Sample Category Title

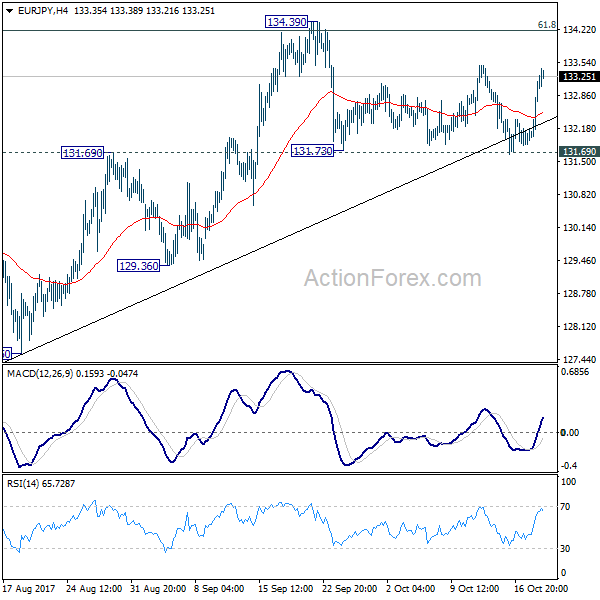

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.28; (P) 132.77; (R1) 133.60; More...

Intraday bias in EUR/JPY remains neutral for the moment. With 131.69 support intact, there is no confirmation of reversal yet. Decisive break of 134.39 high will indicate up trend resumption. Next target will be 141.04 long term resistance. Nonetheless, firm break of 131.69 will be an early sign of medium term reversal and will target 127.55 key support level.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversal and will turn outlook bearish for deeper fall.

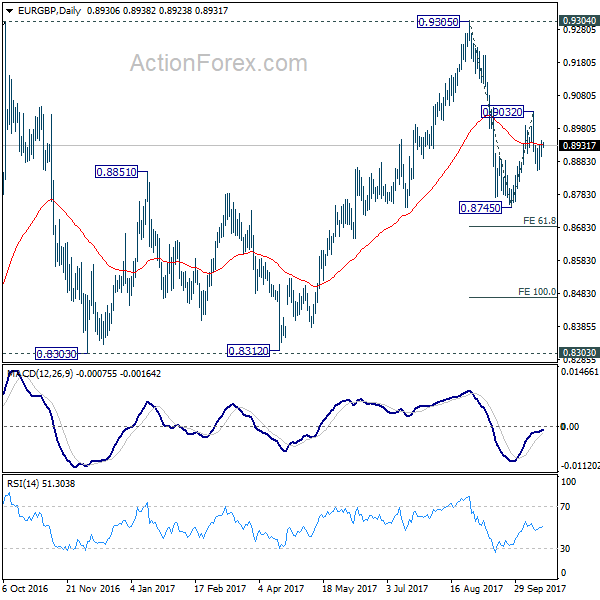

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8899; (P) 0.8923; (R1) 0.8950; More...

Intraday bias in EUR/GBP stays neutral but with 0.9032 resistance intact, deeper decline is in favor. Below 0.8857 will bring retest of 0.8745 first. Break there will extend the fall from 0.9032 to 61.8% projection of 0.9305 to 0.8745 from 0.9032 at 0.8686, and then 100% projection at 0.8472. However, firm break of 0.9032 will turn focus back to 0.9305 high instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

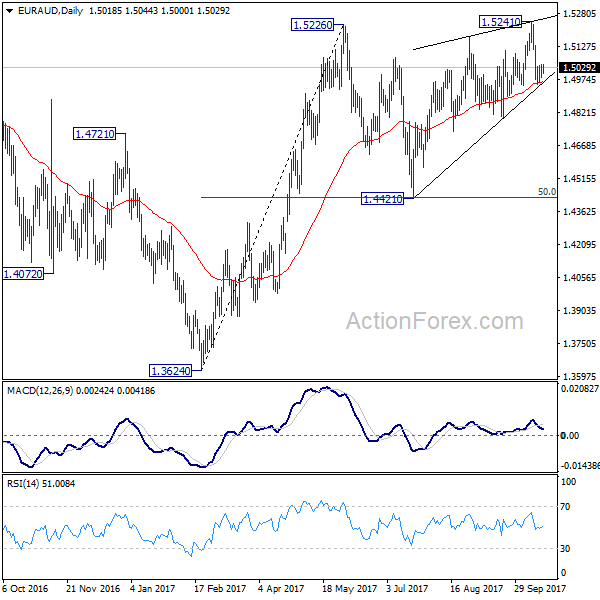

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4985; (P) 1.5014; (R1) 1.5048; More....

