Sample Category Title

USD/CHF Erased The Morning Gains

The rate plunged after the United States data were sent to the public and has erased the earlier gains. USD/CHF is trading in the red and is pressuring a dynamic support after the false breakout above a dynamic resistance. Remains to see what will happen till the end of the day because the rate may squeeze a little after the impressive drop.

Unfortunately, the greenback has taken a hit from the United States data, which has disappointed in the afternoon, failing to come in line with expectations.

The US Retail Sales have increased only by 1.6% in September versus a 0.1% drop in August, less versus the 1.7% estimate, while the Core Retail Sales surged by 1.0%, more versus the 0.9% estimate and versus the 0.5% growth in the former reading period. Moreover, the CPI increased only by 0.5%, less compared to the 0.6% estimate, the Core CPI disappointed as well because has increased only by 0.1%, less versus the 0.2% estimate.

You can see that the rate failed to stay above the UML and now is pressuring the WL2 of the former ascending pitchfork. I've said in the previous reports that the rate could come down to retest the second warning line (WL2) after the false breakout above the median line (ml) of the ascending pitchfork and above the 0.9787 static resistance.

Only a valid breakdown below the WL2 will confirm a further drop in the upcoming period, while a rejection will signal a potential bullish momentum.

EUR/JPY Rising Wedge To Be Confirmed

The EUR/JPY dropped and resumed the yesterday's minor drop. You can see that is the rate is pressuring the downside line of the Rising Wedge and looks determined to breakdown from this chart pattern. I've said that a valid breakdown from this pattern will signal another leg lower in the upcoming period, the first downside target will be at the upper median line (UML) of the major ascending pitchfork.

EUR/CHF Losing Altitude

EUR/CHF decreased after a little today, but looks undecided at this moment. The bulls seem exhausted and could lose significant territory in the upcoming days. I've said in the previous report that a rejection from the WL5 and from the upper median line (uml) will send the rate tumbling. A minor drop is expected if will really fail to close on the mentioned resistance levels.

USD Weakens after Consumer Inflation Report

Volatility rose today after the release of the consumer price index in the US, according to which inflation increased by 0.5% in September, which is 0.1% more than in August, but 0.1% less compared to the forecast. Core CPI increased by only 0.1% against the expected 0.2%. Slower than expected inflation growth reduces the possibility of the interest rate increase anticipated in December. Retail sales data in the US also disappointed investors. The indicator increased by 1.6% in September versus the 1.7% predicted, but this figure was much higher than the decline in August of 0.1%. Hurricanes Irma and Harvey are the likely causes to the disappointing data reports from the US.

The price of the American crude oil benchmark is correcting downwards after a confident increase. Yesterday the WTI bulls were cheered by news on the reduction of inventories in the US by 2.7 million barrels against 1.9 million barrels expected. The growth potential however is limited due to the increase of oil production in OPEC countries. Volatility is likely to remain high today because of the data release by Baker Hughes on active drilling rigs count in America. Rising activity in shale oil production remains the key factor in putting pressure on oil prices.

The aussie is rising against the US dollar on the background of the greenback's depreciation. This managed to offset any negative impact from China's disappointing trade surplus which fell to 28.5 billion dollars in September against the 42.0 billion dollars in August. Remember that China is the major trading partner of Australia so key indicators in China often affect the AUD.

EUR/USD

The EUR/USD price is growing rapidly after it was unable to fix below the 1.1825 mark. The next target in case of maintaining the current positive momentum will be 1.1925. Breaking through this level will open the way to 1.2000. In order to change the current ascending trend, quotes need to break through the support at 1.1800. Crossing the zero point by the MACD signal line may be judged as a stimulus for continued growth.

USD/WTI

The WTI quotes have rolled back after they were unable to overcome resistance at 51.65. The next target in case of decline will be the psychologically important 50.00 mark. On the other hand, gaining a foothold above 51.65 may become a trigger for the bulls to push the price higher up to 52.80. Volatility is likely to be elevated today.

