Sample Category Title

Eurozone Economic Confidence Soared To Almost 17-Year High Level In October

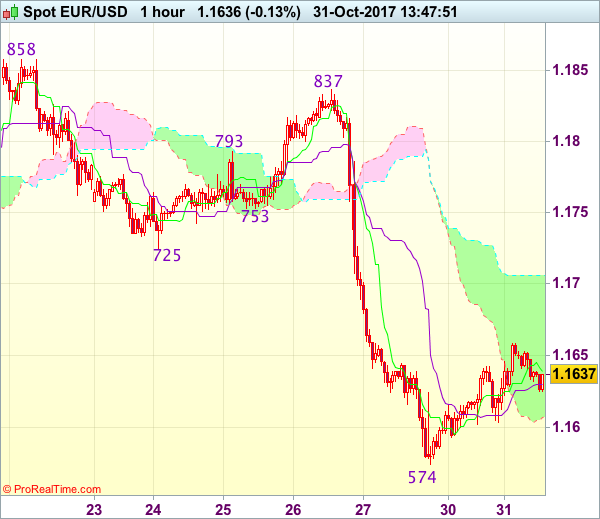

For the 24 hours to 23:00 GMT, the EUR rose 0.30% against the USD and closed at 1.1644, following better than expected Eurozone data.

On the macro front, economic confidence across the Eurozone climbed to its highest level since January 2001 in October, as it rose to 114.0 from a revised level of 113.1 reported in the previous month, suggesting that the region has shown some solid economic recovery following a decade-long economic and financial crisis. Markets had envisaged the economic confidence index to advance to 113.3. Moreover, the region’s business climate index rose more than expected to 1.44 in October, from 1.34 in September, registering its highest level since March 2011. Meanwhile, Eurozone’s final consumer confidence index advanced to -1.0 in October, in line with market expectations. In the previous month, the consumer confidence index had recorded a level of -1.2. The preliminary figures had also indicated an advance to -1.0.

In Germany, the powerhouse economy of the Eurozone, retail sales rebounded by 0.5% on a monthly basis in September, matching the forecast. Retail sales had fallen by a revised 0.2% in the previous month. Separately, Germany’s inflation eased more than expected to 1.6% YoY in October, following a rate of 1.8% in September.

In the US, consumer spending recorded a rise of 1.0% in September, more than market expectations for an advance of 0.9%. In the prior month, personal spending had risen 0.1%. Also, US personal income rose 0.4% in September, in line with market estimates. Additionally, the Dallas Fed manufacturing business index unexpectedly climbed to a level of 27.6, compared to a level of 21.3 in the prior month. Markets were anticipating the Dallas Fed manufacturing business index to ease to 21.0.

Meanwhile, a report stated that US President, Donald Trump, is likely to pick Federal Reserve (Fed) Governor, Jerome Powell, as the next Chair of the US Fed and an announcement about the same would be made by Trump on Thursday.

In the Asian session, at GMT0400, the pair is trading at 1.1635, with the EUR trading 0.08% lower from yesterday’s close.

The pair is expected to find support at 1.1605, and a fall through could take it to the next support level of 1.1576. The pair is expected to find its first resistance at 1.1661, and a rise through could take it to the next resistance level of 1.1688.

Moving ahead, traders will closely asses the Eurozone GDP data for the third quarter along with the region’s consumer prices for October, both due to release today. Additionally, in the US, the consumer confidence index and Chicago PMI data, both for October, along with the home price index for August, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

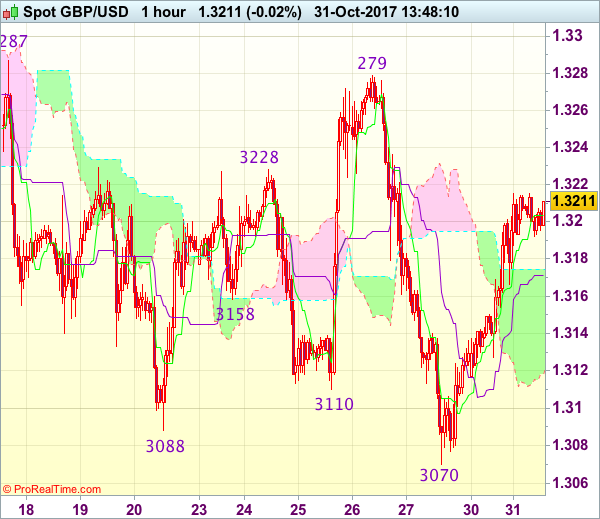

UK’s Consumer Confidence Slipped In October

For the 24 hours to 23:00 GMT, the GBP rose 0.52% against the USD and closed at 1.3206.

