Sample Category Title

Market Update – Asian Session: Asian Equity Markets Opened Mixed Again Before Turning Positive

Asia Summary

Asian equity markets opened mixed again before turning positive, the Nikkei 225 is heading for its highest close since December 1996, thought the yen remained slightly weaker; the upward trend in equities being attributed to more solid economic and market conditions. Uncertainty around the upcoming Japan election and the ramifications of BOJ Gov Kuroda losing his position if PM Abe is not re-elected have started to circulate in the press. Currencies on the whole were little changed in the session, with little economic data to give direction.

China MOF to offer $2B in 5 and 10-year sovereign bonds in Hong Kong, this is the 1st dollar bond offering since 2004, and will compromise of $1B in 5-year bonds and $1B in 10-year bonds. There is speculation that the bonds could be sold at the end of October. The offshore yuan fell for the first time in four sessions amid speculation that traders are squaring up positions amid recent performance and ahead of China’s 19th congress next week. China property names fell after a press report citing China National Development and Reform Commission (NDRC) official that China was developing property measures that would have long lasting effects.

Key economic data

(AU) Australia Sept Westpac Consumer Conf Index: 101.4 v 97.9 prior; m/m: 3.6% v 2.5% prior

(JP) JAPAN AUG CORE MACHINE ORDERS M/M: 3.4% V 1.0%E; Y/Y: 4.4% V 0.7%E

Speakers and Press

China/Hong Kong

(HK) Hong Kong Chief Exec Lam: Sees 2017 GDP higher than 3.5%

(CN) China National Development and Reform Commission (NDRC) deputy chief Ning Jizhe: China is formulating a set of property control measures that will have long-lasting effects, and will unveil the measures at an appropriate time - Xinhua

Japan

(JP) Financial press comments on future of BOJ Gov Kuroda may depend on PM Abe's re-election

US

(US) Fed's Kaplan (moderate, voter): will be assessing the progress of the US economy toward full employment and looking for more signs of upward inflation as while weighing potential interest-rate hikes

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.3%, Hang Seng -0.0%; Shanghai Composite +0.3%; ASX200 +0.6%, Kospi +0.8%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.0%; FTSE100 +0.0%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1828-1.1795; JPY 112.58-112.22; AUD 0.7809-0.7777;NZD 0.7098-0.7069

Dec Gold -0.3% at $1,289/oz; Nov Crude Oil +0.3% at $51.09/brl; Dec Copper -0.1% at $3.06/lb

(AU) Australia buys backs A$900M v A$900M indicated in 2018 (avg yield 1.7925%) and 2019 bonds (avg yield 1.9492%)

(AU) Australia sells A$3.5B (record amount) v A$3.5B indicated in Nov 2022 bonds, bid to cover 3.68x, avg yield 2.4167%

(CN) China MOF to offer $2B in 5 and 10-year sovereign bonds in Hong Kong

USD/CNY (CN) China PBOC sets yuan reference rate at 6.5841 v 6.6273 prior

(CN) China PBOC injects CNY20B v CNY40B in 7-day reverse repos prior, injections match maturities for 2nd consecutive day

(KR) Bank of Korea (BOK) sells KRW2.77T v KRW2.8T indicated in 2-yr monetary stabilization bonds; avg yield 1.85% v 1.73% prior

(CN) China MOF sells 1-yr and 10-yr bonds

(JP) Japan MoF sells ¥643B v ¥800B indicated in 0.80% (0.8% prior) 30-yr bonds; Avg yield: 0.8810% v 0.8320% prior; Bid to cover: 3.98x v 3.67x prior

Equities notable movers

Australia/New Zealand

LHC.AU Acquires rights to promote spinal allograft biologics range from Australian Biotechnologies for A$3.3M; +5.5%

PEB.NZ Announces NZ$21.3M capital raise through a fully underwritten 1 for 6 pro-rata Rights Offer; -16.5%

Japan

5406.JP Follow Up: Says reports about iron powder data are 'true'; founder falsified information for 1 product, no safety issues; -16%

8136.JP Cuts FY17/18 guidance Net ¥4.8B from ¥7.6B; Op ¥6.3B from ¥10.8B; Rev ¥60.3B from ¥65.7B; cuts dividend to ¥55 from ¥80; -9.3%