AUD/USD

The AUD/USD demonstrated a confident rising movement and broke through the resistance at 0.7870. This is the basis for maintaining the current positive momentum and immediate goals will be located at 0.8000 and above it. The RSI on the 15-minute chart is in the overbought territory, indicating a possible pullback to 0.7870.

Weekly Focus: Surfing the Strong Global Business Cycle

Market Movers ahead

- In the US, industrial production for September is due out. The first two months of Q3 have been on the weak side.

- Bank of England Governor Mark Carney, Deputy Governor Sir David Ramsden and MPC member Silvana Tenreyro are due to testify before the UK's Treasury Committee on Tuesday. We will look for any hints on whether they have changed their minds on a November hike.

- It will be an interesting week in China, as the 19th Congress of the Communist Party begins on Wednesday. On the data front, we look for a small decline in GDP growth.

- In Denmark and Sweden, employment data releases for September are due out.

Global macro and market themes

- Global central bankers have been busy on the news wires. However, new research indicates that the accuracy of forecasting of financial and macroeconomic variables has not improved.

- The market will focus on what 'QE path' the ECB will choose on 26 October when the bulk of its decisions regarding the future of the QE programme are due to be disclosed.

- It seems that two 'paths' are on the table: either an extension for six months of EUR40bn a month in purchases or purchases for nine or 12 months of just EUR20-30bn a month.

- We believe for now in the first 'path' but acknowledge that the purchase constraints that make it increasingly difficult for the ECB to buy according to the 'Capital Key' makes a 'longer' but smaller monthly amount 'path' more likely.

Dollar Takes a Breath as Consumer Prices Disappoint; Aussie, Kiwi Gain the Most

While market watchers expected today's US inflation report to give a clearer picture of the inflation path amid concerns whether subdued inflation is temporary or persistent, uncertainties over the direction of inflation increased after US consumer prices disappointed analysts, reducing the odds for a third rate hike before the end of the year.

The widely-expected data on US consumer prices fell short of expectations in September, with the headline CPI index growing at 0.5% m/m, while analysts anticipated the figure to rise by 0.2 percentage points to 0.6%. This was the highest growth posted since February and emerged mainly due to rising gasoline prices. On a yearly basis, the index increased by 2.2% below the 2.3% expected but above the 1.9% seen in August. Excluding volatile items, consumer prices rose by 0.1% instead of remaining steady at 0.2% as was projected. This maintained the yearly measure at 1.7% versus the forecast of 1.8%.

In a separate report, US retail sales experienced the highest growth since November 2011, expanding by 1.6% m/m but missing slightly the forecast of 1.7%. In the previous month, retail spending contracted by 0.1% which was upwardly revised from -0.2%. The core equivalent gauge, which leaves automobiles aside, surprised to the upside, increasing by 0.5 percentage points to 1.0% m/m while projections were for a slower growth at 0.3%.

The dollar fell sharply to 92.78 against its major counterparts, falling back to two-week low levels reached yesterday. Dollar/yen declined by 0.43% to a two-week low of 111.67.

Speaking in Luxemburg, the President of the European Commission, Jean-Claude Junker said that new problems around Brexit emerge "day after day", prolonging the process by more than initially thought. Moreover, he claimed that he cannot find for the time being a compromise as far as the UK's financial obligations are concerned and therefore he cannot suggest for the negotiations to move to the next stage at the EU summit on October 26. Late on Thursday, a report by the German newspaper Handelsblatt stating that the EU Brexit negotiator Michel Barnier wants to offer a 2-year transition period to the UK to stay in the EU under some conditions gave a boost to the pound. However, following Junker's comments, the pound retreated to an intra-day low of $1.3246 before it bounced back to 1.3318 in the wake of the US data.

