Sample Category Title

Market Update – Asian Session: China Q3 GDP Comes In As Expected

Asia Summary

Asian equity markets opened the session mixed. Chinese equity markets have traded somewhat lower as GDP in Q3 met expectations. Recall, there were some expectations that the figure could be better than expected.

The Nikkei 225 opened higher, as the index attempts to gain for the 13th straight session, which would be the longest winning streak in over 20 years.

Japanese banks have traded broadly higher amid the recent gains in government bond yields and earlier rise in some of the larger US banks. Australian banks are also generally trading higher.

Australian energy company quarterly updates were in focus. Santos has gained after raising its FY production forecast, while Woodside Petroleum has declined after reporting lower Q3 revenues and naming a new CFO.

In terms of technology, Taiwanese companies that supply Apple are generally lower following a press report that the US tech firm is said to have cut iPhone 8 orders for Nov and Dec. Also, South Korean chip makers are once again trading lower on today's session. LG Electronics has gained over 5% on reports that the company will partner with Qualcomm on self-driving auto components.

Chinese telecom ZTE Corp has declined by over 3%, despite reporting y/y growth in its 9-month net profits and revenues.

In describing China's GDP data, the Stats Bureau said in the Jan-Sept period consumption contributed 64.5% to GDP. It also expects the domestic economy to maintain improving momentum. Amid the data, China's 10-year bond yield has declined.

Australia's 3-year bond yield has risen by over 4bps, after the September employment change beat expectations, while the unemployment rate unexpectedly fell. Yields have also moved higher following the gains seen in US Treasury yields on Wednesday's session amid comments from influential NY Fed President Dudley. Dudley said the Fed is on the path to achieve 3 rate hikes in 2017 (implying one more rate increase this year). Recall when Dudley previously spoke on Oct 6th, he did not comment on the timing for rate hikes.

At the longer end of the curve, earlier today, Japan's 20 and 30-year JGB yields hit highs not seen since July. Bank of Japan (BoJ) official Nakaso said the central bank will adjust the shape of the yield curve as needed. He added that the BoJ can achieve the same rate with smaller amount of JGB purchases.

Meanwhile, in South Korea the 10-year bond yield has risen over 3bps, as even though the Bank of Korea (BOK) left rates unchanged (as expected), there was a hawkish dissenter at today's policy meeting, who voted for a rate hike. The central bank additionally raised its 2017 GDP growth and inflation forecasts as it believes the impact of souring trade relations with China will ease in 2018.

In foreign exchange, the PBoC's Sept Net Forex Purchase Position saw its first m/m rise since Oct 2015. The data comes amid other signs of easing capital outflows from China. PBoC Gov Zhou said the yuan's trading band (currently 2%) is not too important and the expansion of it is not a current focus.

The Aussie traded toward session highs following the better than expected Sept employment change. However, the currency has since pared gains after the in line China GDP data. The Kiwi has traded lower, as the government formation process in New Zealand continues. On yesterday's session, a NZ First Party official said an announcement was expected during this afternoon.

Looking ahead, US companies due to report earnings today include Bank of NY Mellon, Intuitive Surgical, Nucor, PPG Industries, PayPal, Philip Morris and Verizon.