Macroeconomic data showed that the number of mortgage approvals for house purchases fell less than anticipated to a level of 66.2K in September in the UK, compared to a fall to 66.0K expected by market players. Number of mortgage approvals had recorded a revised reading of 67.2K in the previous month.

Moreover, UK net consumer credit advanced more than expected by £1.6 billion in September, compared to a revised advance of £1.8 billion in the prior month.

Overnight data disclosed that Britain's consumer confidence index eased to a level of -10.0 in October from a reading of -9.0 in the previous month, indicating that consumers remained downbeat about the economy amid ongoing Brexit talks. Market expectations was for the index to fell to -10.0.

In the Asian session, at GMT0400, the pair is trading at 1.3204, with the GBP trading marginally lower from yesterday's close.

The pair is expected to find support at 1.3149, and a fall through could take it to the next support level of 1.3093. The pair is expected to find its first resistance at 1.3238, and a rise through could take it to the next resistance level of 1.3271.

With no major economic release in the UK today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoJ Kept Its Monetary Policy Steady, Cuts Inflation Outlook

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the JPY and closed at 113.13.

In the Asian session, at GMT0400, the pair is trading at 113.16, with the USD trading marginally higher from yesterday’s close.

The Bank of Japan (BoJ), at its latest monetary policy meeting, left its short-term interest rate unchanged at -0.1% by a majority vote of 8-1 and held its asset purchases at an annual pace of ¥80.0 trillion, as expected. In its outlook report, the central bank maintained its forecast for inflation to hit 2.0% in the fiscal year 2019/2020. However, it trimmed its projections for core consumer prices for the fiscal year 2017/2018. The CPI is now expected to rise 0.8% in the current fiscal year, down from the previous projection of 1.1%. BoJ’s new board member, Goushi Kataoka, who dissented from the BoJ’s decision to maintain its interest rate targets, argued that the central bank should signal its willingness to increase stimulus if there is a delay in achieving the 2.0% inflation target.

The pair is expected to find support at 112.84, and a fall through could take it to the next support level of 112.52. The pair is expected to find its first resistance at 113.62, and a rise through could take it to the next resistance level of 114.08.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

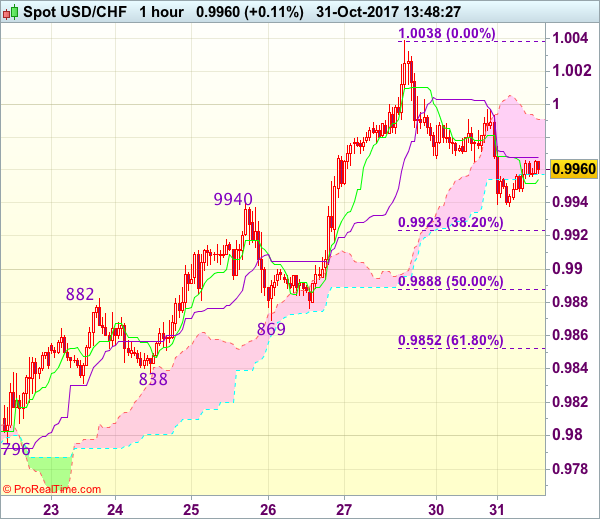

Switzerland’s KOF Leading Indicator Reached Its Highest Level Since September 2010

For the 24 hours to 23:00 GMT, the USD declined 0.19% against the CHF and closed at 0.9956.

In economic news, Swiss KOF leading indicator rose to 109.1 in October, hitting its highest level since September 2010, from a revised level of 106.1 in the prior month. Market expectation was for the KOF leading economic barometer to climb to 106.5.

Meanwhile, data showed that Switzerland's total sight deposits slipped to a level of CHF578.5 billion in the week ended 27 October, from a level of CHF578.6 billion reported in the prior week.