The euro stood tall against the weakening dollar at 1.1873, recouping earlier losses. The ECB's plans to start tapering its bond-buying program next year, according to sources with a knowledge, did little for the common currency. In particular, the ECB policymakers are said to announce in a couple of weeks that they will halve their current monthly asset purchases of 60 billion euros in January and will keep the program active at least for nine months. The question, however, remains on whether the ECB policymakers will close the program next September or will continue with it perhaps for some time. In response to the above, the German 10-year bond yields dropped to 0.40%, the lowest level reached in two-weeks. Besides that, the German Economy Ministry said on Friday that the German economy will continue growing in the second semester but at a slower pace compared to the first semester.

The aussie and the kiwi were the biggest winners against the greenback during the European session. The former was in track to post a green candle for the fourth consecutive day, surging by almost 1% to a two-week high of $0.7896, while the latter hit a nine-day high of $0.7195, being up by 0.86% on the day despite political uncertainties in New Zealand.

In commodities, oil prices retreated before the session-end but managed to remain up by 1.35% as data out of China's General Administration of Customs showed on Friday that Chinese crude oil imports jumped by 9% m/m in September, while oil products imported declined by 15.8% m/m. WTI crude retreated to $51.27 per barrel and Brent slipped to $57.01.

Gold advanced by 0.40% to $1,3000 per ounce on the back of a weaker dollar.

Dollar Faces Uphill Battle on Soft US CPI Data

- European equities are slightly lower and US ones open slightly higher, as EUR/USD moves higher.

- A spike in energy prices in the aftermath of Hurricane Harvey boosted the US cost of living by the most since January (0.5% M/M & 2.2% Y/Y vs 0.6% M/M 2.3% Y/Y consensus), while inflation excluding food and fuel stabilized at 1.7% Y/Y (vs 1.8% Y/Y forecast).

- US retail sales jumped last month by the most in more than two years (1.6% M/M) as motor vehicles lost to hurricanes were quickly replaced and higher prices lifted receipts at gasoline stations. Core retail sales rose by 0.5% M/M. Both were close to expectations, but August figures were upwardly revised.

- EU Commission chairman Juncker has warned Brexit will take longer than the UK government thinks, calling on Westminster to pay if it wants to accelerate talks to its future relationship. He said there was no agreement over the UK's exit bill which would stop negotiations from moving on to trade talks before next week's EU Summit.

- The Bank of England should hold off raising interest rates as Britain's economy shows little sign of encouraging growth, the British Chambers of Commerce argued.

- Bank of America has reported a 13% rise in quarterly profits, as growth in consumer banking and wealth management offset a sharp decline in bond trading revenues. Wells Fargo is still counting the cost of the sham account scandal more than a year since it erupted as it reported a decline in revenues and profits.

- Hungary's base interest rate will stay unchanged at 0.9% until at least 2020, central bank deputy governor Nagy said, adding that downward risks to inflation had increased. The National Bank of Hungary, the most dovish in central Europe, cut its overnight deposit rate in September and announced more steps to ease monetary conditions.

Rates

Core bonds profit from slightly disappointing US CPI

Global core bonds gained ground today, boosted by ECB rumours, slightly disappointing US eco data and political risk ahead of the weekend. At the time of writing, US yields decline by 1.2 bps (2-yr) to 2.7 bps (10-yr). German yields shift 1.2 bps (2-yr) to 3 bps (10-yr) lower. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are nearly unchanged with Portugal underperforming (+3 bps).