Intraday bias in EUR/AUD stays neutral first. But still, as long as 1.5101 minor resistance holds, deeper decline is expected. Break of 1.4945 will affirm the case that fall from 1.5241 is the third leg of consolidation pattern from 1.5226. And, Further break of 1.4791 will target 1.4421 support cluster support (50% retracement of 1.3624 to 1.5226 at 1.4425). We'd expect strong support from there to bring rebound. On the upside, though, above 1.5101 will turn focus back to 1.5241 instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Sustained trading above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

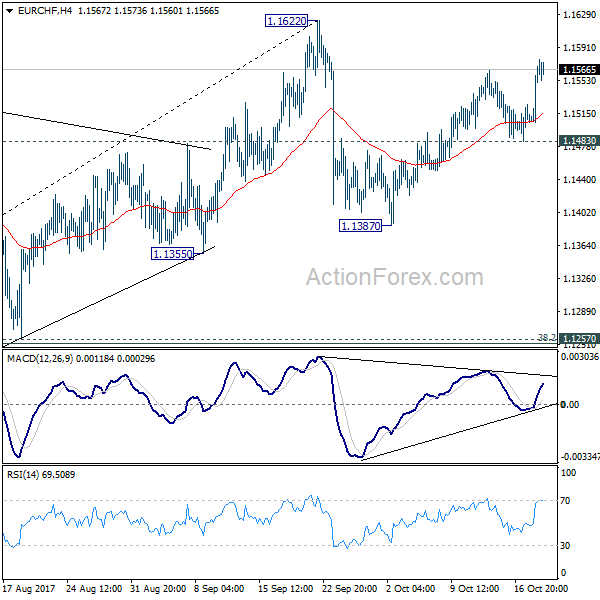

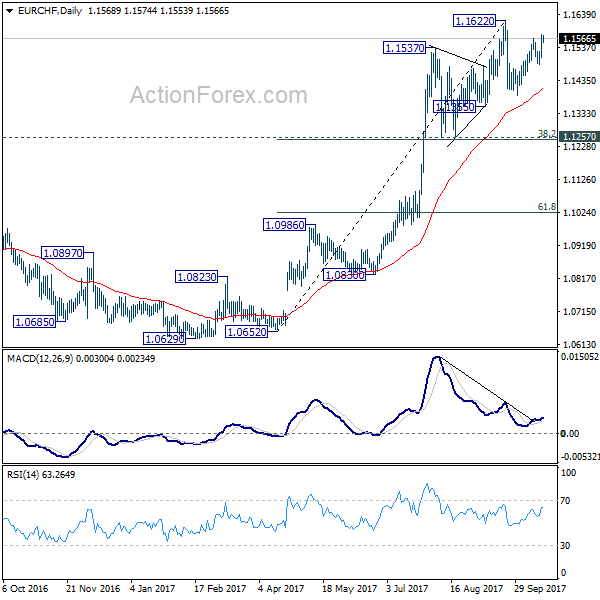

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1523; (P) 1.1551; (R1) 1.1595; More....

Break of 1.1565 suggests that recovery from 1.1387 has resumed. Intraday bias in EUR/CHF is turned back to the upside for retesting 1.1622 high. At this point, we'd still expect resistance from there to limit upside to bring another fall. Consolidation from 1.1622 would extend with another leg. On the downside, below 1.1483 minor support will turn bias to the downside for 1.1387 support and below.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

