Federal Reserve chair (as speculated). US Non-farm payroll expected to rebound from the hurricane-affected Sept report and keep the door open for a 3rd rate hike in Dec.

EUR/USD at 1.1645 area ahead of the NY morning.

GBP/USD continued its soft tone following Thursday’s dovish rate hike by the BOE. Pait hit a 1-month low at 1.3040 in the session. Dealers noted that BOE dropped wording that interest rates may need to rise more than markets expected and that BOE Gov Carney had now linked the future path of rates to the outcome of the Brexit talks. Focus was on the PMI Services data which beat expectations and helped the GBP to move off its worst levels. The data gave some justification to the recent BOE rate hike

Fixed Income

Bund futures trade at 162.81 up 17 ticks, and back towards the October high. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 125.30 up 14 ticks following yesterday’s BOE rate hike that investors interpreted as dovish. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.90 then 124.24.

Friday’s liquidity report showed Thursday’s excess liquidity rose to €1.849T from €1.838T and use of the marginal lending facility rose to €188M from €237M

Corporate issuance saw 5 issuers raise $4.0B in the primary market. For the week ending Nov 1st Lipper fund flows reported IG fund net inflows of $3.6B and High yield funds reported net inflows of $1.2B, most since August.

Looking Ahead

06:00 (EU) Daily Euribor Fixing

06:00 (FR) France Debt Agency (AFT) announces upcoming auctions

06:30 (AT) ECB’s Nowotny (Austria)

06:30 (NO) Norway Central Bank (Norges) Gov Olsen in Bergen

06:30 (ZA) South Africa to sell ZAR800M in I/L 2029, 2033 and 2046 bonds

07:00 (IE) Ireland Oct Live Register Monthly Change: No est v -0.3K prior

07:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month Bills (£0.5B, £1.0B and £2.0B respectively)

07:30 (IN) India Weekly Forex Reserves

07:45 (US) Daily Libor Fixing

08:00 (CL) Chile Sept Retail Sales Y/Y: 4.3%e v 6.0% prior

08:30 (US) Oct Change in Nonfarm Payrolls: +313Ke v -33K prior, Change in Private Payrolls: +302Ke v -40K prior, Change in Manufacturing Payrolls: +15 v -1K prior

08:30 (US) Oct Unemployment Rate: 4.2%e v 4.2% prior, Underemployment Rate: No est v 8.3% prior

08:30 (US) Oct Average Hourly Earnings M/M: 0.2%e v 0.5% prior; Y/Y: 2.7%e v 2.9% prior; Average Weekly Hours: 34.4e v 34.4 prior

08:30 (US) Sept Trade Balance: -$43.3Be v -$42.4B prior

08:30 (CA) Canada Oct Net Change in Employment: +15.0Ke v +10.0K prior; Unemployment Rate: 6.2%e v 6.2% prior

08:30 (CA) Canada Sept Intl Merchandise Trade (CAD): -3.0Be v -3.4B prior

09:05 (UK) Baltic Dry Bulk Index

10:00 (US) Sept Final Durable Goods Orders: 2.0%e v 2.2% prelim; Durables Ex Transportation: No est v 0.7% prelim

10:00 (US) Sept Factory Orders: 1.2%e v 1.2% prior; Factory Orders (ex-transportation): No est v 0.4% prior

10:00 (US) Oct ISM Non-Manufacturing Composite: 58.5e v 59.8 prior

10:00 (MX) Mexico Sept Leading Indicators M/M: No est v 0.17% prior

10:45 (US) Oct Final Markit Services PMI: 55.9e v 55.9 prelim, Composite PMI: No est v 55.7 prelim

11:00 (EU) Potential European sovereign ratings after European close

(BE) Belgium Sovereign Debt to be rated by Moody's

(NO) Norway Sovereign Debt to be rated by DBRS

(TR) Turkey Sovereign Debt to be rated by S&P

12:15 (US) Fed’s Kashkari (dove, voter)

13:00 (US) Weekly Baker Hughes Rig Count data

15:00 (CO) Colombia Oct Total PPI M/M: No est v 0.4% prior

16:15 (FR) ECB’s Coeure (France)

XAU/USD Analysis: Forms Symmetrical Triangle

In result of the previous trading session, the exchange rate has formed symmetrical triangle pattern. A combination of the 55-, 100- and 200-hour SMAs in conjunction with the weekly PP located at 1,274.00 suggests that the pair most probably is going to make a breakout in the upward direction. On the other hand, that side also contains a combined resistance set up by the 61.8% Fibonacci retracement level and the updated monthly PP 1,279.41. For this reason, the fully-fledged breakout most probably will be postponed until release of information on the American employment change and change in salaries. There is a need to take into account that on daily chart the pair has formed an ascending triangle pattern, which implies the further appreciation of the yellow metal against the buck.

USD/JPY Analysis: Anticipates US Employment Change Release

None of the yesterday's events created an impulse strong enough to force the pair to make a breakout from the rectangle pattern. Moreover, expectations of the upcoming release of information about the state of the American labour market led to formation of a minor symmetrical triangle pattern. A sharp plunge looks unlikely, as the southern side is reliably protected by a combination of the 100- and 200-hour SMAs together with the weekly PP at 113.79. On the other hand, a resistance area between the 114.25 and 114.35 levels managed to neutralize surge of the rate more than once in the past. Nevertheless, if the employment change appears to be really positive, traders with bullish outlook are likely to use this occasion to try to elevate the pair to the July 2017 maximum at 114.50.

GBP/USD Analysis: Sinks To 1.3040 Amid Interest Rate Hike

A decision to raise the interest rate led to 110 points fall of the rate. Initially, the bottom line of a dominant ascending channel managed to halt the pair near 1.3120. However, the subsequent Governor Carney press conference boosted this process and bears managed to push the pair to the weekly S1. On daily chart it seems that yesterday's downfall confirmed existence of a new medium-term descending channel. However, even in that case it looks like the Pound has to restore some lost positions before making a decisive breakout from the dominant ascending channel. An upcoming release of the British Services PMI might provide some small impulse for the upward movement. On the other hand, the two resistance levels near 1.3085 and 1.3107 most likely will manage to constrain the pair.