Korea

069620.KR To expand production of botulinum toxin, named “Nabota”, at new plant in Hwaseong city, South Korea following govt approval; +12%

China/Hong Kong

2333.HK Reports Sept sales 102K units, +4.5% y/y; production 97.8K units, +0.2% y/y; +15%

Europe Seen Higher As Catalonia Seeks Talks With Madrid

European equity markets are expected to open a little higher on Wednesday, with Spain’s IBEX a strong outperformer after Catalan leader Carles Puigdemont adopted a softer stance on independence on Tuesday.

While Puigdemont remained clear that they had been given a mandate for independence by the Catalan people, his call for talks in order to find a peaceful resolution was the much preferred option at this stage. A declaration of independence on Tuesday could have led to a chain of events that made the situation much worse and seen Puigdemont arrested, likely leading to more unrest.

It’s now over to Madrid to decide how it is going to handle the situation, starting with whether it will agree to hold talks with the Catalan leadership on the issue. Outside mediation has been rejected by numerous officials including French President Emmanuel Macron who claimed Madrid can handle the situation. While a softer approach has boosted markets in the near-term is a positive, there remains a strong chance that the situation deteriorates quickly again if Madrid rejects talks and the Catalans are backed into a corner and forced to declare, an outcome that doesn’t seem entirely unlikely given Madrid’s handling of the situation so far.

Developments in Spain are likely to remain the key focal point from a European perspective this morning in the absence of any notable scheduled economic events. The week as a whole is going to be a little quiet on this front, with the only notable event being ECB President Mario Draghi’s appearance at the World Bank and IMF event in Washington on Thursday.

The US is also in for a quieter week when it comes to economic data but with third quarter earnings season getting underway – including results from Delta and Blackrock today and JP Morgan and Citigroup tomorrow – there should be no shortage of newsflow.

The release of the FOMC minutes this evening is today’s key event, with traders looking for further insight into the Fed’s interest rate plans. The dot plot from the last meeting made it clear that another rate hike this year and three more next year is still expected from within the committee but remarks since then from individuals not being overly convincing and a new Chair possibly taking over early next year, a huge amount of uncertainty remains.

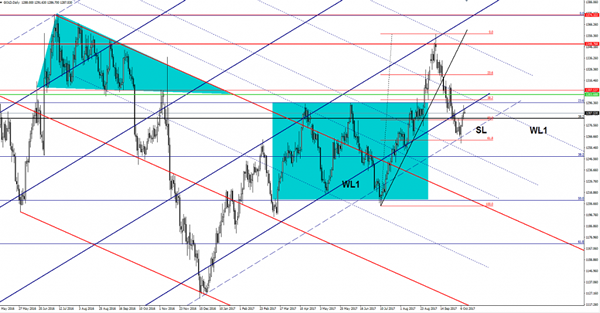

Elliott Wave View: FTSE

FTSE Short term Elliott Wave analysis suggests the decline to 7196.58 on 9/15 low ended Primary wave ((4)). The Index is currently within Primary wave ((5)) which is subdivided as a zigzag Elliott Wave structure. The first leg Intermediate wave (A) of this zigzag is in progress as 5 waves impulse where Minor wave 1 ended at 7327.50 and Minor wave 2 ended at 7289.75. Up from there, Minor wave 3 ended at 7527.59 and Minor wave 4 ended at 7493.68. The Index has broken above Minor wave 3 at 7527.59, suggesting that it’s in the final Minor wave 5 higher which should also complete Intermediate wave (A).

Cycle from 9/15 low is mature and Intermediate wave (A) could end soon. Once Intermediate wave (A) is complete, Index should pullback in Intermediate wave (B) in 3, 7, or 11 swing to correct cycle from 9/15 low (7196.58) before the rally resumes. We do not like selling the proposed pullback. As far as pivot at 9/15 low stays intact in the Intermediate wave (B) pullback later, expect Index to extend to a new high.

