Sample Category Title

Trade Idea Wrap-up: EUR/USD – Sell at 1.1705

EUR/USD - 1.1672

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1643

Kijun-Sen level : 1.1639

Ichimoku cloud top : 1.1643

Ichimoku cloud bottom : 1.1643

Original strategy :

Sell at 1.1705, Target: 1.1605, Stop: 1.1740

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1705, Target: 1.1605, Stop: 1.1740

Position : -

Target : -

Stop : -

Euro’s intra-day rebound has retained our view that near term sideways trading is likely to continue and although initial upside risk remains for the rebound from 1.1574 low to extend marginal gain from here, as this move is still viewed as retracement of recent decline, reckon upside would be limited to 1.1700-05 (50% Fibonacci retracement of 1.1837-1.1574) and bring retreat later, below 1.1600-05 would signal the rebound from 1.1574 low has ended, bring retest of this level first. A drop below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold.

In view of this, we are looking to sell euro on further subsequent recovery as 1.1700-05 should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

BoE Keeps its Flexibility on Further Rate Hikes Next Year

Bank of England did not comment on rate path

As expected, the Bank of England (BoE) raised the Bank Rate by 25bp from 0.25% to 0.50% with the vote count 7-2 (Sir David Ramsden and Sir Jon Cunliffe dissented) in line with our expectation but against the consensus view of a 6-3 vote count. It is likely this explains why EUR/GBP moved lower initially. However, UK yields declined 6-9bp across the 2-10Y curve and EUR/GBP ended higher, as the Bank of England did not comment on current market pricing (two hikes over three years, this is also what the BoE's projections are based on), meaning the BoE keeps its flexibility. In addition, the BoE said it will 'monitor closely' incoming data 'including the impact of today's increase in Bank Rate'. During the press conference, Mark Carney said the rate hike is just a 'small adjustment' and that the BoE has 'stretched the horizon of which CPI inflation should return to 2% target due to unusual circumstances' (Brexit). Still, Carney noted that inflation is expected to remain slightly above 2% even assuming the two hikes over three years currently priced in the market. Overall, the signal is neutral, which was more dovish than the market had expected, in line with our expectation. Another important thing is that the BoE says that potential growth is 1.5% y/y, so as long as GDP grows by above 0.3% q/q, then the economy will continue running hotter.

We still believe the BoE will stay on hold next year and not hike again before 2019, so this is more about taking back the emergency cut from August 2016 just after the Brexit vote. We think it is likely the BoE is too optimistic on wage growth and we believe the BoE does not want to tighten monetary policy too much relative to the ECB. The ECB has just extended QE by nine months, meaning it is unlikely to raise rates before 2019. Markets currently price in a Fed-like hiking cycle with one hike a year.

Relative rates, growth and Brexit uncertainty set to support EUR/GBP near term

EUR/GBP increased following the rate hike announcement in line with our expectation as the BoE refrained from commenting on future rate hikes. With the next rate hike priced by November 2018, we see market pricing as slightly on the hawkish side in the sense that it is more likely that rate hike expectations for 2018 will be lowered in coming months than that more rate hikes in 2018 are priced in. Overall, we still expect EUR/GBP to trade within the 0.8650-0.9000 range in coming months, with Brexit uncertainty remaining a source of volatility. In the near term, we expect relative rates, growth and Brexit uncertainty to be EUR/GBP positive and we still expect the cross to test the high end of the range.

Longer term, Brexit negotiations remain the key determinant for GBP and we still see potential for a further decline in EUR/GBP driven by possible clarification on Brexit negotiations and valuations. However, with the ECB moving towards an exit as well and as relative growth is set to remain EUR/GBP positive, we see only modest downside potential in the year ahead. We target 0.87 in 6M and 0.86 in 12M.

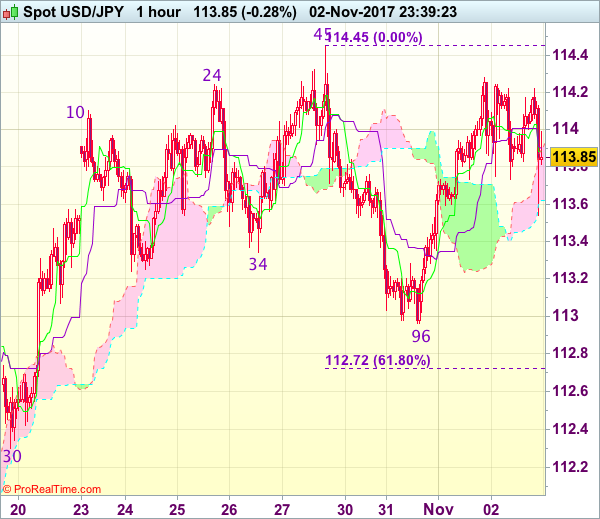

Trade Idea Wrap-up: USD/JPY – Buy at 113.20

USD/JPY - 113.84

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.98

Kijun-Sen level : 114.01

Ichimoku cloud top : 113.61

Ichimoku cloud bottom : 113.45

Original strategy :