In the Asian session, at GMT0400, the pair is trading at 0.9959, with the USD trading a tad higher from yesterday's close.

The pair is expected to find support at 0.9933, and a fall through could take it to the next support level of 0.9907. The pair is expected to find its first resistance at 0.9991, and a rise through could take it to the next resistance level of 1.0023.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Lower This Morning Ahead Of Canada’s GDP Data And BoC Governor Poloz’s Speech

For the 24 hours to 23:00 GMT, the USD marginally rose against the CAD and closed at 1.2831.

In the Asian session, at GMT0400, the pair is trading at 1.2841, with the USD trading 0.08% higher from yesterday's close.

The pair is expected to find support at 1.2815, and a fall through could take it to the next support level of 1.2789. The pair is expected to find its first resistance at 1.2864, and a rise through could take it to the next resistance level of 1.2887.

Later in the day, all eyes would be on Canada's economic growth data for August and a speech by the Governor of the Bank of Canada (BoC), Stephen Poloz.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Market Update – Asian Session: China PMI Declines, Sending Yields Lower

Asia Summary

Asian equity markets have opened generally lower, following the mixed trading session in the US.

In the tech sector, chip giant, Samsung Electronics has gained over 1%. The company confirmed its Q3 results, announced a plan to increase capital returns to shareholders and said it plans to raise its FY17 Capex by over 80% y/y. Softbank has declined by over 5%, following the speculation that the merger between Sprint and T-Mobile could be canceled. Shares of Nintendo have risen by over 6%, as the company raised its FY forecast on demand for its Switch device.

South Korean advertising firm Cheil Worldwide has gained over 9%, as the company reported better than expected Q3 results. Shares of Lotte Shopping and Lotte Tour have outperformed. Earlier today, South Korea and China agreed to work toward improving bilateral relations.

Fast Retailing has declined by over 0.4% amid the earlier weakness seen in the S&P 500’s Consumer Discretionary sector. Australian Retailer Woolworth’s has gained over 1.5%, as Q3 revenues rose by over 3%.

Steel makers are currently trading mixed. Kobe Steel has gained over 1%, after reporting its financial results. At the same time, Nippon Steel and South Korea’s Posco have declined by over 1%. In Oct, China’s Steel PMI declined, according to an industry association.

The auto sector in Japan has traded generally lower. On Wednesday (Nov 1st), Honda is expected to release its financial results.

Japanese mega banks have added on to the losses seen in the prior session. In the brokerage space, Nomura has declined by over 2% after the company reported a decline in its quarterly profits. There has also been some weakness in the banking sector in China/Hong Kong. Shares of the Bank of China have declined by over 3%, after the company reported flat Q3 profits. China Communications Construction has dropped over 2% following its 9-month results. In the mining sector, Glencore said it would move to have its Hong Kong listing withdrawn in 2018.

Meanwhile, China’s Oct official manufacturing and non-manufacturing PMIs each declined from the prior month. The country’s sovereign 10-year bond yield has declined for the first time in 5 sessions, after yields moved to the highest level since late 2014 during the prior session.

In terms of the Chinese shorter-term rates, there has been speculation that the PBoC could announce a medium-term lending facility (MLF) by as soon as Friday. Liquidity conditions in China may tighten in the near term with around CNY1T in funds expected to mature this week, says the China Securities Journal.

In Japan, as speculated the BoJ left policy unchanged and lowered its inflation forecasts. Once again at today’s policy meeting, official Kataoka was the dovish dissenter on the belief that the central bank’s policy should target the 15-year JGB yield as opposed to the 10-year yield, which is currently the focus.

There has been little initial impact on the Yen following the policy decision. In New Zealand, the Kiwi has declined by over 0.4%, as PM Ardern confirmed plans to crack down on foreign purchases of residential properties. On tomorrow’s session, New Zealand’s Q3 employment figures are expected to be released. Ardern has previously said the incoming government plans to review the RBNZ’s mandate to see whether it should cover employment

Japanese companies expected to report results later today include, Asahi Glass, Daiichi Sankyo, FUJIFILM, Japan Airlines, JTEKT, JVC Kenwood, Mitsubishi Heavy, NEC Corp, NGK Insulators, Nippon Express, Nitto Denko, Oki Electric Industry, Omron, Panasonic, Sony, Sumitomo Heavy and TEPCO.