Bunds opened the session on a positive note, but soon reached a temporary high, before turning sideways till the US economic releases. We suspect some technical inter-market positioning was behind the move as also in other markets some moves occurred simultaneous. However, news agencies referred it to an article based on ECB sources. The ECB would consider cutting the monthly bond buying by half (to €30 bn) and keep the programme active for at least nine months. It isn't obvious to us why that should push the Bund higher. The €30 bn looks lower than markets expectations (negative), while the 9 month is probably a bit longer than expected (positive). Of course, if (forward guidance on) rates are the key driver, then the 9 months extension may have more weight than the €30 bn pace and push back rate expectations. The rise of the bund and the decline of the euro make sense along the lines of that reasoning. At the same time, ECB Hansson, admittedly a super-hawk, suggested according to a news agency that the ECB could tweak it guidance on rates and even raise them before the bond-buying stops. The main move of today's session occurred during US dealings, after slightly disappointing CPI data. While headline inflation rose by 0.5% M/M and 2.2% Y/Y, it was slightly below expectations. Core CPI stabilized at 1.7% Y/Y while consensus expected a small acceleration. Retail sales were strong, but close too forecasts. Core bonds surged higher, in line with this week's performance (downside exhausted after last week's payrolls). Geopolitical risk drew some safe haven flows as well (eg. US Iran nuclear deal).

Currencies

Dollar faces uphill battle on soft US CPI data

Early this morning, FX markets faced a technical repositioning with EUR/USD, USD/JPY and EUR/USD pushed lower. However, calm returned soon as investors awaited the US CPI and retail sales data. Retails sales were strong, but inflation was slightly softer than expected. The latter proved to be the more important factor for (FX) markets, putting the dollar under pressure. EUR/USD rebounded off the low 1.18 area and trades currently around 1.1870. USD/JPY dropped below 112 (currently 111.75).

Overnight, Asian equities mostly extended the established uptrend. Chinese trade data were OK, suggesting good activity and supporting positive sentiment in the region. There was again a 'disconnect' between rising Japanese equities and USD/JPY. The latter struggled not to fall below 112 even as the Nikkei surpassed 21K. The dollar also lost a few ticks against euro. EUR/USD traded in the 1.1845 area.

There was some nervous repositioning in several major cross rates at the start of European trading. We didn't see a clear explanation. Core yields, especially German ones, declined. USD/JPY dropped below 112. The decline spilled over into EUR/JPY and even put downward pressure on EUR/USD. The pair dropped to the 1.1815 area. However, this 'stop-loss' repositioning soon petered out as there was no further guidance from interest rate markets or equities.

US investors eagerly awaited key US CPI and retail sales data. (Core) retail sales were marginally stronger than expected. The CPI was slightly softer than consensus with the headline CPI rising from 1.9% Y/Y to 2.2% Y/Y (2.3% Y/Y expected) and core inflation stable at 1.7% Y/Y (1.8 Y/Y expected). The dollar hesitated upon the publication of the data, but the small miss in inflation finally prevailed. US yields declined and so did the dollar. EUR/USD rebounded off the low 1.18 area, reached just before the US data release. The pair trades currently in the 1.1870 area. So a return below the 1.1800/23 support area is unlikely, which is disappointing for USD bulls. USD/JPY is also drifting below the 112 big figure. Lower interest rates outweigh positive equities. USD/JPY trades in the 111.75 area. A further decline below the 111.50 area would deteriorate the short-term picture in this cross rate.

Hope on 'EU concession' supports sterling

Yesterday's roller-coaster ride of sterling finally turned out in favour of the UK currency. Sterling initially sold off as EU Barnier said that the negotiations on a divorce bill ended in a stalemate. However, sterling reversed initially losses on rumours/comments that the EU would consider to start preparations for a transition period.

(FX) markets saw the glass half full rather than half empty this morning on headlines that the EU would consider a transition period, something the UK is aiming for. EUR/GBP dropped below the 0.89 barrier. Enthusiasm eased later in the session on comments from Germany and EU's Juncker who highlighted that the Brexit process remains extremely difficult. EUR/GBP rebounded (temporary?) back above 0.89. In the end, sterling maintained yesterday's rebound. Will sterling enter calmer waters, awaiting new signs from next week's EU summit? EUR/GBP trades in the 0.8910 area. Cable extended gains north of 1.33, partially due to USD weakness after the 'soft' US inflation.