Yen and Franc Stay Weak on Strong Risk Appetite, Euro Outperforms Dollar

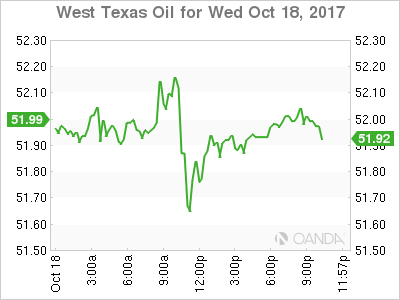

Japanese Yen and Swiss Franc remain the weakest ones for the week on strong global risk appetite. German DAX closed at new record of 13043.03 yesterday. That was followed by 160.16 pts rise in DOW to 23157.60, and 1.9pts rise in S&P 500 to 2561.26. Both were record highs. US treasury yield followed and closed up 0.041 at 2.339. But that was not followed by Dollar as the greenback reversed earlier gains in late US session. Indeed, Euro is seen to be outperforming Dollar against Swiss Franc and Yen. In other markets, Gold is now back below 1280 after recent recovery hit 1308.4 and lost steam. WTI crude oil is firm at around 52 but struggle to get through 52.86 near term resistance.

Fed Kaplan and Dudley warned tax cut could be harmful

Dallas Fed President Robert Kaplan said that is if the US President Donald Trump's tax plan is just a "short-term stimulus, or basically a tax cut funded by growth in deficit", it could be "harmful". Kaplan added that "we are either at full employment or are nearing full employment, and my concern is that if we do a tax cut financed by increasing the debt, the deficit, we'll get the short-term up and then come right back down to trend growth, and when it's over, we'll be more highly leveraged than we were before."

New York Fed President William Dudley said that "we are a long way from tax reform". But, "if we would be able to lower the corporate tax rate and broaden the base... that would be good for the United States". Nonetheless, he expressed his concerns that there is little discussion on government debt levels. And he warned that "are going to start to ramp up as the Fed continues to raise short-term interest rates. Investors right now aren't focused on debt service burdens anywhere in the world...That could change quickly."

Fed's Beige Book economic report showed that US growth was "split between modest and moderate" among the regions. Labor markets were widely described as "tight". And, labor shortages in some sectors were actually "restraining business growth". However, "despite widespread labor tightness, the majority of districts reported only modest to moderate wage pressures." Employers opted for "sign-on bonuses, overtime, and other non-wage efforts to attract and retain workers" instead.

UK May assures EU citizens ahead of EU summit

UK Prime Minister Theresa May offered some more incentive for EU officials just ahead of the summit in Brussels. In her Facebook page, May pledged that "EU citizens who have made their lives in the UK have made a huge contribution to our country. And we want them and their families to stay. I couldn't be clearer: EU citizens living lawfully in the UK today will be able to stay." May has been trying to save Brexit negotiations after it was described as deadlocked by EU officials last week. There is practically no chance for EU to approve the "go" for trade agreement talks this week. But some officials are seeing 50/50 chance of having that "sufficient progress" by December.

Japan trade surplus narrowed, with temporary slow down in exports

Japan trade surplus narrowed to JPY 0.24T in September. Export grew 14.1% yoy, lower than expectation of 14.9% yoy, and the first slowdown in three months. Nonetheless, the 18.1% yoy growth of export back in August was the fastest in nearly four years. It's generally seen that the slowdown is temporary and recovery in global economy is still in place. Imports rose 12.0% yoy, also below expectation of 15.0% yoy.

Improving labor market could allow RBA to pare back stimulus

Australia NAB business condition index rose 2 pts to 15. But business confidence dropped 1 pt to 7 in Q3. NAB chief economists Alan Oster noted that overall results point to improvements in the economy. And, "a positive byproduct of that has been solid outcomes for hiring intentions and capex plans for the year ahead." Also, "there now seems to be sufficient evidence to suggest that the labour market will continue to improve enough to allow the RBA to pare back some of its emergency stimulus."

Separately released, employment grew 19.8K in September, above expectation of 15.0K. That's also the 12 straight month of growth. Full time jobs grew 6.1K while part-time jobs grew 13.7K. Participation rate was unchanged at 65.2%. Unemployment rate dropped to 5.5%, below expectation of 5.6%. That's also the lowest reading since May, which then was the lowest since early 2013.