Key economic data

(JP) BANK OF JAPAN (BOJ) LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10%; AS EXPECTED

(NZ) NEW ZEALAND SEPT BUILDING PERMITS M/M: -2.3% V +5.9% PRIOR (1st decline in 5-months)

(CN) CHINA OCT OFFICIAL GOVT MANUFACTURING PMI: 51.6 V 52.0E

(KR) South Korea Sept Cyclical Leading Index Change: -0.2 v 0.1 prior

(KR) SOUTH KOREA SEPT INDUSTRIAL PRODUCTION M/M: 0.1% V 2.2%E; Y/Y: 8.8% V 4.8%E

(JP) JAPAN SEPT OVERALL HOUSEHOLD SPENDING: -0.3% V 0.6%E

(JP) JAPAN SEPT PRELIM INDUSTRIAL PRODUCTION M/M: -1.1% V -1.6%E; Y/Y: 2.5% V 2.0%E

(NZ) New Zealand Oct ANZ Business Confidence: -10.1 v 0.0 prior; Activity Outlook: 22.2 v 29.6 prior

(AU) Australia Sept HIA New Home Sales m/m: -6.1% v 9.1% prior

(AU) AUSTRALIA SEPT PRIVATE SECTOR CREDIT M/M: 0.3% V 0.5%E; Y/Y: 5.4% V 5.6%E

Speakers and Press

Japan

(JP) Japan said to set FY18 budget at ~¥98T v ¥97.5T set in FY17 - Nikkei

Korea

(KR) South Korea Ministry of Foreign Affairs: South Korea and China agreed to restore their bilateral relations to a "normal development path swiftly" as stronger ties meet their mutual interests

China/Hong Kong

(CN) Former China SAFE (FX regulator) official sees stronger US dollar putting pressure on the yuan – China Securities Times

(CN) PBoC said to check bank demand for medium-term lending facility (MLF) loans, with possible operations on Friday - financial press

(CN) China liquidity conditions expected to tighten with ~CNY1T in funds are due to mature this week - China Securities Journal

Australia/New Zealand

(NZ) New Zealand PM Ardern: To amend law to classify residential homes as sensitive which means non-residents can't buy existing homes; expects law to be introduced before Christmas

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng -0.2%; Shanghai Composite -0.3%; ASX200 +0.0%, Kospi +0.6%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax closed for holiday; FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1653-1.1632; JPY 113.28-112.98; AUD 0.7699-0.7672;NZD 0.6882-0.6838

Dec Gold -0.1% at $1,276/oz; Nov Crude Oil -0.2% at $54.05/brl; Dec Copper -0.1% at $3.11/lb

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6397 V 6.6487 PRIOR

(CN) PBoC OMO: Injects CNY300B combined CNY150B in 7-day, 14-day and 63-day reverse repos v CNY140B prior; Net injection CNY80B v CNY40B prior

Equities notable movers

Australia/New Zealand

SGH.AU Updates on recapitalization; -20.6%

AHZ.AU Reports Q1 (A$) Rev 1.9M, +23% y/y; -13%

Japan

7974.JP Reports H1 Net profit ¥51.5B v ¥38.3B y/y, Op profit ¥40.0B v loss ¥5.95B y/y, Rev ¥374B v ¥137B y/y; Raises FY18 outlook’ +4%

3092.JP Reports H1 Net ¥9.6B v ¥8.1B y/y; Op ¥13.8B v ¥10.6B y/y; Rev ¥42.7B v ¥31.6B y/y; -9%

China/Hong Kong

000338.CN Reports Q3 (CNY) Net profit 1.95B, +316.1% y/y; +7.3%

Korea

005930.KR Reports Q3 (KRW) Net 11.2T v 10.8Te; Op 14.5T v 14.5T prelim; Rev 62.1T v 62.0T prelim; +1.6%

Trade Idea : USD/CHF – Buy at 0.9920

USD/CHF - 0.9958

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9957

Kijun-Sen level : 0.9968

Ichimoku cloud top : 0.9991

Ichimoku cloud bottom : 0.9958

Original strategy :