Buy at 113.40, Target: 114.30, Stop: 113.05

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.20, Target: 114.20, Stop: 112.85

Position : -

Target : -

Stop : -

As the greenback has retreated after rising to 114.28 yesterday, suggesting consolidation below said resistance would take place and pullback to 113.60 cannot be ruled out, however, reckon downside would be limited to 113.40 and bring another rise later towards indicated strong resistance at 114.45-50 but break there is needed to retain bullishness and confirm early upmove has resumed for headway to 114.75-80 and later towards 115.00 but near term overbought condition should limit upside.

In view of this, we are looking to buy dollar on pullback as 113.15-20 should limit downside and bring another rise later. Below said support at 112.96 would abort and suggest top has been formed at 114.45, bring retracement of recent rise to 112.70-75 (61.8% Fibonacci retracement of 111.65 to 114.45) but previous resistance at 112.48 should hold.

The Bank of England Lowers Economic Forecast

The EUR/USD price keeps consolidating despite yesterday's publication of the FOMC statement on monetary policy where it was noted that the regulator plans to increase interest rates one more time during this year and three more times in 2018. At the same time, the news of Donald Trump nominating Jerome Powell to the Fed's chair position should stimulate the hawkish sentiment on the market. The greenback was supported by news on the decline in the initial jobless claims in the US to 229,000 from the expected 235,000 thousand. Traders are waiting for tomorrow's release of labor market data. The NFP report is expected at 12:30 GMT to come in at 312,000 so an improvement on that number is likely to lead to a price decline of the EUR/USD.

The British pound has shown a sharp decline after the Bank of England increased the interest rate by 0.25% to 0.50% and lowered the economic outlook of the UK economy. GDP is now growing at 1.5% compared to 1.75% in August. The economic growth in 2018 is forecasted at 1.7% compared to 1.8% anticipated earlier. The GBP/USD remains under pressure thanks to negative sentiment around the influence of Brexit on the state of the national economy.

The aussie price resumed positive dynamics after the recent correction. Optimistic sentiment has strengthened on the background of positive statistics on the trade balance, which showed the surplus increased to 1.75 billion compared to 1.42 billion expected. Tomorrow traders will be on the watch for the retail sales report in Australia due at 00:30 GMT.

EUR/USD

The EUR/USD price continued growing after touching the SMA100 on the 15-minute chart. In case of further growth, the price may return to the important 1.1700 line. The signal to sell may come from breaking through the local minimum near 1.1600. In this case the next targets will be at 1.1500 and 1.1450.

GBP/USD

The GBP/USD price has shown a sharp decline after it was not able to gain a foothold above 1.3250. The target range in case of further decline will be 1.3000-1.3050. The RSI on the 15-minute chart is in the oversold zone which may trigger a price rebound with potential target at 1.3150.

AUD/USD

The AUD/USD was not able to reach the SMA on the 15-minute chart and resumed positive dynamics. Growth may continue the positive dynamics along the inclined resistance line and in case of breaking through 0.7740, the immediate objectives will be at 0.7800 and 0.7900. Strong support at 0.7635 is likely to restrain negative dynamics.

Yen Gains Ground Ahead of Fed Chair Nomination

USD/JPY has posted losses in the Thursday session, erasing the gains seen on Wednesday. In North American trade, USD/JPY is trading at 113.96, down 0.27% on the day. On the release front, Japanese Consumer Confidence improved to 44.5, beating the estimate of 43.6 points. In the US, today's highlight was unemployment claims, which dropped to 229 thousand. This beat the estimate of 235 thousand. The focus will be on employment numbers on Friday, as the US releases Average Hourly Earnings, Nonfarm Payrolls and the unemployment rate. We'll also get a look at ISM Nonfarm Manufacturing PMI.

