Sample Category Title

Currencies: Will Payrolls Be Strong Enough To Inspire Further USD Gains?

Sunrise Market Commentary

- Rates: Payrolls unable to give US Treasuries firm direction?

The outcome of the payrolls is highly uncertain. We see risks for a strong report. However, a Treasury sell-off won’t trigger a relevant break of key support. Similarly, key resistance looks to tough to break in case of a weak report. We envisage a sell-on-upticks in the latter case. - Currencies: Will payrolls be strong enough to inspire further USD gains?

Yesterday, the formal nomination of Jerome Powell as Fed Chairman and a proposal on US tax reforms were not able to give the dollar clear directional guidance. Today, the focus is on the US payrolls. We expect a strong report. A positive surprise in average hourly earnings is probably needed to support further USD gains

The Sunrise Headlines

- US equities ended the session nearly unchanged with the Dow outperforming after recouping early losses (on tax plan). Asian shares trade mixed with Japanese markets closed for a holiday. China underperforms.

- House Republican leaders rolled out their sweeping tax plan. The proposal cuts the corporate rate to 20%, reduces the number of individual brackets and eliminates the estate tax. It also halves the cap on the popular mortgage-interest deduction on new home sales and imposes a levy of up to 12% on offshore earnings. Trump said the bill will be law by Christmas.

- Brent headed for a fourth weekly gain, with the Saudi and Russian energy ministers possibly meeting in Uzbekistan to discuss oil-output cuts. Brent trades currently at $60.86/barrel.

- Venezuela is restructuring its global debt. President Maduro said PDVSA will make one last $1.1 billion payment before negotiating with banks and investors. Risk of contagion seems limited. Mexican peso was little changed in Asia.

- Apple forecasts record sales tied to robust demand for the iPhone X. It will help generate as much as $87 bn. in the Dec. quarter. Tim Cook said production which has had problems was "going well" and initial demand is strong."

- Mr.Powell pledged to pursue the Fed's goals of stable prices and maximum unemployment while keeping an eye on financial market risks. Trump officially named him to succeed Janet Yellen as Fed chairman.

- Chinese Caixin-Markit services PMI rose to 51.2 in October, up from 50.6 previously. New business growth was modest while business expectations picked up slightly.

- The market calendar will be dominated by the US payrolls. Minor items are the UK services PMI and speeches of ECB Nowotny & Coeuré and Fed Kashkari

Currencies: Will Payrolls Be Strong Enough To Inspire Further USD Gains?

Will payrolls trigger a new USD up-leg?

The dollar showed no clear trend yesterday. Markets awaited the nomination of the new Fed chairman and the tax proposal of the GOP. Equities and the dollar dropped temporary as the first details of the tax plan hit the screens, but the decline was soon reversed. US president Trump as expected appointed Jerome Powell as Fed Chairman. In the end, both factors had only limited impact on markets. The nomination of Powell was largely discounted. The tax proposals are still subject to amendments. EUR/USD finished the session at 1.1658 (from 1.1619). USD/JPY closed the session in well-known territory just north of 114.

Overnight, Asian equities show modest gains. Tech stocks are supported by strong earnings from Apple published after the WS close. Chinese equities underperformed even as the Caixin services PMI rose from 50.6 to 51.2. Chinese authorities consider tighter rules on foreign investments. USD/JPY is little changed in the 114 area in light trading conditions (Japanese markets are closed). EUR/USD holds a tight range in the 1.1650/70 area. Yesterday’s rebound of the Aussie dollar is aborted by poor Q3 retail sales. AUD/USD returned below the 0.77 handle.

Today, the October US payrolls will dominate trading. After a hurricane-distorted September report, a strong bounce is expected. Consensus expects net payrolls’ growth of 323K. We side with the consensus and expected a strong figure. The unemployment rate is expected stable at 4.2%. Average Hourly Earnings are probably the most important element of the report. A moderate 0.2% M/M gain is expected. That would slow the Y/Y advance to 2.7% from 2.9%. We see the risks on the upside. Other US eco data (trade deficit, ISM, factory orders) will be only of second tier importance.