Key economic data

(CN) CHINA Q3 GDP Q/Q: 1.7% V 1.7%E; Y/Y: 6.8% V 6.8%E

(JP) JAPAN SEPT TRADE BALANCE: ¥670.2B V ¥556.8BE; ADJ: ¥240.3B V ¥367.3B PRIOR

(AU) AUSTRALIA SEPT EMPLOYMENT CHANGE: +19.8K V +15.0KE; UNEMPLOYMENT RATE: 5.5% V 5.6%E

(AU) Australia Sept RBA Govt FX Transactions (A$): -762M v -581M prior

(KR) BANK OF KOREA (BOK) LEAVES 7-DAY REPO RATE UNCHANGED AT 1.25%; AS EXPECTED

(CN) CHINA SEPT FIXED ASSETS EX RURAL YTD Y/Y: 7.5% V 7.7%E

(CN) CHINA SEPT RETAIL SALES Y/Y: 10.3% V 10.2%E; YTD Y/Y: 10.4% V 10.3%E

(CN) CHINA SEPT INDUSTRIAL PRODUCTION Y/Y: 6.6% V 6.5%E; YTD Y/Y: 6.7% V 6.7%E

(CN) China PBoC Sept Net Forex Purchase Position (CNY): +0.9B m/m (first rise since Oct 2015)

Speakers and Press

Japan

(JP) Japan PM Abe Cabinet approval rating declines 2 pct points to 38% - Asahi Poll

(JP) BoJ Nakaso: Will adjust shape of yield curve as needed; BoJ can impact rates even if JGBs to buy become scarce

South Korea

(KR) South Korea Finance Ministry: While North Korean tensions have persisted, financial markets have been stable and the impact on the economy has been limited - statement ahead of parliamentary audit due Oct. 19-20

China/Hong Kong

(CN) China Economist sees China avg annual GDP growth at 5% from 2020-2035 - Chinese press

(CN) PBOC Yi Gang: Price stability not equal to financial stability -speaking at 19th Party Congress

(CN) China Banking Regulatory Commission (CBRC) Guo: China to deepen reform, opening up banks - speaking at 19th Party Congress

(CN) China Wind data shows Q3 performance forecast reports from China's listed companies have beaten market expectations – Xinhua

USD/CNY (CN) PBOC Gov Zhou: Yuan trading band is not too important, band expansion is not a current focus

(CN) China FX Regulator SAFE Chief/PBoC Pan: China FX market supply and demand basically balanced

(CN) China Stats Bureau (NBS) Xing: Jan-Sept consumption contributed 64.5% to GDP growth, 32.8% for capital formation and 2.7% for net exports; Domestic economy to maintain steady and improving momentum

Australia/New Zealand

(NZ) New Zealand National Party Leader English: Does not know whether NZ First will support National; Will present to caucus the ‘broad parameters' of agreement with NZ First and will seek their support

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.4%, Hang Seng -0.2%; Shanghai Composite -0.4%; ASX200 +0.0%, Kospi -0.4%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1816-1.1792; JPY 113.09-112.88; AUD 0.7871-0.7841;NZD 0.7171-0.7123

Dec Gold -0.1% at $1,281/oz; Nov Crude Oil -0.1% at $51.98/brl; Dec Copper -0.1% at $3.17/lb

(NZ) New Zealand sells NZ$200M in 2.75% 2025 bonds; avg yield 2.7545%; bid-to-cover 2.66x

(CN) China PBOC injects CNY140B in combined 7-day and 14-day reverse repos v CNY300B prior; injects net CNY100B v CNY270B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.6093 V 6.5991 PRIOR

(JP) Japan MoF sells ¥1,78T in 5-yr JGBS; avg yield -0.0820% v -0.110% prior; bid-to-cover 4.24x v 4.07x prior

Equities notable movers

Australia/New Zealand

RCR.AU Awarded gas-fired power plant contract with PT Kartanegara Energi Perkasa in Indonesia worth ~A$75M; +6%

PEN.AU To divest 74% stake in South Africa Karoo projects through an active process; -4.8%

Korea

047810.KR Will not to put co. under evaluation for possible delisting, trading resumes; +14.3%

China/Hong Kong

763.HK Reports 9-month (CNY) Net 3.91B v 2.86B y/y, Op 5.29B v 952M y/y, Rev 76.6B v 71.6B y/y; -5%

US

AAPL Said to cut orders for iPhone 8 and Plus by around 50% for Nov and Dec to 5-6M units/month - Taiwanese Press; -0.9% after hours