FTSE 1 Hour Elliott Wave Chart

Zigzag is a common type of corrective structure. It’s a 3 waves corrective structure labelled as ABC. Wave A has an internal subdivision of 5 waves and can be either an impulse or a diagonal. Wave B can be any corrective structure. Finally, wave C also has internal subdivision of 5 waves and also can be either an impulse or a diagonal. Zigzag therefore is a 5-3-5 Elliott Wave structure. Wave C typically ends at 100% – 123.6% of wave A.

Gold Shows Exhaustion Signs

Gold made a false breakout above the first warning line (WL1) of the ascending pitchfork and now could drop again. Price failed to close right on the WL, signaling that the bears could take control again. It could come down to test and retest the long term 38.2% retracement level. I want to remind you that only a drop below the sliding parallel line (SL) will confirm a larger drop in the upcoming weeks.

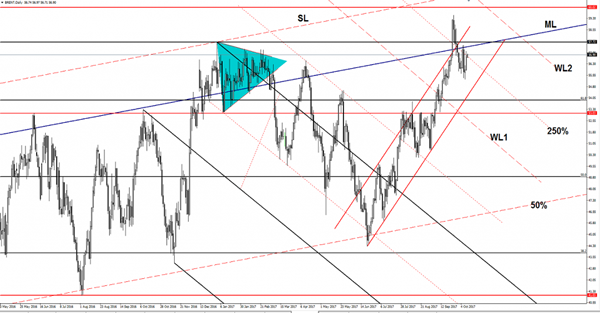

Brent Oil Another Retest Expected

Brent increased in the yesterday's session and climbed above the 250% Fibonacci line (descending dotted line), but failed to close above it. Now is trading in the green and tries to climb towards the median line (ML) of the major ascending pitchfork where he may find resistance again. Technically, it should drop sharply as long as is trading below the ML, only a breakout above this dynamic obstacle and above the 57.72 level will announce an increase at least till will reach the 59.50 previous high.

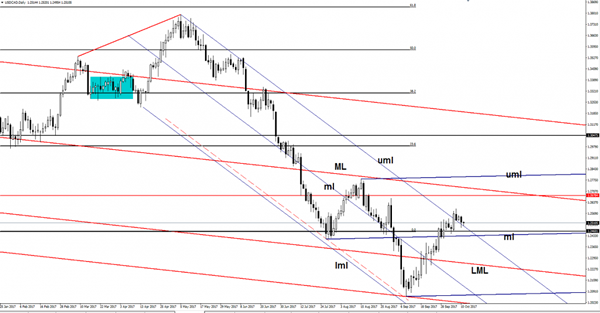

USD/CAD Still In The Buyers Territory

The USD/CAD decreased little today and stays much above the 1.2483 yesterday's low. Price has come down to retest a broken resistance level and now is somehow expected to climb much higher on the short term. However, the rate could drop much deeper to test and retest some important support levels before will start another upside momentum.

Right now is very important to see what will happen on the USDX, which is located right above a critical support, a drop somewhere below the 93.30 level will signal a further drop and a USD depreciation.

Technically, the price should increase again, but unfortunately, the fundamental factors will take the lead and will drive the price. We may have a high volatility tonight after the FOMC Minutes will be released, a disappointment will demolish the USD.

USD/CAD retested the upper median line (uml) of the minor descending pitchfork and now should increase again. It could still drop along the upper median line (uml) till will reach and retest the 1.2460 static support and the median line (ml) of the blue ascending pitchfork. The next upside targets are at the median line (ML) of the major descending pitchfork and at the 1.2678 horizontal resistance.

Only a drop within the descending pitchfork's body will signal a broader drop in the upcoming period, this scenario will take shape if the traders will be disappointed by a dovish FED.

Euro Higher On Easing Political Uncertainty, US Dollar Dips On Tax Reform Doubts

Tax Reform Doubts Weigh on Dollar. The U.S. dollar wobbled against its peers on Wednesday and edged further away from a 10-week high scaled recently amid speculation that the U.S. tax overhaul plan introduced by President Donald Trump would stall, with a buoyant euro adding further pressure on the greenback. Fed uncertainty also continues to weigh on the currency. Despite last week’s U.S. dollar rally on the back of some stellar ISM economic data, there was far from a consensus buy-in on the move as Fed Chair uncertainties continued to dominate traders psyche. After all, it took little more than a baseless

North Korea headline to send the dollar reeling. While the market continues to look to Fridays CPI for some guidance, there’s increasing chatter that the street will ignore the print being more concerned with the next Fed Chair.