The dollar was in better shape at the end of last week, but the rebound slowed this week. The publication of a tax proposal and the nomination of Powell as Fed Chairman were not able to break the stalemate. If the payrolls (especially AHE) are strong, the dollar might try a new up-leg. However, recent price action showed that there is little room for disappointment.

LT we maintain a EUR/USD sell-on-upticks bias. Of late, the dollar failed to gain against the euro despite widening interest rate differentials since early September. This trading dynamic was broken after the ECB decision last week. Policy divergence between the ECB and the Fed is again on the radar. However, any additional rate support for the dollar will probably be modest near term. So, further EUR/USD decline might develop gradually

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but there are no convincing follow-through gains yet. If the break is confirmed, it would signal that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY’s momentum was positive in September. The pair regained 110.67/95 resistance, a positive. The 114.49 correction top is the next resistance. Sentiment improved last week, but the first test on Friday failed. We don’t preposition for a sustained break higher.

EUR/USD broke below 1.1662 support, but breaks still needs to be confirmed

EUR/GBP

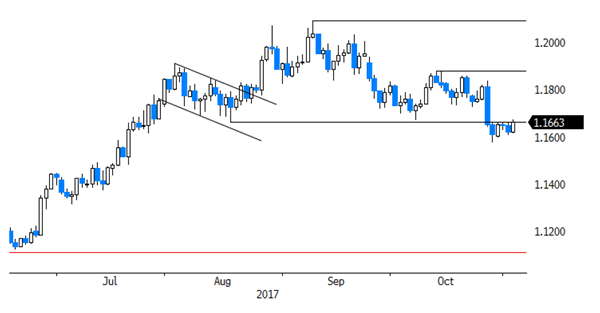

Sterling tumbles on soft BoE assessment

Yesterday, the BoE voted 7-2 to raise the base rate by 0.25 bp. However, the policy assessment was very dovish. The BOE assumes that inflation will return close to 2% by the end of the 3-year forecasting horizon. In order to meet the target, only two additional rate hikes are pencilled in. So, this scenario only sees very limited interest rate support for sterling medium term. EUR/GBP jumped from the low 0.88 area to 0.89 area and closed the session at 0.8927. Cable also fell off a cliff and finished the session at 1.3059 (from 1.3245).

Today, the UK services PMI will be published. A small decline from 53.6 to 53.2 is expected. This would confirm the picture that the UK economy has entered an era of lower growth. Markets will also monitor the consequences of the reshuffles within the UK government. More political instability will undermine confidence in the UK government and in sterling. In a day-to-day perspective, the decline of sterling might slow after yesterday’s sell-off. However, sterling remains vulnerable to negative eco and political news which is still highly likely to reoccur.

EUR/GBP staged a strong uptrend from April till late August with a top at 0.9307. Rising UK inflation and the BoE preparing markets for a rate hike caused a sterling rebound. This rebound did run into resistance. EUR/GBP tried to regain the 0.89/90 area, but there were no follow-through gains. EUR/GBP retested the 0.8743 support earlier this week, but rebound sharply yesterday. We maintain the view that the 0.8733 -0.8652 support area will be though to break in a sustainable way. A EUR/GBBOP buy-on-dips approach is favoured. 0.9023/33 is the first important resistance for the EUR/GBP cross rate

EUR/GBP: rebounds off 0.8733/43 support on soft BoE policy assessment

Forex: Sterling Falls On Rate Rise

In line with market expectations, the Bank of England raised the UK base rate to 0.5% (from 0.25%) on Thursday. The rise, the first in 10 years, was widely expected as the UK has seen inflation well above the Bank of England’s target rate of 2.0% (3.0% in September), with Governor Carney stating “The pace at which the economy can grow without generating inflationary pressures has fallen relative to pre-crisis norms. This reflects persistent weakness in productivity growth since the crisis and, more recently, the more limited availability of labour.” Whilst the rate hike was already “priced-in” by the markets, GBP suffered losses of 1.8% against EUR and 1.5% against USD following the announcement. Many attribute the downward pressure on GBP because of Governor Carney hinting that rates would rise twice more in the next 3 years, with rates edging up to 1% by the end of 2020. The future pace of rate rises is exceptionally slow and it is based on a relatively gloomy growth outlook which resulted in the markets selling GBP against its peers.