The Federal Reserve rate statement was expected to be little more than a run-up to the December rate decision, and indeed there were no surprises from Janet Yellen and Co. The Fed indicated that a rate increase is very likely at the December meeting, and was careful not to change any of the wording in its statement regarding future rate hikes. The rate statement noted that hurricanes which hit the US had caused a decline in payrolls in September, but the Fed did not expect the hurricanes to "materially alter the course of the national economy over the medium term." The markets are expecting a strong rebound in nonfarm payrolls – the forecast for Friday's US nonfarm payrolls is a robust 311 thousand, after a decline of 33 thousand in September. Still, wage growth, which was remained soft despite the strong economy, is expected to slow to 0.2 percent, as inflation remains the Achilles heel of a robust US economy.

With fed futures prices in at 96 percent, a December rate hike from the Fed appears a done deal. What can we expect in 2018? This will depend to a large degree on the new chair of the Fed, who will take over from Janet Yellen in February. Janet Yellen will wind up her 3-year term in February, and she is not expected to be reappointed by President Trump. The front runner is economist Jerome Powell, who is expected to maintain the Fed's current policy of small, incremental rates. Trump is expected to make his choice later on Thursday, and the markets could react once the new Fed chair is announced.

BoE Hikes, But Sterling Tumbles on Soft BoE Assessment

- European equities traded down today, but are off the intra-day lows, showing currently losses of 0.30%. US equities show marginal losses, as the initial dive on the tax reform headlines is reversed.

- Republicans unveiled plans to slash the corporate tax rate to 20%, without cutting the top rate for the richest Americans as part of a sweeping overhaul of the tax code as they seek to secure a first major legislative victory for President Donald Trump

- Traders are painting the Bank of England's tightening cycle with the 'one and done' brush after the central bank finally raised overnight borrowing costs for the first time in more than a decade. UK gilts prices rallied sharply. The decline in yields means the policy sensitive two-year gilt yield is drifting below the new base rate of 0.5%.

- The BoE warned Brexit was having a "noticeable impact" on the UK's economic outlook in its monetary policy release earlier this afternoon, as it increased interest rates for the first time in a decade, with "considerable risks" for how households, businesses and financial markets respond to Britain's withdrawal from the trading bloc

- Germany's labour market continued tightening in October, leaving the country's jobless rate (5.6%) at the lowest level since its reunification in 1991. The number of unemployed Germans decreased by 11,000, a decline of 1,000 more than economists had forecast.

Rates

UK gilts only game in bond markets today.

Global core bonds had a sideways oriented session in the absence of new valuable information and ahead of tomorrow's US payrolls that kept many investors sidelined. During the European session, the EMU PMI business sentiment for October was nearly unchanged compared to the preliminary figures and German unemployment fell further, but did so in line with expectations. During the US session, initial claims were somewhat lower than expected and productivity somewhat higher, but they were as often ignored. At the time of closure of our report, some headlines on the tax plan roll over the screens. In an initial reaction, US Treasuries go marginally higher, but have ceded in the meantime part of the "minimal" gains. At the time of writing, changes on the German yield curve are insignificant range (0-0.6 bp). The US yield curve flattens somewhat further with yield declines varying between 1.2 bp (2-yr) and 2.9 bps (10-30-yr).

The calmness in the core bond markets wasn't duplicated in the UK bond space. The BoE meeting triggered a large decline of UK yields across the curve. The BoE, as expected, raised the bank rate by 25 bps to 0.50%, the first rate hike in more than 10 years. However, more importantly for markets, it was likely the most dovish hike that was delivered by the BoE. Indeed, the statement no longer said that rates might have to rise faster than markets discount. This means that in the next 2-3 years rates are expected to be increased only 2 times to bring the bank rate in 2020 at 1%. The statement also said that the next rate hike is not imminent and few hikes are enough to bring inflation close to the objective in a 3-yr horizon.

On intra-EMU bond markets, 10-yr yield spreads versus Germany are little changed with Greece again the noticeable exception, as it still profits from rumours about a big rate swap that should enhance liquidity (-20 bps).

Currencies

USD awaits new Fed-chair, tax bill and payrolls

Today, the dollar showed no clear trend. The EMU and US eco data were OK but hardly affected FX trading. Markets awaited to nomination of the new Fed-chairman and were looking for concrete details on the US tax reform bill. EUR/USD hovered in the mid 1.16 area. USD/JPY tried to regain the 114 area. Even so, the dollar hardly profited from the Fed keeping the door open for a December rate hike.