Euro Hovered Near 10-Day Peak after Catalonia’s Leader Speech. The Euro popped 30 pips on Catalan President Puigdemont parliament speech where he called for deferred independence, a friendly way of extending talks with the Spanish government and hopefully agree how to prevent a future separation. Spanish banks stocked up on European Central Bank money at a weekly auction on Tuesday, fearing jitters on the funding market if Catalonia breaks away from Spain.

Gold Gains on Weaker Dollar. Gold rose for a fourth day on Wednesday, after hitting a near two-week high in the previous session, supported by weakness in the U.S. dollar. Spot gold jumped to $1,294 an ounce, the highest level since Sept. 27.

Oil Up on Signs of Tighter Market. Oil prices edged up on Wednesday, extending 2 percent gains recorded the previous day, on signs that markets are gradually tightening after years of oversupply, although the outlook for 2018 remained less certain. U.S. WTI crude futures were trading at $51.07 per barrel, up 0.3 percent from their last settlement, Brent crude futures were at $56.71, up 0.2 percent from their last close. Traders said they would look to the U.S. fuel inventory data on Wednesday and Thursday for indicators on price direction.

Watch Out Today for:

14:00 pm GMT: USD FOMC Minutes

Market Morning Briefing: Aussie Has Some Chances Of Testing 0.77 On The Downside

STOCKS

Dow (22830.68, +0.31%) could face rejection from resistance zone of 22800-22850 levels and could possibly see a corrective dip in the next few sessions. Only on a break above 22850, we would look at higher levels of 23000.

Dax (12949.25, -0.21%) is trading below important resistance near 13000-13035 levels and while that holds, the index could either trade sideways below 13000 or come off sharply towards 12900-12850 in the near term. Directional view remains bearish for the coming sessions.

Nikkei (20878.13, +0.26%) is up sharply and is ready to test crucial long term resistance near 21000 in the coming sessions. A sharp correction from 21000 is the preferred scenario.

Shanghai (3387.31, +0.13%) has bounced well from 3360, also the 21-day MA, contrary to our expectation of a test of 3325. While above 3360, the price could rise towards 3400-3425 levels in the near term.

10000 is a good near term support for the Nifty (10016.95, +0.28%) and while the index trades above this support, there could be chances of seeing an up move towards 10100 soon. Only on a fall below 10000, we would negate the chances of an immediate upside.

COMMODITIES

Gold (1287.70) has dipped slightly. A test of 1280 is possible in the coming sessions before again rising back towards 1290-1295. Gold is likely to remain trapped in the 1280-1300 region for at least the next 4-5 sessions.

Silver (17.11) has immediate resistance near 17.25 and while that holds, price could come off slightly towards 17.00-16.80 in the near term.

Brent (56.67) and WTI (51.05) have both bounced from support levels as expected and are trading higher today. While above 56.65, Brent has scope of rising towards 57.45 and WTI could rise to 52 before seeing another down leg. Near term looks bullish.

Copper (3.0545) rose back again above 3.05 maybe due to a rise in the Chinese stocks. While the price sustains above 3.05, we could see a test if 3.10 or even higher in the near term.

FOREX

Dollar Index (93.33) is trading lower as expected but could be trapped in the 93-94 levels for the next 2-sessions. Euro (1.1803) also moved up to test 1.1825 as expected but could see a small dip to 1.1750 again in the near term. Trade within 1.1730-1.1850 is possible in the coming sessions.

Dollar Yen (112.465) is stuck and trades narrow in the 113.25-112.00 region. As mentioned yesterday, the sideways consolidation may continue for some more time. Thereafter a fall below 112 seems more likely.

Pound (1.3194) could test 1.3250-1.3300 on the upside while above 1.3100.

Aussie (0.7780) has some chances of testing 0.77 on the downside but at the same time prices are attempting a rise towards 0.7850 too. Overall near term trade within 0.7850-0.77 is possible.