Elsewhere

China GDP rose 6.8% yoy in Q3, slowed from 6.9% yoy but met expectation. Retail sales rose 10.3% yoy in September, above expectation of 10.2% yoy. Fixed asset investments rose 7.5% yoy, below expectation of 7.7% yoy. Industrial production rose 6.6% yoy, above expectation of 6.4% yoy.

Swiss trade balance and UK retail sales are featured in European session. From US, jobless claims, Philly Fed survey and leading indicators will be released.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1523; (P) 1.1551; (R1) 1.1595; More....

Break of 1.1565 suggests that recovery from 1.1387 has resumed. Intraday bias in EUR/CHF is turned back to the upside for retesting 1.1622 high. At this point, we'd still expect resistance from there to limit upside to bring another fall. Consolidation from 1.1622 would extend with another leg. On the downside, below 1.1483 minor support will turn bias to the downside for 1.1387 support and below.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance JPY Sep | 0.24T | 0.32T | 0.37T | 0.31T |

| 0:30 | AUD | NAB Business Confidence Q3 | 7 | 7 | 8 | |

| 0:30 | AUD | Employment Change Sep | 19.8k | 15.0k | 54.2k | 53.0k |

| 0:30 | AUD | Unemployment Rate Sep | 5.50% | 5.60% | 5.60% | |

| 2:00 | CNY | GDP Y/Y Q3 | 6.80% | 6.80% | 6.90% | |

| 2:00 | CNY | Retail Sales Y/Y Sep | 10.30% | 10.20% | 10.10% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Sep | 7.50% | 7.70% | 7.80% | |

| 2:00 | CNY | Industrial Production Y/Y Sep | 6.60% | 6.40% | 6.00% | |

| 4:30 | JPY | All Industry Activity Index M/M Aug | 0.20% | -0.10% | ||

| 6:00 | CHF | Trade Balance (CHF) Sep | 2.47B | 2.17B | ||

| 8:30 | GBP | Retail Sales M/M Sep | -0.10% | 1.00% | ||

| 12:30 | USD | Initial Jobless Claims (OCT 14) | 240K | 243K | ||

| 12:30 | USD | Philadelphia Fed Business Outlook Oct | 22 | 23.8 | ||

| 14:00 | USD | Leading Indicators Sep | 0.10% | 0.40% | ||

| 14:30 | USD | Natural Gas Storage | 87B |

Regional Update Post China GDP

The Australian employment change number was slightly better at 19.8k versus 15k expected

Unemployment has edged down to 5.5% from 5.6%

AUDUSD did bounce some 20 pips higher and was poised to benefit from any hint of US weakness. But with the China GDP coming in on consensus, whatever bullish sentiment the markets were positioned for an upside surprise after Zhou Xiaochuan’s comment earlier this week that the economy could grow 7 percent in the second half of the year should get priced out quickly. The GDP reading could weigh negatively on both mainland Stock and currency markets as traders may position for further weakness into year-end suspecting financial curbs will continue to have a negative impact on growth in China with GDP possibly topping.

USDCNH traders were caught short likely positioning for a more robust GDP print

The rest of the data is not terrible, but I suspect the markets will focus on a possible slower China growth narrative

Outside of regional concerns the Big dollar doing little more than running in circles awaiting the nomination of the next Fed Chair and headway on the contentious tax reform bill.

Research Japan: Abe Set For Another Term Despite Declining Public Support

Today's key points

- PM Abe's LDP close to maintaining single party majority in Lower House.

- Looks like vote of confidence in Abenomics and thus a reappointment of BoJ governor Kuroda and a continuation of QQE and YCC.

- USD/JPY could bounce higher if Abe wins, but relief rally should be shallow and short-lived

Shinzo Abe and his Liberal Democratic Party (LDP) are poised to remain the biggest party by far and continue in government after the general election to the Lower House on 22 October. In Japan, the electoral system tends to favour the biggest party. In the 465-seat Japanese Lower House, 289 seats are elected in single constituent first-past-the-post elections while the remaining seats are elected with proportional representation. The main question is currently whether the LDP and its coalition partner Komeito can maintain their two-thirds super majority that they have held since the general election in 2012. Abe needs to form a two-thirds majority in order to realise his plans to revise Japan's 70-year-old pacifist constitution, and thus validate the existence of the Japan Self-Defense Force. For this, he probably needs to collaborate with the new Party of Hope and not the Buddhist pacifist Komeito.