Overnight, Asian equities outside Japan trade with modest losses. The US equity rally showed some signs of fatigue. This weighed on Asian indices and on US yields. It prevented the dollar to return to the recent highs against the euro and yen. USD/JPY returned below the 114 handle, while EUR/USD traded again in the mid 1.16 area.

The EMU Manufacturing PMI was revised marginally lower from 58.6 to 58.5. Even so, the report still indicates above-trend EMU growth at the start of the fourth quarter. German unemployment data gave a similar signal. As usual the data had no impact on the euro. In technical trading, EUR/USD hovered up and down around the 1.1650 pivot. USD/JPY struggled to regain the 114 barrier. Yesterday's Fed statement kept the door open for a December rate hike. However, it didn't changed the USD trading dynamics today.

The early morning US data didn't bring any high profile news. Jobless claims declined slightly more than expected to 229K (from 234K). Q3 productivity (3.0%) and unit labour costs (0.5%) were slightly higher than expected. The impact on the dollar remained very limited. At the time of writing, the first fragmented details of the GOP tax plan are rolling on the screens. (FX) markets are not impressed. US bond yields, the dollar and US equities are all ceding modest ground. EUR/USD trades in the 1.1675 area. USD/JPY trades around 113.65.

BoE hikes, but sterling tumbles on soft BoE assessment

Over the previous days, sterling had a strong run as investors didn't want to be positioned short sterling in the run-up to the first BoE rate hike in more than 10 year. However, the sterling rally slowed in the run-up to the BoE decision this morning. The BoE voted 7-2 to raise the base rate by 0.25% to 0.50%. However, the policy assessment was very dovish. The BOE assumes that inflation will return close to the 2% policy horizon by the end of the 3-year forecasting horizon. In order to meet the target, the BOE assumes that only two additional rate hikes are needed till the end of 2020. Of course, several risk factors can change the main BoE scenario, but the main scenario only sees very limited interest rate support for sterling in the short-to-medium term. UK yields nosedived and sterling was heavily sold upon the BoE policy announcement. EUR/GBP jumped from the low 0.88 area and filled offers in the 0.89 area. Cable fell off a cliff. The pair trades currently in the low 1.31 area. The BoE continues to give more weight to supporting growth in times of (Brexit-related) uncertainty rather than to reducing inflation when setting its policy balance. This is a structural negative for sterling.

Bank of England Raises Interest Rates for the First Time in Over a Decade

As widely anticipated and well communicated in advance, the Bank of England's Monetary Policy Committee (MPC) raised its policy rate by 25 basis points to 0.5%. The decision was well supported by the MPC, with a majority voting in favour (7-2).

This is the first increase in the Bank's key policy rate since July 2007. But, back then the economy was growing at a 2.5% annualized pace, and the policy rate was set at 5.75%, or 525 basis points higher than the current policy rate. In addition, the MPC voted unanimously to maintain their stock of corporate and UK government bond purchases at £10 billion and £435 billion, respectively.

The MPC made it clear that the decision to tighten was due to the shift in the balance of risks around inflation to the upside. Bank of England Staff projections anticipate that headline inflation will peak at just above 3.0% y/y in October, which is just above the operational target range of 1 to 3%. Inflation has been running at the upper end of the range since this past Spring, driven by the pass-through to consumer prices from the post-Brexit referendum depreciation in the exchange rate and a steady move higher in energy. Today's move is widely viewed by the MPC as necessary to ensure that inflation moves sustainably back down within the target range.

Financial market reaction to the announcement was dovish, sending the pound down by about 1% versus the U.S. dollar in the aftermath of the decision. UK government bonds were bid, with the 10-yr UK government bonds yield falling by over 6 basis points to 1.28.

In the Inflation Report, projections for economic growth have been revised up on a Q4/Q4 basis for 2017 to 1.5% from 1.3%, revised down for 2018 to 1.7% from 1.8%, and unchanged in 2019 at 1.7%. Similarly, the inflation outlook was revised up for 2017 to 3.0% from 2.8%, and revised down slightly in 2018 to 2.4% from 2.5%; the outlook for 2019 was unchanged at 2.2%. The unemployment rate is now expected to hold at 4.2% through 2019, down from the 4.5% level in the August projection. This is consistent with the Bank's view that tightening labour market will help support wage growth, but low productivity growth will prevent nominal wages from rising persistently above 4.0% as was typical in the pre-2007 era. Low productivity growth is a phenomenon that has been plaguing other advanced economies as well, often being singled out as one of the key reasons as to why wage growth has remained so weak in the past decade despite unemployment rates falling to historic lows.