Dollar Rupee (65.29) closed at slightly lower levels yesterday after making an intra day low of 65.19. Our initial target of 65.00 remain on the cards for the near term.

INTEREST RATES

The US yields are trading low as expected. The 5Yr (1.95%), 10Yr (2.35%) and the 30Yr (2.89%) could be stable or move down to 1.90%, 2.30% and 2.80% respectively in the near term. The 30YR seems to be stable compared to the 10YR and the 5Yr which are vulnerable to a further fall in the next few sessions.

The US-Japan 10YR (2.28%) is headed downwards and could test 2.20% on the downside which could possibly pull down Dollar Yen to lower levels in the near term or at least keep the currency pair stable.

The German-US 2YR (-2.21%) and the German-US 10YR (-1.90%) seem to have bounced from support levels and look bullish in the near term. This could be a boost for Euro and indicative of Euro strength in the medium term.

Tax Reform Doubts Weigh On The Dollar

Tax Reform doubts weigh on the Dollar

Tax Reform

Tax reform doubts are weighing on the greenback all but reversing out last weeks gains. Concerns appear to be based in the Senate due to the paper thin majority the Republicans hold(52-48) as reports surface that Marc Short, Trump's legislative affairs director, “is increasingly worried that one Senator could derail the Administration's tax plan. Rand Paul, who helped to kill health reform, could be “a no on everything” ( politico). If the grandstanders in the parties right-wing follow Rand Paul lead, Tax Reform will most certainly struggle to pass.

Once again the Tump administration is caught in a Catch 22 of their own devices. By wooing the anti-establishment vote at the hight of the populist fervour, they've created political monsters from those senators who rode the tea-party wave into power that now stand prepared to veto any reform unless it meets and ultra-right agenda.

And when you factor in Trump's escalating feud with Senator Bob Corker, the math is starting to look a bit a tad shaky.

Fed Uncertainty

Fed uncertainty continues to weigh on both the currency and bond markets as the ten-year US bond yields are unable to breach the 2.40 mark. Despite last weeks USD dollar rally on the back of some stellar ISM economic data, there was far from a consensus buy-in on the move as Fed Chair uncertainties continued to dominate traders psyche.After all, it took little more than a baseless North Korea headline to send the dollar reeling.

While the market continues to look to Fridays CPI for some guidance, there's increasing chatter that the street will ignore the print being more concerned with the next Fed Chair.

For what its worth, oddsmakers are shading Powell as the most likely candidate versus Warsh, roughly 40%-30%. Some in the Powell camp feel further vindicated by his latest headline: Powell has cancelled a Friday speech entitled “Are Rules Made to be Broken? Discretion and Monetary Policy.”. The suggestion is that by removing this controversial headlined statement, setting the stage for an open vetting process.

Catalan

The big event of the day was Catalan President Puigdemont parliament speech where he called for deferred independence. A friendly way of extending talks with the Spanish government and hopefully agree how to prevent a future separation. The EUR popped 30 pips on the speech but gained little traction as this is little more than kicking the can down the road. It's unlikely we've heard the last of this debate despite cooler heads prevailing.

Chinese Yuan

Eyes will be on the CNY fix this morning as the Pboc guides the Yuan to an appreciating path of stability ahead of a critical national leadership meeting next week. Also, there were some significant positions unwound which are suspected to be exporter driven Again exporters suffer the consequences of hoarding dollar, and there's no question that in my view the Pboc is hell-bent on creating two-way currency flows the RMB complex

EM Asia FX

Not too surprisingly Asia EM FX is looking a lot brighter today.

Tax reform issues are lead with around the greenback neck, US treasury yields are broadly lower, and Catalan risk has efficiently been rolled over to a future date, so investor appeal for both riskier assets and currencies has tentatively materialised.

The Korean Won has been on a tear as investors play catch up in equity markets after a week-long holiday.

Finally, there has been minimal fallout from this week's Turkish tumult, while tensions remain high there was minimal regional contagion.

USD/CAD Canadian Dollar Higher Despite Disappointing Housing Data

The Canadian Dollar rose against the US dollar on Tuesday after markets in the two countries came back from holidays. The loonie got a boost from higher oil prices after the Organization of the Petroleum Exporting Countries (OPEC) continues to signal a willingness to extend its production cut agreement with other major producers and plans to cut Saudi exports in November.