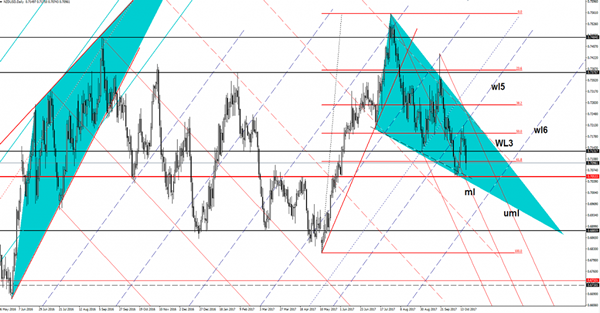

NZD/USD Falling Wedge?

The NZD/USD drops like a rock and should reach the 0.7053 static support. Remains to see what will happen in the upcoming days because a USDX’s drop will force the pair to increase again. Price could move in range on the short term, I’ve drawn a Falling Wedge pattern, but this is far from being confirmed. The behavior could change if the rate will start to make higher lows and could signal another leg higher.

Gold Should Drop Further

The rate has dropped further and has resumed the bearish momentum. Technically, it should drop to reach and retest the sliding line (SL) of the ascending pitchfork after the breakdown below the 50% retracement level. Remains to see how will react when will hit the SL, a valid breakdown will confirm a drop towards the 61.8% retracement level.

AUD/USD More Upside In View

The currency pair has increased in the morning and seems poised to climb much higher in the upcoming days as the USDX failed to breakout above the 93.81 static resistance. The dollar index has slipped lower and is pressuring a dynamic support, a valid breakdown will signal a further drop and will force the USD to depreciate versus its rivals.

The USDX could move sideways on the short term before will recapture enough directional energy to start a bullish momentum.

The Aussie increased on the good Australian data and on the mixed Chinese data. The Australian Unemployment Rate decreased from 5.6% to 5.5% in September, while the Employment Change was reported at 19K, much below the 14.1K estimate.

The Chinese GDP was reported at 6.8% in the third quarter, matching expectations, while the Industrial Production increased by 6.6%, less versus the 6.4% estimate and compared to the 6.0% growth in the former reading period.

The AUD/USD increased after the yesterday’s indecision and could jump much higher in the upcoming days. The next upside target will be at the upper median line (uml) of the descending pitchfork, where he may find resistance again. It could be attracted by the confluence area formed between the 23.6% retracement level with the upper median line (uml). The failure to reach and retest the median line (ml) of the descending pitchfork and the failure to close below the 0.7835 should send the rate higher.

Daily Wave Analysis: EUR/USD 61.8% Fib Bounce Starts Triangle Chart Pattern

Currency pair EUR/USD

The EUR/USD bounced at the 61.8% Fibonacci level of potential wave B (purple) and support trend line (blue). A break above the resistance trend line (orange) would confirm a bullish breakout within wave C of wave X (pink). A break below the support trend line and 78.6% Fibonacci level makes a bullish ABC less likely and price will probably continue lower as part of wave 4 (light purple).

The EUR/USD broke above the resistance trend lines (dotted orange) and could be building a wave 1-2 if price stays above the 100% Fibonacci level of wave 2 vs 1.

Currency pair GBP/USD

The GBP/USD is still undecided about a bearish or bullish direction and could still go both ways. The two main scenarios are: a bearish ABC (green) or a wave 123 (green) is taking place. Price invalidates that wave 4 (orange) correction if price breaks above the resistance trend line (yellow). A break below the support trend line (blue) increases the chance of a bearish break within wave 5 (orange).

The GBP/USD bounced at the support trend line (blue) and could either be building a wave 1—2 pattern (brown) or an ABC corrective wave (grey). The wave (brown) is invalidated if price breaks above the 100% Fib level.

Currency pair USD/JPY

The USD/JPY broke above two resistance trend lines (dotted) but it could be building a larger WXY (pink) correction within wave 2 or B (purple) if price stays below the 138.2% Fibonacci level of wave X (pink). Strong momentum today however could make such a wave 2/B (light purple) correction less likely.