To no surprise, President Trump nominated Jerome Powell as the next Federal Reserve Chairman on Thursday at the White House. Trump stated: “He’s strong, he’s committed, he’s smart” and “I am confident that with Jay as a wise steward of the Federal Reserve, it will have the leadership it needs in the years to come.” The position requires Senate confirmation, but Mr. Powell is likely to get broad support from the Republican Senate majority. The Fed is expected to raise its benchmark interest rate again in December, likely Ms. Yellen’s final act as Fed Chair. Under Mr. Powell’s leadership, the Fed will likely continue its projected path of raising its interest rate 3 more times next year, as well as continuing to pare back its massive Fixed Income portfolio.

The markets are now focused on today’s Nonfarm Payrolls report for October, scheduled to be released at 12:30 GMT. Market expectations for a strong number were recently re-enforced with the ADP National Report showing the US private sector hired 235K workers in October, the most in 8 months.

EURUSD is little changed in early Friday trading at around 1.1665.

USDJPY is currently trading around 113.96.

GBPUSD, after a significant drop on Thursday, appears to be holding steady in early session trading at around 1.3075.

Gold is unchanged overnight, currently trading around $1,277.

WTI is 0.16% higher in early Friday trading at around $54.95.

Major data releases for today:

At 12:30 GMT, the US Department of Labor will release Nonfarm Payrolls for October. Market consensus is expected to show that the US economy added 310K jobs in October. In September, the economy shed jobs for the first time in 7 years, following disruptions from Hurricanes Harvey & Irma. NFP never fails to cause general market volatility, and this release will be no different, with expected volatility regardless of the number released.

At 12:30 GMT, US average hourly earnings (MoM & YoY) for October will be released. The annualized rate rose to 2.9% in September, demonstrating the fastest pace of growth in 8 years. This pace is expected to slow down to 2.7% year-on-year in October and 0.3% month-on-month from September’s 0.5%.

At 12:30 GMT, and to round off the set of impactful data releases from the US, will be US Unemployment rate. Forecasts are calling for the rate to remain unchanged at 4.2% – any deviation from expectation will cause a spike in USD volatility.

At 12:30 GMT, Statistics Canada is scheduled to release Unemployment rate and the Net Change in Employment for October. The Unemployment rate is expected to come in unchanged at 6.2%, with the net change forecast at 15K, an increase from the previous reading of 10K. Expect CAD volatility following the releases.

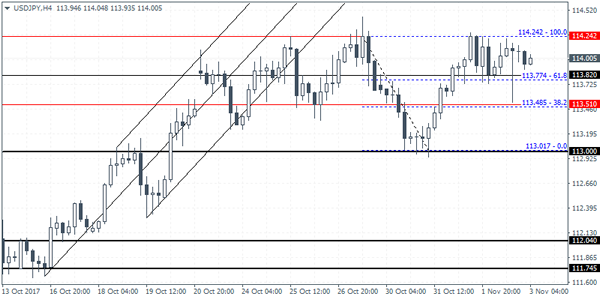

USDJPY Intraday Analysis

USDJPY (114.00): The USDJPY continues to trade near the major resistance level of 114.31 - 114.00 region. The sideways price action could signal a major breakout in the near term. On the 4-hour chart, we notice the inverse head and shoulders continuation pattern taking shape. Neckline resistance is formed at 114.24 which could be breached in the short term. This could put the upside bias in USDJPY towards 115.00 in the near term. However, failure to breakout above 114.24 resistance could mean that USDJPY will maintain the sideways range in the near term.