For a while, PM Abe might have regretted his 25 September call for a snap election, as Tokyo governor Yoriko Koike founded Kibō no Tō (Party of Hope) just hours before Abe declared an early election. Koike is a popular political figure in Japan and a former minister of defence in the first Abe cabinet. When the leader of the opposition Democratic Party (DP), Seiji Maehara, announced that the party had split just a few days later, and many of the representatives started to emerge as candidates for Party of Hope, a united opposition and a strong alternative to LDP rule was suddenly a possibility. However, not all DP candidates got along with Koike, which has split the opposition once again as the new Constitutional Democratic Party of Japan (CDP) rose from the ashes. Furthermore, Koike has decided not to run for parliament, which effectively leaves Party of Hope without a PM-candidate.

Polls look promising for Abe

Abe has probably breathed a sigh of relief, as recent polls have ticked in suggesting that the LDP will win a significant majority. The newspaper Mainichi gives the LDP 292 seats in the 465-seat Lower House. Adding Komeito's projected 31 seats gives the coalition close to 70% of the seats, slightly more than they held before the house was dissolved. Party of Hope and the CDP currently stand to win only 48 and 47 seats, respectively. If the polls remain unchanged, it would put Abe on track to be re-elected as chairman of the LDP in September 2018 and thus likely to become the longest-ever serving Japanese prime minister. With as many as 43% of voters preferring not to see Abe stay as prime minister and an approval rating of only 37%, this outcome could appear somewhat puzzling, though. Lack of any clear alternative is part of the explanation. That said, the majority of voters have still not decided who to vote for, which means there is still uncertainty over the election outcome

Economy still in great shape but sales tax hike is looming

Should Abe's coalition stumble at the finish line, Japan is not likely to change political course dramatically. Party of Hope is a conservative party close to the LDP in many areas. One key difference relates to the planned sales tax hike in October 2019, though. Abe needs it to fund social security spending and at some point pay down Japan's enormous debts. Koike wants to freeze it to ensure economic recovery and impose a tax on companies' internal reserves instead. Also, the CDP does not want to impose the hike all at once.

We expect the Japanese economy to stay on track, supported by the global economic recovery. The large Japanese manufacturing sector recently showed the most optimistic business outlook in a decade and the economy in general seems in good shape. That said, it is a risk that Abe will focus too much on revising the constitution and refrain from working hard on the third pillar of Abenomics (structural reform). No matter what, it remains a challenge for Abe to keep the economic upturn going for another two years so Japan does not go into recession when the sales tax hike hits. It might be wiser to make the increase gradually in order to avoid a situation like 2014, where private consumption surged due to exactly a sales tax hike. We saw some improvement in domestic demand earlier this year, but generally the economy is still very dependent on the global economic recovery and an ultraaccommodative economic policy still looks necessary.

In our main scenario, we expect the Bank of Japan (BoJ) to keeps its policy unchanged, maintaining the short-term policy interest rate at -0.1% and the 10Y Japanese government bond (JGB) yield at 0% over our 12M forecast horizon, assuming BoJ governor Haruhiko Koruda is reappointed when his term ends in April - this seems likely, as Abe can do this with a simple majority.

FX outlook: we still look for a higher USD/JPY

Solid victory for Shinzo Abe expected in the FX market……. Financial markets seem complacent that Abe will remain prime minister after the general election on Sunday, and there is hardly any election risk premium priced in the FX option market. Hence, while USD/JPY could bounce higher after the election if Abe secures a two-thirds majority, market pricing indicates that a possible relief rally would be shallow and short-lived.

But… USD/JPY supported by Fed-BoJ divergence and global business cycle We still see USD/JPY moving higher in coming months as the global business cycle environment remains constructive for the cross and as we expect the Fed will hike interest rates in December. We target the cross at 113 in 1M (previously 111) and 114 in 3M. Longer term, we expect the combination of 1) Fed-BoJ divergence, 2) higher global yields (eventually) supported by global growth recovery and 3) portfolio outflows out of Japan will continue to keep the cross floating. We target USD/JPY at 115 in 6M and 116 in 12M. Downside risks to our forecast primarily arise from the yen's high correlation with 10Y US yields, a high sensitivity to risk appetite in general and a stretched short JPY positioning.