The Canadian dollar has appreciated versus the US dollar by 7.42 percent so far in 2017. The CAD is trading near the 80 cent price level but was close to the 70 cent level earlier in the year. The loonie strength can be explained by the following factors: a stable oil price, strong economic growth and an ineffectual Trump administration.

West Texas oil prices have been trading in a range of $43 to $53 after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers have extended the production cut agreement. The supply restrictions have been offset by higher production levels in Brazil, Canada and the United States. Higher global demand for energy remains elusive and until then there is will be the push and pull between OPEC and US producers.

The Canadian economy leads economic growth in the Group of Seven. The International Monetary Fund (IMF) just updated gross domestic product (GDP) forecast to record a 3 percent gain in 2017. The Bank of Canada (BoC) hiked interest rates twice in 2017 to deal with the unexpected improvement in the economy after it said monetary policy stimulus was no longer needed. A third rate hike remains a possibility but is less likely as the momentum of the economy is showing signs of slowing down in the third quarter. The highest point of the year for the Canadian currency was after a surprise rate hike announcement in September when it traded at 82 cents. The ball now is on the hands of the U.S. Federal Reserve with a heavily anticipated December US interest rate hike that would again wide the gap with Canadian rates.

The greenback started 2017 on a tear with Donald Trump ready to unleash tax reform and infrastructure spending to achieve higher growth. Things have not worked out that way with immigration and healthcare reforms pushed ahead of the more market friendly initiatives. The focus on divisive policies has cost the current US administration substantial political capital as just now it gears up to attempt to pass the much awaited tax reforms. The North American Free Trade Agreement (NAFTA) renegotiation will also ramp up in the final months of the year as both Mexico and the United States wish to avoid it spilling over to 2018 as they both have elections in that year. The US remains a difficult partner to negotiate specially with the commander in chief openly dismissing the treaty. Talks so far have been less than productive, but there are some positive signs although by now it is almost a given that the process will not be speedy as the position of the US remains far from that of its partners.

The beginning of the year painted a picture where the loonie would be touching 60 cents, but steady oil prices, sound growth in Canada and an uncertain political climate in the US have pushed the currency closer to 90 cents. It will be difficult for the Canadian dollar to reach that levels without a third rate hike or a satisfactory renegotiation of NAFTA but the flip side is that only the Fed is actively boosting the US dollar, while the White House sometimes does more harm that good.

The USD/CAD lost 0.28 percent during the Tuesday session. The currency pair is trading at 1.2516 after opening higher in Asia at 1.2555. The return of North American trading resulted in a sell off of US dollar that benefited the loonie. The rise in oil prices and the uncertainty about US political reforms got the pair under 1.25 only to end the session at current levels.

Housing data released on Tuesday is still showing a slowdown in the sector. Housing starts fell to 217,118 but still beat expectations of a fall below 210,000. Building permits also cooled down with a 5.5 percent decrease in August.

The Bank of Canada (BoC) Deputy Governor Carolyn Wilkins spoke at an International Monetary Fund (IMF) panel in Washington. She said that household debt is one vulnerability of the Canadian economy that the bank is taking close attention. The BoC does not seem concerned with the financial system as the big banks are well capitalized, but a shock in prices could impact Canadian families. The central bank has hiked twice in 2017 as it deemed the economy did not need the stimulus it provided with the two rate cuts in 2015 on the eve of the drop in oil prices.

New house prices will be the next big economic release in Canada with a forecast of 0.3 percent gain as the real estate prices have fallen after regulation and higher rates. The Canadian economy got a vote of confidence today as the IMF improved its forecast for the end of the year, but there is no denying that the pace of growth has slowed down and is still too vulnerable to a major shock like the NAFTA deal being scrapped by the Trump administration.

Market events to watch this week:

Wednesday, October 11

2:00pm USD FOMC Meeting Minutes

Thursday, October 12

8:30am USD PPI m/m

8:30am USD Unemployment Claims

10:15am EUR ECB President Draghi Speaks

11:00am USD Crude Oil Inventories

Friday, October 13

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m