The USD/JPY bullish break above the resistance trend line (dotted red) could be part of a bullish wave C (purple) of wave X (pink) correction. This could be confirmed if price breaks below the support trend line (blue).

In The UK, We Get Retail Sales For September

Market movers today

Today, the two-day EU summit in Brussels kicks off. Markets will again focus on any headlines regarding Brexit , as UK Prime Minister Theresa May will share her reflections on the current state of negotiations during EU leaders' working dinner later today.

In the UK, we get retail sales for September. The indicator usually moves markets but in reality it is a very weak indicator of actual consumption growth.

The Philly Fed index is due to be released in the US and consensus is for a moderate decline to 22.0, as any meaningful progress with tax legislation and the potential for fiscal stimulus remains absent .

In Scandinavia, the Swedish unemployment rate for September is due out , which we estimate to have decreased slightly to 6.5% (see next page).

Selected market news

Yesterday, the UK jobs report showed an unchanged unemployment rate at 4.3% and weekly earnings excluding bonuses at 2.1% y/y in August down from 2.2% y/y in July. In our view, the report should not alter the core Bank of England (BoE) members' view, i.e. that it is appropriate to raise the Bank Rate by 25bp at the upcoming monetary policy meeting next month.

Today, the political developments in Spain will again be back in focus as the deadline for the Catalan President Carles Puigdemont to clarify the Catalan leader's position on independence is 10:00 CEST.

In China, the 19th Congress of the Communist Party opened yesterday with Xi Jinping presenting the so-called work report. Overall, the report contained few surprises. With Xi Jinping starting on his second five-year term, we should expect continuity on all policies: a continuation of the corruption campaign, strengthening of economic and financial reforms and a continued gradual opening of the Chinese economy. However, it is likely to happen in the usual ‘two steps forward, one step back' fashion, as China is balancing reforms with control by the leadership. If something rocks the boat , China favours regaining control at the expense of opening up, as we have seen over the past few years when it sealed capital out flows following the financial storm in 2015/early 2016.

Overnight economic data releases showed Chinese growth in Q3 17 at 6.8% y/y (in line with consensus). We look for a moderate slowdown in China over the next year due to financial tightening and measures to cool housing. We forecast GDP growth to be 6.8% in 2017 and to fall to 6.3% in 2018. A hard landing is not likely though, as residential inventories are low and exports are supported by robust global growth.

Elliott Wave View: AUDUSD Intra Day

AUDUSD Short Term Elliott Wave view suggests that Primary wave ((W)) ended at 0.7731 on October 6th low. Up from there, Primary wave ((X)) is currently unfolding as a double three Elliott Wave structure. Intermediate Wave (W) of ((X)) ended at 0.7807 and Intermediate wave (X) of ((X)) ended at 0.7815. Near term, while pullbacks stay above 0.7815, but more importantly above 10/6 low at 0.7731, expect pair to extend higher. At this stage, pair still needs to break above Intermediate wave (W) at 0.7815 to give more validity to this view. Until then, we can’t rule out a double correction in Intermediate wave ((X)).

AUDUSD 1 Hour Elliott Wave Chart

Double three ( 7 swings) is one of the most common corrective patterns in Elliott wave’s theory. We often refer to double three structure as a 7-swing structure. It is a great pattern that allows traders to trade with a well-defined level of risk and target areas. Below is the image of a Double Three structure. It has labels of (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

Australia’s Unemployment Rate Dipped To A 4-Month Low In September

For the 24 hours to 23:00 GMT, the AUD rose 0.08% against the USD and closed at 0.7848.

LME Copper prices declined 1.1% or $74.5/MT to $6971.5/MT. Aluminium prices declined 0.2% or $4.5/MT to $2106.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7848, with the AUD trading flat against the USD from yesterday's close.