EURGBP Intraday Analysis

EURGBP (0.8920): The EURGBP posted a strong rebound yesterday as price rallied to a 4-day high. With price action breaking past the 0.8867 - 0.8850 minor resistance level we expect further upside gains to continue. In the near term, any declines are likely to be supported near 0.8867 - 0.8850 price level that could turn to support. In such a case, the next upside target in EURGBP will be near 0.9016 level which was previously tested. While the bias remains to the upside, EURGBP could be seen moving back into a range if price falls below 0.8850 support. This could keep the sideways price action intact and will see the EURGBP testing the lower support near 0.8778

EURUSD Intraday Analysis

EURUSD (1.1657): The consolidation in the EURUSD continues as price action remains trading flat below 1.1672. The euro was seen posting modest gains, but did not manage to make any significant progress. With price trading below the main resistance level of 1.1704 and 1.1672 we expect the bias to remain to the downside. On the 4-hour chart, the bearish flag pattern remains the main point of focus. Price action is expected to break down to the downside and will be validated on a close below the previous low of 1.1573. This will open the downside target in EURUSD towards 1.1411 eventually marking the completion of the bearish flag pattern. To the upside, a breakout above 1.1704 - 1.1672 could however signal a shift in the short-term direction.

Markets Turn To Payrolls Report Trump Nominates Powell

The Bank of England hiked interest rates in a widely expected move, raising the rates by 25 basis points. The BOE Governor advised that rate hikes will be gradual. Yesterday's rate hike was the first in a decade. The dovish forward guidance saw the British pound weakening strongly. GBPUSD fell 1.4% on the day while the EURGBP rose 1.8%. It was one of the strongest declines in the British pound in a year.

In the US President Trump officially nominated Fed member, Jerome Powell to be the next central bank chair. Powell was one of the main contenders for the post. However, markets view Powell as a cautious dove, but he is expected to continue to push ahead with the current monetary policy course.

Looking ahead the October payrolls report will be coming out today. According to the economists polled, the US economy is seen adding +300k jobs as normalcy returns. Revisions to September's payrolls data could also be weighing on investors as data showed a decline in jobs during the September month. The average hourly earnings are expected to rise 0.2% while the US unemployment is expected to remain steady at 4.2%.

Jobs Data Wraps Up Big Week For The US

- Jobs Report Eyed as Fed Gets New Chair;

- GBP Vulnerable Ahead of Services PMI Data.

It's been a very busy week for financial markets in which the Bank of England has raised rates for the first time in a decade, Donald Trump has elected a new Fed Chair and his long awaited tax reform has been unveiled, among many other things.

The US jobs report is widely regarded as the most important economic report each month and yet, in a week that's been packed full of other major announcements, it's not attracted the same kind of attention it usually would. Still, with the Fed now poised to raise interest rates again in December having passed up the opportunity to earlier this week, focus will be on the jobs data for signs of weakness.

As has been the case for quite a while now, the job creation and unemployment figures will likely draw the immediate attention of traders and could even trigger the early moves in markets, but it's the wages that will likely have a larger influence on Fed policy. An unusually large number of jobs is expected to have been created last month – 312,000 – which follows the decline the month before following the hurricanes in September. While this rebound in jobs will come as a relief, it's unlikely to trigger the same kind of move that it normally would in the absence of the previous month's decline.

The appointment of Jerome Powell to succeed Janet Yellen as Fed Chair is widely regarded as a continuity play by Trump, which means markets are still behind the curve when it comes to US rate hikes next year. With other spots on the Board of Governors still up for grabs, Trump's other appointments may offer more insight into the future direction of the Fed but this should give a good indication of the direction he's headed. With that in mind, wages should be important today as improvements here could offer the clearest indication that inflation will follow.