Dollar Lacks Conviction

Dollar lacks conviction

The lack of conviction and some questionable US economic data had all but stalled the USD dollar rally against most G-10. The exception being USDJPY where the election tail risk premium is being priced out and speculators are adding long positions anticipating a decisive Abe victory on Sunday.

In reality, the latest USD dollar rally was always suspect at best based solely on optimism surrounding the possibility of Taylor’s Fed Chair appointment and a slightly more hawkish tone from the Fed. The former is a guess at best and the latter, well that’s a guessing game too.

The focus should be on the US Senate face-off over two critical pieces of legislation: budget resolution vote and tax reform. With lots of demands yet to be ironed out on both sides of the floor, another cloud of uncertainty forms over the Foggy Bottom. But Treasury Secretary Steven Mnuchin was in no the mood to mince words when he told Congress to cut taxes or risk a stock market crash. Dollar sentiment will remain very guarded until these key issues are resolved.

You know the old saying, where there’s doubt stay out.And according to overnight price action trader did precisely that as the Greenback spent the better part of the NY session plodding aimlessly within confined ranges.

Little to be gleaned from US economic data overnight as both the beige book and housing data prints distort due to the hurricane effect

There certainly a lot of noise in the market but the main distraction remains who will be the next Fed chair.

The Euro

Traders have lightened Eur positioning ahead of the EU leaders’ summit where Brexit is top of the agenda. Political noise is difficult to navigate and usually best to let the dust settle before re-engaging. But the reality is Euro traders are waiting for next week’s European Central Bank meeting for direction, and the current ranges will likely hold until then.

Japanese Yen

Whether its a case USDJPY playing catch up to the Nikkie, election risk premiums were unwinding or funds buying on expectation of a convincing Abe victory, all paths lead to the same destination. Not too unexpectedly were testing the 113 handle as we turn the corner towards weeks end and Sunday’s Japanese elections.

The British Pound

Another though London session for Sterling markets, however, Cable was able to drag itself off the mat as traders reduce risk ahead of the EU Summit on Brexit.

Brexit concerns are paramount as even yesterday boisterous UK jobs failed to get an initial rise out of the markets.

At times positioning looks arbitrary at best. purely based on headline risk.As a result, the Pound is becoming tortuous and messy to trade.

New Zealand Dollar

Not to belabour the issue at hand but New Zealand First, the kingmaker-party post-election should announce its coalition decision today. Weaker milk auctions yesterday were more or less ignored and there an air market optimism in early trade.

Australian Dollar

Awaiting local Jobs report and the China Data dump before updating views

FX Asia

Besides the apparent Fed Chair debate, local markets are focusing on local central bank decision and the accompanying musings.

Bank of Indonesia: expected to hold rates steady at 4.25 % but markets leaning for another cut in 2018

Bank of Korea: expected to remain on hold but the voting splits ( dissidents) are of interest to the markets.The BoK prefers running behind the rate curve, and this should be the case this month. But in reality, it makes little sense turning the rate hike screws on given the geopolitical landscape.

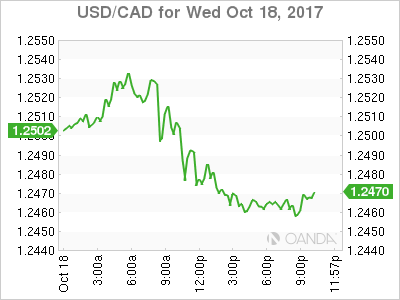

USD/CAD Canadian Dollar Surges On Strong Manufacturing Sales

The Canadian dollar is higher on Wednesday on a surprise surge in manufacturing sales. Canadian manufacturing sales jumped 1.6 percent in August. The positive gain broke a trend of two negative readings with advances in 8 of the 21 industries. The auto sector was the biggest driver of the recovery. The forecast called for a contraction and the surprise to the upside boosted the loonie that was on its way to appreciate after a NAFTA setback earlier in the week.