Overnight data revealed that Australia's seasonally adjusted unemployment rate unexpectedly dropped to 5.5% in September, hitting its lowest level since May 2017 and boosting optimism over the health of the nation's labour market. Markets had expected the nation's unemployment rate to remain unchanged at 5.6%. Further, the number of people employed in the nation advanced by 19.8K in September, surpassing market expectations for an increase of 15.0K and following a gain of 54.2K in the previous month.

Elsewhere in China, Australia's largest trading partner, the gross domestic product (GDP) advanced 6.8% on an annual basis in the third quarter of 2017, at par with market consensus and following a rise of 6.9% in the previous quarter.

Further, the nation's retail sales climbed more-than-expected by 10.3% on an annual basis in September, compared to a rise of 10.1% in the previous month, while markets had anticipated for an increase of 10.2%. Also, the nation's industrial production rose 6.6% YoY in September, accelerating to a three-month high and beating market expectations for a gain of 6.5%. Industrial production had registered an advance of 6.0% in the prior month.

The pair is expected to find support at 0.7821, and a fall through could take it to the next support level of 0.7793. The pair is expected to find its first resistance at 0.7874, and a rise through could take it to the next resistance level of 0.7899.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Construction Output Fell In August

For the 24 hours to 23:00 GMT, the EUR rose 0.23% against the USD and closed at 1.1796.

Macroeconomic data showed that the Euro-zone's seasonally adjusted construction output eased 0.2% on a monthly basis in August, following a revised flat reading in the prior month.

The US Dollar declined against a basket of major currencies, after the latest data suggested housing sector could act as a drag on the nation's economic growth in the third quarter.

Data indicated that housing starts declined to a one-year low in September, after it fell 4.7% on a monthly basis to an annual rate of 1127.0K, hurt by Hurricanes Harvey and Irma that disrupted the construction of single-family homes in the South. Housing starts had registered a revised reading of 1183.0K in the previous month, while markets were anticipating for a drop to a level of 1175.0K. Additionally, the nation's building permits plunged 4.5% MoM to an annual rate of 1215.0K in September, while investors had envisaged for a fall to a level of 1245.0K and after registering a revised level of 1272.0K in the prior month.

Other economic data showed that the nation's MBA mortgage applications rebounded 3.6% in the week ended 13 October 2017, after recording a drop of 2.1% in the prior week.

Separately, the Fed's Beige Book report indicated that the pace of US economic growth was “split between modest-to-moderate range”, with some regions experiencing major disruptions from hurricanes. However, it revealed that wage growth remained stubbornly low despite “widespread” labour shortages and few indications of a pick-up in price pressures.

In the Asian session, at GMT0300, the pair is trading at 1.1797, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1746, and a fall through could take it to the next support level of 1.1694. The pair is expected to find its first resistance at 1.1833, and a rise through could take it to the next resistance level of 1.1868.

In absence of any macroeconomic releases in the Euro-zone today, investors will focus on the US initial jobless claims followed by leading indicators data for September, due to release later today.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s ILO Unemployment Rate Remained Steady At Its Lowest Since 1975 In The Three Months To August

For the 24 hours to 23:00 GMT, the GBP rose 0.13% against the USD and closed at 1.3209, after data showed that Britain's ILO unemployment rate remained steady at a 42-year low level of 4.3% in the three months to August, meeting market expectations.

Further, the nation's average earnings including bonus rose more-than-anticipated by 2.2% on an annual basis in the June-August period, compared to a revised similar rise in the May-July period. Markets had anticipated average earnings including bonus to gain 2.1%.

In the Asian session, at GMT0300, the pair is trading at 1.3204, with the GBP trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.3153, and a fall through could take it to the next support level of 1.3102. The pair is expected to find its first resistance at 1.3242, and a rise through could take it to the next resistance level of 1.3280.

Trading trend in the Pound today is expected to be determined by the release of UK's retail sales data for September, slated to release in a few hours.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.