The European session will likely be a little quieter this morning, with the only notable data being the services PMI from the UK. The services sector is hugely important for the UK economy, accounting for more than three quarters of total output, which would explain why GDP has slowed in recent quarters in line with the decline in this figure despite other areas, such as manufacturing, having improved.

The pound may be vulnerable to further downside today in the event of a weaker reading, having fallen more than 1% following yesterday's rate hike. The increase itself was almost entirely priced in but traders were clearly not prepared for the dovish statement that accompanied it triggering some profit taking. A weaker PMI number today could see 1.30 come under pressure in GBPUSD.

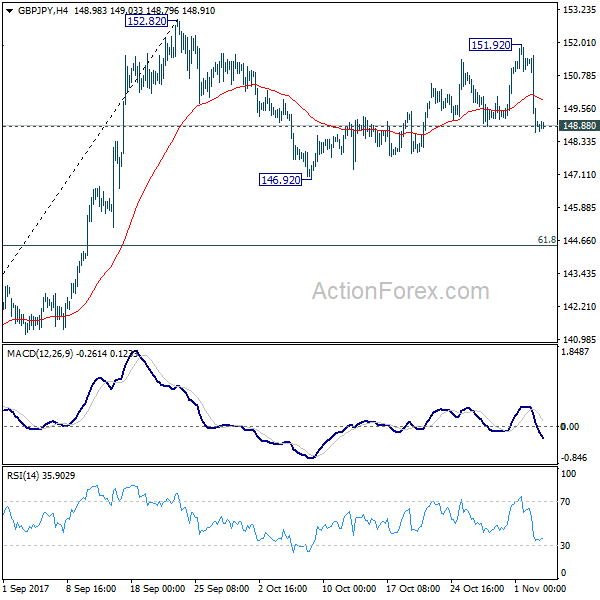

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.91; (P) 149.71; (R1) 150.76; More

The break of 148.88 minor support argues that choppy recovery from 146.92 has completed at 151.92 already. Intraday bias is turned back to the downside for 146.92 first. Break will resume the decline from 152.82. But at this point, we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, above 151.92 will retest 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.66; (P) 132.90; (R1) 133.24; More....

Intraday bias in EUR/JPY remains neutral for the moment.On the downside, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level. That will also complete and double top pattern (134.39, 134.48) and confirms near term reversal. 55 day EMA will also be firmly taken out. In that case, deeper decline should be seen back to 127.55 key support. On the upside, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

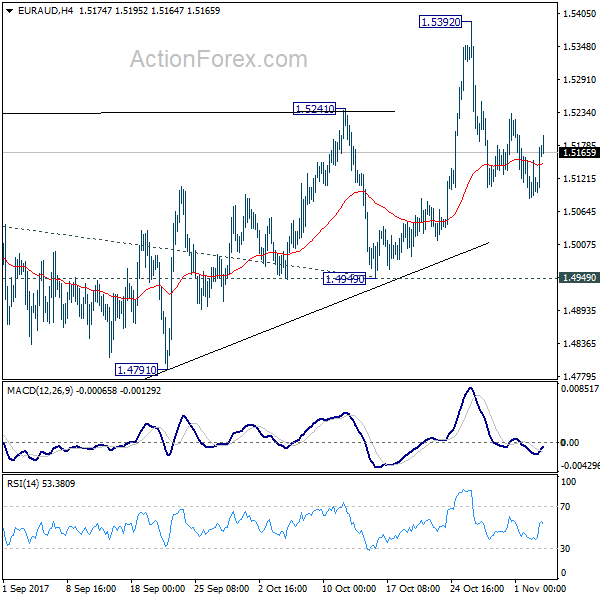

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5081; (P) 1.5117; (R1) 1.5148; More....

EUR/AUD is staying in consolidation from 1.5392 and outlook is unchanged. As long as 1.4949 support holds, outlook remains bullish. Medium term rally from 1.3624 is in favor to continue. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.