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9755

USD/CHF - 0.9734

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9739

Kijun-Sen level : 0.9739

Ichimoku cloud top : 0.9745

Ichimoku cloud bottom : 0.9735

Original strategy :

Sold at 0.9755, Target: 0.9655, Stop: 0.9775

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9775

New strategy :

Hold short entered at 0.9755, Target: 0.9655, Stop: 0.9775

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9775

As the greenback met renewed selling interest at 0.9772 and has slipped today, retaining our bearish view that the decline from 0.9837 top has resumed and downside bias remains for this move to extend weakness to 0.9669-70 (61.8% Fibonacci retracement of 0.9565-0.9837 and previous support) but previous support at 0.9642 should remain intact due to oversold condition, bring rebound later.

In view of this, we are holding on to our short position entered at 0.9755. Above said resistance at 0.9772 would defer but only break of resistance at 0.9808 would signal low is formed and indicate the pullback from 0.9837 has ended, bring retest of this level later.

Trade Idea Wrap-up: GBP/USD – Hold long entered at 1.3250

GBP/USD - 1.3300

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3293

Kijun-Sen level : 1.3238

Ichimoku cloud top : 1.3193

Ichimoku cloud bottom : 1.3193

Original strategy :

Bought at 1.3250, Target: 1.3350, Stop: 1.3245

Position : - Long at 1.3250

Target : - 1.3350

Stop : - 1.3245

New strategy :

Hold long entered at 1.3250, Target: 1.3350, Stop: 1.3245

Position : - Long at 1.3250

Target : - 1.3350

Stop : - 1.3245

As the British pound found renewed buying interest at 1.3121 yesterday and has rallied, suggesting the rise from 1.3027 low is still in progress, hence consolidation with upside bias is seen for this move to bring a stronger retracement of recent decline, hence gain to 1.3345-50 would be seen, however, near term overbought condition should limit upside to 1.3375-80 (61.8% Fibonacci retracement of 1.3596-1.3027) and 1.3400 should hold from here.

In view of this, we are holding on to our long position entered at 1.3250. Below 1.3245 would defer and risk test of the Kijun-Sen (now at 1.3223), break there would defer and suggest an intra-day top is formed, bring weakness to 1.3200, then towards 1.3175 but said support at 1.3121 should remain intact.

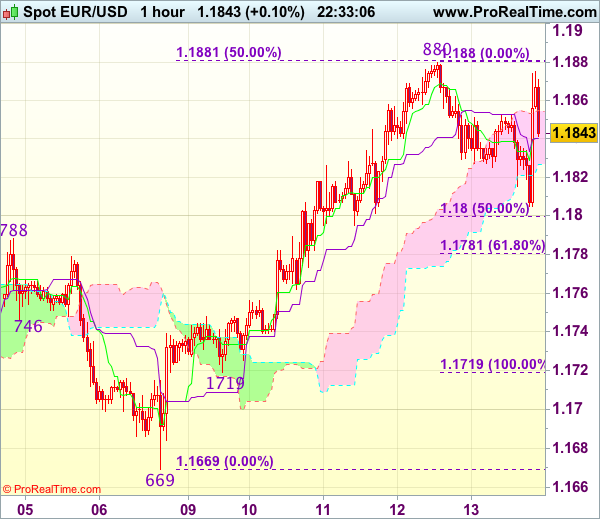

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1843

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1840

Kijun-Sen level : 1.1840

Ichimoku cloud top : 1.1855

Ichimoku cloud bottom : 1.1827

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency found renewed buying interest at 1.1805 (just missed our long entry) and has staged a strong rebound in NY morning, suggesting the pullback from 1.1880 (this week’s high) has possibly ended there and consolidation with upside bias is seen, however, break of said resistance at 1.1880 is needed to confirm recent upmove from 1.1669 low has resumed for headway to 1.1895-00 (61.8% Fibonacci retracement of 1.2035-1.1669) first.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Only below minor support at 1.1795 would defer and risk correction to 1.1770 but downside should be limited to 1.1745-50 and price should stay above indicated support at 1.1719, bring another rise later.