Buy at 0.9920, Target: 1.0030, Stop: 0.9885

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9915, Target: 1.0030, Stop: 0.9880

Position : -

Target : -

Stop : -

Although dollar has recovered from 0.9938, reckon 1.0000 would limit upside and near term downside risk remains for the corrective fall from 1.0038 (last week’s high) to bring retracement of recent rise to 0.9920-25 (38.2% Fibonacci retracement of 0.9737-1.0038), however, reckon 0.9905-10 would limit downside and bring another rise later, above 1.0000 would bring retest of said resistance at 1.0038, break there would extend recent rise from 0.9421 low to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 resistance.

In view of this, we are looking to buy dollar again on pullback as 0.9915-25 should limit downside, bring another rise later. Below 0.9885-90 (50% Fibonacci retracement of 0.9737-1.0038) would defer and suggest top is possibly formed, risk test of support at 0.9869.

Trade Idea : GBP/USD – Sell at 1.3255

GBP/USD - 1.3207

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3204

Kijun-Sen level : 1.3171

Ichimoku cloud top : 1.3175

Ichimoku cloud bottom : 1.3118

Original strategy :

Sell at 1.3255, Target: 1.3135, Stop: 1.3290

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3255, Target: 1.3135, Stop: 1.3290

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after staging a strong rebound from 1.3070, suggesting near term upside risk remains for further gain to 1.3240-50, however, as broad outlook remains consolidative, reckon upside would be limited and indicated strong resistance at 1.3279-87 would remain intact, bring retreat later, below 1.3120-25 would signal the rebound from 1.3070 has ended, bring weakness to 1.3100, then retest of 1.3070, break there would extend the erratic decline from 1.3338 to 1.3050, then towards recent low at 1.3027.

In view of this, we are looking to sell cable on further subsequent recovery as 1.3255-60 should limit upside. Only above indicated strong resistance at 1.3279-87 would abort and shift risk to the upside for the erratic rise from 1.3027 low is still in progress for further gain to 1.3300-10, then towards 1.3340-50.

Trade Idea : EUR/USD – Sell at 1.1700

EUR/USD - 1.1635

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1639

Kijun-Sen level : 1.1630

Ichimoku cloud top : 1.1706

Ichimoku cloud bottom : 1.1607

Original strategy :

Sell at 1.1685, Target: 1.1585, Stop: 1.1720

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1700, Target: 1.1595, Stop: 1.1735

Position : -

Target : -

Stop : -

Euro’s recovery after falling to 1.1574 late last week has retained our view that further consolidation above this level would be seen and corrective bounce to 1.1660-65 cannot be ruled out, however, reckon upside would be limited to the upper Kumo (now at 1.1706) and bring another decline later, below said support at 1.1574 would extend recent decline from 1.2093 top to 1.1550-55 but loss of downward momentum should prevent sharp fall below 1.1520-25 and reckon 1.1500 would hold from here.

In view of this, we are looking to sell euro on subsequent recovery as the upper Kumo (now at 1.1706) should limit upside and bring another decline. Only above previous support at 1.1725 (now resistance) would signal low is formed instead, bring retracement of recent decline to 1.1750-55 first.

Trade Idea : USD/JPY – Sell at 113.80

USD/JPY - 113.12

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.13

Kijun-Sen level : 113.37

Ichimoku cloud top : 113.90

Ichimoku cloud bottom : 113.84

Original strategy :

Sell at 114.20, Target: 113.20, Stop: 114.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 113.80, Target: 112.80, Stop: 114.15

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after dropping from 114.45 (last week’s high), adding credence to our view that top has been made there and consolidation with downside bias remains for this fall to bring retracement of recent upmove, hence further fall to 112.70-75 (61.8% Fibonacci retracement of 111.65-114.45) is likely, however, near term oversold condition should limit downside to 112.50 and reckon previous support at 112.30 would hold from here, bring rebound.

In view of this, we are looking to sell dollar on recovery but at a lower level as the lower Kumo (now at 113.84) should cap upside and bring another decline. Above 114.20-25 would abort and signal the retreat rom 114.45 has ended, bring retest of indicated strong resistance at 114.45-50 which is likely to hold on first testing.