Falling oil inventories in the US reversed a downtrend in crude prices. The Energy Information Administration (EIA) reported a drawdown of 5.7 million barrels beating a forecast of a 4.7 million decline. The comments from the Iraqi prime minister had prices lower as the disruption of oil supply for the region was restored with security restored to Kirkuk.

Canadian Foreign Affairs Minister Chrystia Freeland was part of a trilateral press conference on Tuesday at the end of hte fourth round of trade talks. Freedland said that the demands from the United Sates are making the negotiation more challenging. The US trade representative Robert Lighthizer stuck to his mandate by President Trump and focused only on reducing America’s trade deficits. The Mexican representative tried to be more amicable and stressed that the process does not have to end with a lose-lose result.

The USD/CAD lost 0.40 percent on Wednesday. The currency pair is trading at 1.2468 with a rising loonie recovering from a NAFTA negotiation nearing deadlock as the three nations remains too far apart on big issues. The Canadian dollar has been one of the best in the last six months. The CAD has appreciated 7.36 percent in that time frame due to strong economic growth and two rate hikes by the Bank of Canada (BoC). The slowdown in GDP gains came at the same time NAFTA talks are entering into the more difficult issues. The US had warned it would not back down in its effort to reduce trade deficits and had already increased tariffs for some Canadian goods.

The surprise gain in manufacturing sales could be followed by a better than expected data on retail sales and consumer price index to be released on Friday, October 20. Housing data was weak in the US on Wednesday with building permits coming in lower than expected at 1.22 million and housing starts also underperforming expectations at 1.13 million. The biggest question marks around the US remain on the political realm with the name of the next Fed chair still unknown and the tax reform effort failing to take off as it faces harder scrutiny.

The Bank of Canada (BoC) will issue its monetary policy report and rate statement on Wednesday, October 25 at 10:00 am. There are less than 20 percent probabilities of a rate hike in October after the central bank took the market by startled investors when October seems to be the more likely meeting to announce the second rate hike. Governor Stephen Poloz will host a press conference at 11:15 am EDT. The BoC was criticized for its lack of warning on the October rate move given that in June it had gone all out to get the market onside with the eventual July lift in the Canadian benchmark rate

Oil is flat on Wednesday. Crude prices were higher after the release of the larger than expected drawdown in US inventories and rumours that the Organization of the Petroleum Exporting Countries (OPEC) is seeking a 9 month extension to the current production cut deal. Less supply drove up prices, with West Texas Intermediate crossing the $52 price level. WTI could not hold the gains and with higher gasoline and distillate stocks.

The oil rich province of Kirkuk is now in the hands of the central Iraqi government with supply set to resume to normal levels. The situation in Northern Iraq had put oil at a premium alongside the return of US economic sanctions to Iran that would limit global supply.

Market events to watch this week:

Thursday, October 19

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, October 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

7:15pm USD Fed Chair Yellen Speaks

China Hints, Aussie Jobs Next

Signals from China are usually subtle and actions are often dramatic, we look at Xi's landmark speech to start the Party Congress. The Canadian dollar was the top performer and the yen lagged. The Australian jobs report and a sensitive Chinese GDP reading are up next. The latest Premium video is posted below.

Xi spoke for nearly three-and-a-half hours to start the Congress in what is his longest-ever speech by far. That timeline gave him an opportunity to touch on just about everything, but one thing he didn't mention is an oft-repeated pledge to double growth between 2010 and 2020.

Along with a further emphasis on corruption, stability and a year-2035 horizon for becoming a 'modern' nation, make us wary that any tough choices that need to be made will come soon. The Congress – where new top leaders are installed – takes place every five years and like with all politicians, it's best to take the bad medicine early.

The Congress continues until Tuesday so we will be looking for more signs of deleveraging. The health of the economy will determine the extent of the crackdown. On that front, some key numbers are due at 0200 GMT with GDP, retail sales and industrial production. Growth is expected at 1.7% q/q and 6.8% y/y. We're skeptical of Chinese numbers at the best of times but the data during the Congress is especially dubious. Still, it will be a talking point.

The other big number to watch is the 0030 GMT Australian jobs report. The consensus is for a +15.0K reading following a +54.2K surprise last month. Another strong report and a drop in the 5.6% unemployment rate could help to ease housing worries and jar the RBA out of neutral.