With today's decision, the Bank of England joins two of its G7 peers, the Bank of Canada and the U.S. Federal Reserve, in raising its key monetary policy interest rate this year. However, the Bank of England is in the unique situation of raising rates to ensure inflation moves back down to within its target band, while both the Bank of Canada and the U.S. Federal Reserve raised interest rates to head off what they believe to be rising wage and price pressures that will help move inflation up toward target in coming quarters.

Carney on the Defensive, Tax Reform and Fed Chair Announcement to Come

The controversial decision to raise interest rates at a time of significant economic uncertainty unsurprisingly left Mark Carney on the defensive throughout his press conference on Thursday, as reporters repeatedly questioned why the central bank decided it was the appropriate time for the first rate hike in a decade.

Naturally the decision on whether the raise interest rates is far from straightforward with inflation significantly overshooting the central bank's 2% target and the labour market in good shape, while at the same time the economic outlook is uncertain at best and real incomes are already being squeezed. While the MPC has been divided on the correct course of action in recent months, the pendulum eventually swung in favour of the hawks with some policy makers clearly of the belief that they had reached the limitations of how much inflation they could stomach.

As can be interpreted from the market reaction though, the rate hike came with quite a dovish twist. Policy makers refrained from including language in the statement that suggest markets were behind the curve on rate hikes which would indicate that two over the next three years is expected, which would represent an extremely gradual tightening process. Given the assumptions that the central bank has on labour market slack and the relationship with wages and inflation, it's possible that even two hikes may be a little punchy. The experience of the Fed would certainly support this view.

All things considered, the view appears to be that the BoE has taken a risky and unnecessarily step in raising interest rates today, one they may regret and be forced to reverse over the next year or so. Even if this is avoided, with the rate now back at the level the central bank deemed the lower bound for seven years prior to the Brexit referendum, we may be waiting some time for interest rates to rise again.

The BoE's job may be done for the day but the fun may be just beginning for markets, with details of Trump's tax reforms and the new Fed Chair announcement still to come. Jerome Powell is expected to be announced as Janet Yellen's successor late on in the session which will leave another seat available on the Board of Governors for Trump to fill. Certain candidates may have missed out on the position of Chair but with other important roles to be filled, there's potential for them to join Powell at the top.

Tax reform and the future leadership of the Fed have both been very important factors in the dollar revival over the last couple of months so it will be interesting to see how the greenback responds to both of these events today.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8893

Original strategy :

Sold at 0.8850, Target: 0.8735, Stop: 0.8890

Position : - Short at 0.8850

Target : - 0.8735

Stop : - 0.8890

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Current much stronger-than-expected rebound has dampened our bearishness and signals the fall from 0.9033 has ended at 0.8733 yesterday, hence upside risk remains for further gain to 0.8925-30, then test of resistance at 0.8957, however, break of 0.8976 resistance is needed to add credence to this view, bring further gain to 0.9000, then retest of 0.9033 later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. On the downside, expect pullback to be limited to 0.8870 and reckon 0.8830-35 would hold, bring another rise later. Below 0.8830-35 would risk weakness to 0.8800 but only break of 0.8765-70 would abort and signal the rebound from 0.8733 has ended instead.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Buy at 1.2755

USD/CAD - 1.2816

Trend: Near term up

Original strategy :

Buy at 1.2755, Target: 1.2955, Stop: 1.2695

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2705, Target: 1.2905, Stop: 1.2645

Position: -

Target: -

Stop:-

As the greenback has retreated after faltering below resistance at 1.2917, suggesting consolidation below this level would be seen and pullback to 1.2750 cannot be ruled out, however, reckon downside would be limited to 1.2700-05 and bring another rise later, above said resistance at 1.2917 would signal the rise from 1.2061 low is still in progress and extend gain to 1.2950, having said that, as we are still treating this rebound from 1.2061 as wave iv, reckon 1.2975-80 (61.8% Fibonacci retracement of wave iii) would limit upside and 1.3000 should hold, bring selloff later in wave v. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

In view of this, we are looking to reinstate long on subsequent pullback as 1.2700-05 should limit downside and bring another rise. Below 1.2670-75 would defer and suggest a temporary top is possibly formed, bring correction to 1.26350-40 but break there is needed to confirm, bring weakness to 1.2610-15, then test of 1.2591.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.